“The easiest thing to be in the world is you. The most difficult thing to be is what other people want you to be. Don’t let them put you in that position” – Leo Buscaglia

Jobs Update

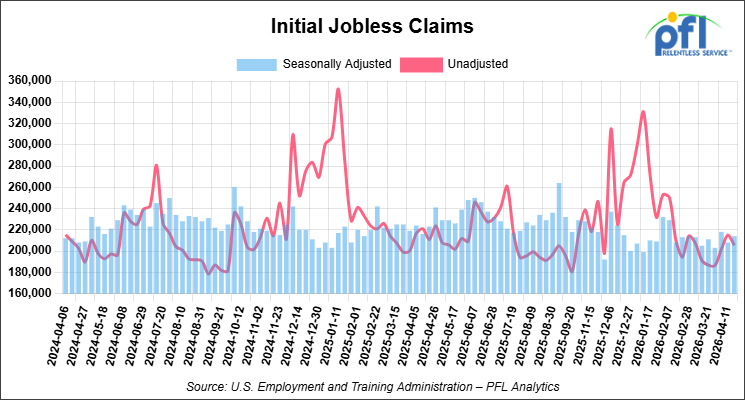

- Initial jobless claims seasonally adjusted for the week ending April 18, 2026 came in at 214,000, versus the adjusted number of 208,000 people from the week prior, up 6,000 people week over week.

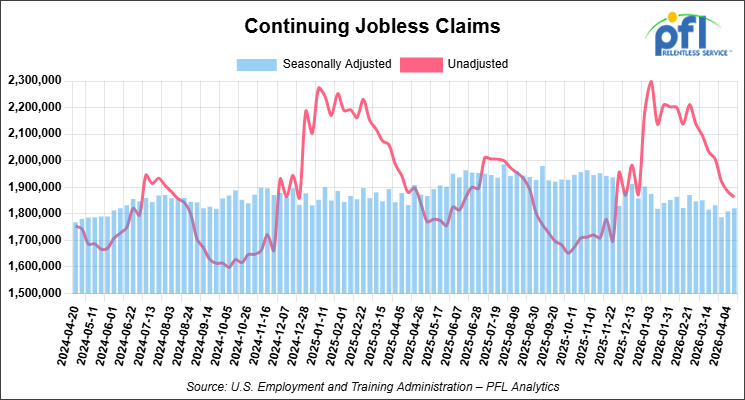

- Continuing jobless claims came in at 1,821,000, versus the adjusted number of 1,809,000 people from the week prior, up 12,000 week-over-week.

Stocks closed mixed on Friday of last week and mixed week-over-week

The DOW closed lower on Friday of last week, down -79.61 points (-0.16%), closing out the week at 49,230.71, down -217.21 points week-over-week. The S&P 500 closed higher on Friday of last week, up 56.68 points (0.80%), and closed out the week at 7,165.08, up 39.04 points week-over-week. The NASDAQ closed higher on Friday of last week, up 398.09 points (1.63%), and closed out the week at 24,836.60, up 368.12 points week-over-week.

In overnight trading, DOW futures are pointing lower and are expected to open at 49,303 this morning, down 89 points from Friday’s close.

Crude oil closed mixed on Friday of last week and higher week-over-week

West Texas Intermediate (WTI) crude closed down -1.45 per barrel (-1.5%), to close at $94.40 on Friday of last week, but up $10.55 week-over-week. Brent crude closed up 0.26 per barrel (0.3%), to close at $105.33, and up $14.95 week-over-week.

One Exchange WCS (Western Canadian Select) for June delivery settled on Friday of last week at US$14.74 below the WTI-CMA (West Texas Intermediate – Calendar Month Average). The implied value was US$74.65 per barrel.

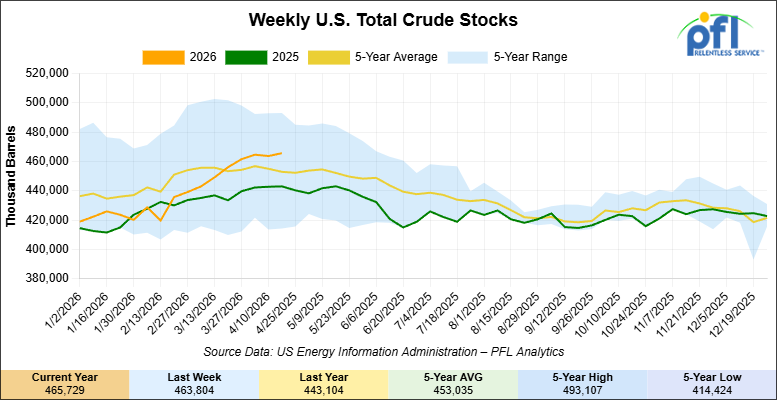

U.S. commercial crude oil inventories (excluding those in the Strategic Petroleum Reserve) increased by 1.9 million barrels week-over-week. At 465.7 million barrels, U.S. crude oil inventories are 3% above the five-year average for this time of year.

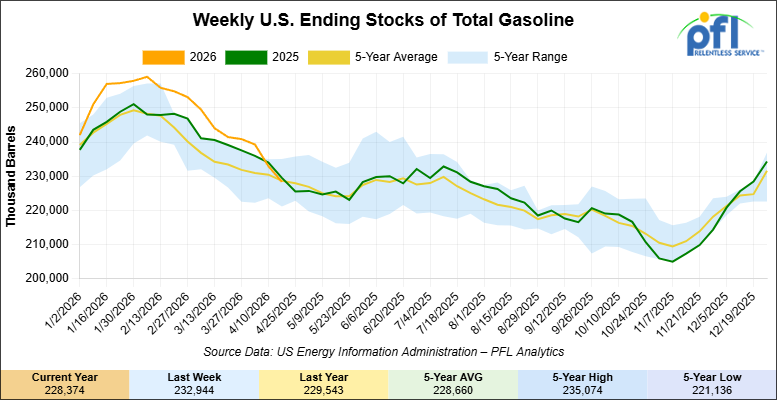

Total motor gasoline inventories decreased by 4.6 million barrels week-over-week and are 0.5 % below the five-year average for this time of year.

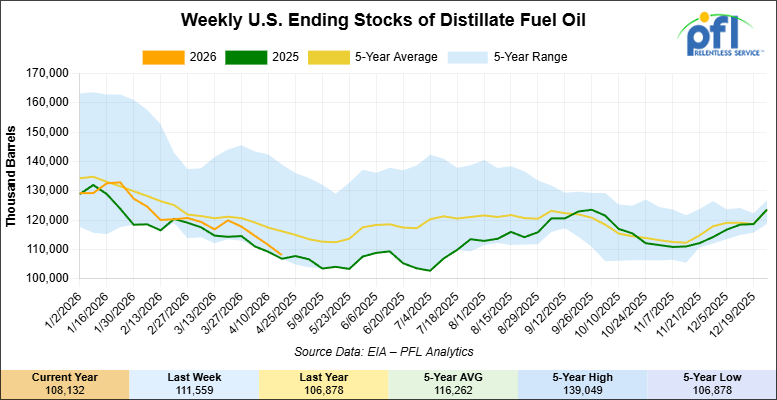

Distillate fuel inventories decreased by 3.4 million barrels week-over-week and are 8% below the five-year average for this time of year.

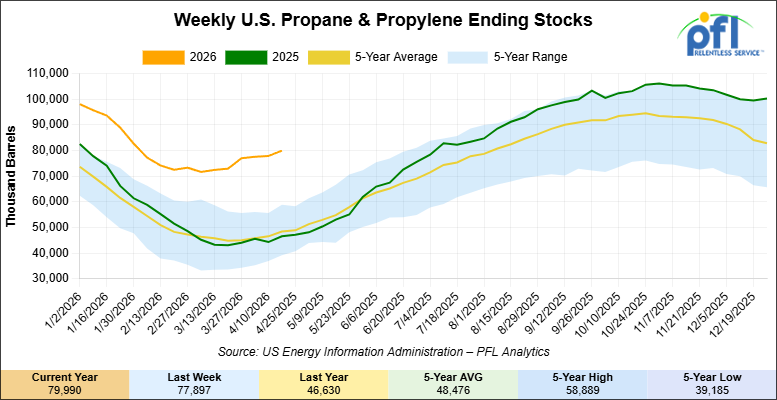

Propane/propylene inventories increased by 2.1 million barrels week-over-week and are 69% above the five-year average for this time of year.

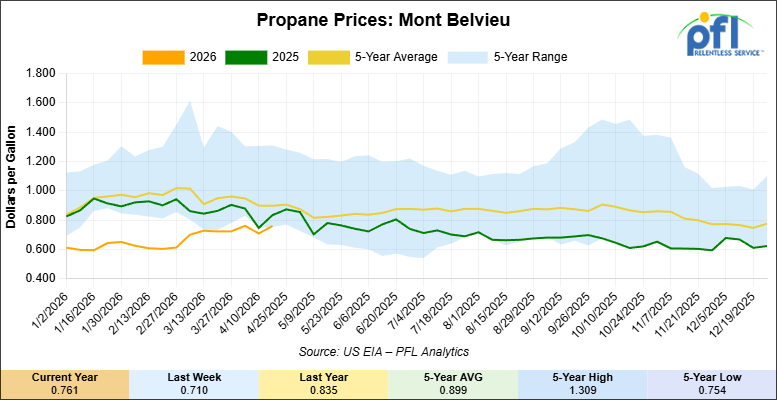

Propane prices closed at 76.1 cents per gallon on Friday of last week, up 5.1 cents per gallon week-over-week, but down 7.4 cents year-over-year.

Overall, total commercial petroleum inventories decreased by 1.8 million barrels week-over-week, during the week ending April 17, 2026.

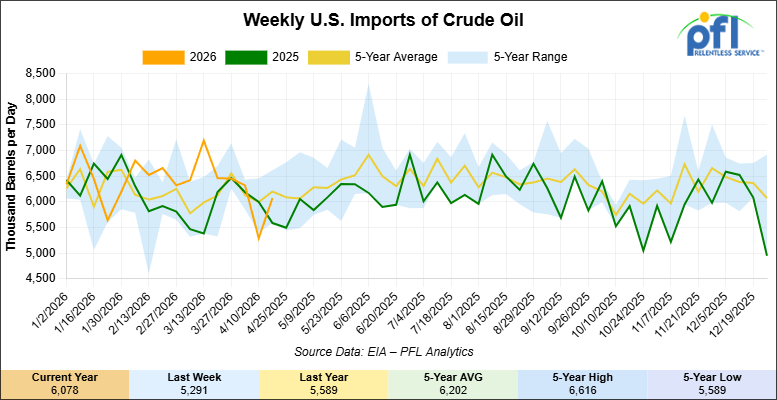

U.S. crude oil imports averaged 6.1 million barrels per day during the week ending April 17, 2026, an increase of 787,000 barrels per day week-over-week. Over the past four weeks, crude oil imports averaged 6 million barrels per day, 0.4% less than the same four-week period last year. Total motor gasoline imports (including both finished gasoline and gasoline blending components) averaged 587,000 barrels per day, and distillate fuel imports averaged 190,000 barrels per day during the week ending April 17, 2026.

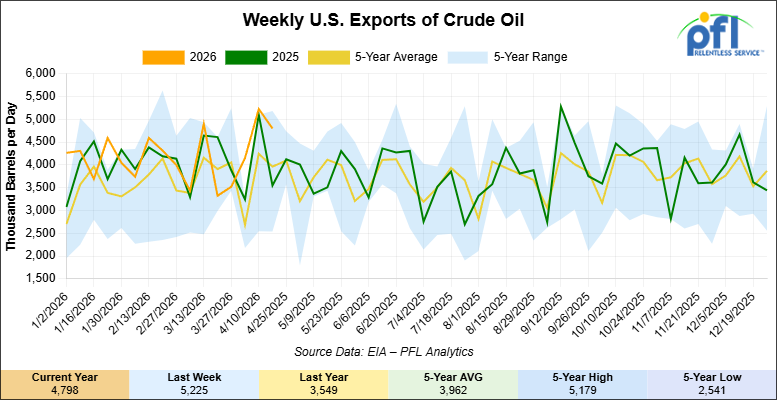

U.S. crude oil exports averaged 4.798 million barrels per day during the week ending April 17, 2026, a decrease of 427,000 barrels per day week-over-week. Over the past four weeks, crude oil exports averaged 4.423 million barrels per day.

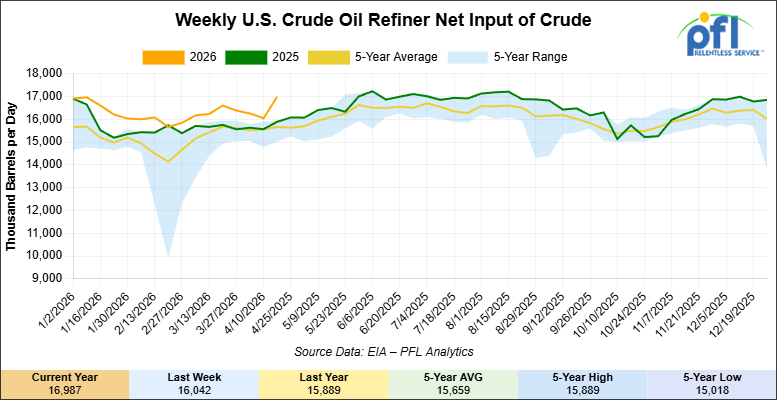

U.S. crude oil refinery inputs averaged 16 million barrels per day during the week ending April 17, 2026, which was 55,000 barrels per day less week-over-week.

WTI is poised to open at $96.40, up $2 per barrel from Friday’s close.

North American Rail Traffic

Week Ending April 22, 2026:

Total North American weekly rail volumes were up (+1.30%) in week 17, compared with the same week last year. Total Carloads for the week ending April 22, 2026 were 333,933, up (+2.09%) compared with the same week in 2025, while weekly Intermodal volume was 336,179, up (+0.53%) year over year. 8 of the AAR’s 11 major traffic categories posted year-over-year increases. The largest decrease came from Forest Products (-13.17%). The largest increase was Grain (+19.17%).

In the East, CSX’s total volumes were up (+1.19%), with the largest decrease coming from Metallic Ores and Metals (-14.61%), while the largest increase came from Other (+12.55%). NS’s total volumes were up (+2.13%), with the largest increase coming from Petroleum & Petroleum Products (+30.93%), while the largest decrease came from Forest Products (-8.81%).

In the West, BNSF’s total volumes were up (+7.29%), with the largest increase coming from Grain (+28.99%), while the largest decrease came from Coal (-11.89%). UP’s total volumes were down (-0.14%), with the largest increase coming from Grain (+19.28%), while the largest decrease came from Coal (-16.87%).

In Canada, CN’s total volumes were down (-0.08%), with the largest increase coming from Grain (+37.04%), while the largest decrease came from Farm Products (-11.91%). CPKCS’s total volumes were down (-20.11%), with the largest increase coming from Grain (+15.86%), while the largest decrease came from Forest Products (-68.54%).

Source Data: AAR – PFL Analytics

North American Rig Count Summary

Rig Count

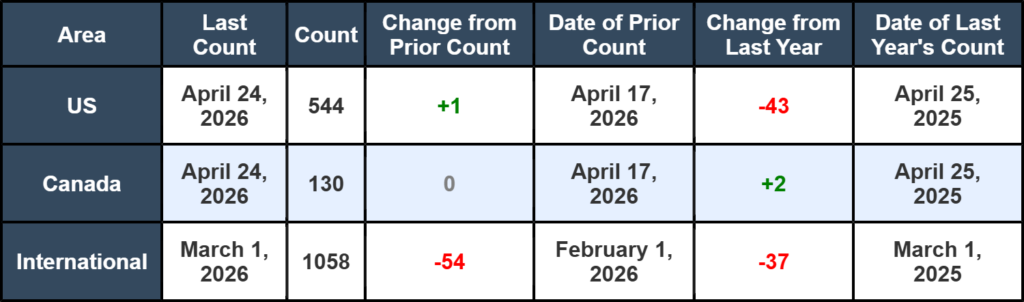

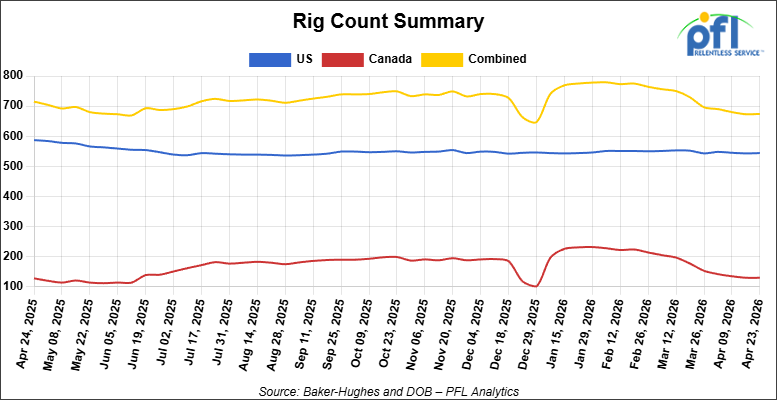

North American rig count was up by +1 rig week-over-week. The US rig count was up by +1 rig week-over-week, but down by -43 rigs year-over-year. The US currently has 544 active rigs. Canada’s rig count was unchanged week-over-week and up by +2 rigs year-over-year. Canada currently has 130 active rigs. Overall, year-over-year we are down by -41 rigs collectively.

We are watching a few things out there for you:

PFL Attended Last Week’s WCRTC Spring Networking Event Calgary, Canada

The Western Canadian Rail & Transportation Club hosted its Spring Networking event on Thursday of last week at the Royal Canadian Pavilion in Calgary, Canada, bringing together professionals from across the rail, logistics, and transportation sectors. Cyndi from PFL’s Calgary office was in attendance. The conversations on the floor reflected an industry navigating some real headwinds. Here is what people were talking about:

Service performance came up throughout the evening. Grain car delivery performance has remained below 90% for nine consecutive weeks as of late March 2026, a trend attendees acknowledged is worth watching closely as the spring shipping season gets underway.

The topic generating the most discussion was labour uncertainty heading into the next two years. With collective agreements covering tens of thousands of Canadian rail workers expiring over the next 24 months, the room was candid about the risk. Potential work stoppages could affect over $1 billion worth of goods daily, a number the Canadian Chamber of Commerce has been vocal about. The federal government is exploring binding arbitration to manage the risk, but the industry is watching nervously, particularly after the disruptions of 2024.

One bright spot that came up in conversation was the federal government’s temporary suspension of the fuel excise tax on diesel and gasoline running April through September 2026, welcome cost relief for carriers and shippers dealing with elevated global fuel prices.

We Are Watching Tank Car Tariffs

Folks, the lead story this week for everyone in our world is the inclusion of rail tank cars under Section 232. The 25% tariff on the full value of imported tank railcars under HTS 8606.10.0000, along with a matching 25% tariff on axles, wheels, and couplers, took effect on April 6th. The order explicitly supersedes the USMCA exemptions that previously allowed duty-free import of Mexican-built tank cars and components, and that is where the immediate pain is going to land.

Union Tank Car, which builds exclusively at its Alexandria, Louisiana plant, requested the inclusion back in September of last year. Roughly 75% of competitor tank car production sits in Mexico. Greenbrier and Trinity, both with significant Mexican capacity, sent letters of opposition. Union Tank won. Senator Bill Cassidy of Louisiana took a victory lap two weeks ago, claiming credit for protecting the 350 jobs in Alexandria. The political optics are clear, but the practical effect is that builders with Mexican exposure will pass the 25% straight through to shippers ordering new equipment.

This is a cost story for PFL’s customers, full stop. New build economics that were already strained by steel prices and a thin tank car backlog now have another twenty-five points loaded on top of any car with Mexican content. Existing equipment values just got a meaningful tailwind, lease renewals are about to get more interesting, and the tariff is not getting repealed any time soon. PFL is fielding calls from shippers trying to figure out whether to pull forward 2027 and 2028 orders or wait it out. There is no clean answer, but the calculus has shifted hard in favor of locking down what you can today. We are happy to walk through fleet implications with anyone who wants the conversation.

We Are Watching Hormuz

The Iran war is now in its ninth week and oil markets are still struggling to figure out where the range is. WTI closed Friday around $97 per barrel and Brent around $106, with both up roughly 15% on the week alone. Year-to-date WTI is up about 65% and Brent up 73%, with the Strait of Hormuz still effectively closed and no end-state in sight on the US-Iran negotiations.

President Trump extended the ceasefire indefinitely while Washington waits for a new formal proposal from Tehran, but the naval blockade on Iranian ports stays in place. On Thursday, Trump posted on Truth Social that he had ordered the U.S. Navy to “shoot and kill” any vessel laying mines in the Strait. U.S. forces also boarded a sanctioned tanker carrying Iranian crude in the Indian Ocean last week. The IEA’s April Oil Market Report has shipments through the Strait running at 3.8 million barrels per day versus more than 20 million before the crisis, and the market continues to read every headline as escalation rather than resolution.

On the policy side, Trump extended the energy-specific Jones Act waiver by 90 days last week, pushing the expiration to August 15. Phillips 66 has already used it to load 300,000 barrels of Bakken crude on a Malta-flagged Panamex at its Nederland terminal in Texas and deliver it to Monroe Energy’s 190,000 b/d Trainer refinery in Pennsylvania, which Delta Air Lines owns. At least 15 foreign-flagged vessels have moved more than 2.7 million barrels of crude and products under the waiver since it was first issued in March. The waiver is the kind of administrative tool that can disappear with a single executive order once the Iran situation is resolved

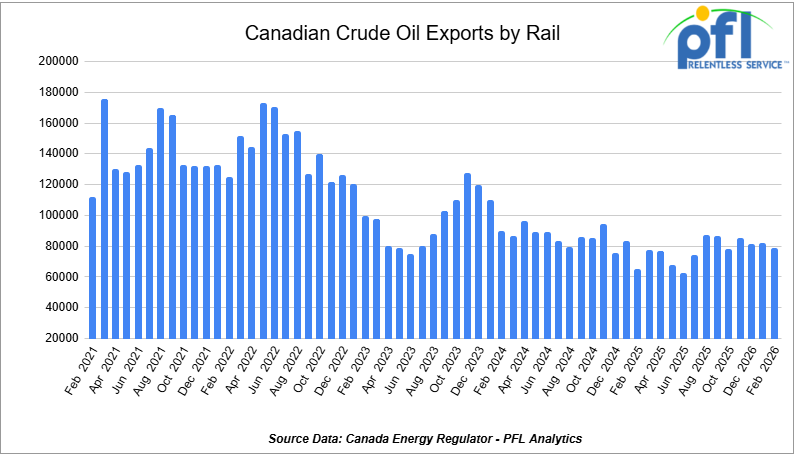

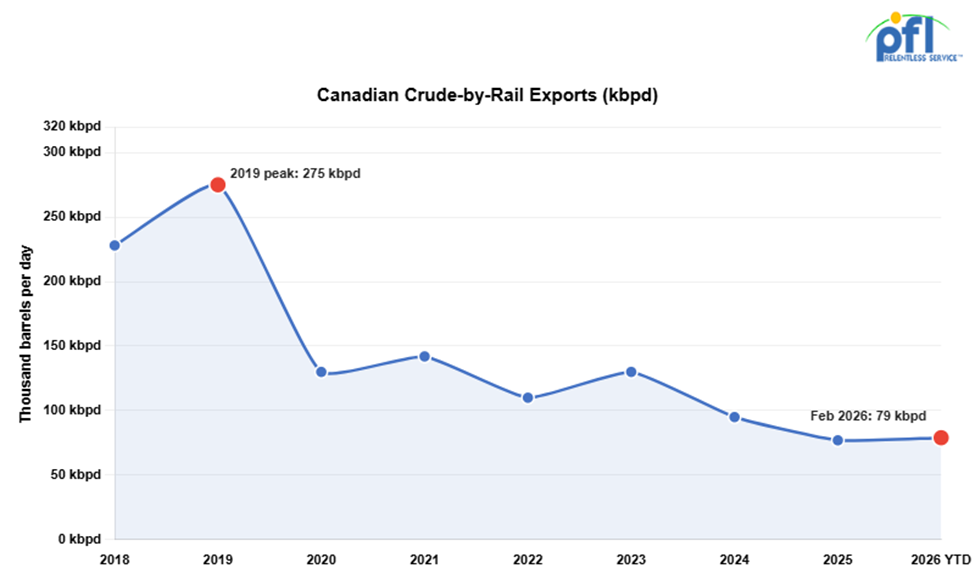

We are Watching Canadian Crude Oil Exports by Rail

The Canadian Energy regulator reported on April 20, 2026, that 79,057 barrels were exported during the month of February 2026, down from 82,183 barrels in January of 2026, a decrease of -3,126 barrels per day month-over-month and its lowest level since October of 2025.

Crude by rail will always be necessary out of Canada for stranded oil not connected by pipelines. Raw bitumen, which is shipped as a non-haz product and is not able to flow in pipelines, is competitive with pipeline tolls and is a growing market to keep an eye on, particularly in light of Strathcona and Gibson announcing new projects. Other factors would be existing long-term contractual commitments and basis – we really need to see basis WTI-CMA (West Texas Intermediate – Calendar Month Average) blowout to -18 per barrel for sustained periods of time to make economic sense. Current rail rates from Alberta to the U.S. Gulf Coast have averaged $15.36 per barrel, making rail competitive whenever WCS-WTI spreads exceed $18 per barrel, including quality adjustments.

We Are Watching Enbridge

Enbridge notified shippers last week that it will apportion May heavy crude nominations on the 3.1 million b/d Mainline by 14% at Superior, Wisconsin, the same level as April and the highest reading since before TMX came on line in May 2024. Light crude at Kerrobert was apportioned 15%. The Chicago WCS 6-3-2-1 crack averaged around $50 per barrel during the May trading cycle, and US Gulf netbacks for Canadian heavy were profitable for most sellers, which is what is driving the demand for Mainline space.

Trans Mountain is running close to capacity on Asian and US west coast pull, so the relief valve that should be taking pressure off the Mainline is not there. Western Canadian production continues to grow at roughly 2% to 4% per year, and existing pipeline egress out of the basin is on track to be fully utilized by the end of this year. Cold weather and seasonal diluent requirements will tighten effective pipeline capacity for bitumen further heading into next winter. Without new long-haul pipeline capacity in service before 2027, the math leaves rail as the only takeaway option for incremental Western Canadian production.

In other Enbridge news, two big stories landed inside 48 hours last week. On Friday of last week, Ottawa approved Enbridge’s $4 billion Sunrise natural gas expansion, adding 300 million cubic feet per day to the Westcoast system that runs from northeast BC and northwest Alberta to the Canada-US border. Construction starts in July with in-service targeted for late 2028. The project has 38 First Nations partners. This is the first major pipeline approval of the Carney era, and CEO Greg Ebel pointedly noted on Friday of last week that the project has been four years in development and still does not have a shovel in the ground.

Earlier in the week, the U.S. Supreme Court ruled unanimously against Enbridge in the Line 5 jurisdictional fight, sending the Michigan attorney general’s case back to state court. Justice Sotomayor wrote that Enbridge waited 887 days to file its motion to remove the case to federal court, well past the 30-day statutory window. Michigan’s Governor Gretchen Whitmer and AG Dana Nessel have been trying to shut down the 540,000 b/d Line 5 since 2019 on public-trust and environmental grounds, and state court is the venue she has wanted from day one.

Line 5 carries mostly Canadian volumes through Michigan to refineries in Ohio, Pennsylvania, Ontario, and Quebec, with NGLs feeding a Sarnia complex. The Mackinac tunnel replacement project is being fast-tracked under a 2025 presidential order, but the underlying state court fight just got a green light to proceed. If Line 5 is forced down for any period of time, the displacement question for tank cars hauling crude and NGLs into the eastern refining footprint becomes immediate and very large – too large to handle in our opinion. PFL has been watching this one for years and thought common sense would come to light at some point. It appears it has not! Stay tuned to PFL for further updates.

We Are Watching Left Wing Carney

Two stories on the prime minister this week. First, the IEA release commitment Canada made back in March turned out to be largely a fiction. The promised 23.6 million barrels was just natural production growth that was already baked in for summer 2026, regardless of the Iran crisis. Canada is the only G7 nation without a strategic petroleum reserve, and when the global system needed real barrels in March, all Ottawa could offer was a relabeling of barrels that were coming anyway.

Second, as we covered last week, Carney met with Manitoba Premier Wab Kinew and laid down what Kinew described publicly as an “aggressive” ultimatum on the Port of Churchill expansion: get LNG flowing within four years or federal support comes off the table. Kinew, to his credit, was honest about it, telling reporters that if the project does not move in that timeline “the ship will probably sail and Manitoba won’t see that benefit.” You cannot deliver LNG out of Hudson Bay in four years through brand new infrastructure across treaty land with no anchor shipper signed and no FID announced.

Meanwhile, Alberta is not waiting. Premier Smith waived the 3% tariff on diluted bitumen exports to South Korea last week, signed an MOU with Hanwha Group covering energy and defense investment, and confirmed her June deadline to submit a 1 million b/d west coast pipeline proposal to the Major Projects Office. Alberta exported about C$400 million worth of crude to South Korea in 2025 and expects that to grow to as much as C$1 billion annually under the new arrangement. Smith is signing actual deals with actual buyers while Carney issues four-year ultimatums on infrastructure he has done nothing to enable.

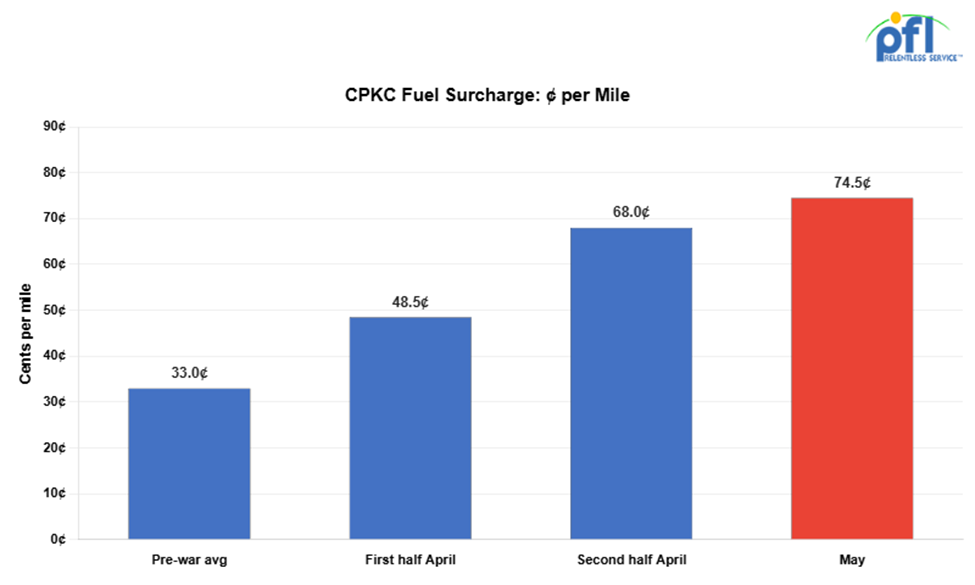

We Are Watching Surcharges

Following up on last week’s coverage of the U.S. Class I surcharge moves, the Canadian carriers are now stepping up similarly. CPKC’s surcharge averaged 33 cents per mile before the Iran war, climbed to 48.5 cents per mile in the first half of April, and 68 cents per mile in the back half. The May surcharge will be 74.5 cents per mile, more than double the pre-war level.

The driver is diesel. UP confirmed on its Q1 earnings call last Thursday that diesel is now running over $4 per gallon in April, well above the $2.35 the carrier had originally forecast in January. CN’s surcharge formula is moving in lockstep, and Class I shippers across the network are absorbing fuel pass-through that no one had budgeted for at the start of the year.

For PFL’s Western Canadian LPG customers, this is a direct hit. Edmonton propane volumes move by rail to British Columbia for export and to U.S. midcontinent destinations, and the route is long enough that the per-mile surcharge translates into real cents per gallon. The arithmetic flows back to producers through softer Edmonton bids as buyers compensate for higher transport. Edmonton propane has averaged a 16.2 cent per gallon discount to Conway in April, and the May surcharge step-up will widen that discount further as buyers price in the higher freight. Western Canadian propane stocks were 21.3% above year-earlier levels at the start of April, so the supply side is not going to absorb the cost. PFL’s NGL fleet customers should expect Q2 economics to look meaningfully different from what was modeled at the start of the year.

We Are Watching the UP/NS Merger

The revised UP-NS merger application is due at the STB this Thursday, April 30. UP and Norfolk Southern have had two months since the original 7,000-page application got rejected in January as incomplete, and the industry is waiting to see whether the carriers actually addressed the deficiencies that BNSF, CSX, CN, and CPKC ripped apart in their December and January filings.

Union Pacific reported Q1 earnings on Thursday and the merger overhang showed up in the numbers. Net income came in at $1.7 billion or $2.87 per diluted share, with merger costs of $36 million or six cents a share weighing on results. CFO Jennifer Hamann acknowledged on the call that diesel is now running over $4 per gallon in April, well above the $2.35 originally forecast in January, which sets up margin pressure heading into Q2. CSX, which reported on Tuesday, raised full-year revenue guidance to mid-single-digit growth on the back of fuel costs and noted that shippers are looking more to rail conversion as truck and fuel costs climb.

The first application failed on basic completeness, not on the merits. Truck diversion data was missing, network maps glossed over overlapping lines, and entire appendices of the merger agreement were left out. The substantive opposition from the rest of the Class I network and major shipper groups has only firmed up since January. If the STB accepts the revised filing as complete in May or June of this year, the formal review starts the clock and a substantive decision will land well into 2027. For tank car owners and lessors, that strategic uncertainty around what the eastern half of the North American rail map looks like in 2028 is going to keep some shippers from committing to long-term lease structures and corridor-specific equipment buys.

We Are Watching Bridger

Comments on the Bridger Pipeline scoping process close on Friday, May 1. Bridger Pipeline LLC, owned by True Companies out of Casper, has filed plans for a 36-inch line running 647 miles from the Canadian border in Phillips County, Montana, south to a terminal at Guernsey, Wyoming. Initial throughput is 550,000 barrels per day with maximum capacity of 1.13 million bpd. The project carries a price tag of roughly $2 billion.

Bridger is positioning itself as the natural U.S. partner for South Bow’s revival of portions of Keystone XL. The Guernsey terminal is not an end market on its own, so the project will need additional connections to Cushing, Patoka, or the Gulf Coast to actually make sense. The route maps include potential tie-ins to Bakken gathering, which gives the project real optionality even before the Canadian crude piece is firmed up. If Trump approves the Presidential Permit and South Bow’s Keystone XL revival gets the corresponding green light, Canadian crude exports to the U.S. could rise by more than 12%.

Construction is years away even in the best case, and the EIS process has barely started. The longer-term takeaway is that any Canadian shipper serious about a multi-year crude rail strategy needs to be modeling the scenario where Bridger and an Alberta-to-BC pipeline both get built late in the decade. PFL is following the scoping comments and the Presidential Permit timeline closely. If you want our read on what this means for your fleet positioning, give us a call.

Lease Bids

- 100, 21.9K 117J Tanks located off of All Class 1s in Midwest. For use in CO2 service. Period: 6 months.

- 30-50, 30K 117J Tanks located off of NS or CSX in Northeast. For use in C5 service. Period: 1 year.

- 20-50, 4000-5000 Covered Hoppers located off of UP or BN in Houston. For use in Urea, Potash, Ammonium Sulfate service. Period: 6-12 Months.

- 200, 33K Pressure Tanks located off of CSX or NS in Ohio. For use in Propylene service. Period: 18 Months.

- 30-50, 25.5K DOT 111 Tanks located off of All Class 1s in Anywhere. For use in Asphalt service. Period: 1-3 Years.

- 40, 33K Pressure Tanks located off of UP in Eunice, LA. For use in Propane service. Period: 1 Year.

- 40, 29K DOT 111 Tanks located off of UP or BN in Midwest. For use in Veg Oil service. Period: 5 Year.

- 70, 30K DOT 117 Tanks located off of NS or CSX in Ohio. For use in Diesel service. Period: 3 months.

- 100, 33K Pressure Tanks located off of UP or BN in Texas. For use in Propane service. Period: 6 Months.

- 20, DOT 117J Tanks located off of NS, CSX, CN, or CPKC in Various. For use in C5 service. Period: 1 year. Need gauge rods.

- 50, 30K DOT 117J Tanks located off of CP or CN in Canada. For use in Jet Fuel service. Period: 1 Year.

Sales Bids

- 28, 3400CF Covered Hoppers located off of UP BN in Texas. For use in Cement service. Cement Gates needed.

- 20, 17K DOT111 Tanks located off of various class 1s in various locations. For use in corn syrup service.

- 120, Various Open-Top Aluminum Rotary Gondolas located off of various class 1s in various locations. For use in Sulphur service. Built 2004 or later.

- 30, 29K DOT111 Tanks located off of various class 1s in Chicago. For use in Veg Oil service.

Lease Offers

- 106, 31.8K CPC1232 Tanks located off of UP or BN in Texas. Last used in Diesel.

- 20, 31.8K DOT117R Tanks located off of UP or BN in Texas. Last used in Diesel.

- 86, 29K DOT117R Tanks located off of UP or BN in Texas. Last used in Gasoline. Coiled and Insulated.

- 21, 6351 Covered Hoppers located off of CN in Wisconsin. Last used in DDG. Available until February 2027.

- 29, 6500 Covered Hoppers located off of CN in Wisconsin. Last used in DDG. Available until February 2027.

- 50, 20K DOT117J Tanks located off of All Class 1s in Moving. Last used in Styrene.

- 29, 25.5K DOT117J Tanks located off of UP or BN in Texas. Cars are currently clean. Cars are currently clean.

- 50, 30K DOT117J Tanks located off of UP or BN in Corpus Christie. Last used in Diesel.

- 200, 340W DOT 112J Tanks located off of All Class 1s in Multiple Locations. Last used in Propane and Butane. Cars are currently clean.

- 15, 6200CF Covered Hoppers located off of All Class 1s in Wisconsin. Last used in Plastic. Cars are currently clean.

- 30, 6500CF Covered Hoppers located off of All Class 1s in Wisconsin. Last used in Plastic. Cars are currently clean.

- 24, 21K Stainless Steel Tanks located off of UP in Texas / Mexico Border. Last used in SULFACTANT. Cars are currently clean.

- 34, 30K DOT 111 Tanks located off of UP in Texas / Mexico Border. Last used in Veg Oil. Cars are currently clean.

- 117, 30K DOT117R Tanks located off of UP or BN in Texas. Last used in Gasoline.

- 100, 28.4K DOT 117J Tanks located off of UP or BN in Beaumont, TX. Cars are currently clean.

- 50, 30K DOT117J Tanks located off of UP or BN in the South. Last used in Ethanol.

Sales Offers

- 81, 31.8K CPC1232 Tanks located off of UP or BN in TX. Last used in Multiple. Requal Due in 2025.

- 35, 3400CF Covered Hoppers located off of UP or BN in Midwest. Last used in Sand.

- 25, 30K 117J Tanks located off of CSX in Jackson, TN. Last used in Fuels. Newly Requalified.

Call PFL today to discuss your needs and our availability and market reach. Whether you are looking to lease cars, lease out cars, buy cars, or sell cars call PFL today at 239-390-2885

Live Railcar Markets

| CAT | Type | Capacity | GRL | QTY | LOC | Class | Prev. Use | Offer | Note |

|---|

PFL will be at the Following Conferences

- Where: Calgary

- Attending: David Cohen (954-729-4774), Curtis Chandler(239-405-3365), Cyndi Popov (403-402-5043)

- Where: Grand Geneva Resort

- Attending: Brian Baker (239.297.4519)

- Conference Website

- Where: Loews Arlington Hotel

- Attending: Brian Baker (239.297.4519), David Cohen (954-729-4774), and Curtis Chandler (239-405-3365)

- Conference Website

- Where: The Westin Galleria Dallas

- Attending: David Cohen (954-729-4774), and Curtis Chandler (239-405-3365)

- Conference Website

- Where: The Westin Galleria Dallas

- Attending: Brian Baker (239.297.4519)

- Conference Website