“The quality of a leader is reflected in the standards they set for themselves.”

– Ray Kroc

Jobs Update

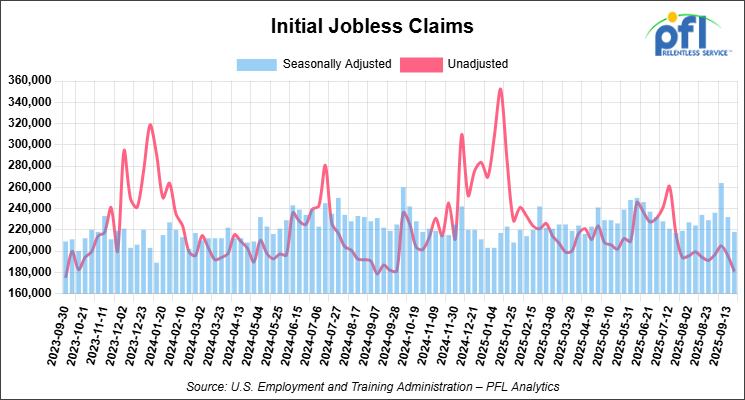

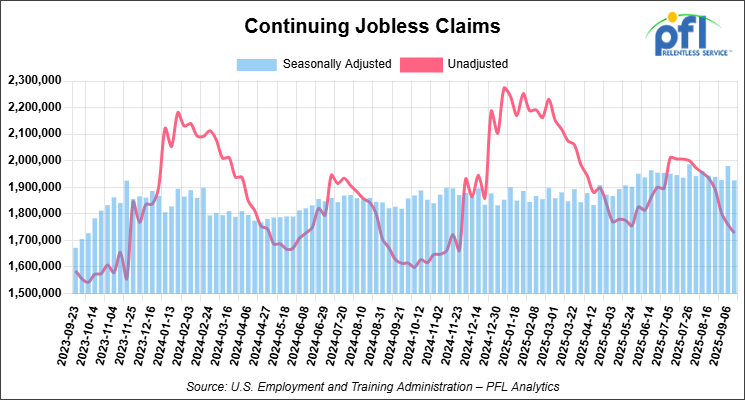

• Initial jobless claims seasonally adjusted for the week ending September 20, 2025 came in at 218,000, versus the adjusted number of 232,000 people from the week prior, down 14,000 people week over week.

• Continuing jobless claims came in at 1,926,000, versus the adjusted number of 1,980,000 people from the week prior, down 54,000 week-over-week.

Stocks closed higher on Friday of last week, but lower week-over-week

The DOW closed higher on Friday of last week, up 299.97 points (0.65%), closing out the week at 46,247.29, down -67.28 points week-over-week. The S&P 500 closed higher on Friday of last week, up 38.98 points (0.59%), and closed out the week at 6,643.70, down -20.66 points week-over-week. The NASDAQ closed higher on Friday of last week, up 99.37 points (0.44%), and closed out the week at 22,484.07, down -147.41 points week-over-week.

In overnight trading, DOW futures traded higher and are expected to open at 46,747 this morning, up 191 points from Friday’s close.

Crude oil closed higher on Friday of last week, and higher week-over-week

West Texas Intermediate (WTI) crude closed up +79 cents per barrel (1.02%), to close at $65.72 per barrel on Friday of last week, up $3.04 per barrel week-over-week. Brent crude closed up +74 cents per barrel (1.14%), to close at $70.10 per barrel, up $3.42 per barrel week-over-week.

One Exchange WCS (Western Canadian Select) for November delivery settled on Friday of last week at US$11.10 below the WTI-CMA (West Texas Intermediate – Calendar Month Average). The implied value was US$53.17 per barrel.

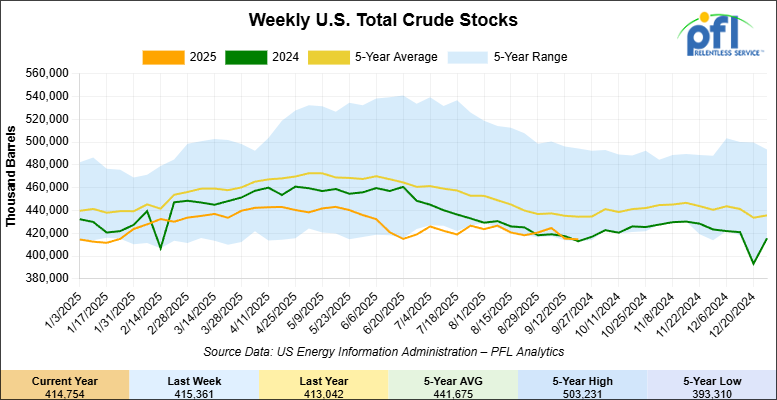

U.S. commercial crude oil inventories (excluding those in the Strategic Petroleum Reserve) decreased by 600,000 barrels week-over-week. At 414.8 million barrels, U.S. crude oil inventories are 4% below the five-year average for this time of year.

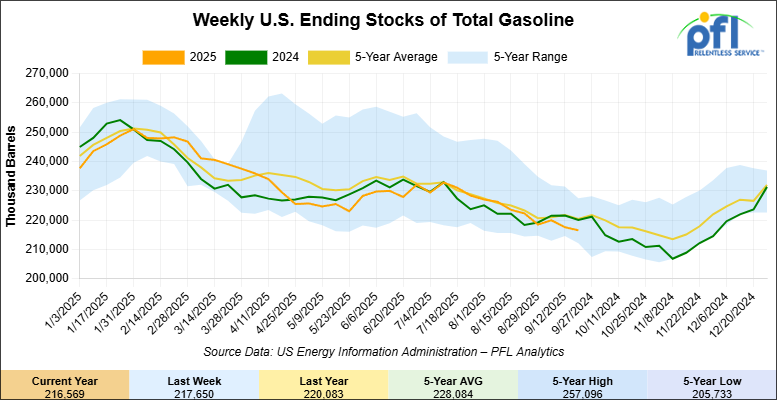

Total motor gasoline inventories decreased by 1.1 million barrels week-over-week and are 2% below the five-year average for this time of year.

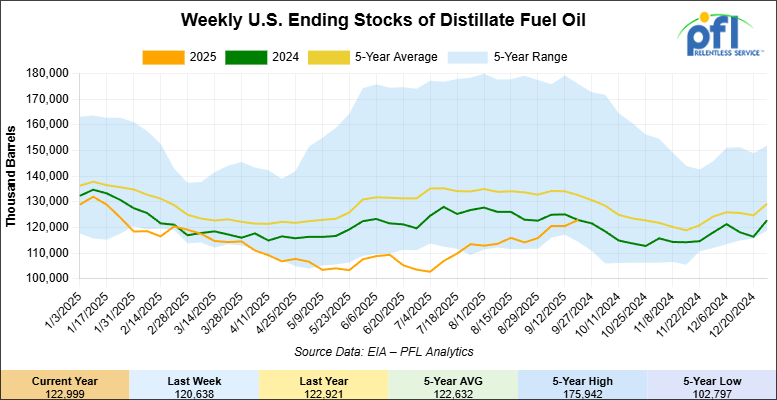

Distillate fuel inventories decreased by 1.7 million barrels week-over-week and are 8% below the five-year average for this time of year.

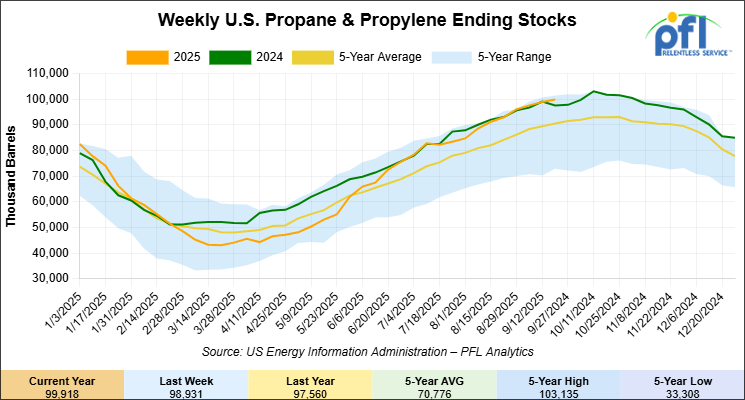

Propane/propylene inventories increased by 1 million barrels week-over-week and are 12% above the five-year average for this time of year.

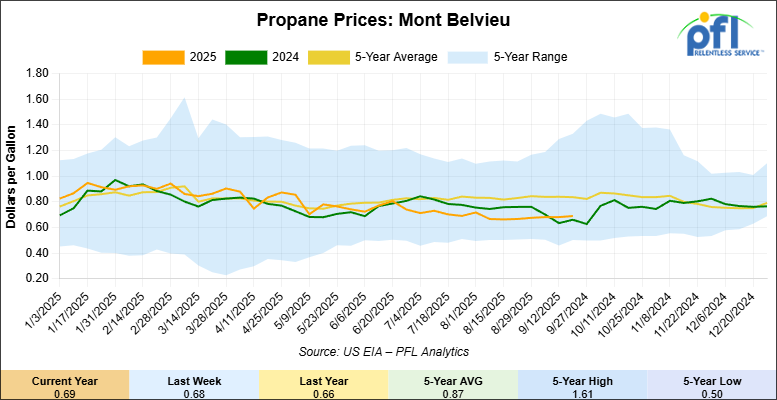

Propane prices closed at 69 cents per gallon on Friday of last week, up 1 cent week-over-week and up 3 cents per gallon year-over-year.

Overall, total commercial petroleum inventories decreased by 500,000 barrels during the week ending September 19, 2025.

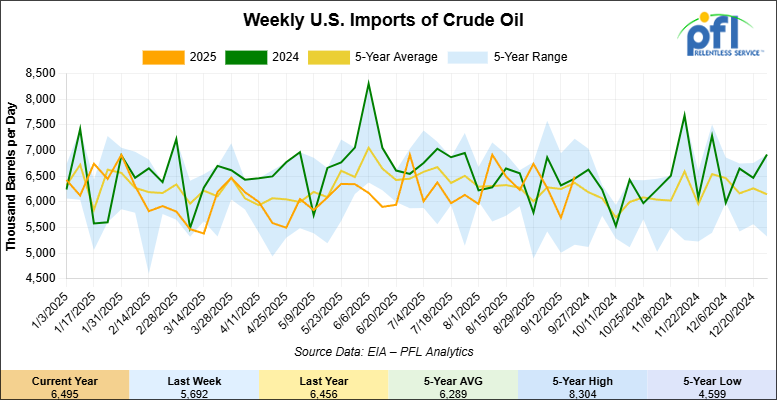

U.S. crude oil imports averaged 6.5 million barrels per day during the week ending September 19, 2025, an increase of 803,000 barrels per day week-over-week. Over the past four weeks, crude oil imports averaged 6.3 million barrels per day, 0.9% less than the same four-week period last year. Total motor gasoline imports (including both finished gasoline and gasoline blending components) averaged 506,000 barrels per day, and distillate fuel imports averaged 69,000 barrels per day during the week ending September 19, 2025.

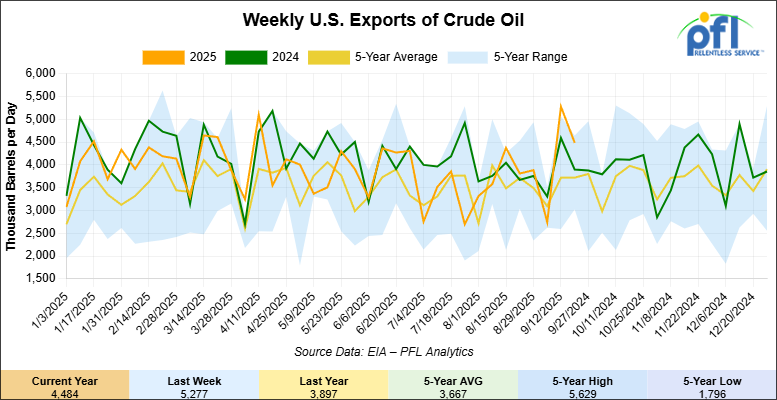

U.S. crude oil exports averaged 4.484 million barrels per day during the week ending September 19, 2025, a decrease of 793,000 barrels per day week-over-week. Over the past four weeks, crude oil exports averaged 4.098 million barrels per day.

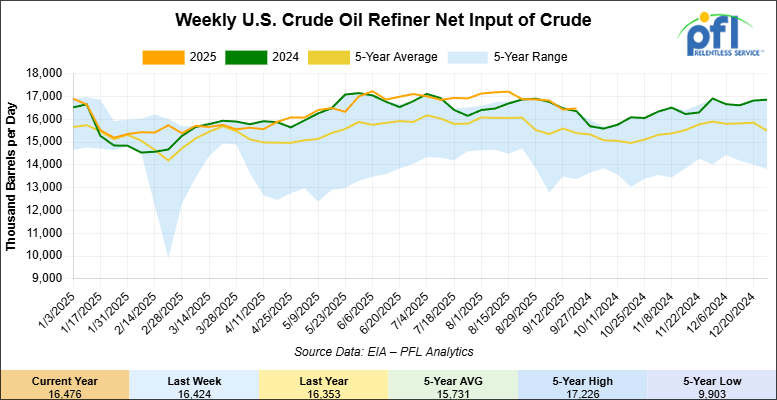

U.S. crude oil refinery inputs averaged 16.5 million barrels per day during the week ending September 19, 2025, which was 52,000 barrels per day more week-over-week.

WTI futures are poised to open at $64.47, down 1.25 cents from Friday’s close.

North American Rail Traffic

Week Ending September 24, 2025:

Total North American weekly rail volumes were down (-3.62%) in week 39, compared with the same week last year. Total Carloads for the week ending September 24, 2025 were 324,445, down (-2.05%) compared with the same week in 2024, while weekly Intermodal volume was 340,982, down (-5.06%) year over year. 9 of the AAR’s 11 major traffic categories posted year-over-year decreases. The largest decrease came from Forest Products (-18.02%), while the largest increase was Grain (+5.54%).

In the East, CSX’s total volumes were up (+1.93%), with the largest decrease coming from Forest Products (-17.17%), while the largest increase came from Intermodal Units (+7.61%). NS’s total volumes were down (-5.00%), with the largest increase coming from Motor Vehicles and Parts (+7.78%), while the largest decrease came from Coal (-25.51%).

In the West, BNSF’s total volumes were down (-1.11%), with the largest increase coming from Coal (+35.31%), while the largest decrease came from Chemicals (-9.02%). UP’s total volumes were down (-5.81%), with the largest increase coming from Grain (+42.44%), while the largest decrease came from Intermodal Units (-15.62%).

In Canada, CN’s total volumes were down (-2.59%), with the largest increase coming from Coal (+35.31%), while the largest decrease came from Other (-32.65%). CPKCS’s total volumes were down (-19.55%), with the largest increase coming from Nonmetallic Minerals (+5.77%), while the largest decrease came from Forest Products (-65.54%).

The most recent AAR data shows grain carloads hit 23,147 for the week ending September 24, representing the strongest grain rail performance in recent weeks as harvest activity accelerates. This marks a 2,170 carload increase compared to the same week in 2024, while most other rail freight categories declined.

The timing is critical as secondary railcar auction bids reached $297 above published tariff rates during the week ending September 18, according to the latest USDA Grain Transportation Report published on September 25. This represents a dramatic spike in railcar premiums as grain shippers compete aggressively for limited equipment during peak harvest season.

Current rail capacity indicators show significant strain. The latest transportation data reveals diesel fuel prices for grain transport climbed to $3.749 per gallon for the week ending September 24, up 21 cents from last year. More importantly, 37 oceangoing grain vessels loaded during the week ending September 18 – 48% more than the same period last year, indicating strong export demand that requires massive inland rail movements to Gulf Coast ports.

When grain shippers are paying $297 premiums over published rates, it signals network congestion that affects all freight categories during the narrow harvest window.

USDA’s latest crop projections, released on September 12, show why rail demand is so intense. The agency confirmed a record 16.814-billion-bushel corn harvest from the most acres planted since 1933. Yet harvest completion remains minimal and recent crop progress reports show the vast majority of this record crop still awaits transport to market.

The October-November peak shipping season lies directly ahead, meaning current capacity pressures will intensify before seasonal demand moderates. Rail networks already operating near capacity during harvest season create bottlenecks that force energy shippers to compete not just with other petroleum products, but with agricultural commodities commanding premium rates during time-sensitive harvest periods.

Current rail economics favor grain during harvest season, as demonstrated by the willingness to pay nearly $300 above standard rates for equipment access. This pricing power reflects agriculture’s seasonal urgency – farmers must move crops before winter weather limits rural elevator access.

Source Data: AAR – PFL Analytics

Rig Count

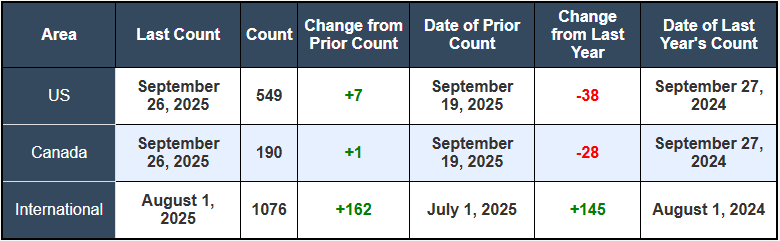

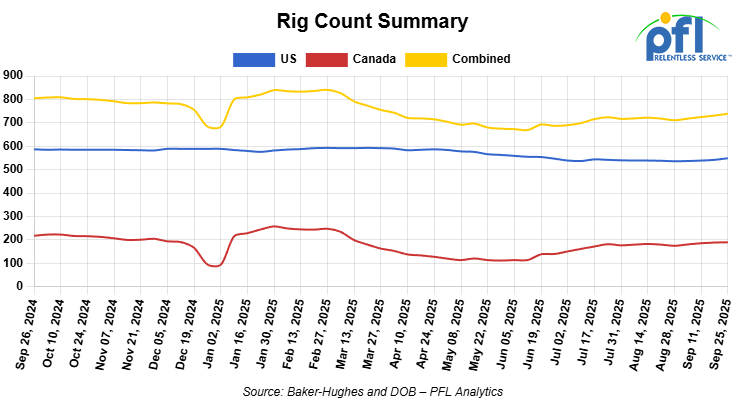

North American rig count was up by +8 rigs week-over-week. The US rig count was up by +7 rigs week-over-week, but down by -38 rigs year-over-year. The US currently has 549 active rigs. Canada’s rig count was up by +1 rig week-over-week, but down by -28 rigs year-over-year. Canada currently has 190 active rigs. Overall, year-over-year we are down by -66 rigs collectively.

North American Rig Count Summary

We are watching a few things out there for you:

We are Watching Natural Gas In Canada

Remember when oil prices went negative not so long ago here in the U.S.? Well Western Canadian natural gas hit unprecedented territory last week as AECO (Trading Hub) spot prices crashed to negative $0.18 per $USMMBtu on Thursday of last week, marking four consecutive days of sub-zero pricing. The collapse has triggered an immediate response from producers across Alberta, with Advantage Energy, ARC Resources, and Pine Cliff Energy all announcing aggressive well shut-ins as the economics of production completely deteriorated.

The pricing catastrophe stems from a perfect storm of oversupply, warm weather and infrastructure constraints. Western Canadian gas storage sits at 90% capacity – 20% above the five-year average for this time of year, and lack of pipeline capacity. Canada’s LNG ramp-up has proceeded slower than anticipated. With limited pipeline takeaway capacity and no market outlet producers continued to drill associated gas wells (wells that contain oil, natural gas liquids, natural gas and oil) alongside oil wells, in the anticipation of Shell led LNG Canada being a market outlet but has faced problems and it ramps up production. The market has effectively broken down for the time being.

For railcar operators, this infrastructure bottleneck demonstrates exactly why transportation flexibility commands premiums. While AECO trades at negative pricing, Henry Hub closed at $2.835 per MMBtu on Friday of last week—a spread of over $3.00 per $USMMBTU created purely by pipeline constraints. When producers shut in gas wells, associated oil production often follows.

The collapse also highlights broader energy infrastructure fragmentation across North America. Natural gas liquids pricing remains supported despite the natural gas crash, as NGL transportation by rail maintains optionality that pipeline-dependent gas lacks. Western Canadian gas producers are essentially paying customers to take their product, while rail-accessible regions maintain pricing power through transport flexibility.

We are watching Petroleum Carloads

The four-week rolling average of petroleum carloads carried on the six largest North American railroads declined to 28,680 from 28,688 which was a decrease of -8 rail cars week-over-week. Canadian volumes were lower. CPKC’s shipments were lower by -10.0% week over week, CN’s volumes were lower by -1.0.% week-over-week. U.S. shipments were mixed. The CSX had the largest percentage increase and was up by +3.0%. The NS had the largest percentage decrease and was down by -16%.

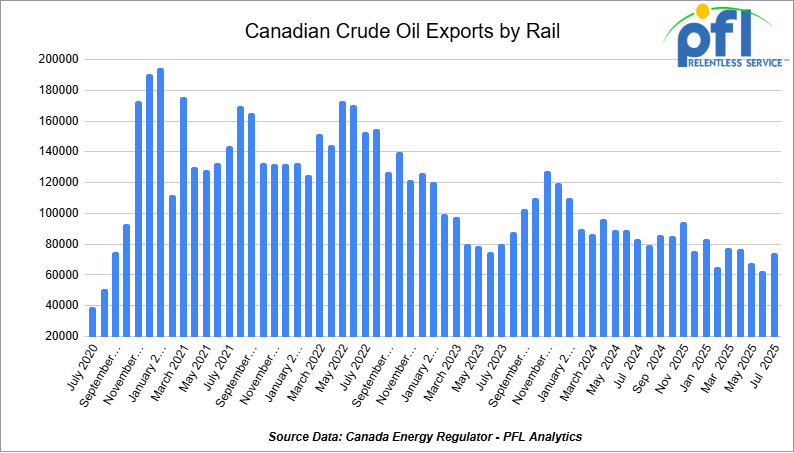

We are watching Canadian Crude by Rail

Crude by rail out of Canada increased month over month. The Canadian Energy regulator reported on September 25, that 74,031 barrels were exported per day during the month of July 2025, up from 62,847 barrels in June of 2025, an increase of 11,184 barrels per day, month over month after two consecutive month-over-month declines.

Crude by rail will always be necessary out of Canada for stranded oil not connected by pipelines. Raw bitumen, which is shipped as a non-haz product and is not able to flow in pipelines, is competitive with pipeline tolls and is a growing market to keep an eye on. Other factors would be existing long-term contractual commitments and basis – we really need to see basis WTI-CMA (West Texas Intermediate – Calendar Month Average) blowout to -18 per barrel for sustained periods of time to make economic sense. Current rail rates from Alberta to the U.S. Gulf Coast has averaged $15.36 per barrel, making rail competitive whenever WCS-WTI spreads exceed $18 per barrel including quality adjustments.

Tank car lease rates for non-pressurized units remained stable, despite increased crude oil activity. This suggests adequate equipment supply for current market conditions.

Though there may be some slack in the system right now, Enbridge surprised the market by accepting all pipeline nominations on their 3 million barrel per day mainline system for October after months of not doing so. Room remains on Transmountain pipeline and production continues to grow in Alberta. At some point, we will hit a wall where crude will be trapped. It is really anybody’s guess.

Here in the U.S., Crude oil price volatility accelerated last week, with Bakken crude jumping $3.12 to $65.18 per barrel. The price movements reflect broader market uncertainty about global supply balances and domestic production trends.

Venezuelan heavy crude has resumed flowing to U.S. Gulf Coast refineries following the Trump administration’s sanctions relief, creating additional competition for Canadian heavy oil that typically moves by rail. However, Venezuelan supply remains limited to existing production capacity. Canadian output continues to grow as oil sands projects ramp up production. Stay tuned to PFL for further details, we are watching this one closely.

We continue to watch MEG Energy

The battle for MEG Energy reached a decisive moment last week when Institutional Shareholder Services recommended that MEG shareholders vote in favor of Cenovus’ $8.3 billion takeover, dealing a potentially fatal blow to Strathcona Resources’ hostile bid. The ISS endorsement came just 12 days before the October 9 shareholder vote, significantly tilting momentum toward the Cenovus deal.

ISS analysts concluded that Cenovus’ offer of $27.50 per share provides “fair value” while Strathcona’s all-stock bid exposes shareholders to “execution risk.” The advisory firm specifically cited concerns about Strathcona’s debt levels and operational track record compared to Cenovus’ established oil sands expertise. Strathcona immediately fired back, calling the ISS analysis “fundamentally flawed,” but proxy advisory firms carry significant weight with institutional investors.

The merger outcome will reshape Canadian oil sands production and transportation patterns for years to come. A combined Cenovus-MEG entity would control 555,000 barrels per day of heavy oil production, creating the second-largest oil sands operator behind only Canadian Natural Resources. This scale provides enormous leverage over pipeline allocations, rail transport decisions, and crude pricing negotiations.

For railcar operators, consolidation typically means fewer but larger shippers with enhanced negotiating power. The combined entity would likely optimize transportation costs through long-term pipeline commitments, using rail primarily for surge volumes and spot market opportunities. However, operational flexibility becomes more valuable as larger producers seek to maximize margins across multiple transportation modes.

MEG’s existing pipeline commitments include 100,000 barrels per day on Enbridge’s Flanagan South and 20,000 barrels per day on Trans Mountain. Cenovus would inherit these allocations while adding its own 450,000 barrels per day of production, potentially reducing the combined entity’s reliance on higher-cost rail transport during normal market conditions.

We continue to watch Enbridge Line 5

The Trump Administration stepped directly into the Great Lakes pipeline battle last week, filing a federal brief supporting Enbridge’s Line 5 operation against Left Wing Michigan Governor Gretchen Whitmer’s shutdown attempts. The Department of Justice argued that Michigan’s revocation of the pipeline’s easement “interferes with U.S. foreign policy” and violates the Transit Pipelines Treaty with Canada.

Line 5 carries 540,000 barrels per day of crude oil and natural gas liquids from Superior, Wisconsin, to Sarnia, Ontario, including the controversial 4.5-mile segment beneath the Straits of Mackinac. Michigan has fought to shut down the underwater portion since 2020, citing environmental risks to the Great Lakes, while Enbridge maintains the pipeline is safe and essential for regional energy supply.

The federal intervention significantly strengthens Enbridge’s legal position and demonstrates the Trump Administration’s commitment to North American energy infrastructure and security despite liberal attempts to shut a much-needed pipeline down to advance the “Green Old Deal”. Federal courts generally defer to executive branch foreign policy determinations, particularly involving treaty obligations with neighboring countries.

For railcar operators, Line 5’s continued operation maintains current crude oil and natural gas liquids flow patterns that could otherwise shift to rail transport. The reality of the situation is there are not enough railcars in the market to fill the gap and everyone knows that.

Line 5 supplies refineries in Michigan, Ohio, Pennsylvania, and Ontario that would need alternative supply sources if Line 5 were shut down. Rail transport from western Canada and the Bakken would have to fill much of this gap, potentially benefiting tank car owners and operators but it would take years to build all the rail cars and infrastructure required to fill the gap. On the rail side alone – 1,250 rail cars would need to be delivered every day or 456,250 rail cars a year, with 2 turns a month you would need a fleet of roughly 19,000 rail cars. Does not seem like it would be a good green solution but a windfall for rail.

Line 5’s dual role as both crude oil and NGL carrier means any shutdown would affect multiple commodity flows. The pipeline moves propane, butane, and natural gasoline alongside crude oil, creating potential rail opportunities across several tank car segments if legal challenges ultimately succeed despite federal support.

The DOJ brief comes as Enbridge proceeds with plans for a $500 million tunnel beneath the Straits of Mackinac that would house replacement pipeline segments in a concrete-lined tunnel. Construction has not yet begun, leaving the existing underwater pipeline as the only current transportation option.

We continue to watch the NS and the UP

The proposed $85 billion Union Pacific-Norfolk Southern merger gained significant political and labor backing last week, dramatically improving its regulatory prospects. President Trump endorsed the deal during a September 19th Oval Office meeting with UP’s CEO Jim Vena, telling reporters the merger “sounds good to me.” The presidential backing came just days after the SMART Transportation Division announced its support on September 22, citing job protection guarantees negotiated with Union Pacific.

The union endorsement removes what could have been the largest obstacle to regulatory approval. SMART-TD represents over 125,000 transportation workers and had historically opposed major rail consolidation. The union secured commitments that no SMART-TD member would be furloughed due to the merger, along with enhanced safety training programs and improved working conditions.

However, shipper opposition intensified last week as the Rail Customer Coalition fired back with letters to the Surface Transportation Board warning of reduced competition and higher freight rates. The American Chemistry Council, American Petroleum Institute, and other major shipper groups argued that past rail mergers led to 40% higher freight rates over 20-year periods.

For tank car operators, the merger creates both opportunities and risks. A transcontinental UP-Norfolk Southern network would streamline crude oil movements from the Bakken and Permian to Gulf Coast refineries, potentially improving service reliability and reducing transit times. However, reduced competition between eastern and western rail networks could pressure rates higher, particularly for captive shippers without pipeline alternatives.

The STB filing deadline of January 29, 2026, gives both sides roughly four months to build their cases. With presidential support and labor backing secured, UP and Norfolk Southern have cleared two major regulatory hurdles, leaving shipper opposition as the primary challenge remaining.

We are Watching the Green old deal

The U.S. Department of Energy intends to cancel more than $13 billion in funds that the Biden administration had pledged to subsidize wind, solar, batteries and electric vehicles, it said on Wednesday of last week.

It was not immediately clear which funds were being targeted.

“By returning these funds to the American taxpayer, the Trump administration is affirming its commitment to advancing more affordable, reliable and secure American energy and being more responsible stewards of taxpayer dollars,” the department said.

We see more cuts coming, as the country shifts away from the green old deal. Stay tuned to PFL!

We Continue to watch Canadian Left Wing Prime Minister Carney

Left Wing Prime Minister, Mark Carney, faced his biggest energy policy contradiction last week as Conservatives forced a House vote demanding elimination of the federal oil and gas emissions cap. The confrontation highlighted the growing disconnect between Carney’s “energy superpower” rhetoric and his continued adherence to the climate policies that industry argues make such ambitions impossible.

Conservative MP Andrew Scheer laid out the fundamental contradiction during last Monday’s parliamentary debate: “Simply put, if Liberals vote yes to an emissions cap, they are voting no to a pipeline.” The motion, which demanded immediate cancellation of the 2030 emissions cap, forced left wing Carney’s government to defend policies that even some within Liberal circles privately acknowledge may need revision.

Behind closed doors, a different conversation has been taking place. Reuters reported on September 11 that federal officials have been discussing with Alberta and energy companies the possibility of dropping the emissions cap entirely in exchange for alternative climate commitments. Three sources confirmed the talks, noting that Carney’s stance has “notably shifted” in recent weeks as industry pressure intensifies and investment continues flowing south of the border. We will soon see it is all talk and will continue to be.

The timing of this policy uncertainty could not be more problematic for Canadian energy infrastructure. Last week marked six months since major energy CEOs first sent their “Build Canada Now” letter demanding regulatory changes, and industry frustration has only intensified. A second letter, published by Canadian Natural Resources and Enbridge, warned of “insufficient progress” in stimulating energy investment despite Carney’s campaign promises to streamline approvals.

For railcar operators, this regulatory paralysis creates sustained opportunities. When pipeline developers cannot secure regulatory certainty or long-term policy support, crude oil transport defaults to rail’s inherent flexibility. The emissions cap uncertainty ensures that even willing pipeline investors remain hesitant to commit capital to projects that may face regulatory reversal or production constraints.

Last week’s parliamentary theatrics exposed the fundamental policy incoherence that has defined left wing Carney’s approach to energy since taking office. He campaigns on maintaining climate policies while simultaneously promising to unleash Canadian energy production—a combination that industry executives argue is mathematically impossible. Pierre Poilievre, leader of Canada’s Conservative Government (leader of the opposition), captured this contradiction during last Wednesday’s debate: “Nobody wants to build a pipeline when the government bans you from producing the oil to put into it.”

The market has already rendered its verdict on Carney’s energy superpower aspirations. Canadian energy companies continue trading at significant discounts to U.S. peers, while foreign investment in the oil patch remains minimal despite record production levels. Major pension funds avoid Canadian energy investments, forcing companies to seek capital from U.S. and international sources that remain skeptical of the regulatory environment.

Environmental groups have noticed the policy drift as well. Environmental defense warned last week that Carney has already cancelled consumer carbon pricing, paused electric vehicle standards, and allowed residential retrofit programs to lapse—suggesting a gradual abandonment of climate commitments without the corresponding regulatory clarity that would actually stimulate energy investment.

The emissions cap represents the ultimate test of Carney’s energy credibility. Industry argues the policy effectively caps production growth regardless of technological improvements or carbon capture investments. Yet left wing environmental constituencies view any retreat from the cap as proof that climate commitments were merely electoral positioning rather than genuine policy priorities.

Last week’s Conservative motion failed along party lines, but the underlying policy contradiction remains unresolved. Carney continues promoting “energy superpower” language while maintaining the regulatory framework that industry argues makes such goals unattainable. This ongoing uncertainty benefits rail transport by ensuring that pipeline investment remains constrained by regulatory risk, keeping crude oil dependent on flexible transportation alternatives.

The fundamental question persists: Can Canada become an energy superpower while maintaining policies designed to constrain energy production growth? Until Carney resolves this contradiction with concrete policy changes rather than rhetorical adjustments, rail transport will continue benefiting from the infrastructure bottlenecks created by regulatory uncertainty and investment hesitation.

We are Watching Key Economic Indicators

Consumer Spending

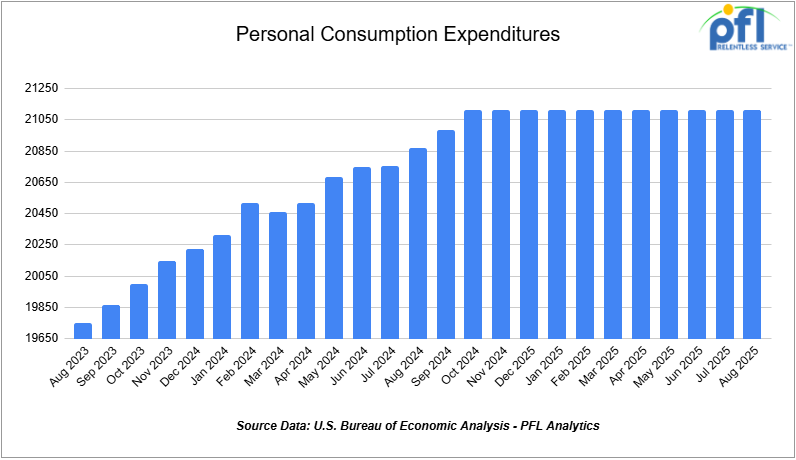

In August 2025, total consumer spending adjusted for inflation increased by 0.4 % over July 2025, up from July’s 0.3 % gain, pointing to continued strength in household demand. According to the U.S. Bureau of Economic Analysis, the increase in current-dollar personal consumption expenditures (PCE) was $129.2 billion, driven by a $77.2 billion rise in services spending and a $52.0 billion increase in goods spending.

The personal savings rate rose to 4.6 % in August, up from 4.4 % (revised) in July, as consumers slightly rebuilt buffers amid elevated price pressures.

Year-over-year, the PCE price index climbed by 2.7%, accelerating from 2.6% in July, while core PCE inflation (excluding food and energy) held at 2.9 %, reflecting persistent inflationary pressures above the Federal Reserve’s 2% target.

Lease Bids

- 30-50, 6000cf Steel Hopper located off of CSX or NS in East. For use in petcoke service. Period: 5 Years.

- 50, 5000CF Covered Hopper located off of UP or BN in Houston. For use in Fertilizer service. Period: 6 Months. Bid: Negotiable.Needed ASAP.

- 10, 2500CF Open Top Hopper located off of UP or BN in Texas. For use in aggregate service. Period: 5 years. Bid: Negotiable.Need Rapid Discharge Doors.

- 10, 25.5K Any Type Tank located off of CSX in Florida. For use in UCO service. Period: 2 Years. Bid: Negotiable.

- 15-20, 29K 117R Tank located off of NS or CSX in Ohio. For use in Ply Oil service. Period: 6-12 Months. Bid: Negotiable.

- 10, 30K 117R or 117J Tank located off of Any Class 1 in USA. For use in Glycerin service. Period: 1 year. Bid: Negotiable.

- 50, 23.5-25.5 DOT111 Tank located off of Any Class 1 in USA. For use in Asphalt service. Period: 5 years. Bid: Negotiable.

- 50-100, 33K 117J Tank located off of BN or UP in Bellview. For use in Butane/ service. Period: Sept-March. Bid: Negotiable.

- 4, 30K 117J Tank located off of Any Class 1 in Michigan. For use in Food Grade Ethanol service. Period: Multi year. Bid: Negotiable.

- 100, 21.9K 117J Tank located off of All Class 1s in Midwest. For use in CO2 service. Period: 6 months. Bid: Negotiable.

- 20, 25.5K Any Type Tank located off of UP in Point Comfort, TX. For use in Diethylene Glycol service. Period: 3-5 Years. Bid: Negotiable.No Lining Required.

- 100, 33K Tank Pressure located off of CN or CP in Canada. For use in Propane service. Period: Winter. Bid: Negotiable.

Sales Bids

- 28, 3400CF Covered Hopper located off of UP BN in Texas. For use in Cement service. Bid: Negotiable.Cement Gates needed..

- 20, 17K Tank DOT111 located off of various class 1s in various locations. For use in corn syrup service. Bid: Negotiable.

- 120, Various Gondola Open-Top Aluminum Rotary located off of various class 1s in various locations. For use in Sulphur service. Bid: Negotiable.Built 2004 or later.

Lease Offers

- 60, 4750 Covered Hoppers located off of UP or BN in Eads, CO. Last used in Grain. Offer: Negotiable. UP to 5 Years, 3 Hopper, Gravity Gate, Trough Hatches.

- 100, 6250 Covered Hoppers located off of UP in US. Last used in DDG. Offer: Negotiable. 1 Year term. Dirty to Dirty. Free move on UP..

- 25, 19.6K DOT111 Tanks located off of UP in US. Last used in Molases. Offer: Negotiable.

- 50, 20K DOT111 Tanks located off of UP or BN in Wichita Falls, TX. Last used in HCL. Offer: Negotiable.

- 50, 30K 117R Tanks located off of CSX, NS, or CN in Detroit. Last used in Diesel. Offer: Negotiable. Multiyear.

- 50, 20K 117J Tanks located off of All Class 1s in Multiple Locations. Last used in Styrene. Offer: Negotiable. Cars are currently moving.

- 22, 25.5K DOT111 Tanks located off of UP in Texas. Last used in Asphalt. Offer: Negotiable.

- 29, 25.5K 117J Tanks located off of BN or UP in Texas. Cars are Clean. Offer: Negotiable.

- 40, 30K Tanks 117J located off of BNSF or UP in Houston. Cars are Clean. Offer: Negotiable.

Sales Offers

- 21, 50′ Boxcar Plate Cs located off of various class 1s in NM. Offer: Negotiable. End of Life.

- 3, 50′ Boxcar Plate Cs located off of various class 1s in multiple locations. Offer: Negotiable. End of Life.

- 27, 50′ Boxcar Plate Cs located off of various class 1s in PQ. Offer: Negotiable. End of Life.

- 100, 3250 Covered Hoppers located off of various class 1s in multiple locations. Offer: Negotiable. Sand Cars.

- 5, 2740 Mill Gondolas located off of various class 1s in NC. Offer: Negotiable. End of Life.

- 1, 2260 Mill Gondolas located off of various class 1s in AL. Offer: Negotiable. End of Life.

- 30, 2740 Mill Gondolas located off of various class 1s in multiple locations. Offer: Negotiable. End of Life.

- 21, 2740 Mill Gondolas located off of various class 1s in WA. Offer: Negotiable. End of Life.

- 9, 4750 Covered Hoppers located off of various class 1s in multiple locations. Offer: Negotiable. End of Life.

- 5, 4750 Covered Hoppers located off of various class 1s in multiple locations. Offer: Negotiable. End of Life.

- 50, 31.8K Tank CPC 1232s located off of UP or BN in TX. Offer: Negotiable. Requal Due in 2025.

- 100, 4600CF Open Top Hoppers located off of BN or CSX in Southeast. Offer: Negotiable. N/A.

Call PFL today to discuss your needs and our availability and market reach. Whether you are looking to lease cars, lease out cars, buy cars, or sell cars call PFL today at 239-390-2885

Live Railcar Markets

| CAT | Type | Capacity | GRL | QTY | LOC | Class | Prev. Use | Offer | Note |

|---|

PFL will be at the Following Conferences

- Where: La Quinta, CA

- Attending: David Cohen (954-729-4774)

- Conference Website

- Where: Hyatt Regency Dallas in Dallas, TX

- Attending:Curtis Chandler (239.405.3365), David Cohen (954-729-4774), Brian Baker (239.297.4519), Cyndi Popov(403) 402-5043

- Conference Website