“The more we do, the more we can do.”- William Hazlitt

Jobs Update

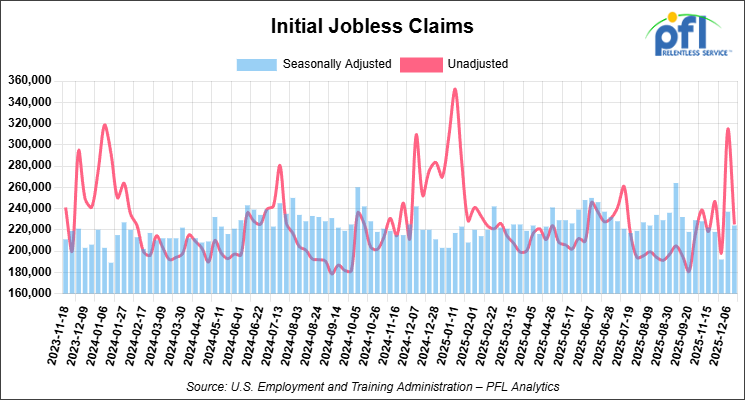

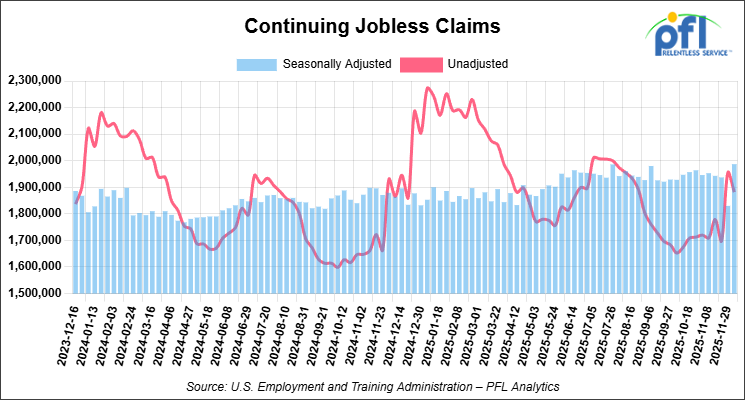

- Initial jobless claims seasonally adjusted for the week ending December 13, 2025 came in at 224,000, versus the adjusted number of 237,000 people from the week prior, down 13,000 people week over week.

- Continuing jobless claims came in at 1,987,000, versus the adjusted number of 1,830,000 people from the week prior, up 157,000 week-over-week.

Stocks closed higher on Friday of last week and mixed week-over-week

The DOW closed higher on Friday of last week, up 182.73 points (0.38%), closing out the week at 48,134.58, down -323.47 points week-over-week. The S&P 500 closed higher on Friday of last week, up 59.95 points (0.88%), and closed out the week at 6,834.71, up +7.30 points week-over-week. 00 up +112.45 points week-over-week.

In overnight trading, DOW futures traded higher and are expected to open at ______ this morning, up/down ______ points from Friday’s close.

Crude oil closed higher on Friday of last week, but lower week-over-week

West Texas Intermediate (WTI) crude closed up +51 cents per barrel (0.9%), to close at $56.66 on Friday of last week, but down -78 cents week-over-week. Brent crude closed up +65 cents per barrel (1.1%), to close at $60.47, but down -65 cents week-over-week.

One Exchange WCS (Western Canadian Select) for February delivery settled on Friday of last week at US$13.00 below the WTI-CMA (West Texas Intermediate – Calendar Month Average). The implied value was US$42.85 per barrel.

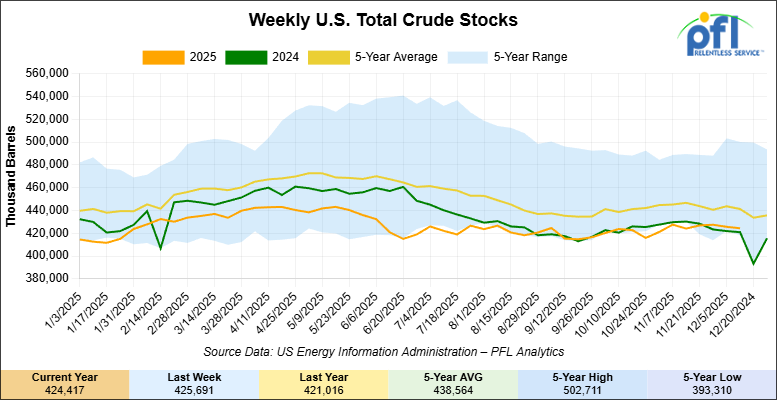

U.S. commercial crude oil inventories (excluding those in the Strategic Petroleum Reserve) decreased by 1.3 million barrels week-over-week. At 424.4 million barrels, U.S. crude oil inventories are 4% below the five-year average for this time of year.

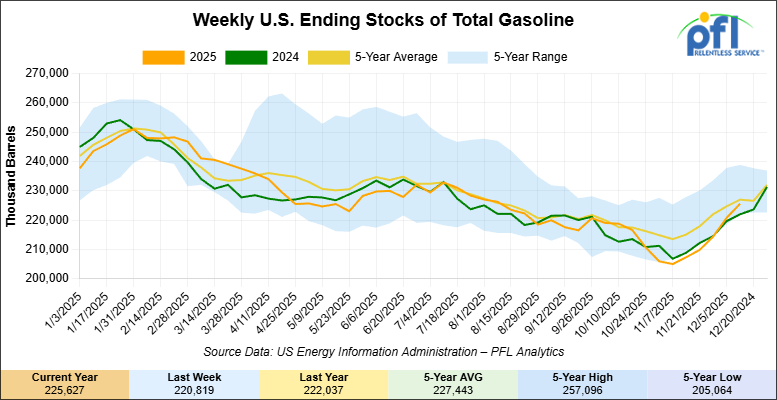

Total motor gasoline inventories increased by 4.8 million barrels week-over-week and are slightly below the five-year average for this time of year.

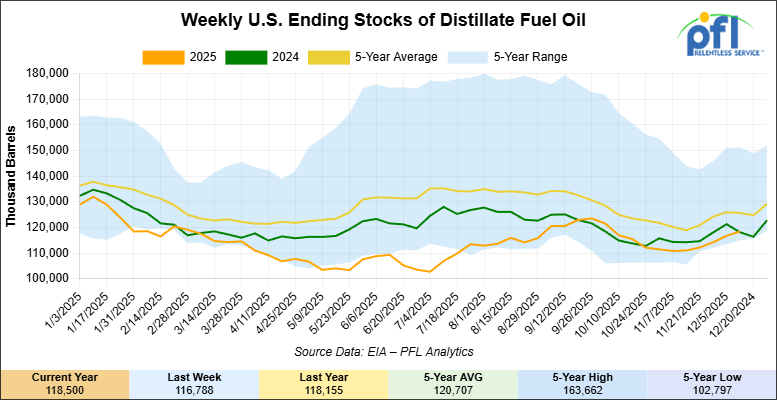

Distillate fuel inventories increased by 1.7 million barrels week-over-week and are 6% below the five-year average for this time of year.

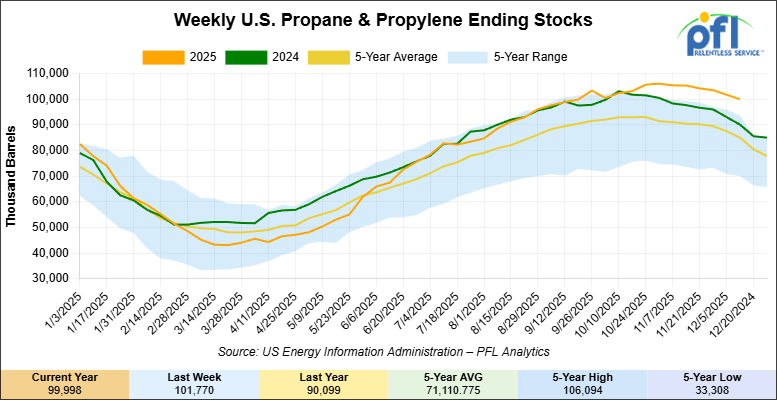

Propane/propylene inventories decreased 1.8 million barrels week-over-week and are 17% above the five-year average for this time of year.

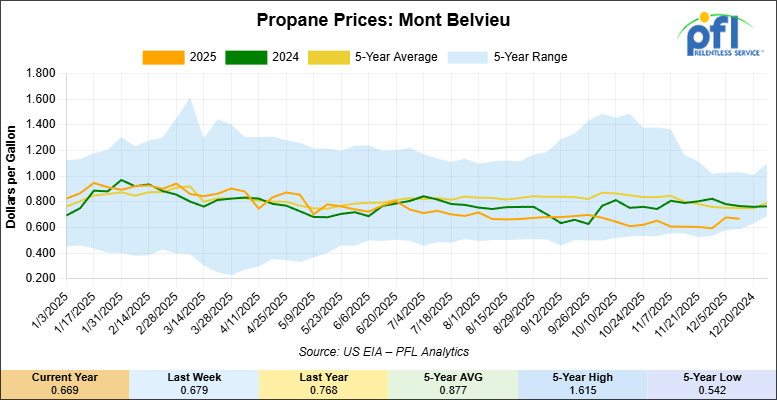

Propane prices closed at 66.9 cents per gallon on Friday of last week, down 1 cent per gallon week-over-week, and down 9.9 cents per gallon year-over-year.

Overall, total commercial petroleum inventories increased by 2.1 million barrels week-over-week during the week ending December 12, 2025.

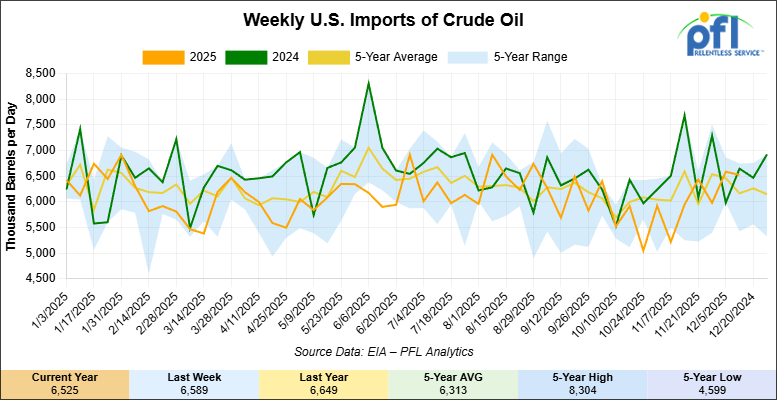

U.S. crude oil imports averaged 6.5 million barrels per day during the week ending December 12, 2025, a decrease of 64,000 barrels per day week-over-week. Over the past four weeks, crude oil imports averaged 6.4 million barrels per day, 1.8% less than the same four-week period last year. Total motor gasoline imports (including both finished gasoline and gasoline blending components) averaged 834,000 barrels per day, and distillate fuel imports averaged 268,000 barrels per day during the week ending December 12, 2025.

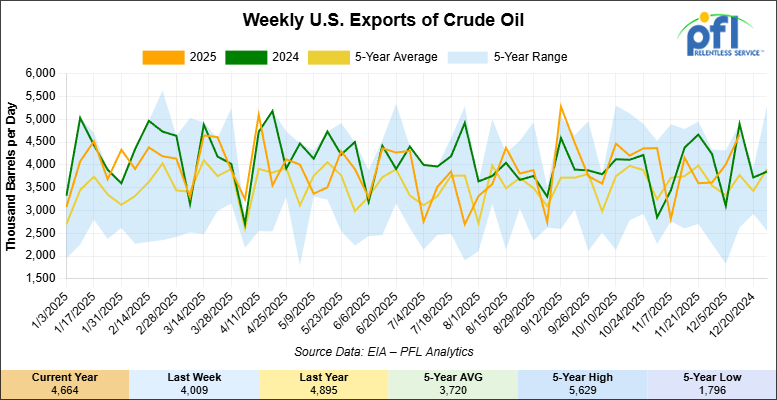

U.S. crude oil exports averaged 4.664 million barrels per day during the week ending December 12, 2025, an increase of 655,000 barrels per day week-over-week. Over the past four weeks, crude oil exports averaged 3.971 million barrels per day.

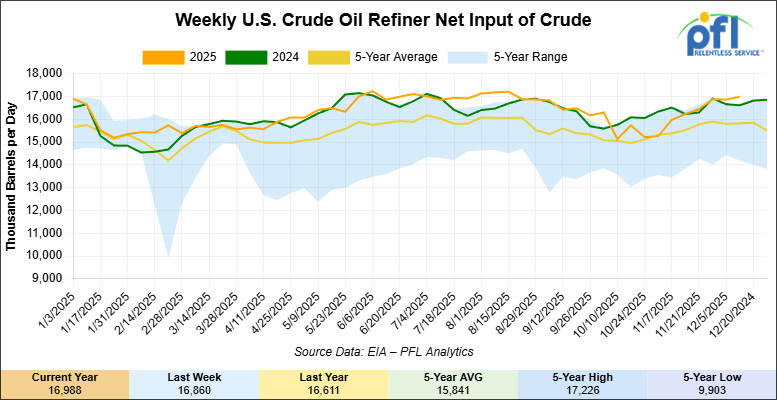

U.S. crude oil refinery inputs averaged 17 million barrels per day during the week ending December 12, 2025, which was 129,000 barrels per day more week-over-week.

WTI futures are poised to open at $57.16, down -28 cents from Friday’s close.

North American Rail Traffic

Week Ending December 17, 2025:

Total North American weekly rail volumes were down (-2.93%) in week 51, compared with the same week last year. Total Carloads for the week ending December 17, 2025 were 318,120, down (-2.73%) compared with the same week in 2024, while weekly Intermodal volume was 356,352, down (-3.10%) year over year. 9 of the AAR’s 11 major traffic categories posted year-over-year decreases. The largest decrease came from Forest Products (-19.12%), while the largest increase was Coal (+9.63%).

In the East, CSX’s total volumes were up (+1.76%), with the largest decrease coming from Metallic Ores and Metals (-17.47%), while the largest increase came from Intermodal Units (+8.04%). NS’s total volumes were down (-0.19%), with the largest increase coming from Petroleum & Petroleum Products (+25.32%), while the largest decrease came from Grain (-26.65%).

In the West, BNSF’s total volumes were down (-2.47%), with the largest increase coming from Other (+9.65%), while the largest decrease came from Metallic Ores and Metals (-24.33%). UP’s total volumes were down (-4.52%), with the largest increase coming from Coal (+22.13%), while the largest decrease came from Grain (-20.06%).

In Canada, CN’s total volumes were down (-4.34%), with the largest increase coming from Other (+134.27%), while the largest decrease came from Chemicals (-16.71%). CPKC’s total volumes were down (-22.63%), with the largest increase coming from Coal (+14.06%), while the largest decrease came from Forest Products (-65.33%).

Source Data: AAR – PFL Analytics

North American Rig Count Summary

Rig Count

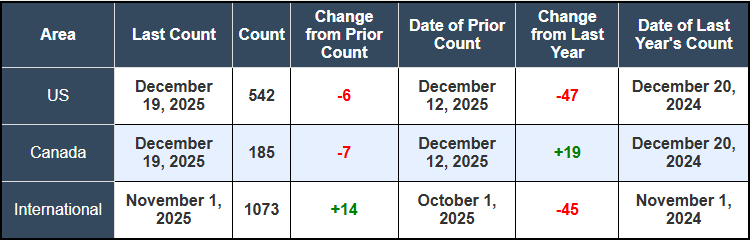

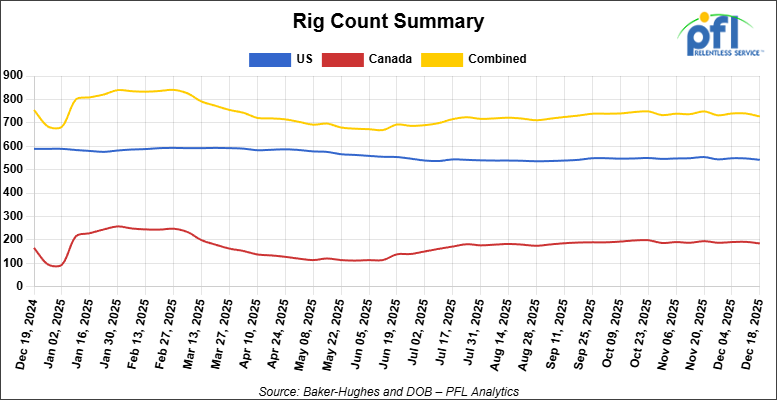

North American rig count was down by -13 rigs week-over-week. The U.S. rig count was down by -6 rigs week-over-week, and down by -47 rigs year-over-year. The U.S. currently has 542 active rigs. Canada’s rig count was down by -7 rigs week-over-week but up by +19 rigs year-over-year. Canada currently has 185 active rigs. Overall, year-over-year we are down by -28 rigs collectively.

We are watching a few things out there for you:

We are watching Petroleum Carloads

The four-week rolling average of petroleum carloads carried on the six largest North American railroads rose to 30,074 from 30,067 which was an increase of +7 rail cars week-over-week. Canadian volumes were mixed. CPKC’s shipments were higher by +3.0% week-over-week, CN’s volumes were lower by -3.0% week-over-week. U.S. shipments were mostly lower. The BNSF had the largest percentage decrease and was down by -17.0%. The NS was the sole gainer and were up by +5.0%

We are Watching Biodiesel Rail Volumes Surge

While crude-by-rail holds steady, the renewable fuels sector is showing significant momentum. New data from the EIA highlights a 24% year-over-year increase in biodiesel rail shipments from the Midwest to the West Coast in September, reaching 9,000 b/d.

This lane is becoming a critical artery for the tank car market. The West Coast relies heavily on rail for biofuels due to a lack of local production capacity relative to its demand, driven by Low Carbon Fuel Standards (LCFS). Total rail shipments of biodiesel from the midcontinent to all regions averaged 12,500 b/d, a clear signal that renewable diesel and biodiesel continue to offer a bright spot for fleet utilization, even as traditional petroleum flows face headwinds.

We are Watching Left Wing Canadian Prime Minister Carney

In Canada, Prime Minister Mark Carney is pushing a “Grand Bargain” on energy that balances new infrastructure with stricter environmental rules. A new Angus Reid poll reveals that 60% of Canadians support Carney’s proposed Alberta-to-BC pipeline, a project formalized in a recent MOU with Alberta Premier Danielle Smith. While the project aims to unlock Asian markets for Canadian crude, it faces fierce opposition from BC’s Premier Eby, setting the stage for a constitutional showdown.

As part of this energy package, Ottawa unveiled “Enhanced Methane Regulations” on December 17. The rules, effective 2028, target a 75% reduction in emissions by 2035. Ottawa’s new “Enhanced Methane Regulations,” finalized this week, come with a government-estimated compliance cost of $48 per tonne of CO2e. However, industry data from the Canadian Gas Association (CGA) and field testing suggests the real-world cost is closer to $3,000 per tonne. This massive gap is critical for “marginal” or low-volume wells, which often rely on older pneumatic devices that are now targeted for replacement. If compliance costs hit $3,000/tonne, operators may choose to shut in these older wells rather than upgrade them. These smaller, dispersed wells often lack pipeline connections and rely on truck-to-rail transloading. A wave of shut-ins in the conventional heavy oil patches of Alberta and Saskatchewan would disproportionately hurt the manifest crude-by-rail business, which utilizes general service tank cars, unlike the unit train business that serves major oil sands projects.

We are Watching Winter Weather Hit the Network

Winter struck with force last week, but the epicenter was in the Northwest, not the East. BNSF was battling with a “persistent weather pattern” that hammered the Pacific Northwest and the Northern Tier with historic rainfall and flooding occurring over the past nine days. The carrier reported that multiple subdivisions have been temporarily taken out of service due to washouts, downed trees, and damaged rail.

As if the flooding wasn’t enough, Arctic air moving east triggered ground blizzard conditions across Montana, Wyoming, and the Upper Midwest. BNSF reported wind gusts exceeding 100 mph in Montana and 70 mph in the Twin Cities, forcing train length restrictions and driving up terminal dwell times. For shippers moving freight across the Northern Corridor, expect reduced velocity and delays as crews work to restore service. Meanwhile, in Eastern Canada, maritime operations have faced terminal closures due to adverse weather, particularly affecting Newfoundland supply lines.

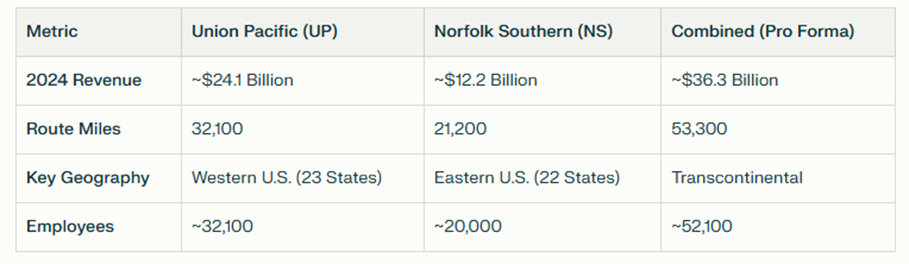

We continue to watch the UP and NS Merger

In a move that promises to reshape the North American rail landscape, Union Pacific (UP) and Norfolk Southern (NS) officially filed their merger application with the Surface Transportation Board (STB) last Friday. The $85 billion deal aims to create the nation’s first true transcontinental railroad; a concept the carriers argue is essential to compete with trucking and streamline the U.S. supply chain.

Union Pacific vs. Norfolk Southern: By the Numbers:

For railcar owners and lessors, the filing contains a critical promise: “improved customer asset utilization.” The carriers contend that a unified network will eliminate time-consuming interchanges—specifically the “artificial barrier” at the Mississippi River—allowing cars to turn more quickly and reducing equipment costs for shippers. The combined entity plans to introduce six new manifest trains to bridge the East-West divide and 84,000 new single-line lanes. However, the proposal faces immediate headwinds; while the deal has secured support from the SMART-TD union and an endorsement from President Trump, it has lost the backing of the Teamsters-affiliated Brotherhood of Locomotive Engineers and Trainmen (BLET), who voiced concerns this week over job security and safety standards.

The Union Pacific (UP) and Norfolk Southern (NS) filing isn’t just big; it is the first test of the modern regulatory era, and the details reveal a clash between operational theory and market reality.

This is the first Class I merger application to be judged under the Surface Transportation Board’s (STB) stricter 2001 merger rules. Unlike the CPKC deal, which was approved under older, more permissive standards, UP and NS must prove their union will enhance competition, not just preserve it. This is a high bar. The applicants argue that creating a transcontinental line allows them to compete with long-haul trucking, converting an estimated 2 million truckloads annually to rail.

For railcar lessors, the most tangible promise is the removal of the “artificial barrier” at the Mississippi River. The carriers claim this will eliminate 2,400 daily railcar handoffs. In theory, this reduction in dwell time increases fleet velocity, effectively increasing capacity without adding cars. However, for lessors, higher velocity can sometimes soften demand for spot market cars if the existing fleet becomes more efficient.

The American Chemistry Council (ACC) has come out swinging, using the term “Nationwide Duopoly”. Their fear is that if UP-NS succeeds, BNSF and CSX will inevitably merge to survive, leaving shippers with only two mega-systems. Chemical shippers are particularly vulnerable to “captive” pricing, and without robust reciprocal switching rules, they see this merger as a threat to their leverage.

Interestingly, labor is divided. The SMART-TD union supports the deal, likely secured by promises of growth and crew consist preservation. However, the Teamsters-affiliated BLET opposes it, citing safety concerns and skepticism about the “growth” narrative. This split could complicate the political optics for the STB, which is sensitive to labor impacts.

The reaction from the rest of the industry has been swift and sharp. Canadian Pacific Kansas City (CPKC) and Canadian National (CN) both issued warnings Friday regarding the merger’s potential to stifle competition. CPKC described the proposal as a “radical change” that poses “extraordinary risks” to the current rail network structure, while CN argued the deal would reduce shipping options by creating a single dominant entity controlling vast swaths of the continent’s rail traffic.

Simultaneously, the American Chemistry Council (ACC) and American Fuel & Petrochemical Manufacturers (AFPM) have come out against the deal. The AFPM stated that without conclusive proof that the merger will enhance competition, it should be denied, citing fears that a new “mega-railroad” would control 51% of petrochemical traffic and 41% of crude and NGL movements. For PFL’s tank car customers, this consolidation raises valid concerns about pricing leverage and service accountability in a market with fewer Class I options.

We are Watching the STB

On the regulatory front, the U.S. Senate confirmed Michelle A. Schultz to a second term as a member of the Surface Transportation Board (STB) on December 18. Her confirmation comes at a pivotal moment, as the Board prepares for what is expected to be a lengthy and rigorous review of the UP-NS application. STB Chairman Patrick Fuchs has already signaled that the agency will take the necessary time to assess the merger’s impact, with reports suggesting an extended procedural timeline to ensure all stakeholders—including skeptical shippers and rival railroads—can be heard.

We are Watching Midland

A quiet circular from November is gaining volume as fleet owners assess the impact of removing Midland vacuum relief valves.

In November, the Association of American Railroads (AAR) cancelled Service Trial 429 for Midland Manufacturing vacuum relief valves (models A-210, A-211, and A-212). While the circular has been out for several weeks, it has started gaining more attention across the industry as owners and lessors assess fleet exposure. The ruling requires that any valves installed under this trial must be removed from service within three years or at the next valve requalification, whichever comes first. Replacement valves must be fully AAR-approved, non-trial components.

This is not an immediate out-of-service issue, but it does introduce a defined compliance path. Affected valves will require planned replacement and subsequent TCID updates. Critically, maintenance timing, shop access, and car positioning should be reviewed ahead of qualification cycles. With an estimated tens of thousands of cars affected, owners who delay planning may find themselves competing for shop capacity later in the compliance window.

PFL Perspective:

Beyond scheduling the physical valve replacement, many fleets are now evaluating approved alternative valve options, qualification timing, and how to sequence work with minimal disruption. PFL works with car owners and lessors to help with coordination, planning, positioning, and execution, including discussing replacement paths, aligning work with upcoming qualifications, and managing storage or staging as cars cycle through maintenance. Early planning can help avoid unnecessary downtime later. Call PFL today- don’t wait for compliance dates to kick in and leave you scrambling.

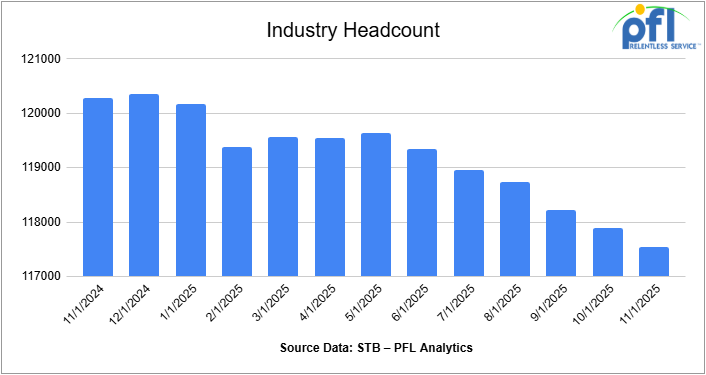

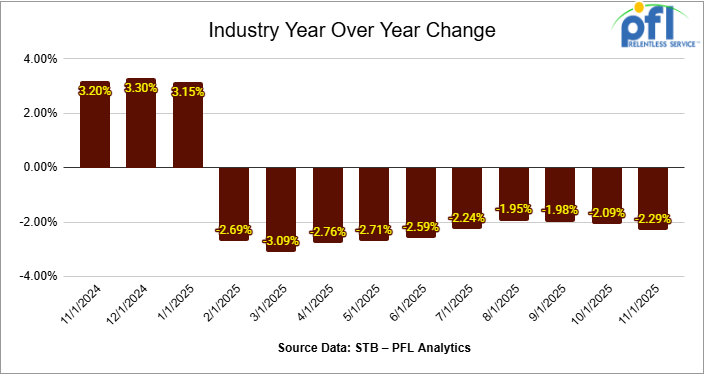

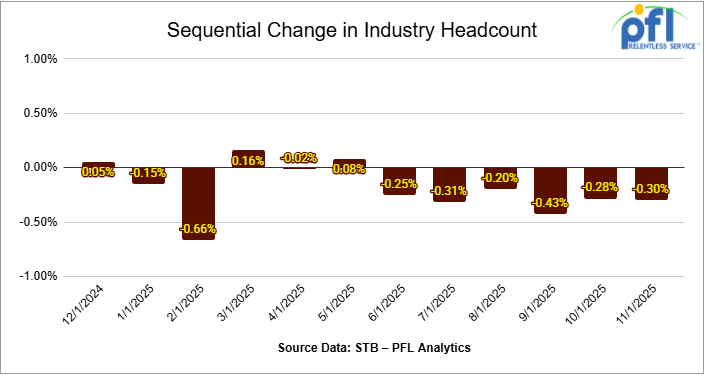

We are Watching Class 1 Head Count

Class I railroads employed 117,540 workers in the United States in November 2025, a 0.30% decrease from October 2025’s count of 117,888 and a 2.29% year-over-year decline from November 2024’s total of 120,290, according to Surface Transportation Board data.

None of the six employment categories posted a month-over-month increase between October and November. All categories declined over the month.

The categories that posted month-over-month decreases were Executives, officials, and staff assistants, down 0.16% to 8,146 workers; Professional and administrative, down 0.33% to 9,001 workers; Maintenance of way and structures, down 0.25% to 29,012 workers; Maintenance of equipment and stores, down 0.36% to 16,444 workers; Transportation (other than train and engine), down 0.86% to 4,847 workers; and Transportation (train and engine), down 0.26% to 50,090 workers.

On a year-over-year basis, two categories posted employment gains: Executives, officials, and staff assistants, up 3.68%, and Maintenance of way and structures, up 0.35%.

Categories that registered year-over-year declines in November were Professional and administrative, down 7.05%; Maintenance of equipment and stores, down 4.13%; Transportation (other than train and engine), down 3.98%; and Transportation (train and engine), down 3.00%.

We are Watching Economic Indicators

Consumer Spending

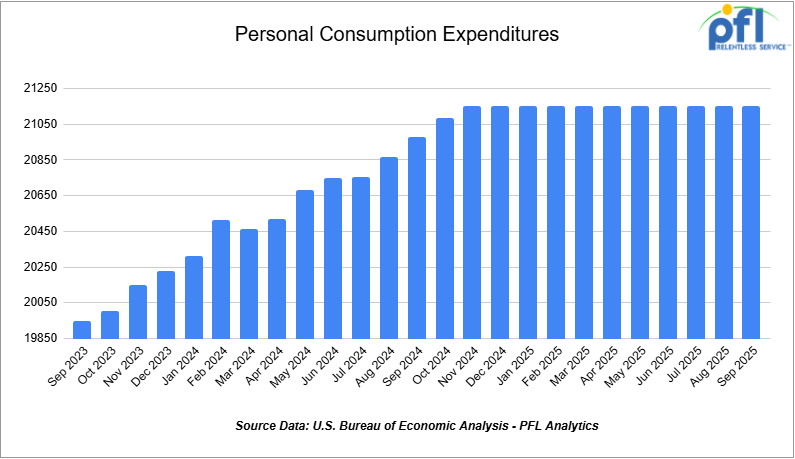

In September 2025, total consumer spending increased by 0.3% over August 2025, reflecting continued, albeit modest, gains in household demand amid persistent price pressures. According to the U.S. Bureau of Economic Analysis, current‑dollar personal consumption expenditures (PCE) rose by $65.1 billion, with the increase driven by a $63.0 billion rise in services spending and a $2.1 billion increase in goods spending.

The personal saving rate slipped slightly to 4.7% in September, down from earlier summer levels, indicating consumers remained willing to spend even as prices remained elevated.

On inflation, the PCE price index rose by 2.8% year‑over‑year, up from 2.7% in August, while core PCE inflation (excluding food and energy) also increased by 2.8% year‑over‑year, reflecting persistent underlying price pressures above the Federal Reserve’s 2% target.

Lease Bids

- 30-50, 6000cf Steel Hopper located off of CSX or NS in East. For use in petcoke service. Period: 5 Years.

- 10, 2500CF Open Top Hopper located off of UP or BN in Texas. For use in aggregate service. Period: 5 years. Need Rapid Discharge Doors.

- 50, 23.5-25.5 DOT111 Tank located off of Any Class 1 in USA. For use in Asphalt service. Period: 5 years.

- 100, 21.9K 117J Tank located off of All Class 1s in Midwest. For use in CO2 service. Period: 6 months.

- 30-50, 30K 117J Tank located off of NS or CSX in Northeast. For use in C5 service. Period: 1 year.

Sales Bids

- 28, 3400CF Hopper Covered located off of UP BN in Texas. For use in Cement service.Cement Gates needed.

- 20, 17K Tank DOT111 located off of various class 1s in various locations. For use in corn syrup service.

- 120, Various Gondola Open-Top Aluminum Rotary located off of various class 1s in various locations. For use in Sulphur service.Built 2004 or later.

Lease Offers

- 100, 30K CPC1232 Tanks located off of UP or BN in Texas. Last used in Diesel.

- 100, 30K DOT117J Tanks located off of UP or BN in Texas. Last used in Gasoline.

- 100, 29K DOT117J Tanks located off of UP or BN in Texas. Last used in Gasoline. Coiled and Insulated.

- 36, 6351 Covered Hopper located off of CN in Wisconsin. Last used in Grain. through 2/27.

- 29, 6580 Covered Hopper located off of CN in Wisconsin. Last used in Grain. through 2/26.

- 18, 6580 Covered Hopper located off of CN in Wisconsin. Last used in Grain. through 2/27.

- 9, 5400 Covered Hopper located off of CN in Wisconsin. Last used in Grain. through 2/27.

- 21, 6351 Covered Hopper located off of CN in Wisconsin. Last used in DDG. Available until February 2027.

- 29, 6500 Covered Hopper located off of CN in Wisconsin. Last used in DDG. Available until February 2027.

- 50, 5380 Covered Hopper located off of UP or BN in Houston. Last used in Fertilizer. Cars are currently clean. Available until February.

- 50, 20K DOT117J Tank located off of All Class 1s in Moving. Last used in Styrene.

- 29, 25.5K DOT117J Tank located off of UP or BN in Texas. Cars are currently clean. Cars are currently clean.

- 90, 30K DOT117J Tank located off of UP or BN in Corpus Christie. Last used in Diesel.

Sales Offers

- 21, 50′ Boxcar Plate Cs located off of various class 1s in NM. End of Life.

- 3, 50′ Boxcar Plate Cs located off of various class 1s in multiple locations. End of Life.

- 27, 50′ Boxcar Plate Cs located off of various class 1s in PQ. End of Life.

- 100, 3250 Covered Hoppers located off of various class 1s in multiple locations. Sand Cars.

- 5, 2740 Mill Gondolas located off of various class 1s in NC. End of Life.

- 1, 2260 Mill Gondolas located off of various class 1s in AL. End of Life.

- 30, 2740 Mill Gondolas located off of various class 1s in multiple locations. End of Life.

- 21, 2740 Mill Gondolas located off of various class 1s in WA. End of Life.

- 9, 4750 Covered Hoppers located off of various class 1s in multiple locations. End of Life.

- 5, 4750 Covered Hoppers located off of various class 1s in multiple locations. End of Life.

- 50, 31.8K Tank CPC 1232s located off of UP or BN in TX. Requal Due in 2025.

- 100, 4600CF Open Top Hoppers located off of BN or CSX in Southeast. N/A.

Call PFL today to discuss your needs and our availability and market reach. Whether you are looking to lease cars, lease out cars, buy cars, or sell cars call PFL today at 239-390-2885

Live Railcar Markets

| CAT | Type | Capacity | GRL | QTY | LOC | Class | Prev. Use | Offer | Note |

|---|

PFL will be at the Following Conferences

- Where: La Quinta, CA

- Attending: David Cohen (954-729-4774)

- Conference Website

- Where: Hyatt Regency Dallas in Dallas, TX

- Attending:Curtis Chandler (239.405.3365), David Cohen (954-729-4774), Brian Baker (239.297.4519), Cyndi Popov(403) 402-5043

- Conference Website