“Life is precarious, and life is precious. Don’t presume you will have it tomorrow, and don’t waste it today.” – John Piper.

Jobs Update

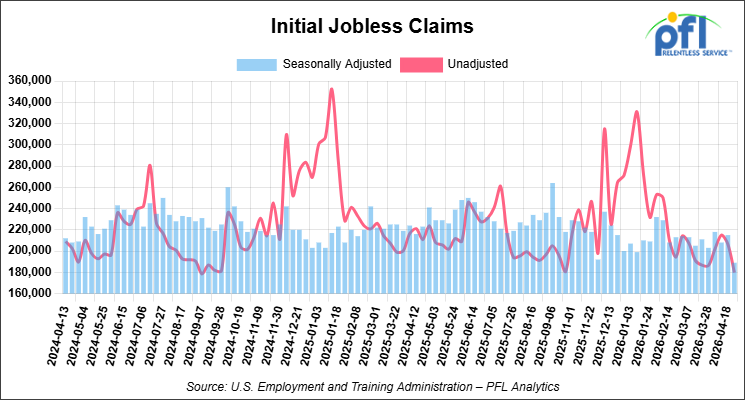

- Initial jobless claims seasonally adjusted for the week ending April 25, 2026 came in at 189,000, versus the adjusted number of 215,000 people from the week prior, down 26,000 people week over week.

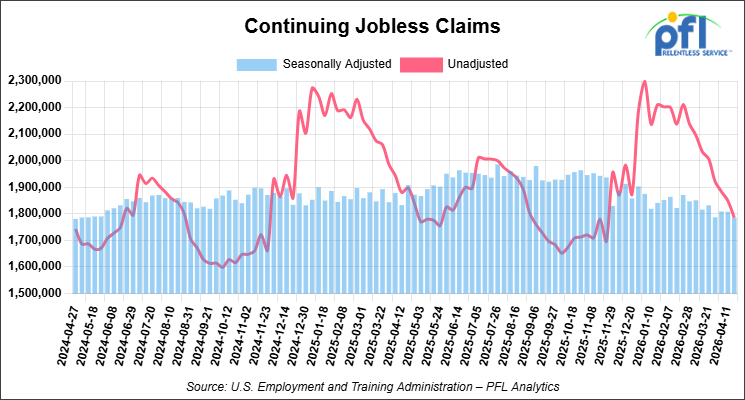

- Continuing jobless claims came in at 1,785,000, versus the adjusted number of 1,808,000 people from the week prior, down 23,000 week-over-week.

Stocks closed mixed on Friday of last week and higher week-over-week

The DOW closed lower on Friday of last week, down -152.87 points (-0.31%), closing out the week at 49,499.27, up 268.56 points week-over-week. The S&P 500 closed higher on Friday of last week, up 21.11 points (0.29%), and closed out the week at 7,230.12, up 65.04 points week-over-week. The NASDAQ closed higher on Friday of last week, up 222.13 points (0.89%), and closed out the week at 25,114.44, up 277.84 points week-over-week.

In overnight trading, DOW futures traded lower and are expected to open at 49,395 this morning, down -251 points from Friday’s close.

Crude oil closed lower on Friday of last week, but higher week-over-week

West Texas Intermediate (WTI) crude closed down -$3.13 per barrel (-3%), to close at $101.94 on Friday of last week, but up $7.54 per barrel week-over-week. Brent crude closed down -$2.33 per barrel (-2%), to close at $108.17 per barrel, but up $2.84 per barrel week-over-week.

One Exchange WCS (Western Canadian Select) for June delivery settled on Friday of last week at US$15.60 below the WTI-CMA (West Texas Intermediate – Calendar Month Average). The implied value was US$81.65 per barrel.

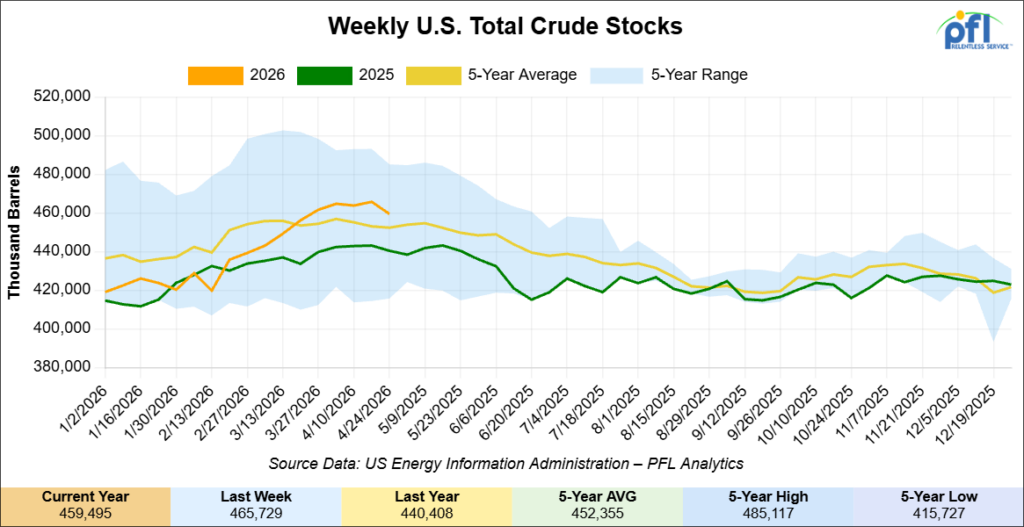

U.S. commercial crude oil inventories (excluding those in the Strategic Petroleum Reserve) decreased by 6.2 million barrels week-over-week. At 459.5 million barrels, U.S. crude oil inventories are 1% above the five-year average for this time of year.

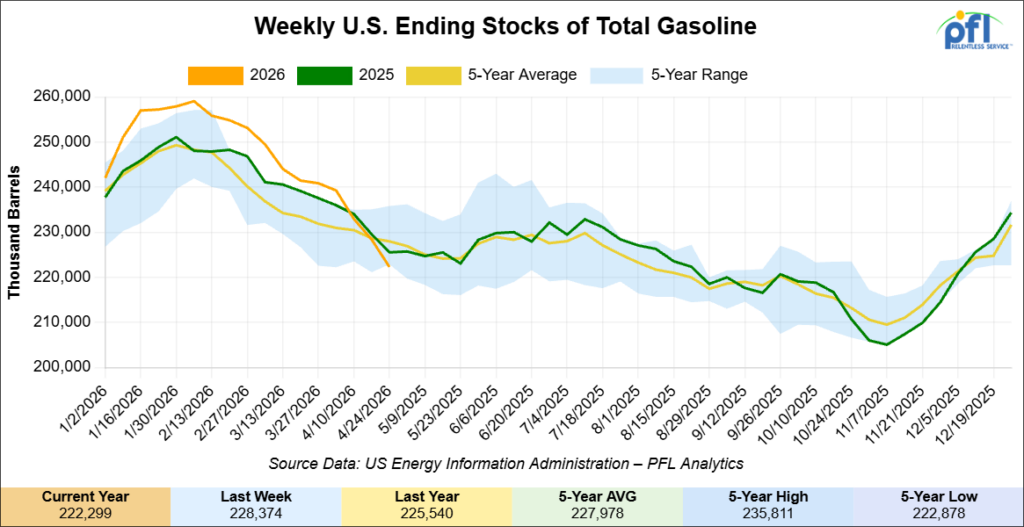

Total motor gasoline inventories decreased by 6.1 million barrels week-over-week and are 2% below the five-year average for this time of year.

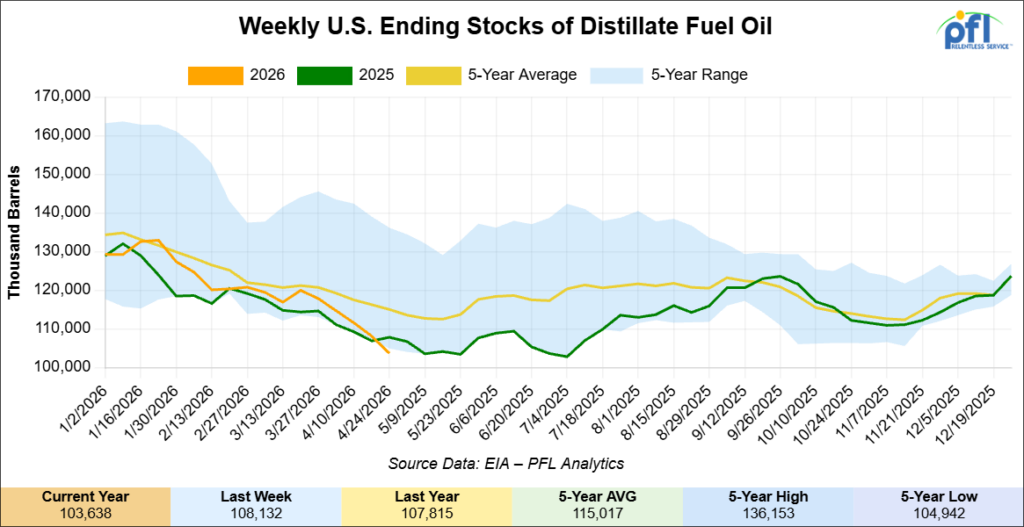

Distillate fuel inventories decreased by 4.5 million barrels week-over-week and are 11% below the five-year average for this time of year.

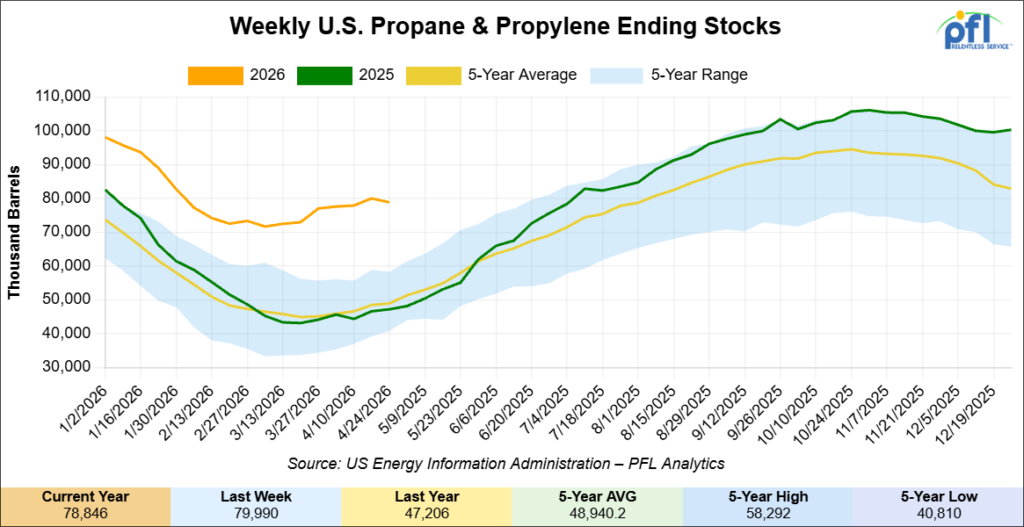

Propane/propylene inventories decreased by 1.1 million barrels week-over-week and are 62% above the five-year average for this time of year.

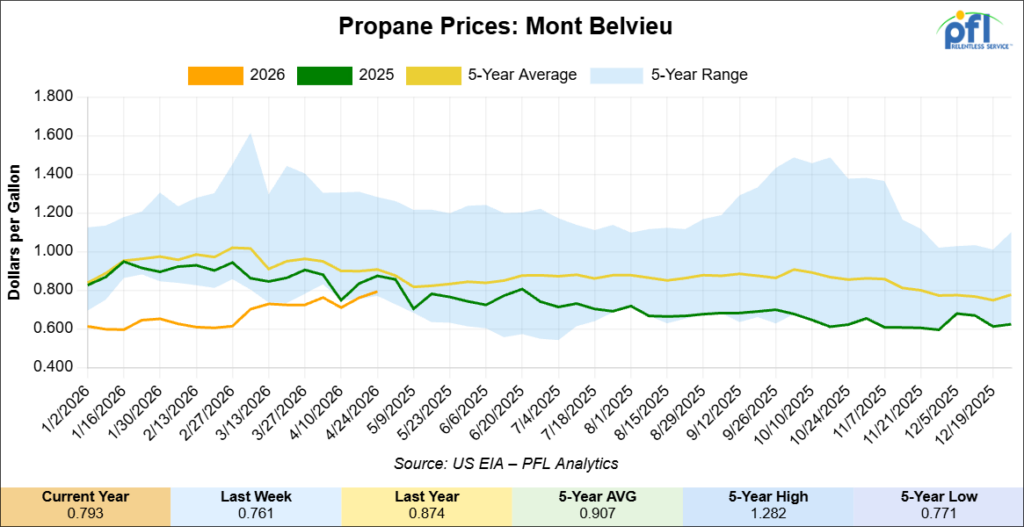

Propane prices closed at 79.3 cents per gallon on Friday of last week, up 3.2 cents per gallon week-over-week, but down 6.3 cents year-over-year.

Overall, total commercial petroleum inventories decreased by 17.0 million barrels week-over-week during the week ending April 24, 2026.

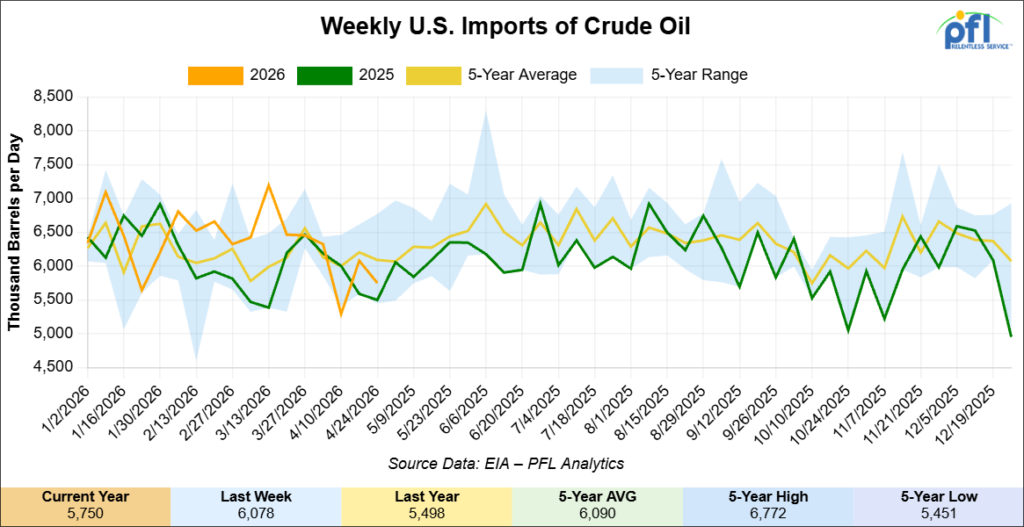

U.S. crude oil imports averaged 5.8 million barrels per day during the week ending April 24, 2026, a decrease of 329,000 barrels per day week-over-week. Over the past four weeks, crude oil imports averaged 5.9 million barrels per day, 0.7% more than the same four-week period last year. Total motor gasoline imports (including both finished gasoline and gasoline blending components) averaged 344,000 barrels per day, and distillate fuel imports averaged 126,000 barrels per day during the week ending April 24, 2026.

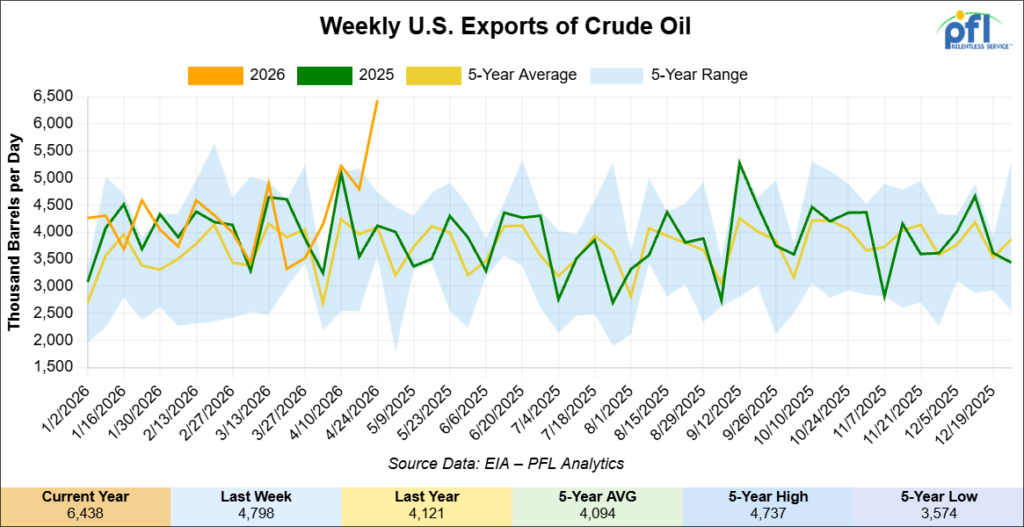

U.S. crude oil exports averaged 6.438 million barrels per day during the week ending April 30, 2026, an increase of 1.640 million barrels per day week-over-week. Over the past four weeks, crude oil exports averaged 5.153 million barrels per day.

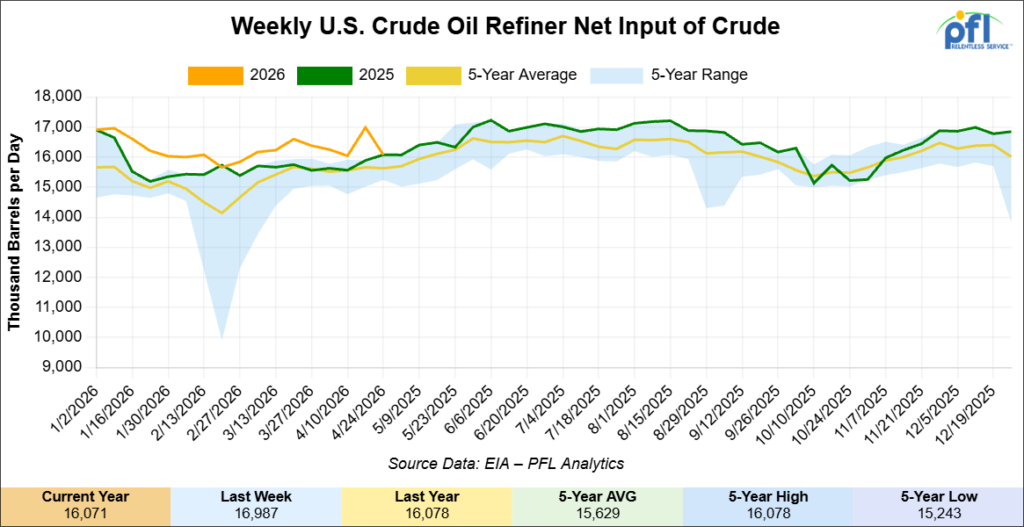

U.S. crude oil refinery inputs averaged 16.1 million barrels per day during the week ending April 24, 2026, which was 85,000 barrels per day more week-over-week.

WTI is poised to open at $105.79, up $3.85 per barrel from Friday’s close.

North American Rail Traffic

Week Ending April 29, 2026:

Total North American weekly rail volumes were up (+1.38%) in week 18, compared with the same week last year. Total Carloads for the week ending April 29, 2026 were 338,550, up (+0.03%) compared with the same week in 2025, while weekly Intermodal volume was 339,419, up (+2.77%) year over year. 6 of the AAR’s 11 major traffic categories posted year-over-year increases. The largest decrease came from Forest Products (-15.01%). The largest increase was Motor Vehicles and Parts (+14.90%).

In the East, CSX’s total volumes were up (+5.87%), with the largest decrease coming from Metallic Ores and Metals (-16.84%), while the largest increase came from Other (+17.58%). NS’s total volumes were up (+5.91%), with the largest increase coming from Petroleum & Petroleum Products (+22.57%), while the largest decrease came from Forest Products (-9.66%).

In the West, BNSF’s total volumes were up (+3.98%), with the largest increase coming from Motor Vehicles and Parts (+12.59%), while the largest decrease came from Other (-12.54%). UP’s total volumes were down (-0.55%), with the largest increase coming from Motor Vehicles and Parts (+26.72%), while the largest decrease came from Coal (-22.78%).

In Canada, CN’s total volumes were down (-5.71%), with the largest increase coming from Motor Vehicles and Parts (+37.01%), while the largest decrease came from Intermodal Units (-16.80%). CPKCS’s total volumes were down (-23.68%), with the largest increase coming from Nonmetallic Minerals (+20.95%), while the largest decrease came from Forest Products (-67.01%).

Source Data: AAR – PFL Analytics

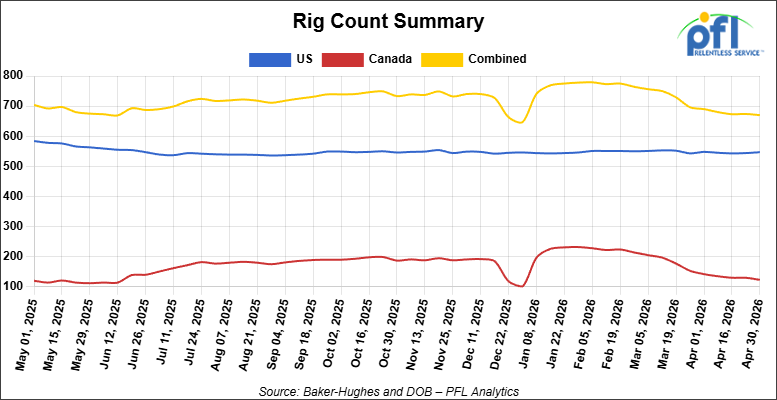

North American Rig Count Summary

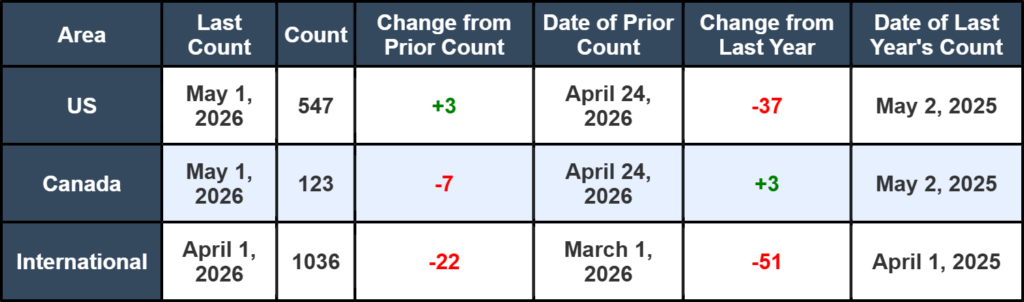

North American rig count was down by -4 rigs week-over-week. U.S. rig count was up by +3 rigs week-over-week, but down by -37 rigs year-over-year. The U.S. currently has 547 active rigs. Canada’s rig count was down by -7 rigs week-over-week but up by +3 rigs year-over-year. Canada currently has 123 active rigs. Overall, year-over-year we are down by -34 rigs collectively.

International rig count which is reported monthly was down by -22 rigs month-over-month and down by -51 rigs year-over-year. Internationally there are 1036 active rigs.

We are watching a few things out there for you:

We Are Watching the UP and NS

Union Pacific and Norfolk Southern submitted their amended $85 billion merger application to the Surface Transportation Board on Thursday of last week, four months after the board rejected the initial December filing as incomplete. The revised application runs more than 7,000 pages and is the first in rail merger history to use 100% actual traffic data from all six North American Class Is rather than STB sample data. The STB now has 30 days to determine whether the filing is complete; comments on completeness are due May 8th. UP CEO Jim Vena said the deeper analysis reinforces the public-benefit case. NS President, Mark George, framed it as being fundamentally about growth.

UP and NS are projecting 2.1 million trucks diverted from highway to rail and roughly $3.5 billion per year in shipper cost savings if the merger goes through. The amended filing also commits the railroads to divest control of the Terminal Railroad Association of St. Louis, the 170-mile short line where UP holds 42.84% and NS holds 14.29%. The TRRA divestment is structured to address concerns the original filing did not adequately handle competitive access in St. Louis.

The day before the filing, BNSF and CPKC went public with the Stop the Rail Merger Coalition alongside the American Chemistry Council, the American Farm Bureau Federation, the Teamsters Rail Conference, the Alliance for Chemical Distribution, the National Industrial Transportation League, and the Vinyl Institute. A McLaughlin & Associates poll commissioned by the coalition found 71% of Americans oppose the merger after learning about its impacts and 68% believe the merged carrier would keep the cost savings rather than pass them through. CN’s response to the refile was sharper than the field, calling the failure to remedy competitive harms “fatal” to the application and noting that the areas of overlap are more extensive than the applicants identify. BNSF CEO, Katie Farmer, was direct in calling it a Wall Street deal rather than a customer-driven one.

For the tank car market, the merger is now in its substantive review phase. Comment windows open over the next several months, and a substantive STB decision is unlikely before late 2027. Anyone running long-tail equipment commitments through corridors that touch the Eastern half of the network needs to be modeling both outcomes.

We are Watching Petroleum Carloads

The four-week rolling average of petroleum carloads carried on the six largest North American railroads fell to 28,934 from 29,171 which was a decrease of -237 rail cars week-over-week. Canadian volumes were lower. CN’s shipments were lower by -4.0% week-over-week, CPKC’s volumes were lower by -5.0% week-over-week. U.S. shipments were mostly lower. The UP had the largest percentage decrease and was down by -5.0%. The NS was the sole gainer and was up by +2.0% week-over-week.

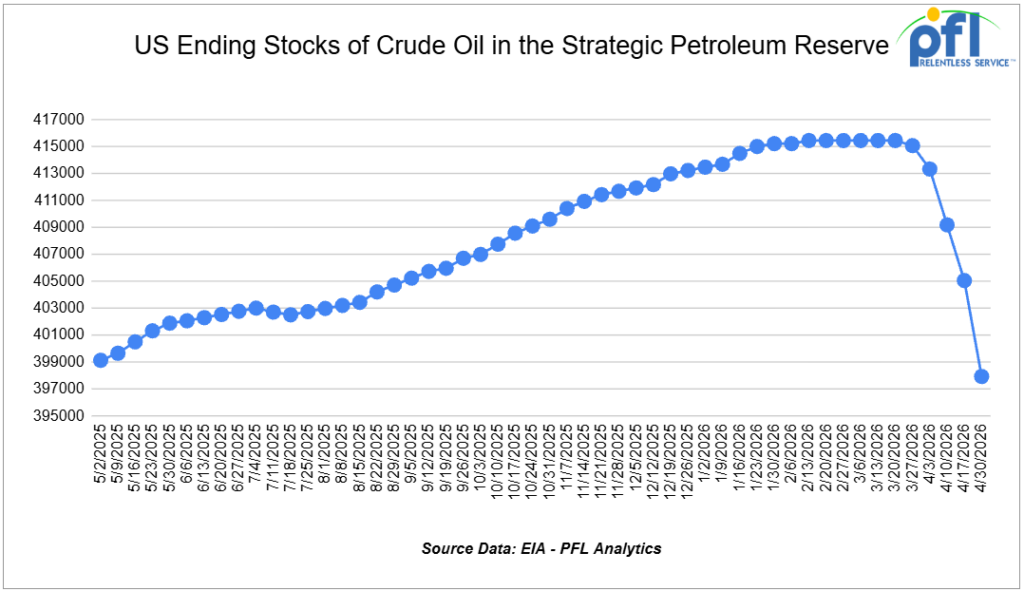

We Are Watching Our Strategic Petroleum Reserves

On Thursday of last week The U.S. Department of Energy (DOE) issued a Request for Proposal (RFP) for an emergency exchange of up to 92.5-million-barrels of crude oil from the Strategic Petroleum Reserve (SPR). The solicitation opens competitive bidding, continuing DOE’s execution of President Trump’s swift 172-million-barrel release as part of a coordinated 400-million-barrel action by International Energy Agency (IEA) member nations’ strategic reserves.

In a press release “Under President Trump’s leadership, the Department has executed a historic, record-speed series of SPR exchange solicitations—the largest in the Reserve’s 50-year history, moving critical crude oil supplies quickly to market to address short-term oil flow disruptions and strengthen energy security for the United States and its allies.”

The crude oil will originate from the SPR’s Bayou Choctaw, Bryan Mound, Big Hill, and West Hackberry sites. This action builds on the Department’s three previous emergency exchange RFPs, which together quickly awarded approximately 80 million barrels across two completed exchanges. DOE’s earlier exchanges demonstrated the SPR’s ability to rapidly deliver crude oil under emergency authorities while securing a 24 percent premium in returned crude oil barrels—growing the reserve at no cost to American taxpayers.

Under DOE’s exchange authority, participating companies will return the borrowed 92.5-million-barrels of crude with additional premium barrels, ensuring the SPR grows beyond current levels while delivering immediate supply to refiners and global oil markets. Bids under the New Exchange are due today at 11:00 AM CST. Bottom line – we are pulling hard from storage right now, folks, see below:

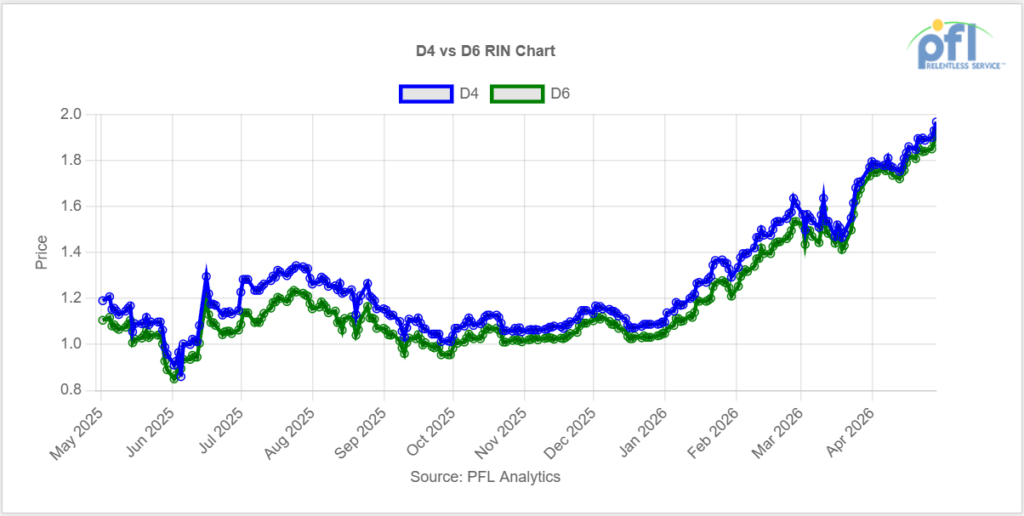

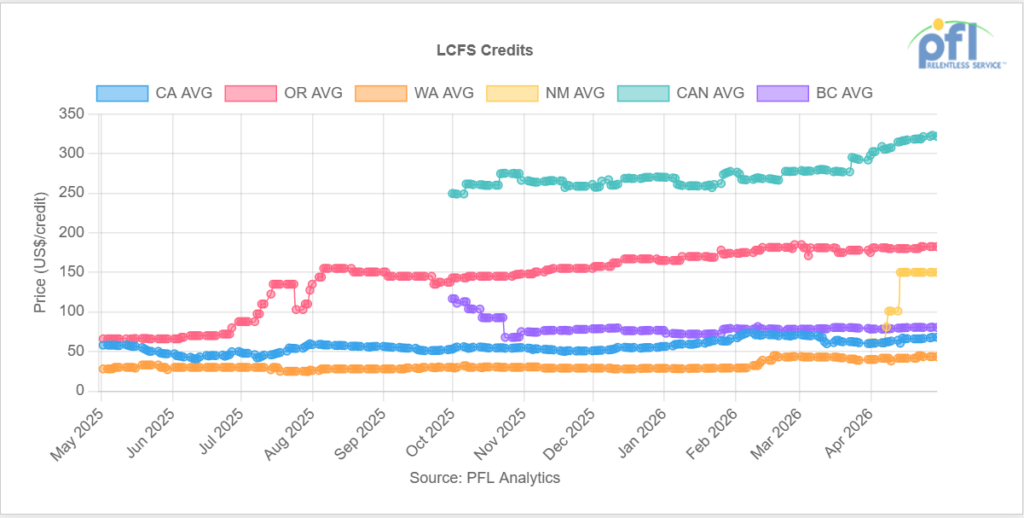

We Are Watching California

The poor people of California are getting whacked right now due to bad left wing State policies. The price of RIN’s and LCFS credits have soared and have added costs to what are already high gasoline and diesel prices at the pump.

On Friday of last week, LCFS credits in California closed at $69.50 per MT, up $3.00 per MT week-over-week. D4 RIN’s closed at $2.00 per RIN, up 11 cents per RIN week-over-week. D6 RINs closed at $1.97 per RIN, up 13 cents per RIN week-over-week.

In addition, California lost 17% of their refining capacity over the past year with Phillips 66 closure of its 139,000 barrel per day Los Angeles refinery and Valero’s 145,000 barrel per day closure of its Benicia complex. Bottom line for California is that they are importing 129,000 barrels per day of gasoline alone and paying significant premiums to get the product to market as countries are rationing refined fuels in the wake of the ongoing conflict in the middle east.

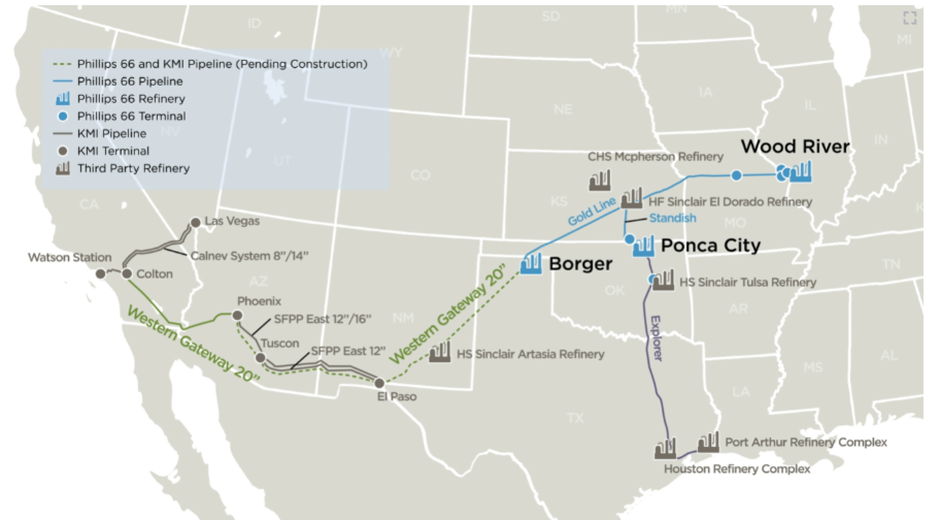

On April 20th, Phillips 66 and Kinder Morgan announced the advancement of the Western Gateway Pipeline (Western Gateway), a proposed refined products pipeline system, following a successful second open season that secured long-term shipper commitments sufficient to move the project forward, subject to the execution of definitive transportation service agreements, joint venture agreements, and respective board approvals.

The Western Gateway will connect Midwest and Gulf Coast refinery supply to Phoenix, Arizona and California markets with connectivity to Las Vegas, Nevada via Kinder Morgan’s CALNEV Pipeline. The Western Gateway Pipeline will consist of a new-build pipeline from Borger, Texas to Phoenix, Arizona, combined with Kinder Morgan’s existing SFPP, L.P. pipeline from Colton, California to Phoenix, Arizona, which will be reversed to enable east to west product flows into California. The Western Gateway Pipeline will be fed from Midwest and Gulf Coast supplies connected to Borger, Texas. The Gold Pipeline, operated by Phillips 66, which currently flows from Borger to St. Louis, will be reversed to enable refined products from Midwest and Gulf Coast refineries to flow toward Borger and supply the Western Gateway Pipeline.

The project is targeting an in-service date of mid-2029.

Proposed System Map

Source: Kinder Morgan – PFL Analytics

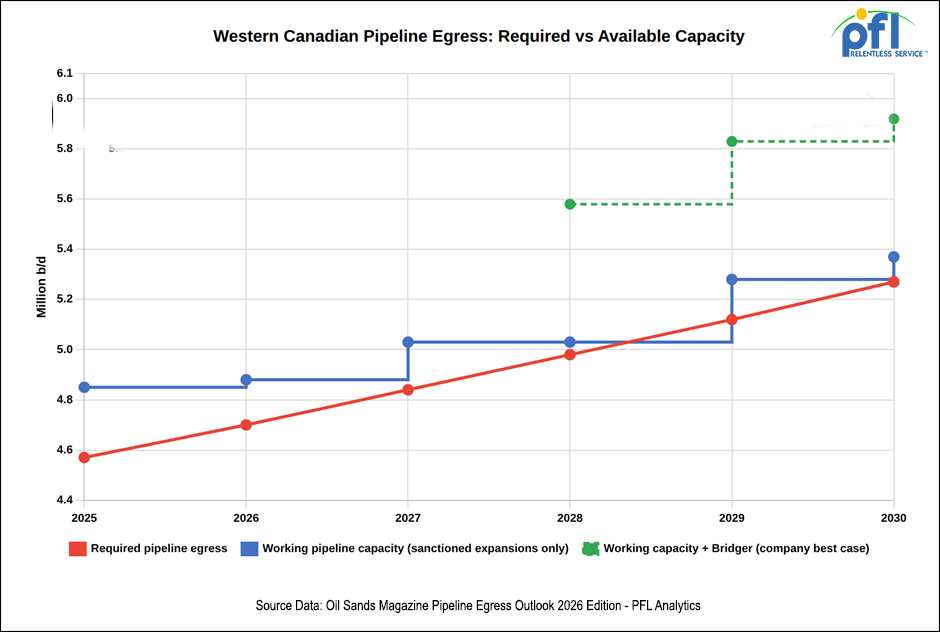

We Are Watching Bridger

Last Thursday President Trump signed the cross-border permit authorizing the Bridger Pipeline / South Bow project we have been tracking, a 647-mile, 36-inch, 550,000 b/d line running from the Canada-US border in Phillips County, Montana to a crude terminal at Guernsey, Wyoming. Bridger is designed to scale to 1.13 million barrels per day with additional pump stations, which would lift Canadian crude exports to the U.S. by more than 12% at full build-out. Bridger executive partner Tad True called the permit one step closer to reality. Alberta Premier Danielle Smith took a victory lap. White House staff secretary Will Scharf called it a long-term energy dominance and security win. Canadian Energy Minister Tim Hodgson framed it the same way.

The permit is a milestone, not a green light. South Bow’s Prairie Connector concept feeds Bridger from Hardisty using existing approved corridors and pipe that has been sitting idle in Alberta and Saskatchewan since Keystone XL was cancelled in 2021. Guernsey is a tank farm rather than an end market, so onward connections to Cushing, Patoka, or the Gulf Coast still need to be built or commercially secured. The BLM scoping period for the federal Environmental Impact Statement closes today, with the final EIS targeted for April 2, 2027 and a final decision by May 31, 2027. Bridger spokesman Bill Salvin has said construction could begin as early as July 2027, if all permits are obtained on schedule, with a 12-to-18-month build pointing to in-service in the second half of 2028 while Trump is still in office.

That is the company’s bull case timeline. Comparable projects have slipped meaningfully against company schedules, with Trans Mountain Expansion taking roughly five years longer than originally planned and Mountain Valley taking six. Bridger also carries the 2015 Yellowstone River spill on its record, the route crosses BLM, USFS, and Army Corps lands, and Indigenous consultation on a project of this scale is rarely fast. A more realistic base case is 2029 or 2030 in-service with material slip risk beyond, which means rail and the existing pipeline grid remain the only egress option for incremental Western Canadian volumes well into the next decade. PFL has been watching this one for years and thought common sense would come to light at some point. It appears it finally has, but the trains are not coming off the rails any time soon. Stay tuned to PFL for further updates.

We Are Watching Left Wing Carney

Two stories on the prime minister last week, both unflattering. First, the Bridger permit. While Trump signed a cross-border permit for a 647-mile Canadian-crude line into Wyoming last Thursday, Ottawa has approved exactly zero new bitumen pipelines on the Canadian side since taking office. The shortest path to market for incremental Alberta bitumen, in the year of the largest oil supply disruption in modern history, runs through Montana because the Carney government has not built one of its own.

Second, the November MOU with Premier Smith continues to slip. The April 1 deadline for the four foundational arrangements came and went without final agreement on the carbon pricing framework or the Oilsands Alliance MOU. Smith has set a July 1 deadline for her own government to submit a West Coast pipeline proposal to the federal Major Projects Office. Even on an accelerated regulatory track, Carney’s two-year review timeline puts in-service for any Alberta pipeline well into the 2030s.

PFL has been tracking the Carney pipeline file since the MOU signing. In our opinion, the Bridger permit signing in Washington while Ottawa is still negotiating with itself tells you everything you need to know about which jurisdiction wants this oil moved and which one does not. Stay tuned to PFL for further updates.

We Are Watching the UAE

The United Arab Emirates exits OPEC effective Friday of last week, ending a 59-year membership. UAE Energy Minister Suhail al-Mazrouei framed it as a need for greater flexibility, but the substance is straightforward: Abu Dhabi has invested heavily to expand upstream capacity well above its OPEC allocation, the quota tensions have been festering for years, and the war in Iran created the political cover to leave. The UAE’s departure removes a meaningful source of spare capacity from the OPEC quota system during the most disruptive supply shock since the 1970’’s.

The departure does not put barrels into the market in the immediate term because Hormuz remains effectively closed. Roughly 12 to 15 million barrels per day of crude, refined products, LPG, and petrochemicals are constrained by the closure, amounting to nearly 500 million barrels of lost hydrocarbon supplies each month. The earliest credible estimate for the strait reopening is July, which does not account for repairs to onshore production and refining damage from the war, and the U..S.. has separately said it will take six months to clear the mines Iran laid in the strait.

The pull on US Gulf Coast barrels has been significant. Enterprise Products Partners reported Q1 crude exports of 866,000 barrels per day, up 18% year-over-year, with the Trump administration’s late-March SPR drawdowns sending roughly 400,000 barrels per day to European buyers across May and June. Enterprise expects Q2 export volumes to push above 1 million barrels per day, and very large gas carrier rates loading in Houston have hit their highest levels since November 2023 on Asian LPG demand replacing lost Mideast Gulf supply. For Canadian and US barrels, the long-tail case for keeping North American rail and export infrastructure available through this window has not weakened.

We Are Watching Shell

Shell announced its $22 billion acquisition of Calgary-based ARC Resources last Monday, the largest Canadian energy deal in years. The deal moves Shell from the seventh-largest Montney producer to the second, adding roughly 1.5 million net acres to its existing 440,000 acres and bringing approximately 2 billion barrels of proved-plus-probable reserves into the portfolio. ARC reported its own Q1 results inside the same week with record production of 418,000 barrels of oil equivalent per day, up 12% year-on-year, with condensate output up 19% to 104,000 barrels per day and natural gas liquids up to 52,000 barrels per day.

The strategic logic runs through Kitimat. Shell is the 40% lead partner in LNG Canada, which started Phase 1 commercial operations last summer. Shell CEO Wael Sawan suggested on Tuesday of last week that a final investment decision on Phase 2 could come by the end of this year, which would effectively double the facility’s 14 million tonne per year nameplate capacity. Qatar’s LNG export capacity remains substantially offline because of the war in Iran, and the Asian premium has shifted decisively in favor of West Coast Canadian supply over U.S. Gulf Coast competitors.

For PFL’s client base, the relevance is in the liquids stream. ARC is Canada’s largest producer of condensate, and Sawan’s view is that Canada will be “short condensate for a long, long time,” with current shortfalls being met by US imports. That structural condensate deficit drives sustained tank car demand for diluent into the Edmonton and Fort Saskatchewan complex, plus the NGL and butane volumes that move from the Montney to fractionation, blending, and U.S, and Asian export markets.

We Are Watching BP

The BP Whiting lockout entered its seventh week with no settlement. The company has continued to run the 440,000 barrel per day Midwest refinery on replacement labor since locking out 800 United Steelworkers Local 7-1 members on March 19. BP says it has tried twice since early April to restart negotiations and has received no formal response from the union. The union maintains BP’s proposal eliminates roughly 100 positions and includes wage reductions across most classifications, framing the lockout as concession bargaining rather than a contract dispute.

The 2015 BP Whiting work stoppage ran 101 days, and the underlying issues this time are harder, so a long-tail outcome is increasingly the base case.

For Midwest refined product flows, the plant is producing but maintenance and capital project work has been deferred. PFL is monitoring the Midwest crude and product flow chain.

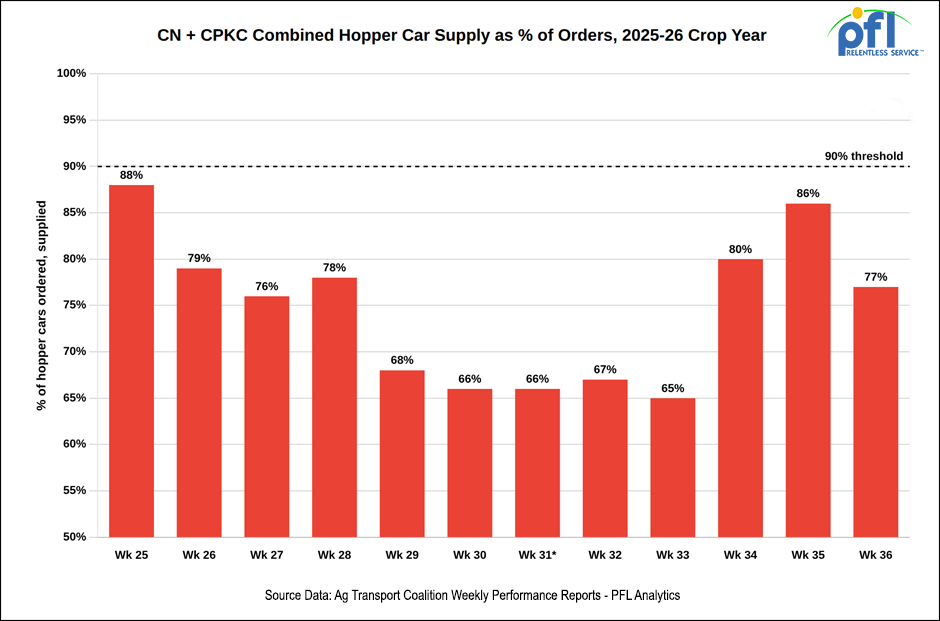

We Are Watching Canadian Grain

The Agriculture Transport Coalition released a hard economic number on rail-driven grain disruption last week as part of its “Too Much on the Line” campaign. A single week of rail and port disruption during peak export season costs Canada’s grain sector up to $540 million, and roughly 94% of that loss comes from missed sales, rather than penalties or added costs. International buyers do not wait. They turn to Australia, the US, and Ukraine, and those sales do not come back.

The damage starts before anyone walks off the job. The analysis found up to $112 million in sales can be lost before a disruption even officially begins, as railways stop accepting new shipments, exporters pull back from commitments, and buyers hedge by sourcing elsewhere the moment a work stoppage looks likely. A one-week shutdown of both CN and CPKC could cost the sector more than $500 million on its own, with port disruptions causing far less damage because nearly all Canadian export grain relies on rail to reach port or market. More than 70% of Canadian grain production is exported, and approximately 94% of those exports move by rail.

The timing of this report is not accidental. Collective agreements covering tens of thousands of Canadian rail workers expire over the next 24 months, and federal labour relations consultations are underway now. The Coalition is pushing for the federal government to appoint a Special Mediator to oversee bargaining and to give the Minister authority to refer disputes to binding arbitration before work stoppages occur, not after. The 2024 dual railway shutdown is still fresh; CN and CPKC both shut down within weeks of each other, costing the sector millions per day until back-to-work legislation passed.

Grain car delivery performance has remained below the 90% threshold for twelve consecutive weeks through week 36 (the week ended April 20), with hopper supply averaging 73% over that stretch and the most recent week at 77%. The system is already running tight without a labor disruption, and the next round of bargaining is the policy lever that determines whether 2026-27 grain movement becomes a structural risk to North American hopper car demand. PFL has clients across the grain hopper fleet and is tracking the consultation process closely.

We are Watching Key Economic Indicators

Consumer Spending

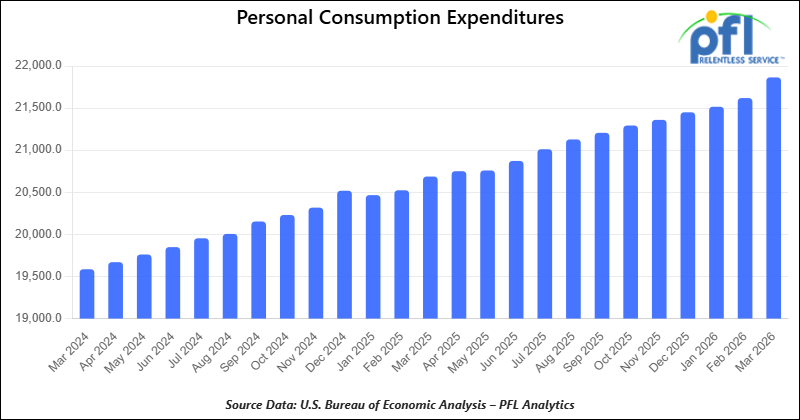

In March 2026, consumer spending strengthened notably, with personal consumption expenditures (PCE) rising 0.9 percent month-over-month. In current-dollar terms, spending increased by approximately $195 billion, with gains across both goods and services, highlighting resilient household demand. On an inflation-adjusted basis, real PCE rose 0.2 percent, indicating modest but positive growth in underlying consumption.

The personal saving rate declined to 3.6 percent in March, suggesting households drew more on savings to support stronger spending.

On inflation, the PCE price index — the Federal Reserve’s preferred gauge — increased 0.7 percent month-over-month in March, pushing the year-over-year rate to 3.5 percent. Core PCE (excluding food and energy) rose 0.3 percent on the month and 3.2 percent year-over-year, indicating that underlying inflation remains elevated and above the Fed’s 2 percent target.

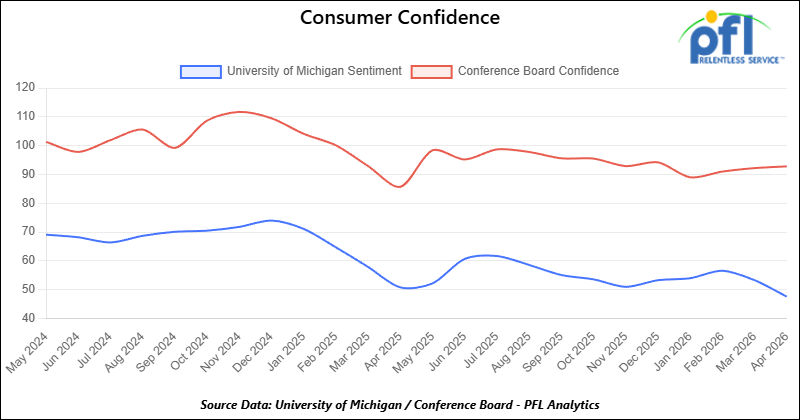

Consumer Confidence

The Index of Consumer Sentiment from the University of Michigan decreased from 53.3 in March to 49.8 in April.

The Conference Board Consumer Confidence Index increased from 92.2 in March to 92.8 in April.

Lease Bids

- 100, 21.9K 117J Tanks located off of All Class 1s in Midwest. For use in CO2 service. Period: 6 months.

- 30-50, 30K 117J Tanks located off of NS or CSX in Northeast. For use in C5 service. Period: 1 year.

- 20-50, 4000-5000 Covered Hoppers located off of UP or BN in Houston. For use in Urea, Potash, Ammonium Sulfate service. Period: 6-12 Months.

- 200, 33K Pressure Tanks located off of CSX or NS in Ohio. For use in Propylene service. Period: 18 Months.

- 30-50, 25.5K DOT 111 Tanks located off of All Class 1s in Anywhere. For use in Asphalt service. Period: 1-3 Years.

- 40, 33K Pressure Tanks located off of UP in Eunice, LA. For use in Propane service. Period: 1 Year.

- 40, 29K DOT 111 Tanks located off of UP or BN in Midwest. For use in Veg Oil service. Period: 5 Year.

- 70, 30K DOT 117 Tanks located off of NS or CSX in Ohio. For use in Diesel service. Period: 3 months.

- 100, 33K Pressure Tanks located off of UP or BN in Texas. For use in Propane service. Period: 6 Months.

- 20, DOT 117J Tanks located off of NS, CSX, CN, or CPKC in Various. For use in C5 service. Period: 1 year. Need gauge rods.

- 50, 30K DOT 117J Tanks located off of CP or CN in Canada. For use in Jet Fuel service. Period: 1 Year.

Sales Bids

- 28, 3400CF Covered Hoppers located off of UP BN in Texas. For use in Cement service. Cement Gates needed.

- 20, 17K DOT111 Tanks located off of various class 1s in various locations. For use in corn syrup service.

- 120, Various Open-Top Aluminum Rotary Gondolas located off of various class 1s in various locations. For use in Sulphur service. Built 2004 or later.

- 30, 29K DOT111 Tanks located off of various class 1s in Chicago. For use in Veg Oil service.

Lease Offers

- 106, 31.8K CPC1232 Tanks located off of UP or BN in Texas. Last used in Diesel.

- 20, 31.8K DOT117R Tanks located off of UP or BN in Texas. Last used in Diesel.

- 86, 29K DOT117R Tanks located off of UP or BN in Texas. Last used in Gasoline. Coiled and Insulated.

- 21, 6351 Covered Hoppers located off of CN in Wisconsin. Last used in DDG. Available until February 2027.

- 29, 6500 Covered Hoppers located off of CN in Wisconsin. Last used in DDG. Available until February 2027.

- 50, 20K DOT117J Tanks located off of All Class 1s in Moving. Last used in Styrene.

- 29, 25.5K DOT117J Tanks located off of UP or BN in Texas. Cars are currently clean. Cars are currently clean.

- 50, 30K DOT117J Tanks located off of UP or BN in Corpus Christie. Last used in Diesel.

- 200, 340W DOT 112J Tanks located off of All Class 1s in Multiple Locations. Last used in Propane and Butane. Cars are currently clean.

- 15, 6200CF Covered Hoppers located off of All Class 1s in Wisconsin. Last used in Plastic. Cars are currently clean.

- 30, 6500CF Covered Hoppers located off of All Class 1s in Wisconsin. Last used in Plastic. Cars are currently clean.

- 24, 21K Stainless Steel Tanks located off of UP in Texas / Mexico Border. Last used in SULFACTANT. Cars are currently clean.

- 34, 30K DOT 111 Tanks located off of UP in Texas / Mexico Border. Last used in Veg Oil. Cars are currently clean.

- 117, 30K DOT117R Tanks located off of UP or BN in Texas. Last used in Gasoline.

- 100, 28.4K DOT 117J Tanks located off of UP or BN in Beaumont, TX. Cars are currently clean.

- 50, 30K DOT117J Tanks located off of UP or BN in the South. Last used in Ethanol.

Sales Offers

- 81, 31.8K CPC1232 Tanks located off of UP or BN in TX. Last used in Multiple. Requal Due in 2025.

- 35, 3400CF Covered Hoppers located off of UP or BN in Midwest. Last used in Sand.

- 25, 30K 117J Tanks located off of CSX in Jackson, TN. Last used in Fuels. Newly Requalified.

Call PFL today to discuss your needs and our availability and market reach. Whether you are looking to lease cars, lease out cars, buy cars, or sell cars call PFL today at 239-390-2885

Live Railcar Markets

| CAT | Type | Capacity | GRL | QTY | LOC | Class | Prev. Use | Offer | Note |

|---|

PFL will be at the Following Conferences

- Where: Calgary

- Attending: David Cohen (954-729-4774), Curtis Chandler(239-405-3365), Cyndi Popov (403-402-5043)

- Where: Grand Geneva Resort

- Attending: Brian Baker (239.297.4519)

- Conference Website

- Where: Loews Arlington Hotel

- Attending: Brian Baker (239.297.4519), David Cohen (954-729-4774), and Curtis Chandler (239-405-3365)

- Conference Website

- Where: The Westin Galleria Dallas

- Attending: David Cohen (954-729-4774), and Curtis Chandler (239-405-3365)

- Conference Website

- Where: The Westin Galleria Dallas

- Attending: Brian Baker (239.297.4519)

- Conference Website