“Only by not forgetting the past can we be master of the future”

– Ba Jin

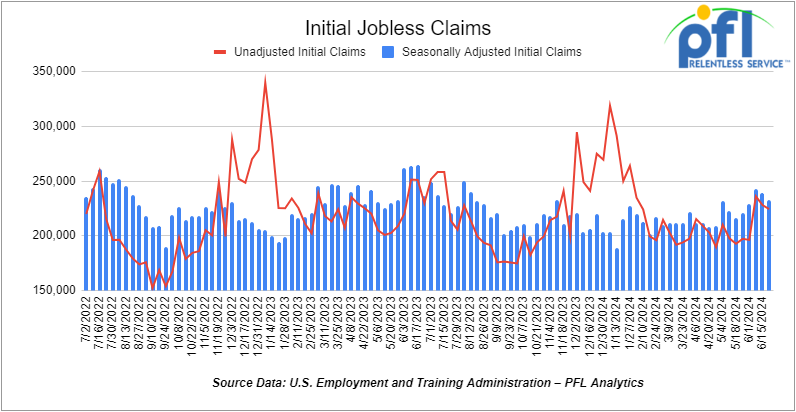

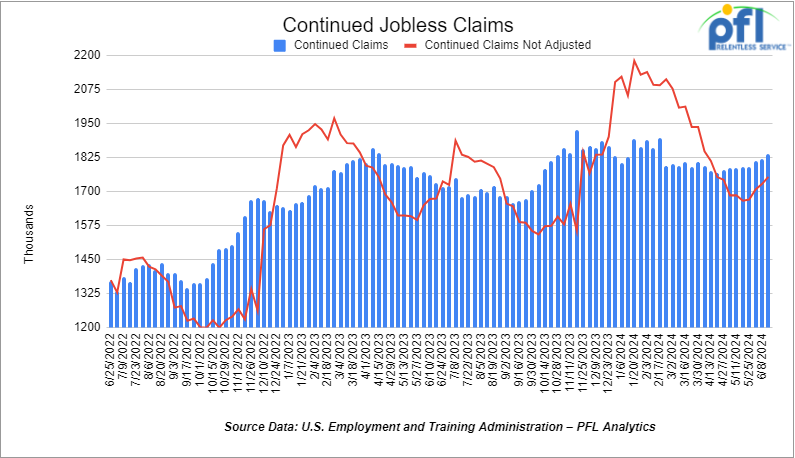

Jobs Update

- Initial jobless claims seasonally adjusted for the week ending June 22nd, 2024 came in at 233,000, down -6,000 people week-over-week.

- Continuing jobless claims came in at 1.839 million people, versus the adjusted number of 1.821 million people from the week prior, up 15,000 people week-over-week.

Stocks closed lower on Friday of last week, but mixed week over week

The DOW closed lower on Friday of last week, down -45.20 points (-0.12%), closing out the week at 39,118.86, down -31.47 points week-over-week. The S&P 500 closed lower on Friday of last week, down -22.39 points (-0.41%), and closed out the week at 5,460.48, down -4.14 points week-over-week. The NASDAQ closed lower on Friday of last week, down -126.08 points (-0.71%), and closed out the week at 17,732.6 up 43.24 points week-over-week.

In overnight trading, DOW futures traded higher and are expected to open at 39,541 this morning up 72 points.

Crude oil closed mixed on Friday of last week, but higher week over week.

WTI traded lower -$0.20 per barrel (-0.24%) on Friday of last week, to close at $81.54 per barrel, up $0.81 per barrel week-over-week. Brent traded up US$0.02 per barrel to close at US$86.41 per barrel on Friday of last week, up US$1.17 per barrel week-over-week.

One Exchange WCS (Western Canadian Select) for August delivery settled Friday at US$13.55 below the WTI-CMA (West Texas Intermediate – Calendar Month Average). The implied value was US$67.00 per barrel.

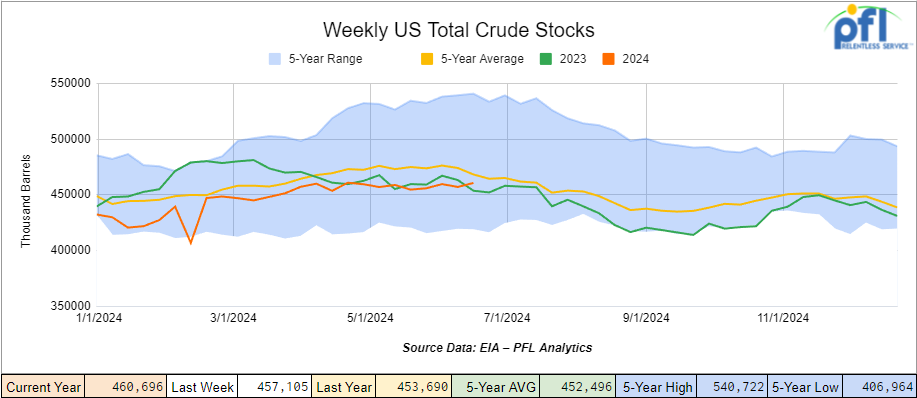

U.S. commercial crude oil inventories (excluding those in the Strategic Petroleum Reserve) increased by 3.6 million barrels week-over-week. At 460.7 million barrels, U.S. crude oil inventories are 2% below the five-year average for this time of year.

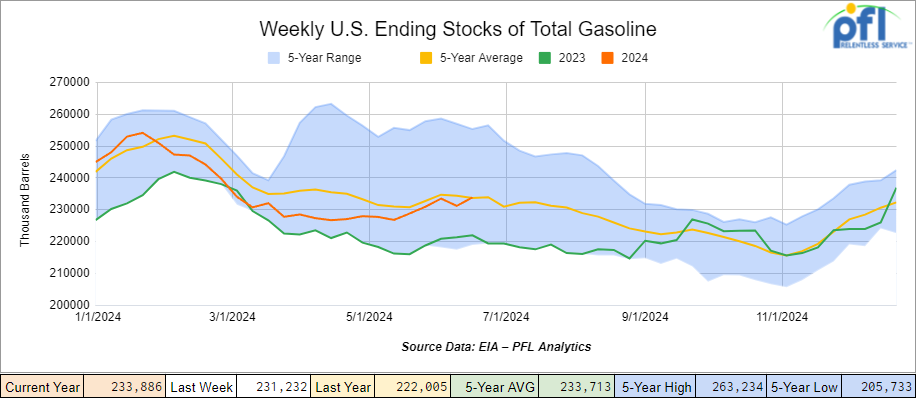

Total motor gasoline inventories increased by 2.7 million barrels week-over-week and the same as the five-year average for this time of year.

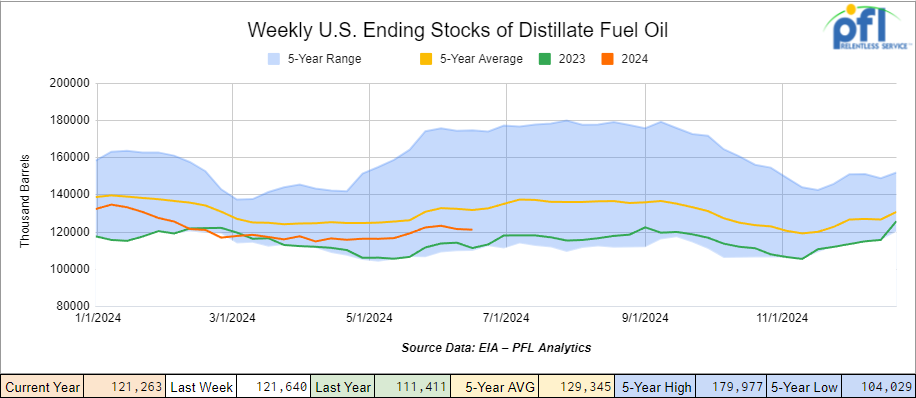

Distillate fuel inventories decreased by 400,000 barrels week-over-week and are 9% below the five-year average for this time of year.

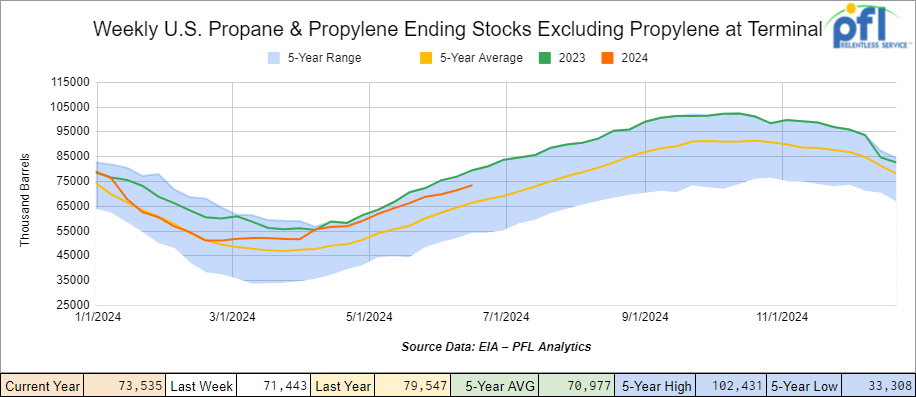

Propane/propylene inventories increased by 2.1 million barrels week–over-week and are 11% above the five-year average for this time of year.

Propane prices closed at 79 cents per gallon, up 2 cents week-over-week, and up 22 cents year-over-year.

Overall, total commercial petroleum inventories increased by 8.2 million barrels during the week ending June 21st, 2024.

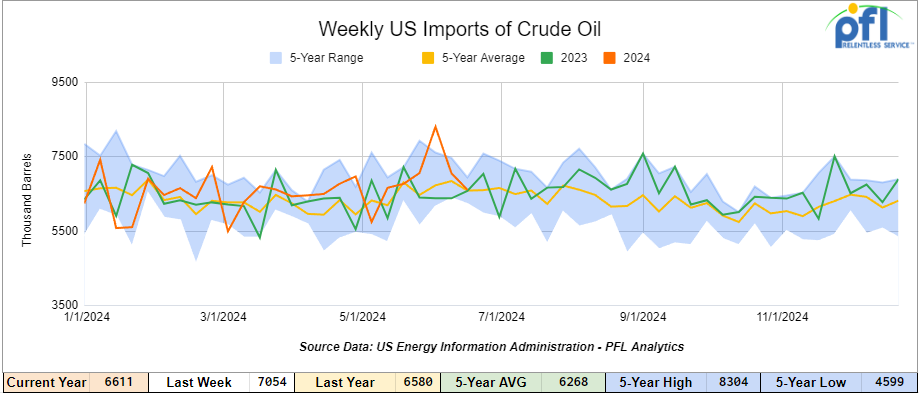

U.S. crude oil imports averaged 6.6 million barrels per day during the week ending June 21, 2024, a decrease of 443,000 barrels per day week-over-week. Over the past four weeks, crude oil imports averaged 7.3 million barrels per day, 13.7% more than the same four-week period last year. Total motor gasoline imports (including both finished gasoline and gasoline blending components) averaged 762,000 barrels per day, and distillate fuel imports averaged 133,000 barrels per day during the week ending June 21, 2024.

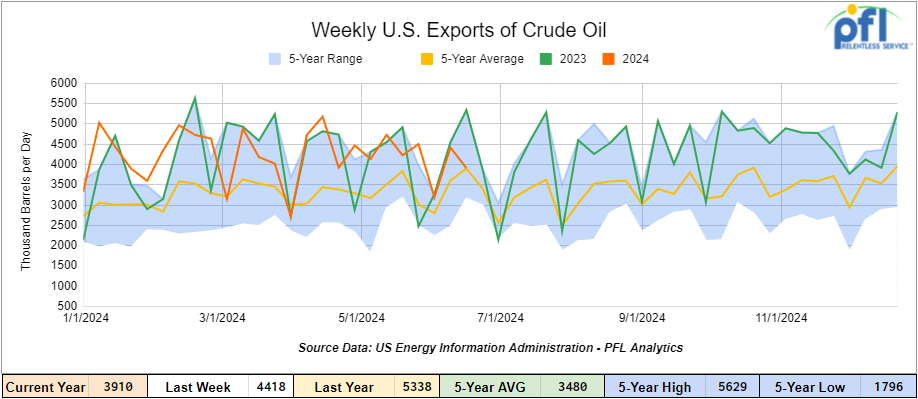

U.S. crude oil exports averaged 3.91 million barrels per day for the week ending June 21st, 2024, a decrease of 508,000 per day week-over-week. Over the past four weeks, crude oil exports averaged 4.004 million barrels per day.

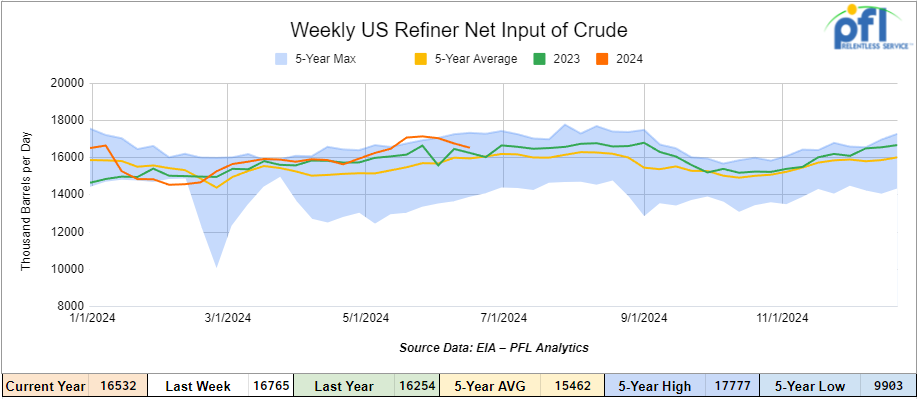

U.S. crude oil refinery inputs averaged 16.5 million barrels per day during the week ending June 21, 2024, which was 234,000 barrels per day less week-over-week.

WTI is poised to open at $81.87, up 33 cents per barrel from Friday’s close.

North American Rail Traffic

Week Ending June 26th, 2024.

Total North American weekly rail volumes were up (2.02%) in week 26, compared with the same week last year. Total carloads for the week ending on June 26th were 336,754, down (-1.11%) compared with the same week in 2023, while weekly intermodal volume was 328,896, up (+5.44%) compared to the same week in 2023. 7 of the AAR’s 11 major traffic categories posted year-over-year increases. The most significant decrease came from Metallic Ores and Metals, which was down (-11.3%). The most significant increase came from Grain which was up (+20.15%).

In the East, CSX’s total volumes were down (-0.92%), with the largest decrease coming from Grain (-23.07%) while the largest increase came from Other (10.5%). NS’s volumes were up (3.98%), with the largest increase coming from Forest Products (+16.37%) while the largest decrease came from Metallic Ores and Metals (-6.77%).

In the West, BN’s total volumes were up (7.77%), with the largest increase coming from Grains (54.79%) while the largest decrease came from Forest Products down (-14.5%). UP’s total rail volumes were up (4.94%) with the largest decrease coming from Nonmetallic Minerals, down (-15.22%) while the largest increase came from Grain which was up (+15.68%).

In Canada, CN’s total rail volumes were down (-15.33%) with the largest decrease coming from Coal, down (-31.46%) while the largest increase came from Farm Products, up (+5.71%). CP’s total rail volumes were down (-16.75%) with the largest increase coming from Other (+83.54%) while the largest decrease came from Nonmetallic Minerals, down (-43.56%).

KCS’s total rail volumes were down (-5.04%) with the largest decrease coming from Other (-38.81%) and the largest increase coming from Nonmetallic Minerals (+40.16%).

Source Data: AAR – PFL Analytics

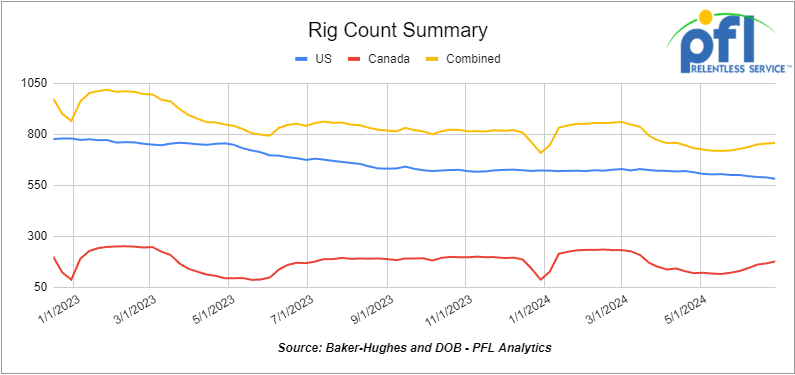

Rig Count

North American rig count was up by 3 rigs week-over-week. U.S. rig count was down by -7 rigs week-over-week, and down by -93 rigs year-over-year. The U.S. currently has 581 active rigs. Canada’s rig count was up by 10 rigs week-over-week, and up by 9 rigs year-over-year. Canada’s overall rig count is 176 active rigs. Overall, year-over-year, we are down -84 rigs collectively.

North American Rig Count Summary

A few things we are watching:

We Continue to watch Potential Rail Strikes in Canada

Union members at CN and CPKC railways have voted to reauthorize strikes at both companies if negotiated settlements can’t be reached. The teamsters Rail Conference (TCRC) has been meeting with the two railroads to replace 3 contracts that expired at the end of last year.

Teamsters Canada said in a statement on Saturday that union members at both railways voted almost 99%in favor of reauthorized strike action.

The union said members previously voted in favor of strike action on May 1, but the 60-day time limit on the vote expired.

It said that meant it had to take the “unusual step” of holding a second strike vote.

After voting for a strike the first time, the Canadian Industrial Relations Board (CIRB) intervened to determine if rail deliveries of critical commodities such as propane need to continue if a strike were to occur. In the meantime, TCRC members voted again between June 14th and June 29th whether or not to strike.

Paul Boucher, the Teamsters Canada Rail Conference President, said the Union wants to go back to the bargaining table with its renewed strike mandate and work with federal government mediators.

A CPKC spokesman said on Friday of last week that it is “unlikely the company or union would be in a legal position to initiate a strike or lockout before mid-July or later, and 72-hours strike or lockout notice must be provided.”

We are watching Petroleum Carloads

The four-week rolling average of petroleum carloads carried on the six largest North American railroads fell to 27,774 from 27,890, which was a loss of -116 rail cars week-over-week. Canadian volumes were mixed. CPKC’s shipments rose by +9.9% week over week, CN’s volumes were lower by -6.7% week-over-week. U.S. shipments were mostly lower. The BN had the largest percentage decrease and was down by -8.7%. The NS was the sole gainer and was up by +.03%

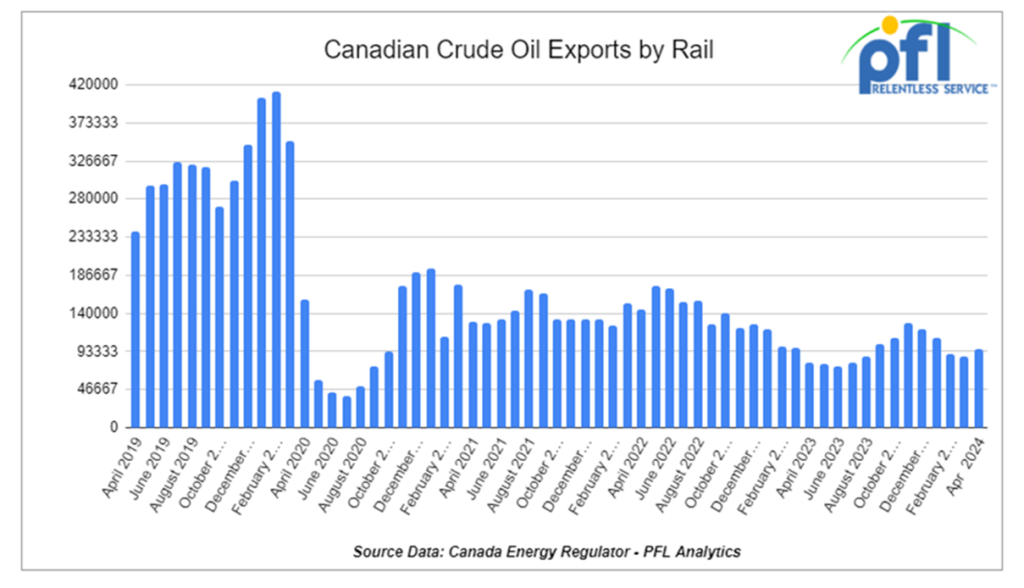

We are Watching Crude by Rail out of Canada

Despite the Trans Mountain expansion, which tripled pipeline capacity from Alberta to Canada’s Pacific Coast to 890,000 barrels, crude by rail out of Canada rose month over month. The Canadian Energy regulator reported on June 24, 2024 that 96,323 barrels were exported during the month of April 2024 from 86,766 barrels in March of 2024, an increase of 9,557 barrels per day,which is its highest reading since January of 2024.

Crude by rail will always be necessary out of Canada for stranded oil not connected by pipelines and raw bitumen shipped as a non-haz product which is not able to flow in pipelines and is competitive with pipeline tolls is a growing market to keep an eye on. Other factors would be existing long term contractual commitments and basis -we really need to see basis WTI-CMA (West Texas Intermediate – Calendar Month Average) blow out to -17 per barrel for sustained periods of time to make economic sense.

Lease Bids

- 20, 4750’s Through Hatch Covered Hoppers needed off of UP BN in USA West for 3 years. Cars are needed for use in Fertilizer service.

- 25-50, 5000CF-5100CF Covered Hoppers needed off of BNSF, CSX, KCS, UP in Gulf LA for 3-10 years. Cars are needed for use in Dry sugar service. 3 bay gravity dump, Hempel 37700

- 4, 6260 Covered Hoppers needed off of CSX in Bostick, NC for 2-4 Years. Cars are needed for use in Polypropene Pellets service.

- 10, 5200cf PD Hoppers needed off of UP in Colorado for 1-3 years. Cars are needed for use in Silica service. Call for details

- 10, 2500CF Open Top Hoppers needed off of UP or BN in Texas for 5 years. Cars are needed for use in aggregate service. Need Rapid Discharge Doors

- 25, 3230 PD Hoppers needed off of NS or CSX in Ohio for 5 years. Cars are needed for use in Flyash service.

- 250, 4000 Rapid Hoppers needed off of BNSF in TX IL for 5 years. Cars are needed for use in Coal service. in rotary/rapid cars with the electric dumping shoe

- 150, 23.5K DOT111 Tanks needed off of any class 1 in LA for 2-3 years. Cars are needed for use in Fluid service. Needed July

- 30, 17K-20K DOT117J Tanks needed off of UP or BN in Midwest/West Coast for 3-5 years. Cars are needed for use in Caustic service.

- 15, 28.3K DOT117J Tanks needed off of any class 1 in any location for 3 years. Cars are needed for use in Glycerin & Palm Oil service.

- 25, 20.5K CPC1232 or DOT117J Tanks needed off of BNSF or UP in the west for 3-5 years. Cars are needed for use in Magnesium chloride service. SDS onhand

- 10, 30k any Tanks needed off of UP BN in Texas for 1 year plus. Cars are needed for use in Fuel Oil service.

- 14, 23.5K DOT111 Tanks needed off of UP in Morrilton, AR for 1 year. Cars are needed for use in Turpentine service.

- 8, 28-30K Any Tanks needed off of UP BN in Texas and Gulf for 5 years. Cars are needed for use in Chlorobenzene service. Need Magrods

- 10, 28.3K 117J Tanks needed off of UP or BN in Texas for 3 Year.

- 25-30, 23.5K or 25.5K Dot 111 or CPC 1232 Tanks needed off of UP or BN in TX, OK, or AR for 3-5 Years. Cars are needed for use in Asphalt service. Needed ASAP., Lined or Unlined. Splash Load

- 10, 25.5K-28.3K DOT 111 Tanks needed off of UP or BN in Houston for 2 Year. Cars are needed for use in Resin service.

- 30, 29K 117J Tanks needed off of BN or CN in Houston or Edmonton for 1-2 Year. Cars are needed for use in Biodiesel service.

- 100, 25.5K DOT 111 Tanks needed off of Any Class 1 in Texas for 3 Years +. Cars are needed for use in Asphalt service.

- 20, 25.5k CPC 1232 Tanks needed off of UP or BN in OK, TX for 3 Year. Cars are needed for use in Asphalt service.

- 10, 30K 117R or 117J Tanks needed off of Any Class 1 in USA for 1 year. Cars are needed for use in Glycerin service.

- 50, 30K 117 Tanks needed off of BNSF or UP in TX for 3-6 Months. Cars are needed for use in Crude service. will look at smaller cars. Prefer short term would look at longer term. Domestic use only

- 100, 15.5K DOT 111 Tanks needed off of Any Class 1 in USA for 1-3 Years. Cars are needed for use in Molten Sulfur service.

- 200, 30K Any Tanks needed off of UP or BN in Texas for RD. Cars are needed for use in Dirty service.

- 50, 23.5-25.5 DOT111 Tank s needed off of Any Class 1 in USA for 5 years. Cars are needed for use in Asphalt service.

- 15-20, 29K 117R Tanks needed off of NS or CSX in Ohio for 6-12 Months. Cars are needed for use in Ply Oil service.

- 80, 25.5K-29K Any Tanks needed off of NS or CSX in Northeast for 1-5 Years. Cars are needed for use in Crude service.

Sales Bids

- 100-150, 3400CF Covered Hoppers needed off of UP BN in Texas. Cars are needed for use in Sand service.

- 10, 2770 Mill Gondolas needed off of any class 1 in St. Louis. Cars are needed for use in Cement service.

- 20, 2770-3400 Mill Gondolas needed off of any class 1 in South Texas. Cars are needed for use in scrap metal service.

- 20-30, 3000 – 3300 PD Hoppers needed off of BN or UP preferred in West. Cars are needed for use in Cement service. C612

- 20-30, Open Top Hoppers needed off of NS or CSX in Northeast. Cars are needed for use in aggregate service. Gravity dump

- 20, 17K DOT111 Tanks needed off of various class 1s in various locations. Cars are needed for use in corn syrup service.

- 2-4, 28K DOT111 Tanks needed off of BNSF Preferred in Minnesota. Cars are needed for use in Biodiesel service. Coiled and insulated

- 100, 15.7K DOT111 Tanks needed off of CSX or NS in the east. Cars are needed for use in Molten Sulfur service.

- 30, 17K-20K DOT111 Tanks needed off of UP or BN in Texas. Cars are needed for use in UAN service.

- 5, 30K DOT 111 Tanks needed off of in US. Cars are needed for use in Fuels service.

- 5, 23,5K DOT 111 Tanks needed off of any class 1 in Texas. Negotiable

Lease Offers

- 200-500, 5200, Covered Hoppers located off of CN and NS in Moving on CN and NS. Cars were last used in Grain. Lease available until Fall.

- 50, ~5400, Covered Hoppers located off of NS, IORY in MI. Cars were last used in bean meal. 1 year+

- 53, 2 containers, Flats Double-stack rail transports located off of KCS in Texas. Cars are clean Lease or sell. (Intermodal Container)

- 15, 33K, 340W Pressure Tanks located off of All Class Ones in North America. Cars were last used in Propane/Butane. Up to 1 year.

- 100+, 29K, 117R Tanks located off of All Class Ones in St Louis. Cars were last used in Veg Oils. Up to 4 Years

- 100+, 29K, 117J Tanks located off of All Class Ones in St Louis. Cars were last used in Veg Oils. Returned by end of 2026

- 100, 30K, 117J Tanks located off of UP or BN in Texas. Cars were last used in Ethanol. Up to 1 year. Must go into ethanol service.

- 200, 25.5K, 117J Tanks located off of CPKC in Moving. Cars were last used in Crude. 6-12 Months

- 5, 25.5K, DOT 111 Tanks located off of UP in Kansas. Cars were last used in Veg Oils. 2 Year Term

Sales Offers

- 24, 5300CF, Plate C Boxcars located off of NS or CSX in Southeast.

- 100-300, 3400, Covered Hoppers located off of various class 1s in multiple locations. Sand Cars

- 19, 4400, Rotary Gondolas located off of UP and BN in California and Wyoming.

- 100, 28.3K, DOT117J Tanks located off of various class 1s in multiple locations.

- 7, 30K, DOT 111 Tanks located off of UP in TX, CA, NM.

Call PFL today to discuss your needs and our availability and market reach. Whether you are looking to lease cars, lease out cars, buy cars, or sell cars call PFL today at 239-390-2885

Live Railcar Markets

| CAT | Type | Capacity | GRL | QTY | LOC | Class | Prev. Use | Offer | Note |

|---|

PFL will be at the Following Conferences

- Where: La Quinta, CA

- Attending: David Cohen (954-729-4774)

- Conference Website

- Where: Hyatt Regency Dallas in Dallas, TX

- Attending:Curtis Chandler (239.405.3365), David Cohen (954-729-4774), Brian Baker (239.297.4519), Cyndi Popov(403) 402-5043

- Conference Website