“It is only the farmer who faithfully plants seeds in the Spring, who reaps a harvest in the Autumn.” – B. C. Forbes

Jobs Update

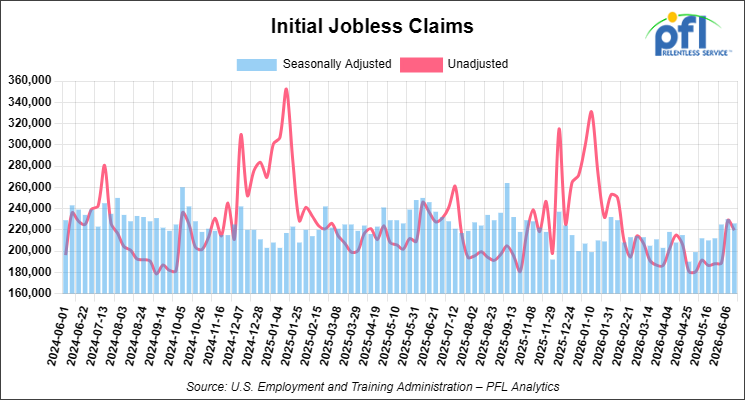

Initial jobless claims seasonally adjusted for the week ending June 16, 2026 came in at 226,000, versus the adjusted number of 230,000 people from the week prior, down 4,000 people week over week.

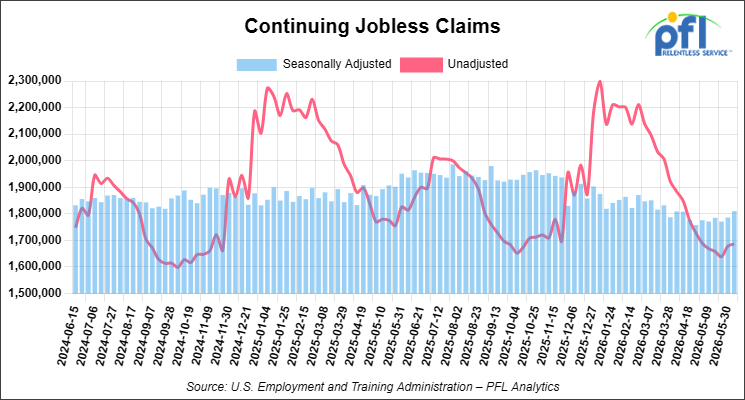

Continuing jobless claims came in at 1,810,000, versus the adjusted number of 1,786,000 people from the week prior, up 24,000 week-over-week.

Stocks closed higher on Thursday of last week and higher week-over-week

The DOW closed higher on Thursday of last week, up 72.15 points (0.14%), closing out the week at 51,564.70, up 362.44 points week-over-week. The S&P 500 closed higher on Thursday of last week, up 80.48 points (1.08%), and closed out the week at 7,500.58, up 69.12 points week-over-week. The NASDAQ closed higher on Thursday of last week, up 496.28 points (1.91%), and closed out the week at 26,517.93, up 629.12 points week-over-week.

In overnight trading, DOW futures traded higher and are expected to open at ______ this morning, up/down ______ points from Thursday’s close.

WTI Crude oil closed down Thursday of last week and lower week-over-week

West Texas Intermediate (WTI) crude closed down -0.19 per barrel (-0.25%), to close at $76.60 on Thursday of last week, and down $8.28 per barrel week-over-week. Brent crude closed up $0.30 per barrel on Friday of last week (0.38%), to close at $79.85, but down $7.48 week-over-week.

One Exchange WCS (Western Canadian Select) for August settled on Thursday of last week at US$12.25 below the WTI-CMA (West Texas Intermediate – Calendar Month Average). The implied value was US$63.48 per barrel.

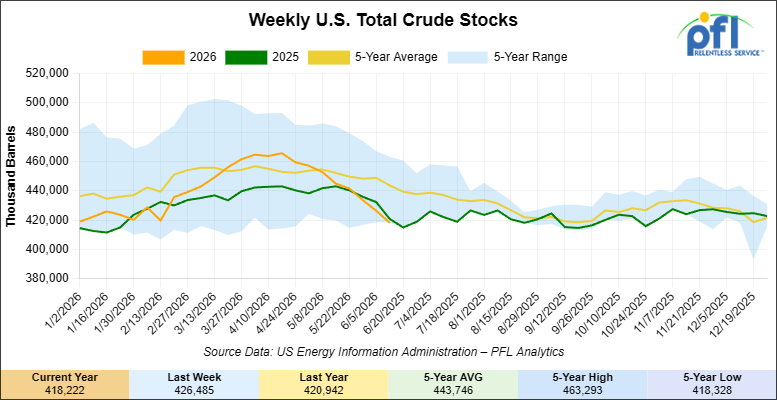

U.S. commercial crude oil inventories (excluding those in the Strategic Petroleum Reserve) decreased by 8.3 million barrels week-over-week. At 418.2 million barrels, U.S. crude oil inventories are 6% below the five-year average for this time of year.

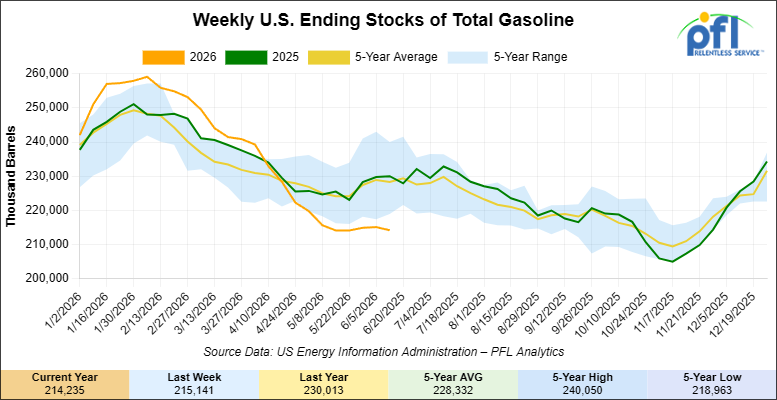

Total motor gasoline inventories decreased by 900,000 barrels week-over-week and are 6% below the five-year average for this time of year.

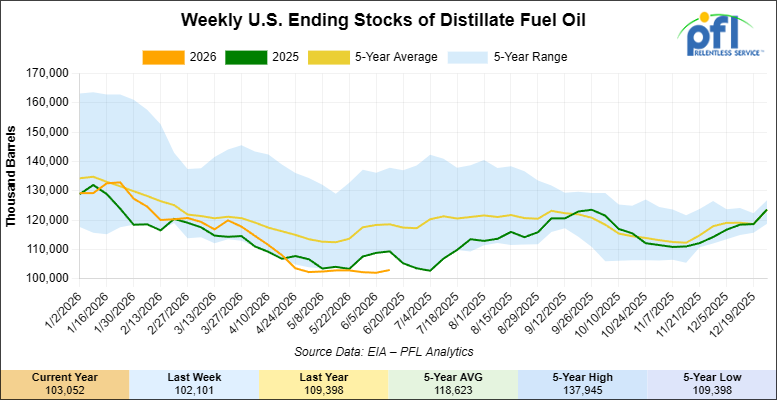

Distillate fuel inventories increased by 1 million barrels week-over-week and are 13% below the five-year average for this time of year.

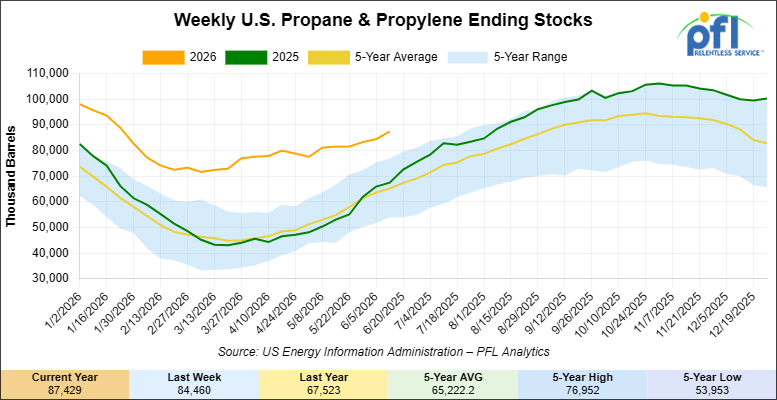

Propane/propylene inventories increased by 3.0 million barrels week-over-week and are 36% above the five-year average for this time of year.

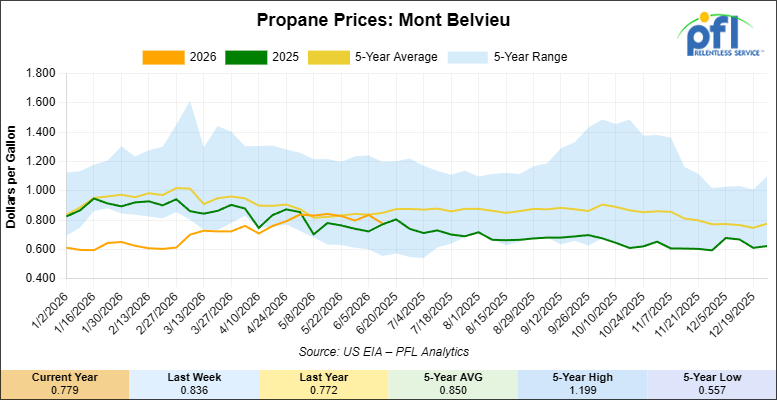

Propane prices closed at 77.9 cents per gallon on Friday of last week, down 5.7 cents per gallon week-over-week, but up 0.7 cents year-over-year.

Overall, total commercial petroleum inventories decreased by 7.9 million barrels week-over-week during the week ending June 12, 2026.

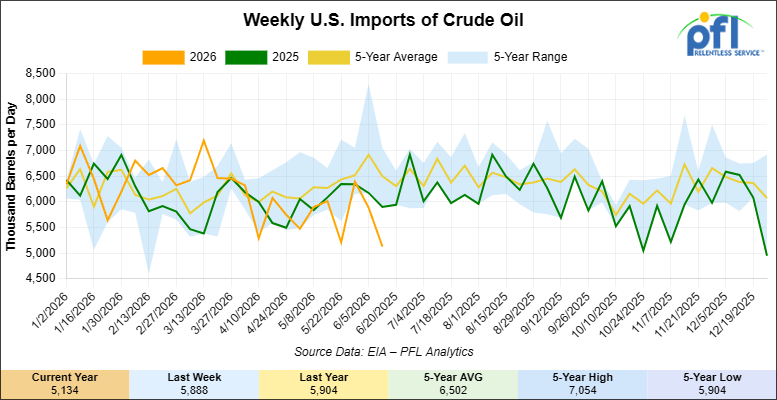

U.S. crude oil imports averaged 5.1 million barrels per day during the week ending June 12, 2026, a decrease of 754,000 barrels per day week-over-week. Over the past four weeks, crude oil imports averaged 5.7 million barrels per day, 7.2% less than the same four-week period last year. Total motor gasoline imports (including both finished gasoline and gasoline blending components) averaged 738,000 barrels per day, and distillate fuel imports averaged 127,000 barrels per day during the week ending June 12, 2026.

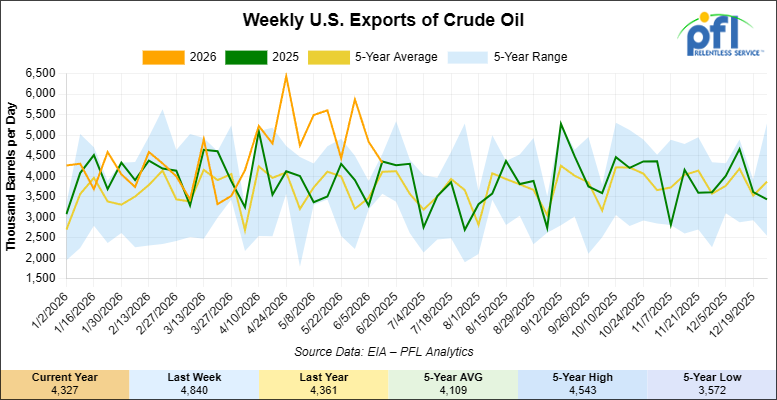

U.S. crude oil exports averaged 4.327 million barrels per day during the week ending June 12, 2026, a decrease of 513,000 barrels per day week-over-week. Over the past four weeks, crude oil exports averaged 4.87 million barrels per day.

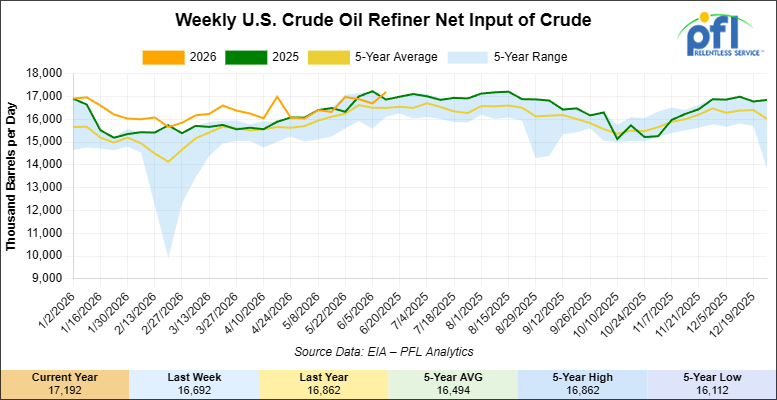

U.S. crude oil refinery inputs averaged 17.2 million barrels per day during the week ending June 12, 2026, which was 230,000 barrels per day more week-over-week.

WTI is poised to open at $80.15, down -$4.73 per barrel from Friday’s close.

North American Rail Traffic

Week Ending June 17, 2026:

Total North American weekly rail volumes were up (+7.33%) in week 25, compared with the same week last year. Total Carloads for the week ending June 17, 2026 were 333,354, up (+3.93%) compared with the same week in 2025, while weekly Intermodal volume was 349,207, up (+10.79%) year over year. 8 of the AAR’s 11 major traffic categories posted year-over-year increases. The largest decrease came from Chemicals (-3.10%). The largest increase was Grain (+17.03%).

In the East, CSX’s total volumes were up (+8.62%), with the largest decrease coming from Metallic Ores and Metals (-3.33%), while the largest increase came from Other (+19.18%). NS’s total volumes were up (+6.10%), with the largest increase coming from Other (+12.03%), while the largest decrease came from Chemicals (-8.06%).

In the West, BNSF’s total volumes were up (+10.52%), with the largest increase coming from Coal (+34.84%), while the largest decrease came from Other (-13.42%). UP’s total volumes were up (+5.58%), with the largest increase coming from Grain (+23.98%), while the largest decrease came from Coal (-8.05%).

In Canada, CN’s total volumes were up (+6.70%), with the largest increase coming from Coal (+34.84%), while the largest decrease came from Farm Products (-4.21%). CPKCS’s total volumes were up (+1.00%), with the largest increase coming from Farm Products (+36.86%), while the largest decrease came from Coal (-31.91%).

Source Data: AAR – PFL Analytics

North American Rig Count Summary

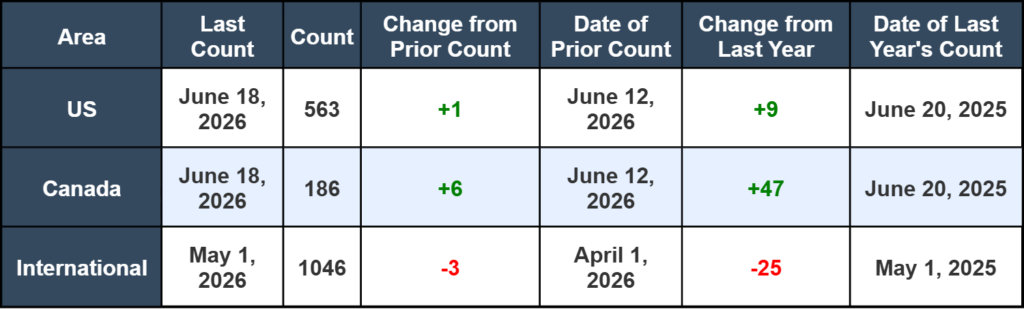

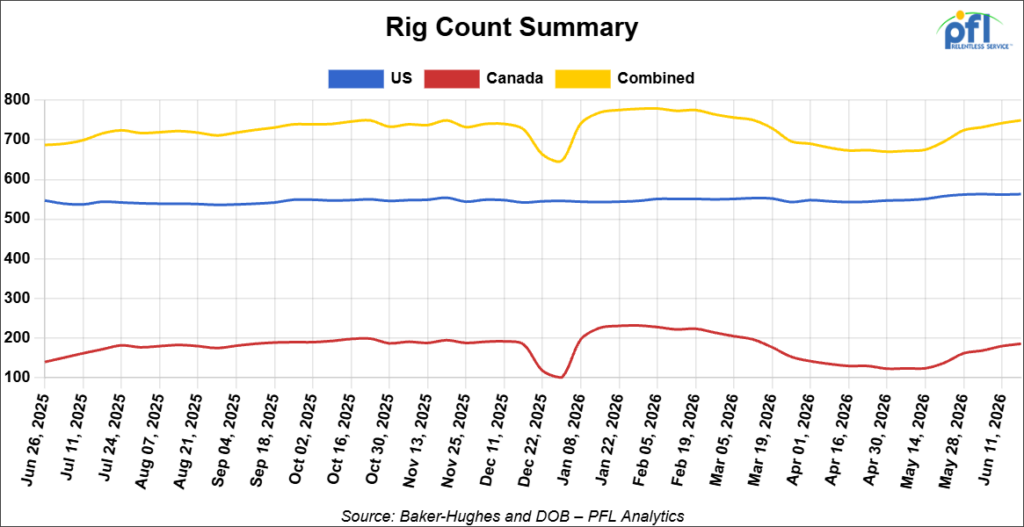

North American rig count was up by +7 rigs week-over-week. The US rig count was up by +1 rig week-over-week, and up by +9 rigs year-over-year. The US currently has 563 active rigs. Canada’s rig count was up by +6 rigs week-over-week and up by +47 rigs year-over-year. Canada currently has 186 active rigs. Overall, year-over-year we are up by +56 rigs collectively.

We are watching a few things out there for you:

We Are Watching Petroleum Carloads

The four-week rolling average of petroleum carloads carried on the six largest North American railroads rose to 29,476 from 29,424 which was an increase of +52 rail cars week-over-week. Canadian volumes were higher. CN’s shipments were higher by +10% week-over-week, CPKC’s volumes were higher by +2.0% week-over-week. U.S. shipments were mostly lower. The UP was the sole gainer and was up by +5.0%. The BN had the largest percentage decrease and was down by -3.0% week-over-week.

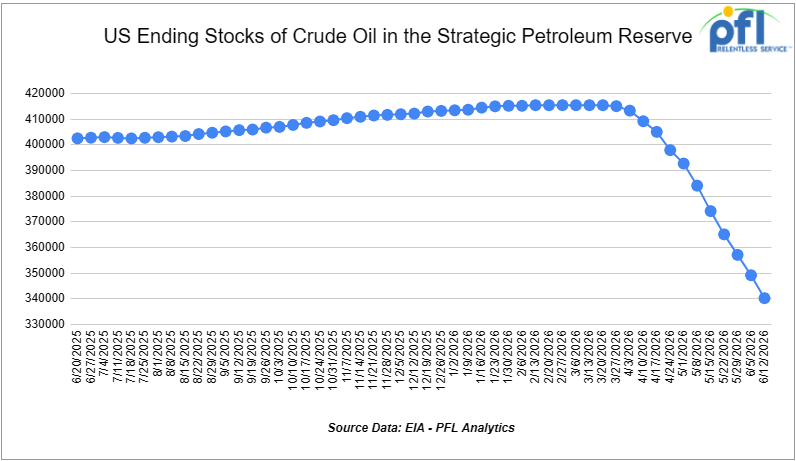

We Continue to Watch Our Strategic Petroleum Reserves

The ongoing emergency drawdown of the U.S. Strategic Petroleum Reserve (SPR) remains a major component of global efforts to offset crude oil supply disruptions stemming from the conflict involving Iran and the continued restrictions on oil shipments through the Strait of Hormuz. Since March, the Department of Energy (DOE) has awarded exchanges covering more than 80 million barrels of crude oil, with additional releases expected as part of a broader international response coordinated through the International Energy Agency (IEA).

The United States committed to making up to 172 million barrels available from the SPR under the IEA’s collective plan to inject roughly 400 million barrels into global energy markets. Officials have argued that the releases are necessary to help stabilize crude supplies and limit further increases in fuel prices as refiners compete for replacement barrels amid ongoing transportation disruptions.

As releases have accelerated, inventories in the SPR have declined to 340.251 million barrels, down sharply from levels above 450 million barrels earlier this year and reaching their lowest level since January 2024. Recent weekly withdrawals have ranked among the largest on record, highlighting the scale of the government’s intervention in oil markets. On average, since the war started with Iran, the United States has withdrawn approximately 1.09 million barrels per-day from the SPR through the week ending June 12, 2026.

Global petroleum inventories have also tightened considerably. The IEA has reported substantial draws in commercial crude and refined-product stockpiles across major consuming nations, underscoring the strain that the conflict has placed on world energy markets. Agency officials have indicated that further coordinated actions remain possible should supply disruptions persist or intensify.

The Administration continues to emphasize that the current program consists primarily of exchange agreements, rather than outright sales. Under these arrangements, companies receiving crude oil today are required to return the borrowed barrels in the future along with additional volumes as a premium. Energy Secretary Chris Wright has stated that the objective is to eventually restore the SPR to levels above those that existed prior to the current emergency releases.

Meanwhile, energy prices remain slightly elevated compared with pre-conflict levels, keeping fuel costs a focus for consumers, businesses, and policymakers alike. Market participants continue to monitor developments in the Middle East, future IEA actions, and the pace of SPR releases as key factors influencing oil prices through the remainder of the year.

We Continue to Watch Hormuz

Crude gave back almost the entire war premium last week after President Trump said on June 14th that a deal to reopen the strait of Hormuz was complete. Iran and the U.S. signed off on the deal on June 19th. The selloff ran straight through the diesel and gasoline complex, with retail gasoline averaging $4.052 per gallon for the week ended June 15th, off 9.4 cents on the week and well below the peaks the trade had been bracing for this summer.

The drawdown that built over the conflict has left visible marks on inventory. Cushing stocks fell to roughly 20 million barrels, the lowest since 2014, on an eighth straight weekly draw. The Strategic Petroleum Reserve as noted above has drawn down roughly 110 million barrels. For the carload side the read is on the spread, not the headline. Chinese buyers paused Trans Mountain purchases almost the moment the news hit, waiting on cheaper delivered barrels as Persian Gulf flows return, and that pause pulls the near-term floor out from under any Canadian crude by rail economics. Jones Act tanker rates tell the same story, off about 75% from their April peak as foreign-flag tonnage floods back in under the wartime waiver. A peace deal seems like good news for the consumer and for refiners, but it takes the urgency out of every high-cost egress option, rail included. The story is not over on this one as tensions persisted over the weekend and Iran now is going to get a bunch of money and does not seem to want to change their ways. We believe that the President is just trying to buy some time here for a variety of reasons but we will be back at it in the not so distant future. Stay tuned to PFL for further updates. This story is far from over.

We are Watching Tank Cars

The National Transportation Safety Board reiterated its call to accelerate the DOT-111 phaseout on June 11 and, more usefully for anyone managing a hazmat fleet, put the DOT-117R retrofit squarely in its sights. Coming out of the Bordulac, North Dakota investigation, the board found that 117R cars, retrofitted from older DOT-111s with a thinner shell, have not delivered the safety performance of new-build 117J cars. This is the live edge of the same Railway Safety Act thread we have tracked for months, and it shifts the conversation from “phase out the 111s” to “the cheaper retrofit may not count.”

The Bordulac derailment, a July 2024 CPKC consist that put 29 cars on the ground including 17 hazmat tank cars, was the first major hazmat-release derailment the board has worked since East Palestine. A broken rail over a collapsed culvert dropped the train, methanol fed a pool fire, and the heat tore into adjacent cars and released anhydrous ammonia. The board issued 11 new recommendations and reiterated six others, including a call for criteria on separating poison-inhalation cars from flammables in the consist. The 111s, in the board’s words, remain dangerously inadequate.

The hard part is that the most consequential recommendation, setting a schedule to require cars to exceed the 117 specification, runs through Congress, and PHMSA has said as much. That keeps it tied to the Railway Safety Act language still working its way through the legislative pipeline. If regulators do tighten on 117Rs the demand does not disappear, it migrates to new-build 117J, and that is the corner of the fleet with the longest lead times and the firmest lease terms. Builders are quoting up to five years, and car owners and lessors are not putting steel on the ground without multi-year commitments. PFL has been telling shipper customers for a while that betting a 20 year asset on a retrofit was the riskier seat. In our opinion, the board just made that case for us.

We are Watching Crude by Rail

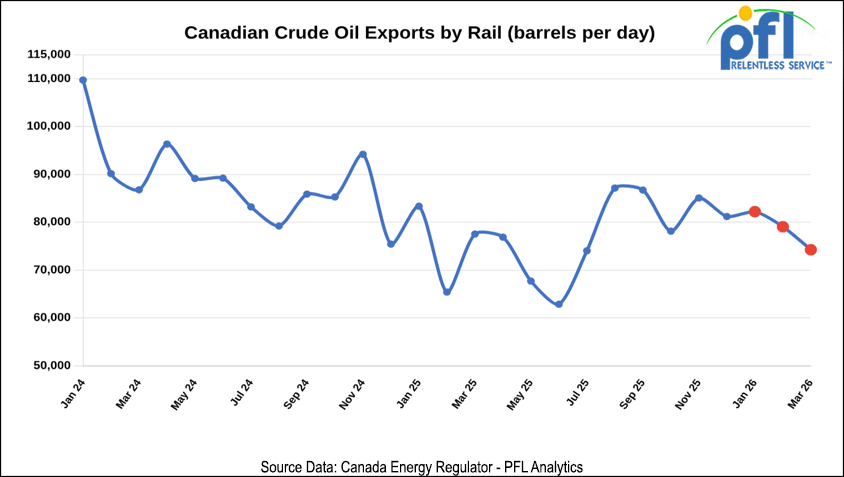

Canadian crude by rail exports ran 74,248 barrels per day in March, a third straight monthly decline from 82,183 in January and 79,057 in February, and they sit near the multi-year lows that have defined the post-Trans Mountain era. At the Hardisty, Western Canadian Select is trading roughly $12.25 under WTI, short of the $18 discount rail needs to be against a $17.32 Alberta-to-Gulf-Coast unit rate. Right now the spread does not work. This is not a market making last-minute moves.

The reason to keep watching crude by rail out of Canada is what is coming, not what is moving. Producers have north of 600,000 barrels per day of timed oil sands growth on the books, with close to another 700,000 in medium and longer-term plans, roughly 1.1 million barrels per day net of Suncor base-mine depletion arriving into the early 2030s. IPC’s Blackrod project started production at the end of May and ramps to 30,000 barrels per day, with regulatory room to 80,000 barrels per day. Pipeline egress does not grow on that schedule: about 180,000 barrels per day of new capacity comes on late next year, and the rest is proposals.

Enbridge eased heavy-crude apportionment to 11% for July, down from 19%, but that is an outage story, not a demand story: Cenovus declared force majeure in early June after heavy rain cut Foster Creek and Christina Lake output. Take the curtailment away and the structural tightness comes straight back, because egress out of the basin does not flex. Light-crude apportionment actually rose to 21% over the same stretch.

None of this turns into rail cars overnight, and the people who got burned on the last run know why. Builders and lessors want five-year commitments, and the Class Ones want a take-or-pay before they will commit crews and power to unit trains, so crude by rail is a committed multi-year decision, not a swing market. But, the setup is the one that has started cycles before: a wall of heavy barrels, fixed pipe, and the basis which is one geopolitical turn away from blowing back out. This could be the beginning of another crude by rail cycle if the trends hold. Time will tell.. PFL helps customers think through fleet timing well before the spread forces the issue, which is exactly when the lead times stop being theoretical.

We Continue to Watch Left Wing Carney

Alberta’s deadline to put its west-coast bitumen pipeline proposal in front of the federal Major Projects Office is July 1st, and the file going in has no private proponent and no route. The province is acting as its own proponent on a line that, on Ottawa’s own best-case timeline, would not be designated a project of national interest until October and would not see construction approval until September 2027. First oil, if a builder ever materializes, lands in the 2030s.

Line that up against the barrels. The oil sands growth wave is arriving now into pipe that does not flex, while the relief Ottawa is advertising moves nothing this decade, so the line does nothing for the egress gap it is sold as solving in the only window that matters. Meanwhile the price of admission is locked in: Alberta’s industrial carbon levy climbs toward C$130 per tonne, and the whole arrangement hangs on the Pathways carbon-capture project that still is not sanctioned. Producers pay the tax for years before a single barrel of this decarbonized oil moves, if it ever does.

In our opinion, this is a plan to write a plan. The tax bill is real and arrives on schedule. The pipe is a press release with a deadline.

We Continue to Watch the Surface Transportation Board

Union Pacific spent last week trying to start a clock the regulator has not acknowledged. Speaking on June 16th, CEO Jim Vena argued that the board’s 12-month statutory window to rule on the Norfolk Southern merger began when the application was accepted on May 28, not whenever the supplemental information lands. The board accepted the filing but held the proceeding in abeyance, ordered an environmental impact statement, and set a July 27th deadline for the additional detail it wants. The agency declined to comment on Vena’s reading.

UP plans to deliver the supplemental information in two batches, the first in early July and the balance by the deadline, ideally before its second-quarter call. The stack the board wants is not trivial: competition effects, service assurance, market-share projections, and the downstream consequences of copycat mergers, all under the 2001 rules that require a deal to enhance competition rather than merely preserve it. This is the first major Class I combination tested against that standard, and a 55,000-mile network handling roughly half of U.S. rail freight is not the file the board rushes.

Vena can read the statute however he likes, but the abeyance, the environmental review, and the volume of what is still outstanding all point the other way on timing. The board may have a path to a mid-2027 decision, but nothing about the last six months suggests it feels rushed. PFL remains unconvinced this gets across the line on the schedule UP keeps floating, and we are watching the July 27th filing closely.

We are Watching Truck Rates

Truckload contract rates set early in the 2026 bid season are not holding, and the carriers told investors at the Wells Fargo conference last week that the reason is structural. Tender rejections are surging, mini-bid activity has spiked, and J.B. Hunt flagged a cumulative rate increase on the order of 20% over the next two years. Routing guides built on cheap capacity are coming apart faster than the usual cycle would explain.

What is different is the supply side. Regulatory enforcement has been purging non-compliant drivers since last fall, cabotage rules are being policed, and the Supreme Court’s Montgomery broker-liability ruling has widened the exposure that kept thinly vetted carriers in the market. Schneider is calling the capacity reduction structural rather than transitory, and contract renewals are running at their highest level since 2021. The old release valve, a flood of new entrants chasing load-board rates, is not there this time.

For rail this is a positive development. Sustained truckload inflation is the cleanest modal-shift tailwind intermodal and carload have had in years, and it widens the lane where rail wins on delivered cost. PFL is watching this one closely and is willing to work with shippers that are thinking of making a switch to rail.

We Are Watching America’s Harvest

Last week, CN, Grupo Mexico, and two short lines announced a new coordinated rail service, called America’s Harvest, is now up and running. For grain shippers looking at Mexico as a growth market, this is exactly the kind of infrastructure that makes expansion possible.

The service moves pulse crops and other agricultural products from Genesee & Wyoming’s Huron & Eastern Railway origins in Kinde and Durand, Michigan, through CN to Mobile, Alabama, where CG Railway ferries the cars to Mexico. From there, Grupo Mexico’s Ferromex or Ferrosur completes delivery to destinations across central and southern Mexico. Transit times range from 15 days to Coatzacoalcos up to 27 days to Guadalajara.

What makes this notable is the coordination. Four separate rail partners: CN, HESR, CG Railway, and Grupo Mexico Transportes, are operating under a single waybill with end-to-end tracking and built-in import and export compliance support. Shippers get one point of contact instead of negotiating separately with each carrier in the chain. Customs pre-clearance lets shippers bypass congestion at the border.

For grain and pulse crop shippers, this solves a real problem. Entering or expanding into the Mexican market has historically meant managing multiple rail handoffs, separate paperwork, and execution risk at each interchange point. America’s Harvest consolidates that complexity into a single coordinated service. HESR’s director of sales and marketing called Mexico a significant and expanding destination for U.S. agricultural exports, and this service is a direct bet on that growth continuing.

PFL will keep watching how this service develops and whether similar coordinated cross-border products emerge for other commodities.

We are Watching the BNSF

The Barstow City Council approved BNSF’s Barstow International Gateway on June 17th, clearing the last local hurdle for a 4,500-acre rail, intermodal, and transload complex west of town. The $4 billion privately funded build would take boxes off ships at Los Angeles and Long Beach, run them up the Alameda Corridor to Barstow for sorting, and build them into eastbound trains there. BNSF puts the truck-mile reduction at roughly 205 million by 2028, rising past 300 million by 2048.

This is an intermodal fluidity play more than a carload one, but it matters to anyone moving freight west: pulling container sorting off the LA basin and inland to Barstow is meant to take pressure off the most congested terminals in the country. Whether it relieves congestion or simply relocates it east will come down to how BNSF phases the build and how the ports cooperate. We are watching the construction timeline.

We Are Watching the Signalmen’s Tentative Agreement

The National Carriers’ Conference Committee reached a tentative agreement with the Brotherhood of Railroad Signalmen last week, and if ratified, it closes out the current round of national rail labor negotiations.

The five-year deal follows the same pattern already ratified by 11 other rail unions: an 18.8% compounded wage increase over five years, enhanced health and welfare benefits with no increase to employee contribution rates, and expanded paid vacation access earlier in employees’ careers. The agreement runs through December 31, 2029, and would raise average annual wages for covered signalmen to $135,000, with average total compensation reaching $190,000.

This is the same union, the BRS, that represents the workers behind the CPKC signals strike in Canada we have been covering. The U.S. and Canadian negotiations are separate, but the parallel is notable: in the U.S., the pattern bargaining process appears to be working as designed, while in Canada, the CPKC dispute remains unresolved with no clear end date. That contrast says something about how differently the two negotiating frameworks are functioning right now.

For shippers, labor stability on the signals side matters more than it might seem. Signals and communications technicians maintain the trackside infrastructure that keeps trains moving safely: switches, crossing warning systems, and signal equipment. A ratified, multi-year agreement removes the risk of a U.S. signals work stoppage through the end of the decade, which is a meaningful stability point given everything else happening in the labour landscape right now.

The deal still needs to clear membership ratification, and a vote timeline has not yet been announced. BRS members have rejected tentative agreements before, most notably during the 2022 national contract dispute. Given the strong participation and ratification trend among the other 11 unions this round, the agreement appears likely to pass, but it is not finalized yet.

PFL will keep watching as the ratification vote proceeds.

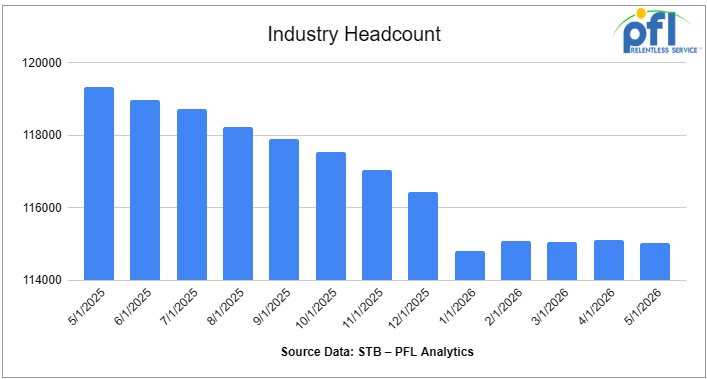

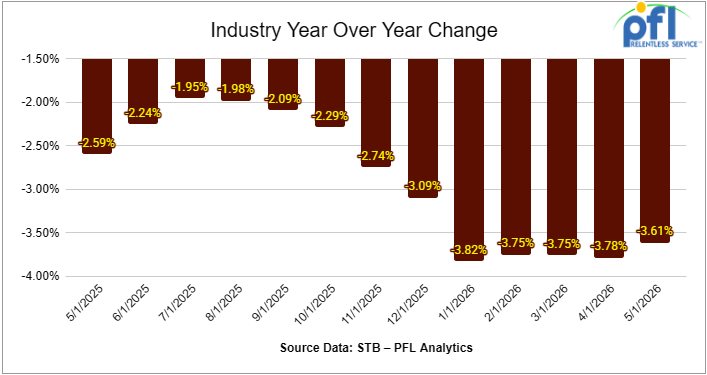

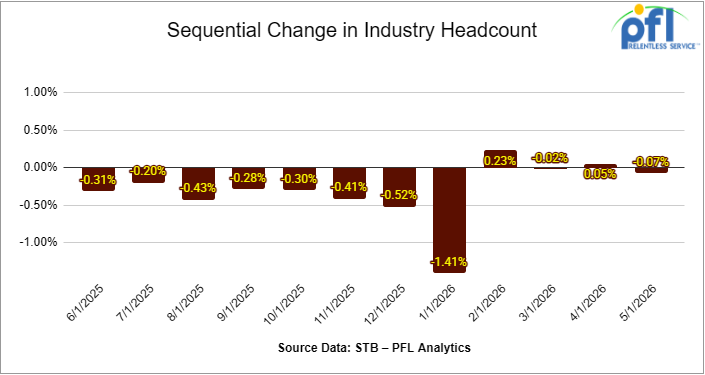

We are watching Class 1 Industrial Headcount

Class I railroads employed 115,030 workers in the United States in May 2026, a -0.07% decrease from April 2026’s count of 115,113 but a -3.61% year-over-year decrease from May 2025’s total of 119,339, according to Surface Transportation Board data.

Two of the six employment categories posted month-over-month increases between April and May 2026. These were Maintenance of Way and Structures, which increased 0.13% to 28,794 workers, and Transportation (train and engine), which increased 0.38% to 48,966 workers.

The categories that posted month-over-month decreases were Executives, officials, and staff assistants, down -0.40% to 7,953 workers; Professional and Administrative, down -0.89% to 8,726 workers; Maintenance of Equipment and Stores, down -0.99% to 15,946 workers; and Transportation (other than train and engine), down -0.75% to 4,645 workers.

No employment categories posted a year-over-year gain in May 2026.

Categories that registered year-over-year decreases in May 2026 were Executives, officials, and staff assistants, down -0.14%; Professional and Administrative, down -5.37%; Maintenance of Way and Structures, down -1.01%; Maintenance of Equipment and Stores, down -6.55%; Transportation (other than train and engine), down -6.71%; and Transportation (train and engine), down -4.03%.

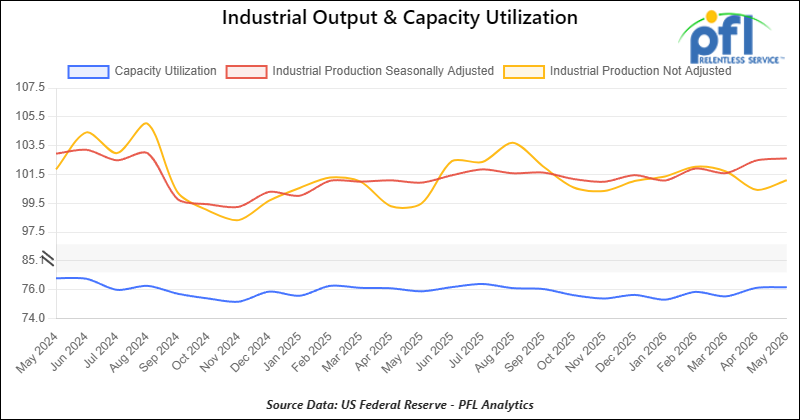

Industrial Output and Capacity Utilization

Manufacturing accounts for approximately 75% of total output. Manufacturing output in May increased 0.14% from April 2026.

Capacity utilization is a measure of how fully firms are using machinery and equipment. Capacity utilization increased by 0.04 percentage points from April in May.

Lease Bids

- 100, 21.9K 117J Tanks located off of All Class 1s in the Midwest. For use in CO2 service. Period: 6 months.

- 30-50, 30K 117J Tanks located off of NS or CSX in the Northeast. For use in C5 service. Period: 1 year.

- 20-50, 4000-5000 Covered Hoppers located off of UP or BNSF in Houston. For use in Urea, Potash, and Ammonium Sulfate service. Period: 6-12 Months.

- 200, 33K Pressure Tanks located off of CSX or NS in Ohio. For use in Propylene service. Period: 18 Months.

- 30-50, 25.5K DOT 111 Tanks located off of All Class 1s in various locations. For use in Asphalt service. Period: 1-3 Years.

- 40, 33K Pressure Tanks located off of UP in Eunice, LA. For use in Propane service. Period: 1 Year.

- 40, 29K DOT 111 Tanks located off of UP or BNSF in the Midwest. For use in Veg Oil service. Period: 5 Year.

- 70, 30K DOT 117 Tanks located off of NS or CSX in Ohio. For use in Diesel service. Period: 3 months.

- 20, DOT 117J Tanks located off of NS, CSX, CN, or CPKC in various locations. For use in C5 service. Period: 1 year. Need gauge rods.

- 300, 5200CF Covered Hoppers located off of CP or CM in Canada. For use in Petcoke service. Period: 3 Year.

- 10, 30K 117J Tanks located off of BNSF in Canada. For use in Propane or Butane service. Period: 3 Year.

- 20, 28K or larger 117J Tanks located off of BNSF or UP in California. For use in Crude service. Period: 6 months.

- 75, 30K 117 Tanks located off of NS in Ohio. For use in Condensate service. Period: 6-12 Months. Mag Rods Not Needed.

- 100, 28.3K DOT 111 or 117 Tanks located off of CP or CN in Canada. For use in VGO service. Period: 1-3 Years.

- 5, 28.3K DOT 111 or 117 Tanks located off of CN in Canada. For use in Bitumen service. Period: Trip Lease.

Sales Bids

- 28, 3400CF Covered Hoppers located off of UP or BNSF in Texas. For use in Cement service. Cement Gates needed.

- 20, 17K DOT111 Tanks located off of various class 1s in various locations. For use in corn syrup service.

- 120, Various Open-Top Aluminum Rotary Gondolas located off of various class 1s in various locations. For use in Sulphur service. Built 2004 or later.

Lease Offers

- 21, 6351 Covered Hoppers located off of CN in Wisconsin. Last used in DDG. Available until February 2027.

- 29, 6500 Covered Hoppers located off of CN in Wisconsin. Last used in DDG. Available until February 2027.

- 50, 20K DOT117J Tanks located off of all class 1s in Moving. Last used in styrene.

- 29, 25.5K DOT117J Tanks located off of UP or BNSF in Texas. Cars are currently clean.

- 200, 340W DOT 112J Tanks located off of all class 1s in Multiple Locations. Last used in propane and butane. Cars are currently clean.

- 15, 6200CF Covered Hoppers located off of all class 1s in Wisconsin. Last used in plastic. Cars are currently clean.

- 30, 6500CF Covered Hoppers located off of all class 1s in Wisconsin. Last used in plastic. Cars are currently clean.

- 6, 21K Stainless Steel Tanks located off of UP in Texas / Mexico Border. Last used in surfactant. Cars are currently clean.

- 100, 28.4K DOT 117J Tanks located off of UP or BNSF in Beaumont, TX. Cars are currently clean.

- 50, 30K DOT117J Tanks located off of UP or BNSF in the South. Last used in ethanol.

- 30, 30K DOT 117R Tanks located off of BNSF in Washington. Last used in renewable jet fuel.

- 80, 30K DOT 117R Tanks located off of BNSF in Washington. Last used in renewable diesel.

- 10, 30K DOT 117R Tanks located off of BNSF in Washington. Last used in renewable naphtha.

- 10, 29K DOT 117R Tanks located off of BNSF and UP in Texas. Last used in gasoline additive. Coiled and Insulated.

- 39, 31K CPC1232 Tanks located off of All Class 1s in Iowa. Last used in diesel.

- 99, 31K CPC1232 Tanks located off of BNSF and UP in Texas. Last used in diesel.

- 1, 31K CPC1232 Tanks located off of BNSF and UP in Texas. Last used in naphtha.

- 2, 30K DOT 117R Tanks located off of BNSF and UP in Texas. Last used in giesel.

- 1, 30K DOT 117R Tanks located off of BNSF and UP in Texas. Last used in gas blend stock.

- 3, 30K DOT 117R Tanks located off of BNSF and UP in Texas. Last used in gasoline.

- 36, 31K CPC1232 Tanks located off of CPKC in Texas. Last used in diesel.

- 6, 31K CPC1232 Tanks located off of CPKC in Texas. Last used in naphtha.

Sales Offers

- 81, 31.8K CPC1232 Tanks located off of UP or BNSF in TX. Last used in Multiple Services. Requal Due in 2025.

- 35, 3400CF Covered Hoppers located off of UP or BNSF in the Midwest. Last used in Sand.

- 25, 30K 117J Tanks located off of CSX in Jackson, TN. Last used in Fuels. Newly Requalified.

Call PFL today to discuss your needs and our availability and market reach. Whether you are looking to lease cars, lease out cars, buy cars, or sell cars call PFL today at 239-390-2885

Live Railcar Markets

| CAT | Type | Capacity | GRL | QTY | LOC | Class | Prev. Use | Offer | Note |

|---|

PFL will be at the Following Conferences

- Where: Calgary

- Attending: David Cohen (954-729-4774), Curtis Chandler(239-405-3365), Cyndi Popov (403-402-5043)

- Where: Grand Geneva Resort

- Attending: Brian Baker (239.297.4519)

- Conference Website

- Where: Loews Arlington Hotel

- Attending: Brian Baker (239.297.4519), David Cohen (954-729-4774), and Curtis Chandler (239-405-3365)

- Conference Website

- Where: The Westin Galleria Dallas

- Attending: David Cohen (954-729-4774), and Curtis Chandler (239-405-3365)

- Conference Website

- Where: The Westin Galleria Dallas

- Attending: Brian Baker (239.297.4519)

- Conference Website