“Have patience. All things are difficult before they become easy.” – Saadi

Jobs Update

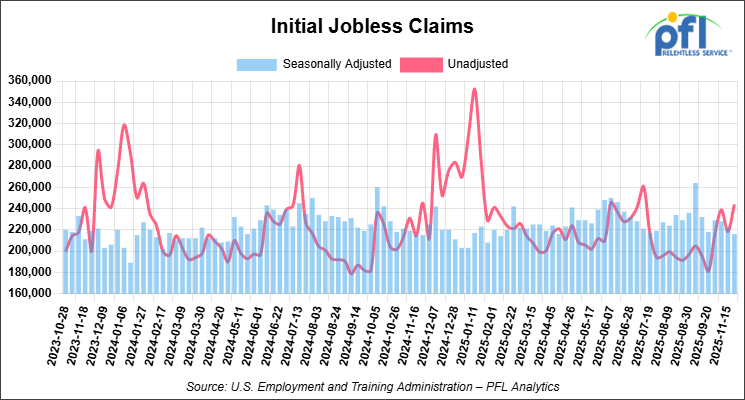

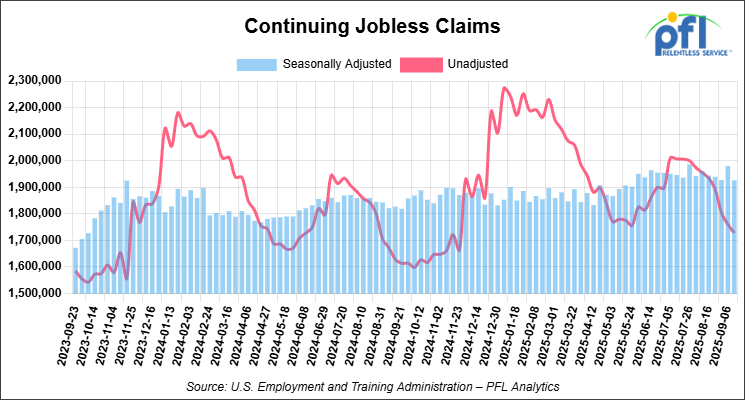

- Initial jobless claims seasonally adjusted for the week ending November 22, 2025 came in at 216,000, versus the adjusted number of 222,000 people from the week prior, down 6,000 people week over week.

- Continuing jobless claims came in at 1,926,000, versus the adjusted number of 1,980,000 people from the week prior, down 54,000 week-over-week.

Stocks closed higher on Friday of last week and higher week-over-week

The DOW closed higher on Friday of last week, up 289.30 points (0.61%), closing out the week at 47,716.42, up 1,471.01 points week-over-week. The S&P 500 closed higher on Friday of last week, up 36.48 points (0.54%), and closed out the week at 6,849.09, up 246.10 points week-over-week. The NASDAQ closed higher on Friday of last week, up 151 points (0.65%), and closed out the week at 23,365.69, up 1,092.61 points week-over-week.

In overnight trading, DOW futures traded lower and are expected to open at 47,550 this morning, down -193 points from Friday’s close.

Crude oil closed lower on Friday of last week but higher week-over-week

West Texas Intermediate (WTI) crude closed down -0.10 per barrel (-0.17%), to close at $58.55 on Friday of last week, but up $0.49 week-over-week. Brent crude closed down -0.14 per barrel (-0.22%), to close at $63.20, but up $0.64 week-over-week.

One Exchange WCS (Western Canadian Select) for January delivery settled on Friday of last week at US$12.40 below the WTI-CMA (West Texas Intermediate – Calendar Month Average). The implied value was US$45.97 per barrel.

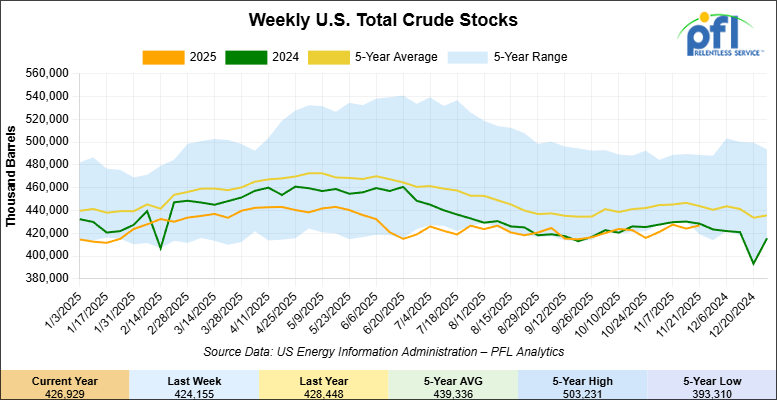

U.S. commercial crude oil inventories (excluding those in the Strategic Petroleum Reserve) increased by 2.8 million barrels week-over-week. At 426.9 million barrels, U.S. crude oil inventories are 4% below the five-year average for this time of year.

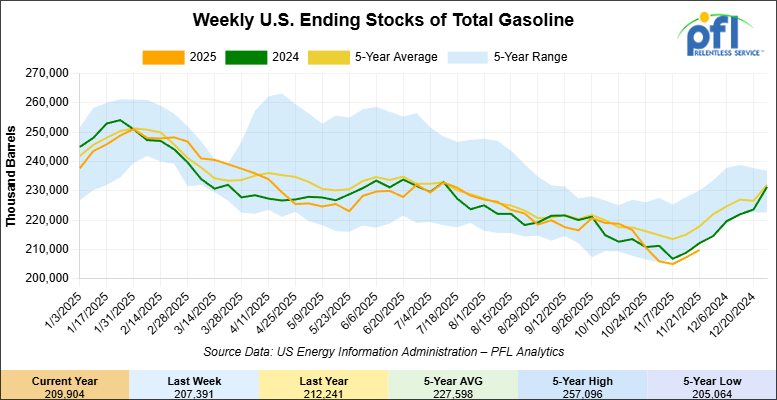

Total motor gasoline inventories increased by 2.5 million barrels week-over-week and are 3% below the five-year average for this time of year.

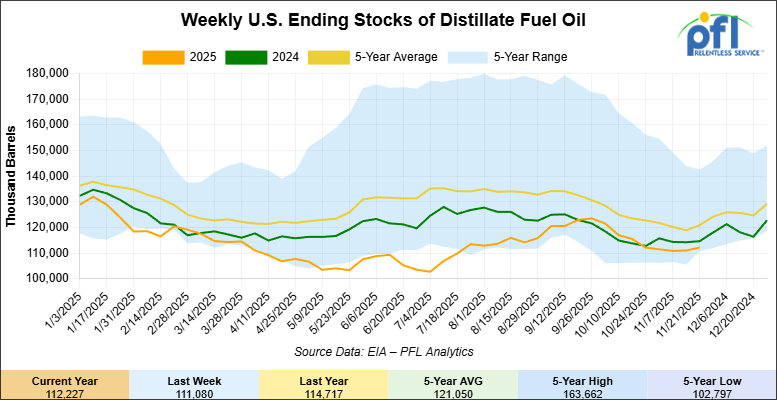

Distillate fuel inventories increased by 1.1 million barrels week-over-week and are 5% below the five-year average for this time of year.

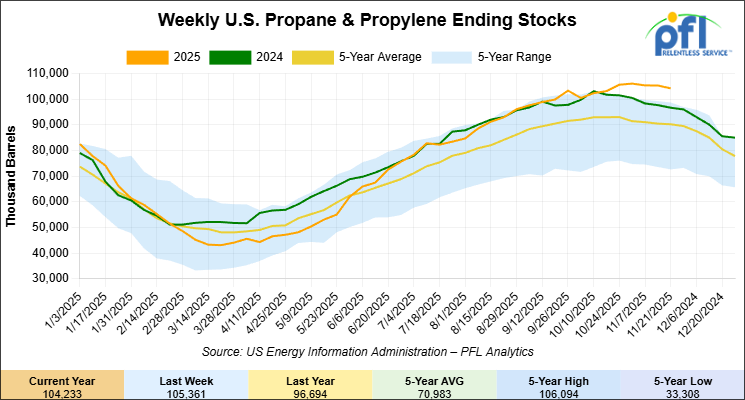

Propane/propylene inventories decreased 1.1 million barrels week-over-week and are 16% above the five-year average for this time of year.

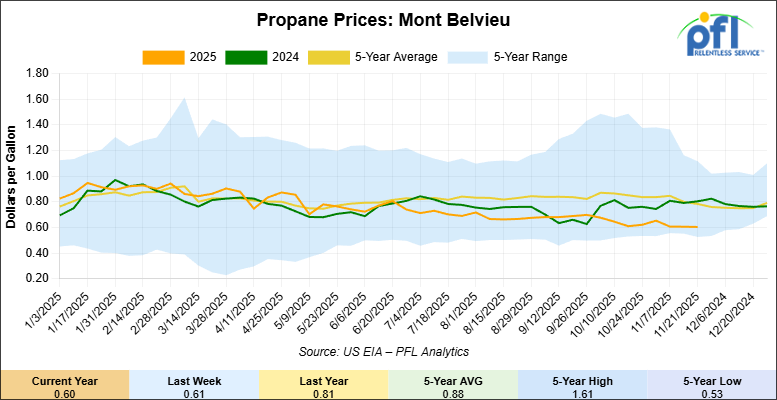

Propane prices closed at 61 cents per gallon on Friday of last week, flat week-over-week, and down 20 cents year-over-year.

Overall, total commercial petroleum inventories increased by 1.6 million barrels week-over-week during the week ending November 21, 2025.

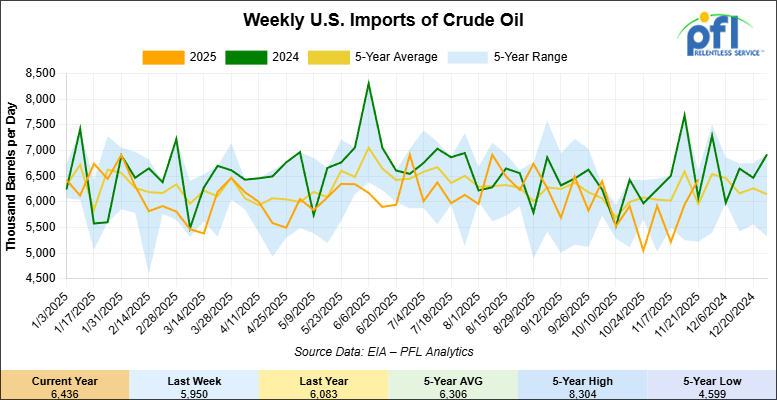

U.S. crude oil imports averaged 6.4 million barrels per day during the week ending November 21, 2025, an increase of 486,000 barrels per day week-over-week. Over the past four weeks, crude oil imports averaged 5.9 million barrels per day, 11.2% less than the same four-week period last year. Total motor gasoline imports (including both finished gasoline and gasoline blending components) averaged 658,000 barrels per day, and distillate fuel imports averaged 199,000 barrels per day during the week ending November 21, 2025.

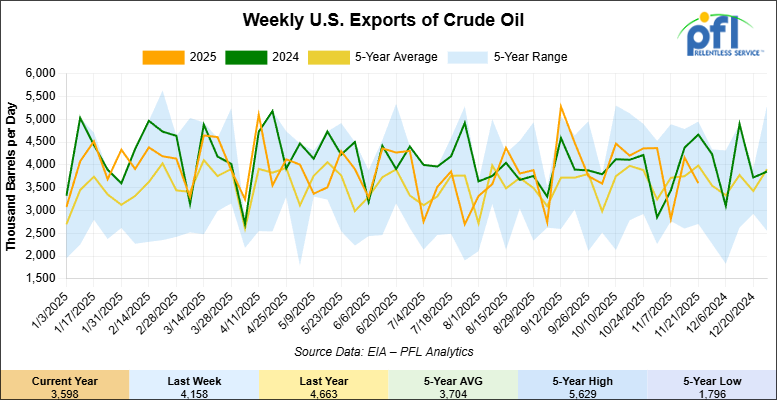

U.S. crude oil exports averaged 3.598 million barrels per day during the week ending November 21, 2025, a decrease of 560,000 barrels per day week-over-week. Over the past four weeks, crude oil exports averaged 3.735 million barrels per day.

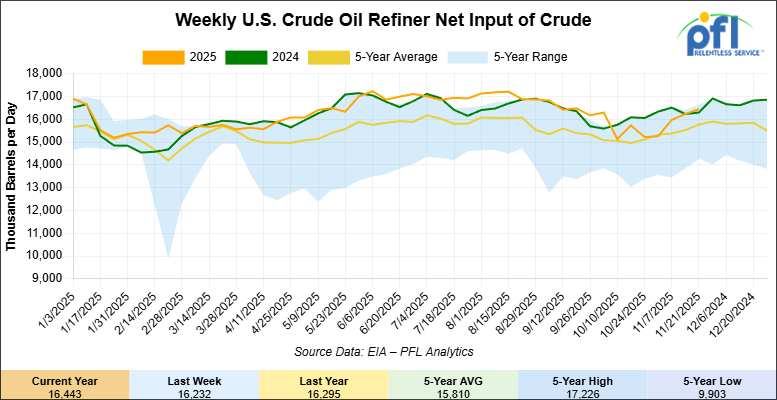

U.S. crude oil refinery inputs averaged 16.4 million barrels per day during the week ending November 21, 2025, which was 211,000 barrels per day week-over-week.

WTI futures are poised to open at $59.28, up 73 cents from Friday’s close.

North American Rail Traffic

Week Ending November 27, 2025:

Total North American weekly rail volumes were down (-5.50%) in week 48, compared with the same week last year. Total Carloads for the week ending November 27, 2025 were 319,755, down (-4.18%) compared with the same week in 2024, while weekly Intermodal volume was 336,580, down (-6.71%) year over year. 7 of the AAR’s 11 major traffic categories posted year-over-year decreases. The largest decrease came from Forest Products (-21.67%), while the largest increase was Coal (+6.71%).

In the East, CSX’s total volumes were up (+1.38%), with the largest decrease coming from Petroleum & Petroleum Products (-23.07%), while the largest increase came from Grain (+53.80%). NS’s total volumes were down (-2.55%), with the largest increase coming from Coal (+19.03%), while the largest decrease came from Grain (-17.10%).

In the West, BNSF’s total volumes were down (-5.33%), with the largest increase coming from Grain (+14.86%), while the largest decrease came from Metallic Ores and Metals (-14.75%). UP’s total volumes were down (-0.96%), with the largest increase coming from Nonmetallic Minerals (+18.14%), while the largest decrease came from Petroleum & Petroleum Products (-10.38%).

In Canada, CN’s total volumes were down (-11.54%), with the largest increase coming from Other (+100.81%), while the largest decrease came from Metallic Ores and Metals (-24.23%). CPKCS’s total volumes were down (-53.47%), with the largest increase coming from Nonmetallic Minerals (-8.72%), while the largest decrease came from Coal (-98.30%).

Source Data: AAR – PFL Analytics

North American Rig Count Summary

Rig Count

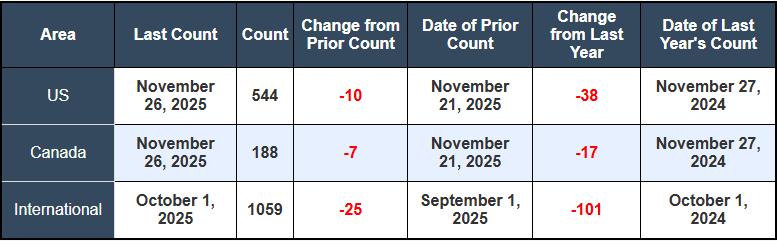

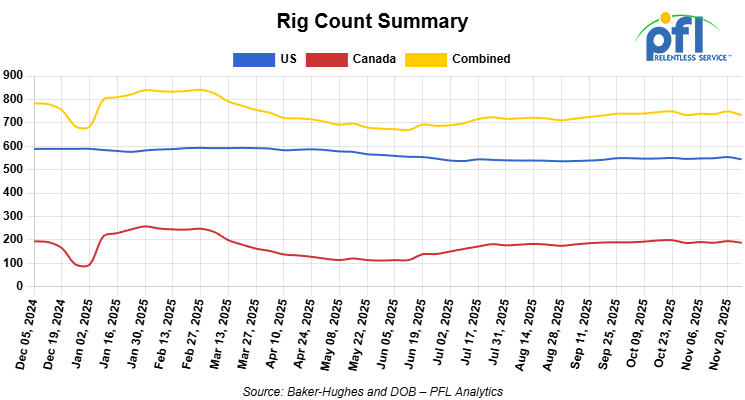

North American rig count was down by -17 rigs week-over-week. The U.S. rig count was down by -10 rigs week-over-week, and down by -38 rigs year-over-year. The U.S. currently has 544 active rigs. Canada’s rig count was down by -7 rigs week-over-week and down by -17 rigs year-over-year. Canada currently has 188 active rigs. Overall, year-over-year we are down by -55 rigs collectively.

We are watching a few things out there for you:

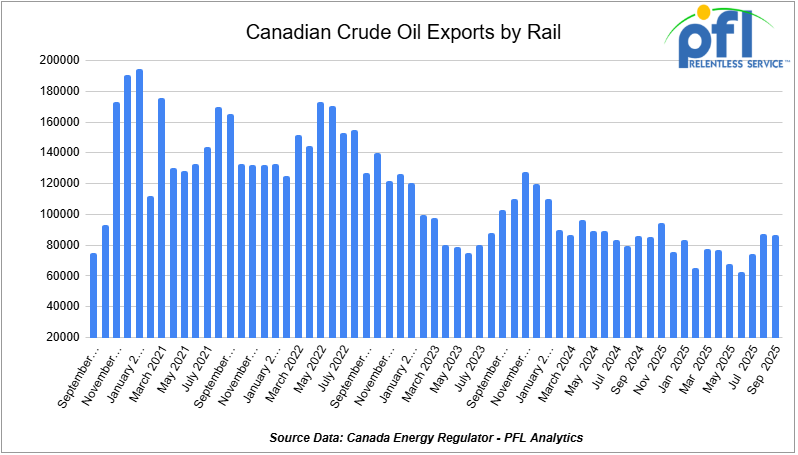

We are watching Canadian Crude by Rail

Crude by rail out of Canada decreased month over month. The Canadian Energy regulator reported on November 26, that 86,711 barrels were exported per day during the month of September 2025, down from 87,141 barrels in August of 2025, a decrease of -430 barrels per day.

Crude by rail will always be necessary out of Canada for stranded oil not connected by pipelines. Raw bitumen, which is shipped as a non-haz product and is not able to flow in pipelines, is competitive with pipeline tolls and is a growing market to keep an eye on. Other factors would be existing long-term contractual commitments and basis – we really need to see basis WTI-CMA (West Texas Intermediate – Calendar Month Average) blowout to -18 per barrel for sustained periods of time to make economic sense. Current rail rates from Alberta to the U.S. Gulf Coast has averaged $15.36 per barrel, making rail competitive whenever WCS-WTI spreads exceed $18 per barrel, including quality adjustments.

Tank car lease rates for non-pressurized units remained stable, despite increased crude oil activity. This suggests adequate equipment supply for current market conditions.

Though there may be some slack in the system right now, room remains on the Transmountain pipeline, but production continues to grow in Alberta. At some point, we will hit a wall where crude will be trapped. There has been some chatter the last few weeks about a new pipeline to Canada’s west coast (see below). We will see if this one comes to fruition – lots of hurdles, opposition and very expensive to build.

We are Watching Carney warm up to Alberta

A massive political and infrastructure development in Canada promises to fundamentally reshape the crude oil logistics landscape, introducing significant long-term risk for the North American rail tank car market while signaling a pragmatic turn in Ottawa.

On Thursday of last week, the federal government of Canada executed a Memorandum of Understanding (MOU) with the province of Alberta, setting in motion a plan for a new high-capacity oil pipeline from Alberta to the northern coast of British Columbia. The pipeline is projected to move up to 1,000,000 barrels of crude oil per day; the deal represents a “seismic shift” in Ottawa’s relationship with the energy sector. Commentators see this as Prime Minister Mark Carney capturing the political “centre ground”- prioritizing economic interests and energy security over ideological gridlock.

In a development welcomed by many in the industry, the accord precipitated the immediate resignation of Environment Minister Steven Guilbeault. The departure of the former Greenpeace activist, who called the agreement a “serious mistake” due to tanker traffic concerns, suggests a cabinet reshuffle aimed at clearing hurdles for industrial development.

This is a classic exchange of environmental concessions for hard infrastructure. In return for Alberta adopting a more stringent industrial carbon pricing regime ($130 per tonne credit value), Ottawa has agreed to suspend the pending oil-and-gas emissions cap and exempt Alberta from federal clean electricity regulations. We wonder what Saskatchewan thinks about this one!

The government agreed to declare a bitumen pipeline carrying “at least one million barrels a day” a “project of national interest,” fast-tracking it under the Building Canada Act. If built, the existing oil tanker ban on the northern B.C. coast would be adjusted to allow exports to Asian markets, breaking a U.S. monopoly on Canadian crude exports. However, like anything the liberals have announced as pro-energy, should be taken with a grain of salt, we wait with bated breath until we see actual results.

We are watching Nutrien

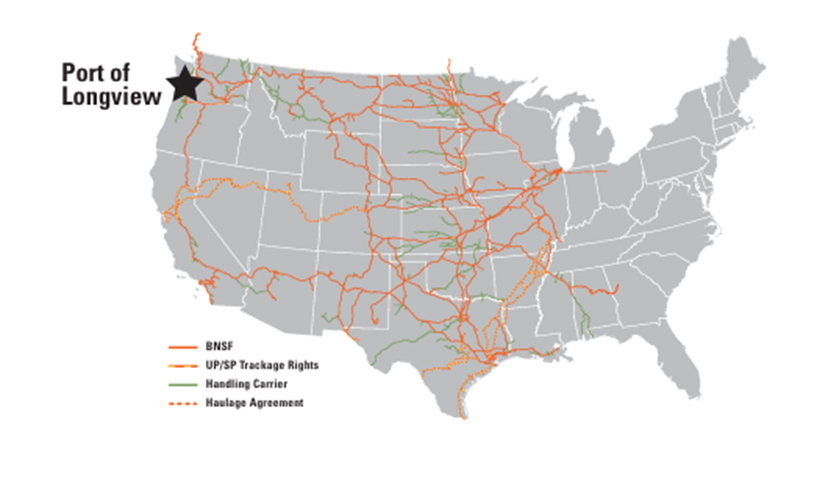

Nutrien Ltd. has made a decisive move that reverberates through the North American logistics sector, opting to invest up to $1 billion in a new export terminal in Longview, Washington, rather than expanding capacity through a Canadian Pacific port. This is not merely a routing adjustment for the world’s largest potash producer; it is a calculated rejection of the current Canadian infrastructure value proposition. By 2031, Nutrien forecasts it will ship as much Canadian-mined potash via U.S. ports as it does through domestic ones, diverting nearly 50% of its non-U.S. bound capacity through foreign territory.

The decision was driven by a rigorous 30-factor commercial assessment where Longview consistently outperformed Canadian alternatives. Nutrien prioritized the “lowest possible total cost per tonne delivered,” and a massive component of that calculation is inland freight and rail velocity.

A critical technical failure point for Canada was the CN Second Narrows Rail Bridge in Vancouver (mentioned in this report on November 10th ). The 97-year-old single-track lift bridge has become a chronic chokepoint for North Shore terminals like Neptune. While Canpotex has repeatedly flagged this vulnerability to Ottawa, no replacement plan has materialized. In contrast, the Port of Longview offered “shovel-ready” capacity and, crucially, dual-carrier access (BNSF and Union Pacific). This competitive tension allows shippers to leverage carriers against one another to secure better long-term rates—an advantage Prince Rupert’s single-carrier (CN only) model cannot match. (see below)

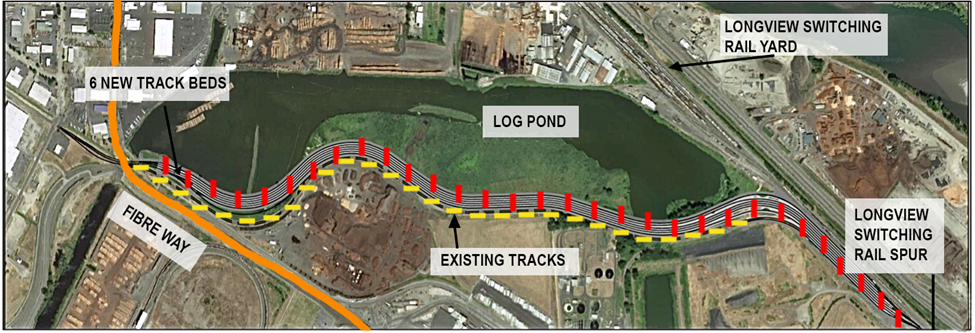

Port of Longview

Source: Port of Longview – PFL Analytics

The divergence highlights a stark contrast in government responsiveness. While the Carney government has pledged to “build big” and double non-US exports, the machinery of the Canadian state was caught flat-footed. Conversely, the U.S. Department of Transportation recently advanced a $35.9 million loan to the Port of Longview specifically to expand rail corridor capacity. The U.S. offered immediate financial engagement and physical rail capacity; Canada offered “internal confusion” regarding which department was responsible for the file.

Beyond the physical infrastructure, the business environment in left wing Carney’s Canada remains a distinct liability. Nutrien’s decision timeline coincided with a period of intense instability, marked by the 2023 Seaway strike, the 2024 West Coast longshoremen strike, and the Class 1 rail lockout in August 2024.

The implementation of Bill C-58 (anti-replacement worker legislation), which came into full effect in June 2025, has further skewed the risk profile. For a company planning a facility with a 30-year operational life, the inability to ensure business continuity during labor disputes is a non-starter. Nutrien’s move to the U.S. leverages established labor relationships and a regulatory framework that offers a higher degree of operational certainty than the current Canadian climate.

This divergence sets a concerning precedent for Prime Minister Mark Carney’s critical minerals strategy. Potash is a strategic commodity for Canada and routing a significant portion of export volume through the U.S. compromises it’s logistical sovereignty. If the structural deficits in cost efficiency and rail competition persist, Canada should anticipate “export leakage” from other future mining projects in copper, nickel, and graphite. Capital flows to the path of least resistance (and where it is treated best), and right now, that path is in the United States.

We are Watching the NS and the UP

The looming formal application for the proposed mega-merger between Union Pacific (UP) and Norfolk Southern (NS), expected as early as this week, has officially taken center stage, injecting a heavy dose of regulatory uncertainty into the market.

The UP is aggressively championing this consolidation as the necessary evolution toward the nation’s first true transcontinental railroad. Their pitch to shippers is straightforward: a streamlined coast-to-coast operation will eliminate the friction of inter-railroad hand-offs—specifically the notorious delays that plague congested gateways like Chicago and New Orleans—driving efficiency and lowering costs.

However, BNSF Railway has taken the gloves off. In a detailed and forceful opposition filed last week, BNSF leadership argues that this mega-merger would “ruin a good thing,” dismantling the competitive balance that currently serves the network. Their objection is not merely rhetorical; it is backed by hard data on carload options. The current North American rail network relies on a web of collaboration among Class I carriers. BNSF argues that removing two major roads (UP and NS) from this mix effectively eliminates half of the existing long-haul options for carload shippers. This forces shippers to negotiate with an entity of “unprecedented” scale, inevitably leading to pricing pressure.

The stakes are highest for industrial commodities where intermodal substitution isn’t an option. Analysts project a combined UP-NS entity would control nearly half of all U.S. rail freight, including 45% of container traffic and 47% of automotive shipments. Most critically, the merger would capture 56% of the metals market. According to some this concentration creates a clear “captive shipper” risk. When the Surface Transportation Board (STB) sees a single entity controlling over half of a vital, non-substitutable market, the probability of strict conditions – such as mandated trackage rights or divestitures – skyrockets.

Regulatory Barometer: The STB’s High Threshold

BNSF contends that meeting the STB’s historically rigorous criteria—which requires the merger to demonstrably enhance competition—will be a “really tall hill to climb.” Compounding this challenge, customers are not widely advocating for the merger, weakening the applicants’ claim that the deal serves the public interest.

Simultaneously, the regulatory ground is shifting beneath the STB’s feet. A new report emphasizes that the Board must update its definition of market dominance to comply with the U.S. Supreme Court’s 2024 Loper Bright decision. The report argues that the STB must finally acknowledge modern economic realities, including geographic and intermodal competition. This legal pressure means the merger review itself could force a rewriting of regulatory standards, potentially making the environment more stringent for all future Class I transactions.

We are Watching the Class 1’s

While M&A dominates the headlines, carriers are quietly deploying private capital to win the battle for velocity and service predictability.

Canadian Pacific Kansas City (CPKC) has solidified its structural advantage in North-South trade with the completion of the second span of the Patrick J. Ottensmeyer International Railway Bridge at Laredo. As the only single-owner rail link between Laredo and Nuevo Laredo, this bridge is the jugular of US-Mexico rail trade.

The new 1,170-foot structure allows for simultaneous bi-directional movement, effectively doubling capacity and eliminating wait times that previously plagued the single track. For shippers in the automotive and manufacturing sectors embracing nearshoring, this physical “moat” de-risks their supply chain. Coupled with 13 new tentative labor agreements ensuring workforce stability, CPKC is positioning itself as the indispensable partner for cross-border logistics.

The Norfolk Southern (NS) is aggressively modernizing its terminals to combat “dwell time.” At hubs like Austell, GA, and Rossville, TN, the NS is transitioning from wheeled systems to stacked operations, boosting parking capacity by over 30 percent.

This isn’t just a physical upgrade; it’s a software play! New Stack Management technology now prevents containers from being “buried,” while a new Appointment System allows drayage providers to schedule profitable dual missions. By reducing friction for drivers, the NS is selling predictability—a high-value currency in a volatile logistics market.

We are Watching Railcar Car Manufacturing

Despite carrier executives forecasting an “anemic” macro environment for 2026, specific pockets of demand are strong. FreightCar America (RAIL), with its portfolio of specialized hoppers and gondolas, maintains a “Moderate Buy” rating, reflecting the steady need for agricultural and construction equipment. Conversely, The Greenbrier Companies (GBX) faces a “Reduce” consensus, as exposure to the slowing intermodal sector and general freight weighs on sentiment.

While the new proposed pipeline project project in Alberta (1 million barrels per day) coupled with Enbridge’s and Transmountain debottlenecking projects (550,000 barrels per day) casts a long shadow over the crude tank car market, the Natural Gas Liquids (NGL) sector remains a bright spot. Midstream operator AltaGas hit record LPG exports of 133,100 b/d in Q3 and is expanding its Ridley Island facility. These projects, which rely heavily on rail to reach the Pacific coast, confirm that the business case for specialized pressurized tank cars remains robust, independent of the volatility in crude oil logistics.

We Are Watching Key Economic Indicators

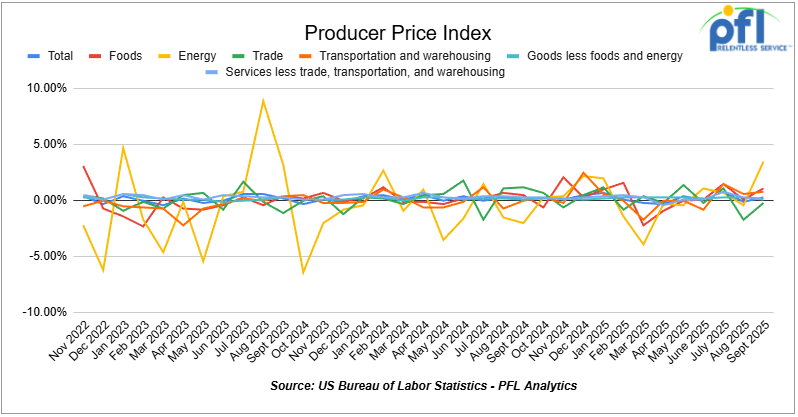

Producer Price Index

In September 2025, the Producer Price Index (PPI) for final demand rose 0.3% month over month, reversing the 0.1% decline in August, and continues to reflect moderate upstream inflation pressures. Core PPI (final demand less foods, energy, and trade services) increased 0.1% month over month, slowing from August’s 0.3% gain. The monthly increase was driven primarily by goods, which climbed 0.9%, led by strong gains in foods (+1.1%) and energy (+3.5%). Goods less food and energy were up 0.2%. Services were flat (0.0%) overall. Within services, trade margins fell 0.2%, transportation and warehousing rose 0.8%, and services excluding trade, transportation, and warehousing edged up 0.1%.

In September 2025, the CPI increased 0.3% month over month, easing from the 0.4% gain in August, and was up 3.0% year over year, a slight pickup from 2.9% the prior month. Core CPI (all items less food and energy) rose 0.2% month over month, down from August’s 0.3% increase, and was up 3.0% year over year. Shelter remained the largest contributor, rising 0.4% for the second straight month. Food prices rose 0.4% (food at home +0.5%, food away from home +0.2%). Energy increased 0.8%, including a 2.3% rise in gasoline.

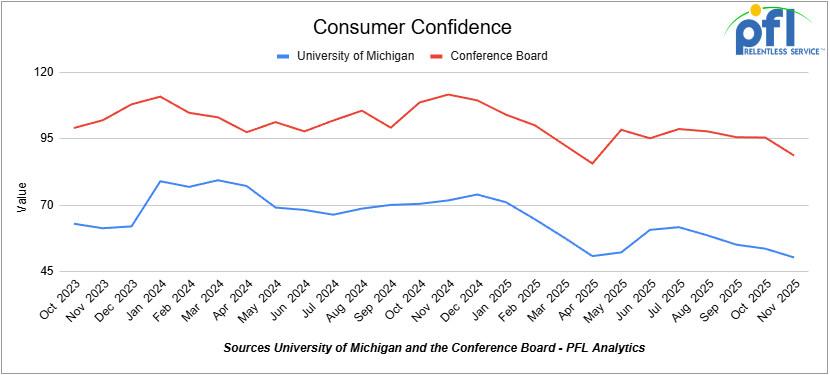

Consumer Confidence

The Index of Consumer Sentiment from the University of Michigan decreased from 53.6 in October to 50.3 in November.

The Conference Board Consumer Confidence Index decreased from 95.5 in October to 88.7 in November.

Lease Bids

- 30-50, 6000cf Steel Hopper located off of CSX or NS in East. For use in petcoke service. Period: 5 Years.

- 10, 2500CF Open Top Hopper located off of UP or BN in Texas. For use in aggregate service. Period: 5 years. Need Rapid Discharge Doors.

- 10, 25.5K Any Type Tank located off of CSX in Florida. For use in UCO service. Period: 2 Years.

- 50, 23.5-25.5 DOT111 Tank located off of Any Class 1 in USA. For use in Asphalt service. Period: 5 years.

- 100, 21.9K 117J Tank located off of All Class 1s in Midwest. For use in CO2 service. Period: 6 months.

- 30-50, 30K 117J Tank located off of NS or CSX in Northeast. For use in C5 service. Period: 1 year.

Sales Bids

- 28, 3400CF Covered Hopper located off of UP BN in Texas. For use in Cement service.Cement Gates needed..

- 20, 17K Tank DOT111 located off of various class 1s in various locations. For use in corn syrup service.

- 120, Various Gondola Open-Top Aluminum Rotary located off of various class 1s in various locations. For use in Sulphur service.Built 2004 or later.

Lease Offers

- 60, 4750 Covered Hoppers located off of UP or BN in Eads, CO. Last used in Grain. Cars are currently clean. UP to 5 Years, 3 Hopper, Gravity Gate, Trough Hatches.

- 100, 6250 Covered Hoppers located off of UP in US. Last used in DDG. 1 Year term. Dirty to Dirty. Free move on UP..

- 25, 19.6K DOT111 Tanks located off of UP in US. Last used in Molases.

- 50, 20K DOT111 Tanks located off of UP or BN in Wichita Falls, TX. Last used in HCL.

- 50, 30K 117R Tanks located off of CSX, NS, or CN in Detroit. Last used in Diesel. Multiyear.

- 50, 20K 117J Tanks located off of All Class 1s in Multiple Locations. Last used in Styrene. Cars are currently moving.

- 29, 25.5K 117J Tanks located off of BN or UP in Texas. Cars are currently clean.

- 40, 30K 117J Tanks located off of BNSF or UP in Houston. Cars are currently clean.

- 50, 5380 Covered Hoppers located off of BNSF or UP in Houston. Cars are currently clean. Available until Feburary.

- 21, 6351 Covered Hoppers located off of CN in Wisconsin. Last used in DDG. Available until February 2027.

- 29, 6500 Covered Hoppers located off of CN in Wisconsin. Last used in DDG. Available until February 2027.

- 100, 30K CPC1232 Tanks located off of UP or BN in Texas. Last used in Diesel.

- 100, 30K DOT117J Tanks located off of UP or BN in Texas. Last used in Gasoline.

- 100, 29K DOT117J Tanks located off of UP or BN in Texas. Last used in Gasoline. Coiled and Insulated.

- 36, 6351 Covered Hopper located off of CN in Wisconsin. Last used in Grain. through 2/27.

- 29, 6580 Covered Hopper located off of CN in Wisconsin. Last used in Grain. through 2/26.

- 18, 6580 Covered Hopper located off of CN in Wisconsin. Last used in Grain. through 2/27.

- 9, 5400 Covered Hopper located off of CN in Wisconsin. Last used in Grain. through 2/27.

Sales Offers

- 21, 50′ Boxcar Plate Cs located off of various class 1s in NM. End of Life.

- 3, 50′ Boxcar Plate Cs located off of various class 1s in multiple locations. End of Life.

- 27, 50′ Boxcar Plate Cs located off of various class 1s in PQ. End of Life.

- 100, 3250 Covered Hoppers located off of various class 1s in multiple locations. Sand Cars.

- 5, 2740 Mill Gondolas located off of various class 1s in NC. End of Life.

- 1, 2260 Mill Gondolas located off of various class 1s in AL. End of Life.

- 30, 2740 Mill Gondolas located off of various class 1s in multiple locations. End of Life.

- 21, 2740 Mill Gondolas located off of various class 1s in WA. End of Life.

- 9, 4750 Covered Hoppers located off of various class 1s in multiple locations. End of Life.

- 5, 4750 Covered Hoppers located off of various class 1s in multiple locations. End of Life.

- 50, 31.8K Tank CPC 1232s located off of UP or BN in TX. Requal Due in 2025.

- 100, 4600CF Open Top Hoppers located off of BN or CSX in Southeast.

Call PFL today to discuss your needs and our availability and market reach. Whether you are looking to lease cars, lease out cars, buy cars, or sell cars call PFL today at 239-390-2885

Live Railcar Markets

| CAT | Type | Capacity | GRL | QTY | LOC | Class | Prev. Use | Offer | Note |

|---|

PFL will be at the Following Conferences

- Where: La Quinta, CA

- Attending: David Cohen (954-729-4774)

- Conference Website

- Where: Hyatt Regency Dallas in Dallas, TX

- Attending:Curtis Chandler (239.405.3365), David Cohen (954-729-4774), Brian Baker (239.297.4519), Cyndi Popov(403) 402-5043

- Conference Website