“People might not get all they work for in this world, but they must certainly work for all they get.”

– Frederick Douglass

Jobs Update

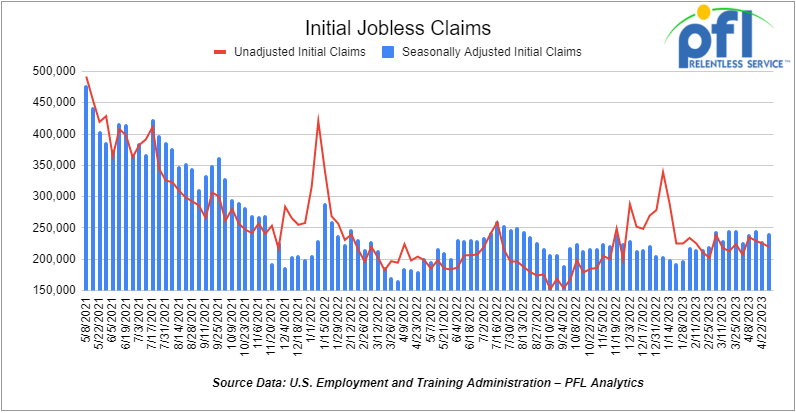

- Initial jobless claims for the week ending April 29th, 2023 came in at 242,000, up 13,000 people week-over-week.

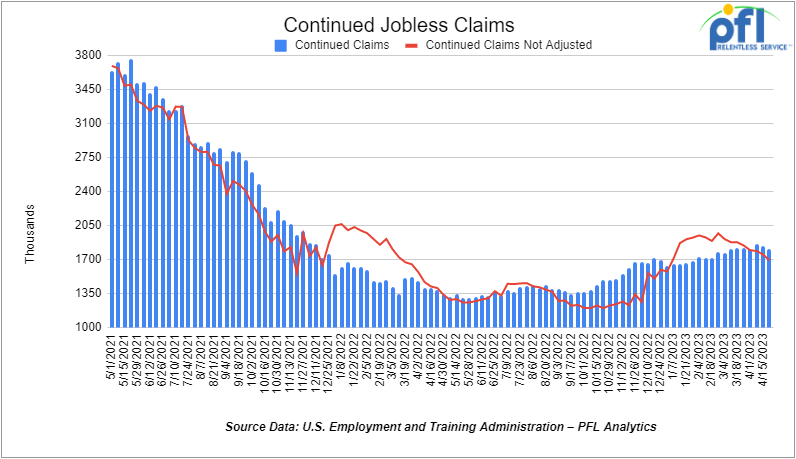

- Continuing jobless claims came in at 1.805 million people, versus the adjusted number of 1.843 million people from the week prior, down -38,000 people week over week.

Stocks closed higher on Friday of last week, but mixed week over week

The DOW closed higher on Friday of last week, up 546.64 points (+1.65%), closing out the week at 33,674.38, down -151.78 points week over week. The S&P 500 closed higher on Friday of last week, up 75.03 points (+1.85%) and closed out the week at 4,136.25, down -33.23 points week over week. The NASDAQ closed higher on Friday of last week, up +269.01 points (+2.2%), and closed the week at 12,235.41, up 8.83 points week over week.

In overnight trading, DOW futures traded lower and are expected to open at 33,780 this morning up 41 points.

WTI closed higher on Friday of last week, but down week over week

WTI traded up $2.78 per barrel (4.1%) to close at $71.34 per barrel on Friday of last week, but down -$5.44 per barrel week over week. Brent traded up US$2.80 per barrel (3.9%) on Friday of last week, to close at US$75.30 per barrel, down -US$4.24 per barrel week over week. In Canadian crude markets, WCS for June delivery settled Friday at US$14.05 below the WTI-CMA. The implied value was US$57.13 per barrel. On Thursday, it settled at US$14.30 below the WTI-CMA for June delivery. The implied value was US$54.14 per barrel. Natgas futures gained 2% on Friday of last week on forecasts for more demand this week and next than previously expected.

Reacting to the precipitous fall in oil prices last week, OPEC+ has confirmed that it would hold its upcoming June 4th policy meeting in person in Vienna, hinting at a further tightening of production targets.

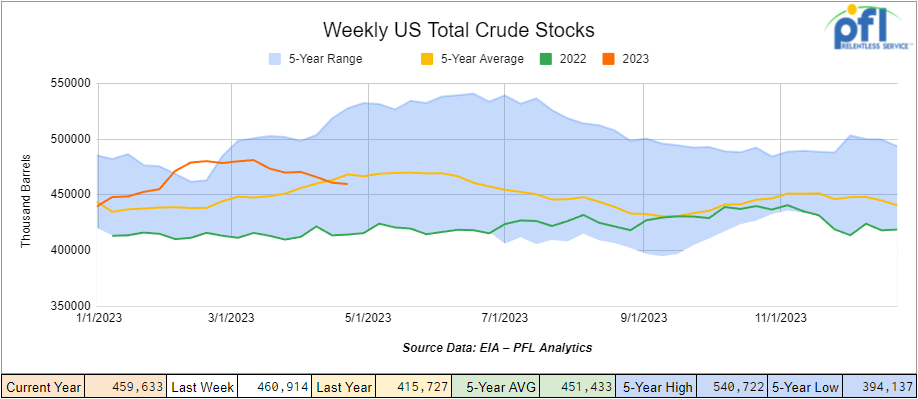

U.S. commercial crude oil inventories (excluding those in the Strategic Petroleum Reserve) decreased by 1.3 million barrels week over week. At 459.6 million barrels, U.S. crude oil inventories are 2% below the five-year average for this time of year.

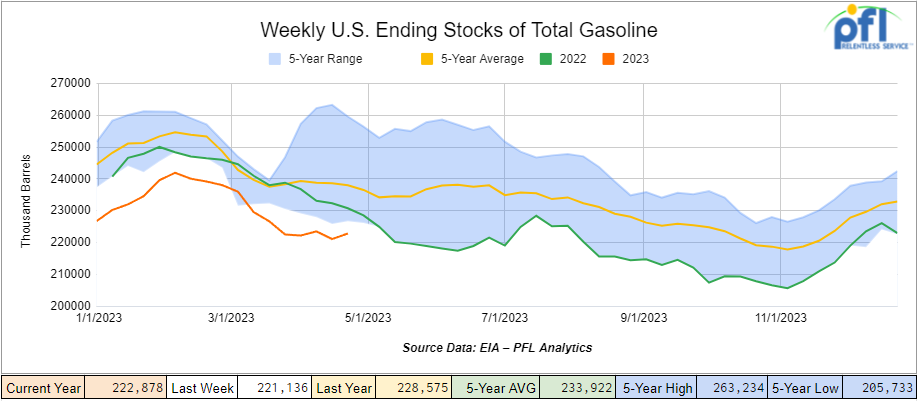

Total motor gasoline inventories increased by 1.7 million barrels week over week and are 6% below the five-year average for this time of year.

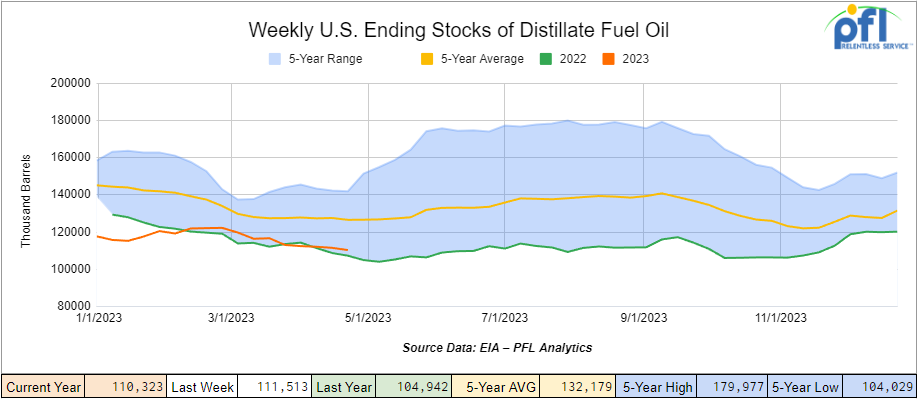

Distillate fuel inventories decreased by 1.2 million barrels week over week and are 12% below the five-year average for this time of year.

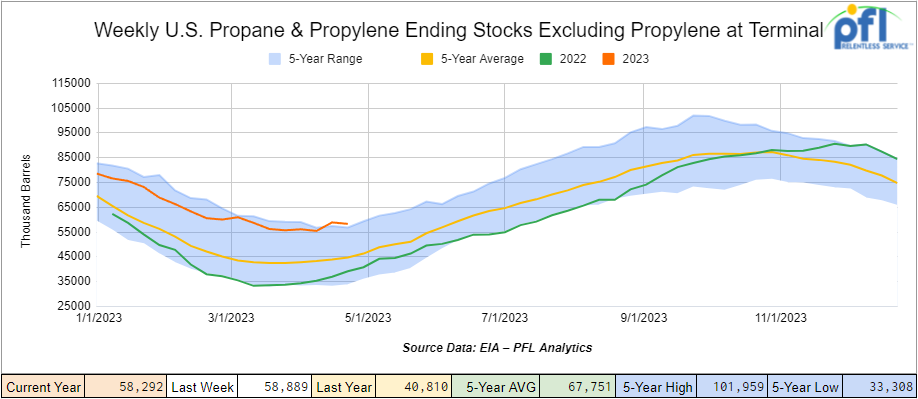

Propane/propylene inventories decreased by 600,000 barrels week over week and are 29% above the five-year average for this time of year.

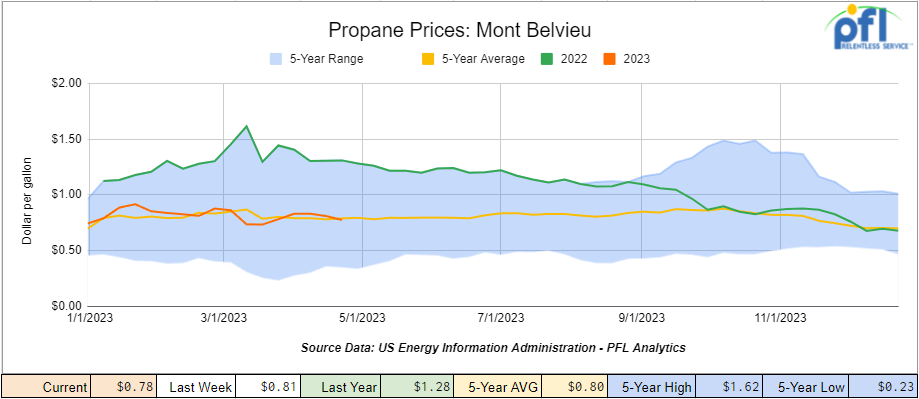

Propane prices closed at 78 cents per gallon, down 3 cents per gallon week over week and down 50 cents per gallon year over year, as inventories increase

Overall, total commercial petroleum inventories increased by 400,000 barrels week over week.

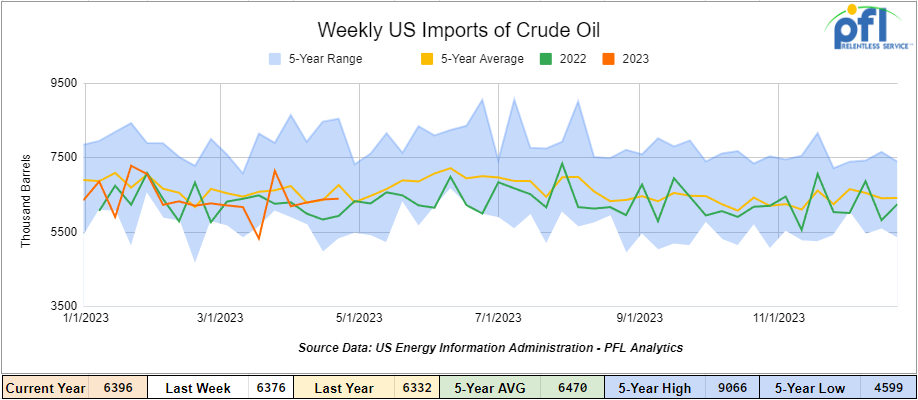

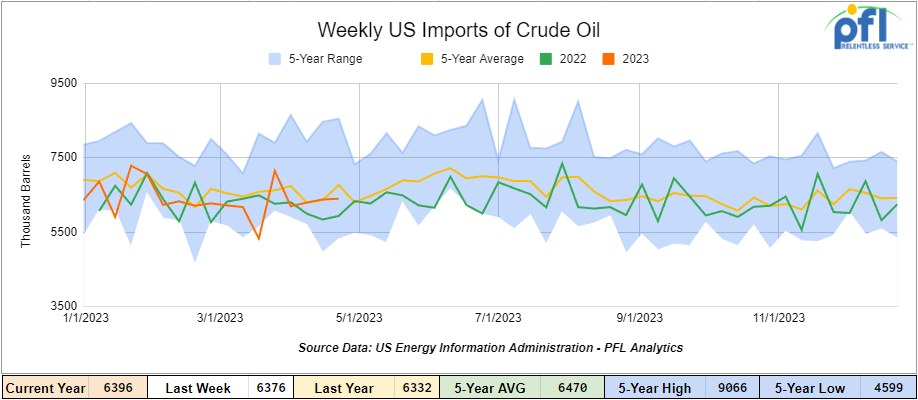

U.S. crude oil imports averaged 6.4 million barrels per day during the week ending April 28th, 2023, an increase of 21,000 barrels per day week over week. Over the past four weeks, crude oil imports averaged 6.3 million barrels per day, 4.8% more than the same four-week period last year. Total motor gasoline imports (including both finished gasoline and gasoline blending components) averaged 798,000 barrels per day, and distillate fuel imports averaged 144,000 barrels per day during the week ending April 28th, 2023.

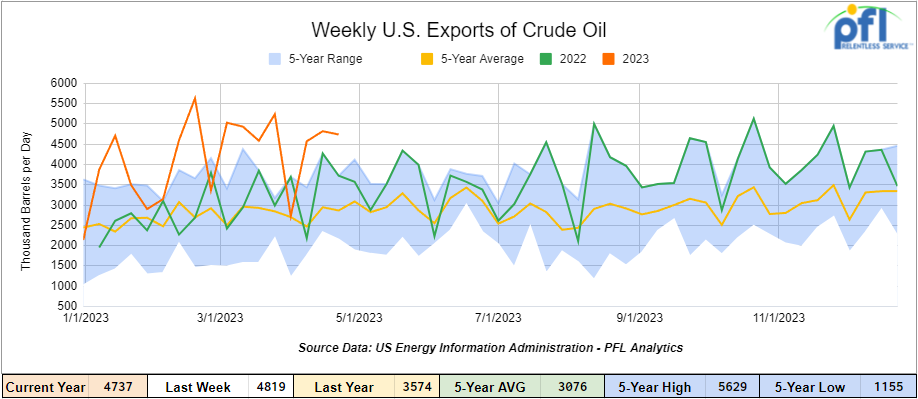

U.S. crude oil exports averaged 4,737 million barrels per day for the week ending April 28th, 2023, a decrease of -82,000 barrels per day week over week. Over the past four weeks, crude oil exports averaged 4.214 million barrels per day.

U.S. crude oil refinery inputs averaged 15.7 million barrels per day during the week ending April 28, 2023 which was 98,000 barrels per day less week over week.

As of the writing of this report, WTI is poised to open at $72.89 up $1.50 per barrel from Monday’s close.

North American Rail Traffic

Week Ending May 3rd, 2023.

Total North American weekly rail volumes were down (-5.47%) in week 17 compared with the same week last year. Total carloads for the week ending on May 3rd were 357,841, up (+1.32%) compared with the same week in 2022, while weekly intermodal volume was 307,126, down (-12.32%) compared to the same week in 2022. 7 of the AAR’s 11 major traffic categories posted year-over-year decreases with the most significant decrease coming from Intermodal (-12.32%). The largest increase came from Motor Vehicles and Parts (+13.75%).

In the east, CSX’s total volumes were down (-3.22%), with the largest decrease coming from Forest Products (-12.97%) and the largest increase from Motor Vehicles and Parts (+18.68%). NS’s volumes were down (-6.08%), with the largest decrease coming from Petroleum and Petroleum Products (-11.48%) and the largest increase from Grain (+28.94%).

In the West, BN’s total volumes were down (-9.48%), with the largest decrease coming from Intermodal (-16.8%), and the largest increase coming from Motor Vehicles and Parts (+23.93%). UP’s total rail volumes were up (0.57%) with the largest decrease coming from Other (-35.46%) and the largest increase coming from Motor Vehicles and Parts (+16.62%).

In Canada, CN’s total rail volumes were down (-11.43%) with the largest increase coming from Metallic Ores and Minerals (+20.96%) and the largest decreases coming from Grain (-37.04%). CP’s total rail volumes were up (+11.21%) with the largest decrease coming from Intermodal (-17.43%) and the largest increase coming from Coal (+346.37%).

KCS’s total rail volumes were down (-13.2%) with the largest decrease coming from Farm Products (-36.67%) and the largest increase coming from Coal (+33.27%).

Source Data: AAR – PFL Analytics

With intermodal volumes down so low this year, the Truckload Market has been under severe pressure. Truckload spot rates have continued to fall, down 42.4% from the prior year this week, according to our FMIC data. Some small carriers are unable to pay their insurance premiums. Things are not expected to turn around until August of 2023. Dry van spot rate per mile ex fuel is currently sitting at $1.35 according to Bloomberg data, and the last two previous cycle lows point to a potential inflection approaching.

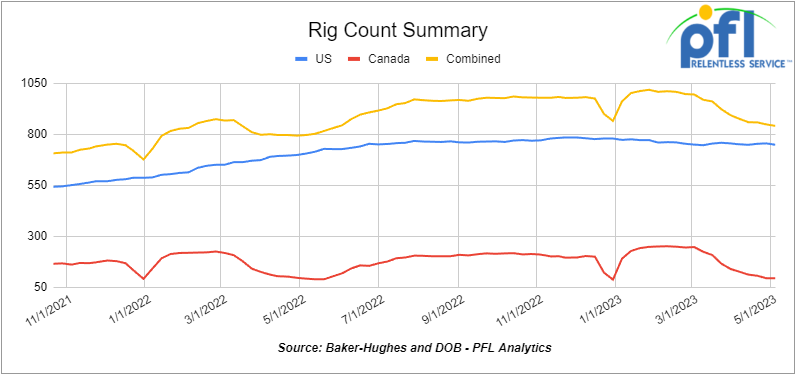

Rig Count

North American rig count was down by -7 rigs week over week. U.S. rig count was down by- 7 rigs week over week and up by +43 rigs year-over-year. The U.S. currently has 748 active rigs. Canada’s rig count was flat week-over-week and up by 2 rigs year over year. Canada’s overall rig count is 93 active rigs. Overall, year-over-year, we are up +45 rigs collectively.

International rig count which is reported monthly was up by 17 rigs month-over month and up 141 rigs year-over-year. Internationally, there are 947 active rigs.

North American Rig Count Summary

A few things we are keeping an eye on

We are watching Petroleum Carloads

The four-week rolling average of petroleum carloads carried on the six largest North American railroads fell to 22,412 from 22,729, which was a loss of -317 rail cars week-over-week. Canadian volumes rose week over week; CP’s shipments increased by +5.6% week over week, and CN’s volumes were higher by +0.2% week-over-week. U.S. shipments were mixed. The NS had the largest percentage increase and was up by 24.8% week-over-week. The CSX had the largest percentage decrease and was down by 6.2%

We are watching Hurricanes

In case you missed it, on April 13, 2023 the Colorado State University Tropical Meteorology Project team predicted a “slightly below-normal” Atlantic hurricane season. The team forecasts 13 named storms, including six hurricanes, two of which will be major hurricanes. On May 3rd, Xubin Zeng, a professor of hydrology and atmospheric sciences at the University of Arizona said “We are not expecting this to be as damaging as 2017.” That said, he emphasizes that “people should get prepared. “This will be a very active hurricane season. That’s our message,” says Zeng, adding that the East Coast and Gulf Coast are typically the regions where hurricanes have the greatest impacts.

We are watching Mountain Valley Pipeline

Equitrans Could Complete MVP in 2023. Equitrans may still complete Mountain Valley natural gas pipe by end-2023. U.S. energy company Equitrans Midstream Corp said on Tuesday of last week that it expects federal agencies to issue the required authorizations for its $6.6 billion Mountain Valley natural gas pipeline from West Virginia to Virginia by the early summer. That should allow the company to finish the long-delayed project by the end of 2023, however, Equitrans warned in its first quarter earnings that “there remains significant risk and uncertainty, including regarding current and likely litigation.” This has been Senator Joe Manchin’s pet project and he wants it built – looks like the Dems are going to throw him a bone!

We are watching Key Economic Indicators

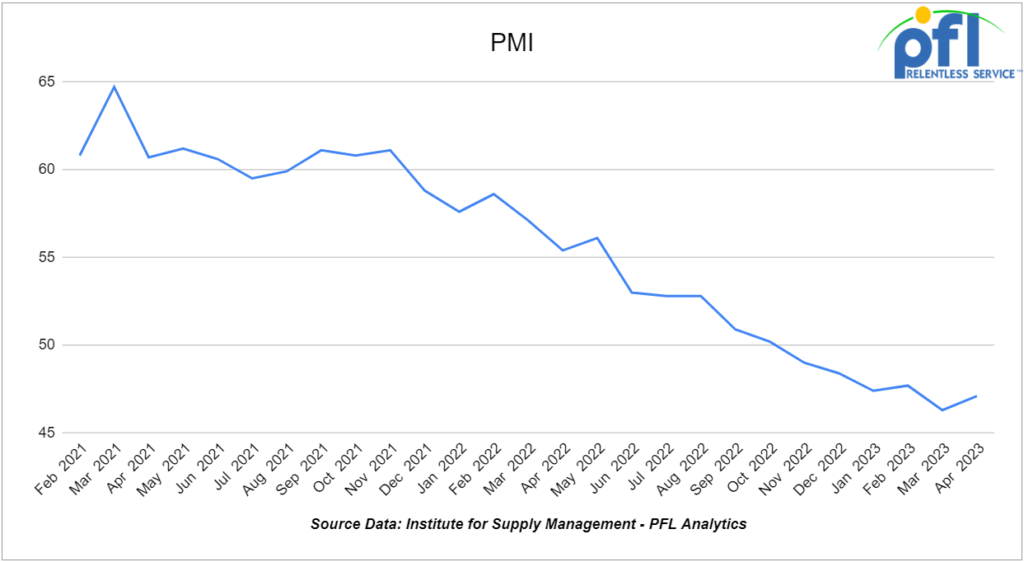

Purchasing Managers Index (PMI)

The Institute for Supply Management releases two PMI reports – one covering manufacturing and the other covering services. These reports are based on surveys of supply managers across the country and track changes in business activity. A reading above 50% on the index indicates expansion, while a reading below 50% signifies contraction, with a faster pace of change the farther the reading is from 50. In April, the PMI decreased to 46.3% from March’s 47.1%, marking the sixth consecutive month of readings below 50% and a 0.8% decrease month over month from March. Meanwhile, the new orders component continued to contract to 45.7% in April.

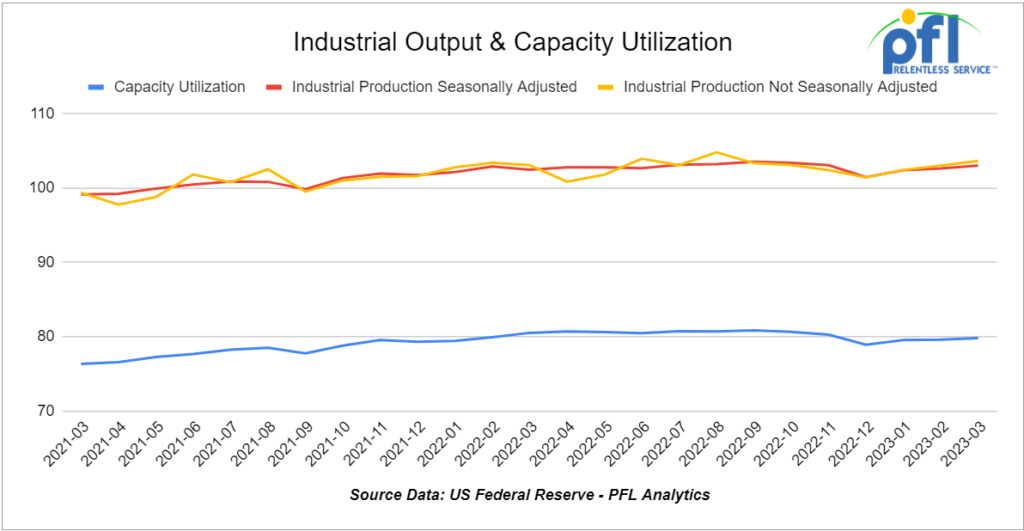

Industrial Output & Capacity Utilization

The Federal Reserve reported that total U.S. industrial output rose a preliminary 0.4% in March 2023 over February 2023, marking its third straight month over month increases. The increase was mainly driven by a jump in utility output in March due to increased demand for heat after an unusually mild February. Year-over-year industrial output in March 2023 was up 0.5% over March 2022, marking the 25th straight year-over-year increase, but the smallest such increase in two years.

Manufacturing output, which accounts for around 75% of total industrial output, fell a preliminary 0.5% in March from February, marking its first decline in three months. Output in March 2023 was down 1.1% from March 2022, its first year-over-year decline after two small year-over-year gains in February and January. Besides utilities, industries with output gains in March from February included grain mill products, petroleum refineries, and agricultural chemicals. Industries with output decreases in March from February included wood products and agricultural chemicals, among others. The capacity utilization rate for manufacturing was 78.1% in March, down from 78.6% in February.

U.S. Unemployment Rate

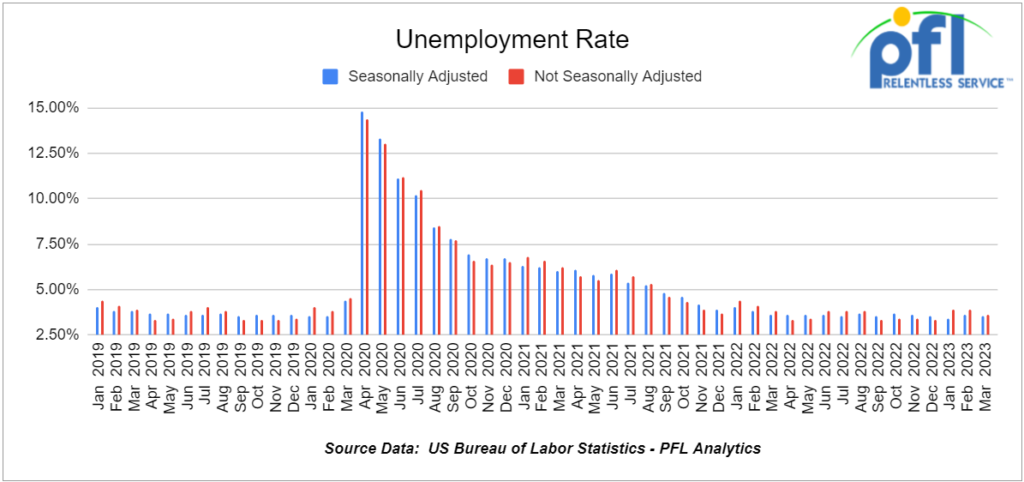

The Bureau of Labor Statistics’ April employment report, released on May 5th, indicated another month of solid job growth. The labor market in the US appears to be strong despite weakness in manufacturing output and the Manufacturing PMI. In April, 253,000 net new jobs were created, and the official unemployment rate fell to 3.4%, matching a 50-year low. The overall labor force participation rate in April was 62.6%, and the participation rate for prime-age workers was 83.3%, the highest it’s been since March 2008. Average hourly earnings for private sector workers rose 4.4% in April 2023 over April 2022, but year-over-year earnings adjusted for inflation have been negative for the past two years. Total job openings were 9.6 million at the end of March, down from 10.0 million in February. Weekly initial unemployment claims in April averaged 237,000, down slightly from March’s 242,000.

Consumer Confidence

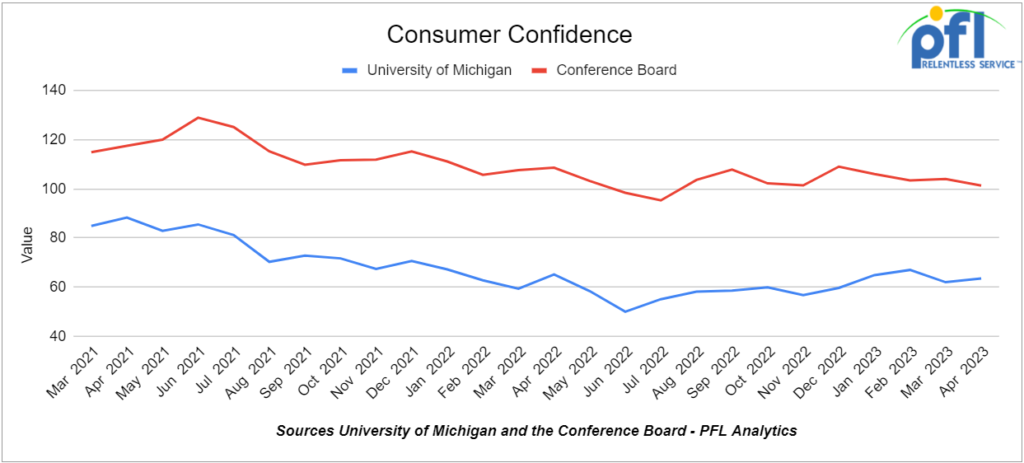

The Conference Board’s Index of Consumer Confidence decreased from 104.0 in March to 101.3 in April, its lowest level in nine months, indicating a downward trend over the past few months. Consumers’ expectations fell, and their outlook for business conditions and labor markets worsened, while purchasing plans for homes, autos, appliances, and vacations pulled back, suggesting consumers may be economizing amid growing pessimism. In contrast, the index of consumer sentiment from the University of Michigan rose slightly in April, with consumers short and long-run economic outlook improving modestly from the previous month.

Consumer Spending

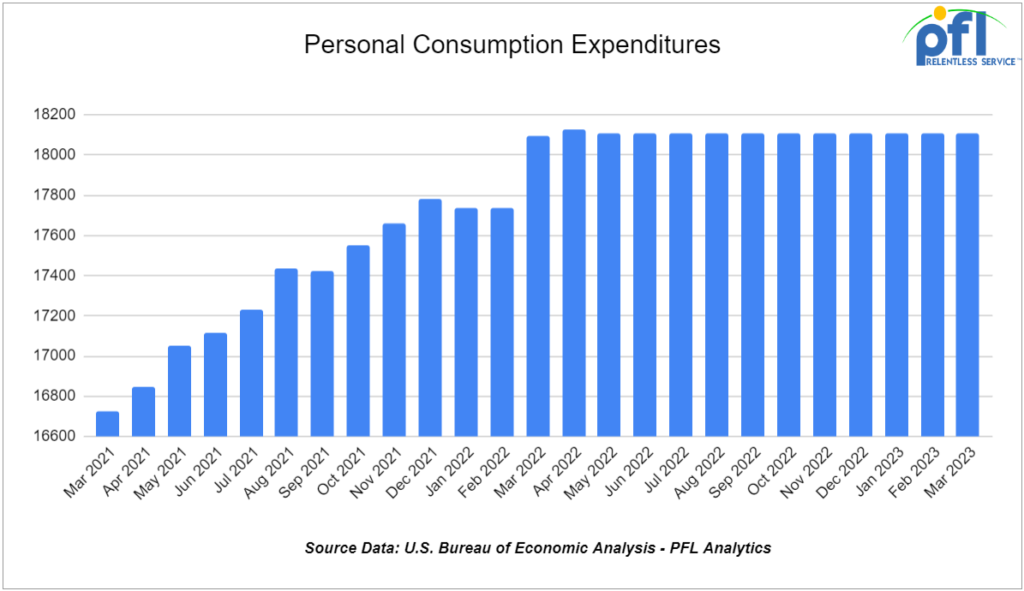

Consumer spending accounts for 70% of GDP and recent data shows a slowdown in spending. In March, total spending was flat compared to the month before and spending on goods has fallen in four of the last five months. Adjusted for inflation, total consumer spending was also flat in March and retail sales fell 0.6%.

We have been extremely busy at PFL with return-on-lease programs involving rail car storage instead of returning cars to a shop. A quick turnaround is what we all want and need. Railcar storage in general has been extremely active. Please call PFL now at 239-390-2885 if you are looking for rail car storage, want to troubleshoot a return on lease scenario, or have storage availability. Whether you are a car owner, lessor or lessee, or even a class 1 that wants to help out a customer we are here to “help you help your customer!”

Leasing and Subleasing has been brisk as economic activity picks up. Inquiries have continued to be brisk and strong Call PFL Today for all your rail car needs 239-390-2885

Lease Bids

- 100, 30K 117J Tanks needed off of CN in Detroit for 1 Year. Cars are needed for use in Diesel service.

- Up to 50, 31.8 117J, 117R, CPC1232 Tanks needed off of any class 1 in Texas or Ohio for 1-3 years. Cars are needed for use in Diesel/Gasoline service.

- 45, 3000 cf PDs Hoppers needed off of any class 1 in Texas for 3 years. Cars are needed for use in any service.

- 25, 30K 117 Tanks needed off of CN in Canada for 1 year. Cars are needed for use in Refined Products service.

- 30, 17K-20K 117J Tanks needed off of UP or BN in Midwest/West Coast for 3-5 Years. Cars are needed for use in Caustic service.

- 13-15, Any Flat Bottom Gondolas needed off of any class 1 in Texas for 1-3 Years. For lease or purchase

- 20, 28.3K DOT 111, 117, CPC 1232 Tanks needed off of any class 1 in Bakersfield, CA for Month to Month. Cars are needed for use in Biodiesel service.

- 10, 286K 15.7K Tanks needed off of KCS in Texas for 1 Year. Cars are needed for use in Sulfuric Acid service. Needed Next few months

- 150, 23.5K DOT 111 Tanks needed off of any class 1 in LA for 2-3 Year. Cars are needed for use in Fluid service. Needed July

- 25-50, 32K 340W Pressure Tanks needed off of NS or CSX in Marcellus for 1-2 Years. Cars are needed for use in Propane service.

- 25-50, 30K DOT 111, 117, CPC 1232 Tanks needed off of CN or CP in WI, Sarnia for 1-2 Years. Cars are needed for use in Diesel service.

- 25-50, 30K DOT 111, 117, CPC 1232 Tanks needed off of any class 1 in Chicago for 1-2 Months. Cars are needed for use in Diesel service.

- 100, 30K DOT 111, 117, CPC 1232 Tanks needed off of any class 1 in Texas for 1 Year. Cars are needed for use in West Texas Sour service.

- 25-50, 25.5K CPC1232 or 117J Tanks needed off of UP or BN in any location for 3-5 Years. Cars are needed for use in Heavy Fuel Oil service.

- 40, 30K 117R or 117J Tanks needed off of CP in MN for 2 Years. Cars are needed for use in Ethanol service.

- 10, 5200cf PD Hoppers needed off of UP in Colorado for 1-3 years. Cars are needed for use in Silica service. Call for details

- 30-40, 286K DOT 113 Tanks needed off of CN or CP/ UP in Canada/MM for 5 Years. Cars are needed for use in CO2 service.

- 70, 32K 340W Pressure Tanks needed off of CP or CN in Edmonton for 3 Years. Cars are needed for use in Propane service.

- 200-300, 28.3K 117R or 117J Tanks needed off of CP or CN in Sarnia for 3 Years. Cars are needed for use in Fuel Oil service.

- 30, 30K DOT 111 Tanks needed off of UP in Texas for 1-3 Years. Cars are needed for use in Diesel service.

- 5-7, 28.3K 117R Tanks needed off of NS or CSX in NC for 1 Year. Cars are needed for use in UCO service.

- 25-50, 5000CF-5100CF Lined Hoppers needed off of BNSF, CSX, KCS, UP in Gulf LA for 3-10 years. Cars are needed for use in dry sugar service. 3 bay gravity dump

- 25-50, 25.5K 117J Tanks needed off of NS CSX in NorthEast for 5 Years. Cars are needed for use in Asphalt/Heavy Fuel Oil service.

- 10-20, 20K-25K CPC 1232 or 117J Tanks needed off of UP CN in Illinois for 3-5 years. Cars are needed for use in Liquid feed service.

- 100-150, 4000CF Covered Hoppers needed off of UP BN in Texas for Purchase or 5 years. Cars are needed for use in Aggregate service.

- 10, any capacity Stainless Steel Tanks needed off of any class 1 in Canada for 5-10 years. Cars are needed for use in Alcohol service.

- 50-100, 25.5K CPC1232 or 117J Tanks needed off of any class 1 in any location for 5 Years. Cars are needed for use in Veg Oil service. Unlined

- 30-50, 30K 117 Tanks needed off of any class 1 in Northeast or Midwest for 1 Year. Cars are needed for use in C5 service. Must have Magrods

- 10-12, 340W Pressure Tanks needed off of UP in Utah to Cali for 1 year. Cars are needed for use in propane service. Needs them in April 2023

- 10-20, 340W Pressure Tanks needed off of CN or CP in Canada for 6 months to 1 year. Cars are needed for use in Propylene service. Immediate

- 100, 33K 340W Pressure Tanks needed off of CN in Canada for 3-5 Years. Cars are needed for use in Propane service.

- 25, 20.5K CPC1232 or 117J Tanks needed off of BNSF or UP in the west for 1-3 years. Cars are needed for use in magnesium chloride service. SDS onhand

- 10-100, 20K CPC1232 or 117J Tanks needed off of BNSF, CN or UP in the south or midwest for 5 years. Cars are needed for use in Urea Ammonium Nitrate service. CN Miss, BN Oklahoma, UP LA and Iowa- Must be lined

- 10, 50-60 footers Plate F Boxcars needed off of CN and UP or BNSF in Texas in Tennessee & Houston for 1 year. Cars are needed for use in Barium Sulfate service. Requires double door boxcars.

- Up to 60, 5150cf Covered Hoppers needed off of CN, CSX, NS in the east or midwest for 3 years. Cars are needed for use in Fertilizer service. 3-4 hatch gravity dumps

- 40, 2400cf Gondolas needed off of various class 1s in Indiana for 6 Months. Cars are needed for use in Rock service. Call for details

- 20-30, 14k Any Tanks needed off of BNSF, UP in Texas for 1-3 Years. Cars are needed for use in HCl service. Call for details

Sales Bids

- 20-25, 25.5K 117, DOT-111, CPC 1232 Tanks needed off of UP or BN in Texas. Cars are needed for use in Veg Oil service. Coiled and insulated

- 15, 30K 117, DOT-111, CPC 1232 Tanks needed off of UP or BN in Texas. Cars are needed for use in Veg Oil service.

- 2-4, 28K DOT 111 Tanks needed off of BNSF Preferred in Minnesota. Cars are needed for use in Biodiesel service. Coiled and insulated

- 100, Plate F Boxcars needed off of BN or UP in Texas.

- 20, 2770 Mill Gondolas needed off of CSX in the northeast. Cars are needed for use in non-haz soil service. 52-60 ft

- 8, 5200 Covered Hoppers needed off of various class 1s in various locations. Cars are needed for use in Plastic Pellet service.

- 10, 4000 Open Hoppers needed off of CSX in the northeast. Cars are needed for use in scrap metal service. Open top hopper

- 20-30, 3000 – 3300 PDs Hoppers needed off of BN or UP preferred in any location, but prefers the west. Cars are needed for use in Cement service. C612

- 20, 17K DOT 111 Tanks needed off of various class 1s in various locations. Cars are needed for use in corn syrup service.

- 100, 15.7K DOT 111 Tanks needed off of CSX or NS in the east. Cars are needed for use in Molten Sulfur service.

- 30, 17K-20K DOT 111 Tanks needed off of UP or BN in Texas. Cars are needed for use in UAN service.

- 30-40, 30K 117, DOT-111, CPC 1232 Tanks needed off of UP or BN in Iowa. Cars are needed for use in CO2 & Ethanol service.

- 1-2, Any DOT 111, 117, CPC 1232 Tanks needed off of any class 1 in Texas. Cars are needed for use in Any service. Coiled and Insulated

- 45, 3000 cf PDs Hoppers needed off of any class 1 in Texas. Cars are needed for use in 3 years service. Negotiable

Lease Offers

- 100-200, 31.8, 1232 Tanks located off of BN in Chicago. Cars are clean Sale or Lease

- 70, 25.5K, 117J Tanks located off of UP in Texas. Cars are clean Call for information

- 150, 30K, DOT111 Tanks located off of various class 1s in various locations. Cars were last used in Ethanol. Call for information

- 30, 23.5K, DOT 111 Tanks located off of UP or BN in Texas. Cars were last used in Clean / UAN.

- 25-100, 17.6K, Dot 111 Tanks located off of UP or BN in Midwest. Cars were last used in Fertilizer / Corn syrup. Free Move

- 20, 20k, Dot 111 Tanks located off of CSX in GA. Cars are clean

- 2, 20K, Dot 111 Tanks located off of UP in TX. Cars are clean

- 5, 20K, Dot 111 Tanks located off of UP in TX. Cars were last used in Sulfuirc Acid. Free Move

- 108, 28.3K, 117R Tanks located off of CN in Canada. Cars were last used in Crude. Free Move, Dirty to Dirty

Sales Offers

- 100, 28.3K, 117J Tanks located off of various class 1s in multiple locations. Clean

- 100, 30K, DOT 111 Tanks located off of various class 1s in multiple locations. Clean

- 100-200, 31.8K, CPC 1232` Tanks located off of BN in Chicago. Sale or Lease

Call PFL today to discuss your needs and our availability and market reach. Whether you are looking to lease cars, lease out cars, buy cars or sell cars call PFL today at 239-390-2885

PFL offers turn-key solutions to maximize your profitability. Our goal is to provide a win/win scenario for all and we can handle virtually all of your railcar needs. Whether it’s loaded storage, empty storage, subleasing or leasing excess cars, filling orders for cars wanted, mobile railcar cleaning, blasting, mobile railcar repair, or scrapping at strategic partner sites, PFL will do its best to assist you. PFL also assists fleets and lessors with leases and sales and offers Total Fleet Evaluation Services. We will analyze your current leases, storage, and company objectives to draw up a plan of action. We will save Lessor and Lessee the headache and aggravation of navigating through this rapidly changing landscape.

PFL IS READY TO CLEAN CARS TODAY ON A MOBILE BASIS WE ARE CURRENTLY IN EAST TEXAS

Live Railcar Markets

| CAT | Type | Capacity | GRL | QTY | LOC | Class | Prev. Use | Offer | Note |

|---|