“Instead of looking at our challenges and limitations as something negative or bad, we can begin to look at them as blessings, magnificent gifts that can be used to ignite our imaginations and help us go further than we ever knew we could go.” – Amy Purdy

Due to the Government Shutdown, we are unable to report last week’s Jobs Update. We apologize for the inconvenience.

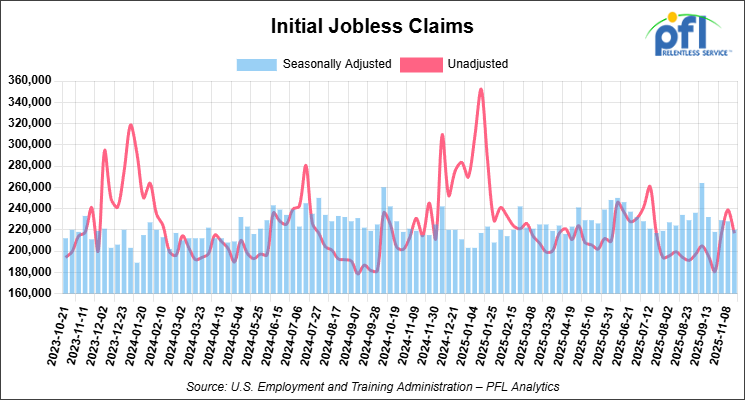

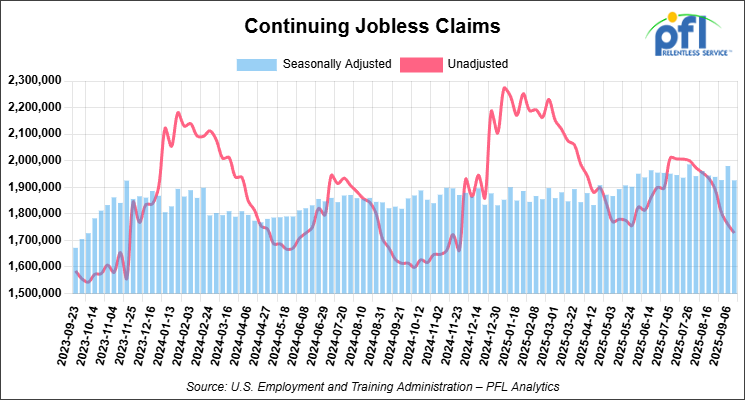

Jobs Update

- Initial jobless claims seasonally adjusted for the week ending November 15, 2025 came in at 220,000, versus the adjusted number of 228,000 people from the week prior, down 8,000 people week-over-week.

- Continuing jobless claims came in at 1,926,000, versus the adjusted number of 1,980,000 people from the week prior, down 54,000 week-over-week.

Stocks closed higher on Friday of last week, but lower week-over-week

The DOW closed higher on Friday of last week, up 493.15 points (1.08%), closing out the week at 46,245.41, but down -902.07 points week-over-week. The S&P 500 closed higher on Friday of last week, up 64.23 points (0.98%), and closed out the week at 6,602.99, but down -131.12 points week-over-week. The NASDAQ closed higher on Friday of last week, up 195.03 points (0.88%), and closed out the week at 22,273.08, also down -627.51 points week-over-week.

In overnight trading, DOW futures traded higher and are expected to open at 46,414 this morning, up 93 points from Friday’s close.

Crude oil closed lower on Friday of last week and lower week-over-week

West Texas Intermediate (WTI) crude closed down -94 cents per barrel (-1.6%), to close at $58.06 per barrel on Friday of last week, and down $2.00 per barrel week-over-week. Brent crude closed down -82 cents per barrel (-1.3%), to close at $62.56 per barrel, and down $1.83 per barrel week-over-week.

One Exchange WCS (Western Canadian Select) for January delivery settled on Friday of last week at US$12.40 below the WTI-CMA (West Texas Intermediate – Calendar Month Average). The implied value was US$46.21 per barrel.

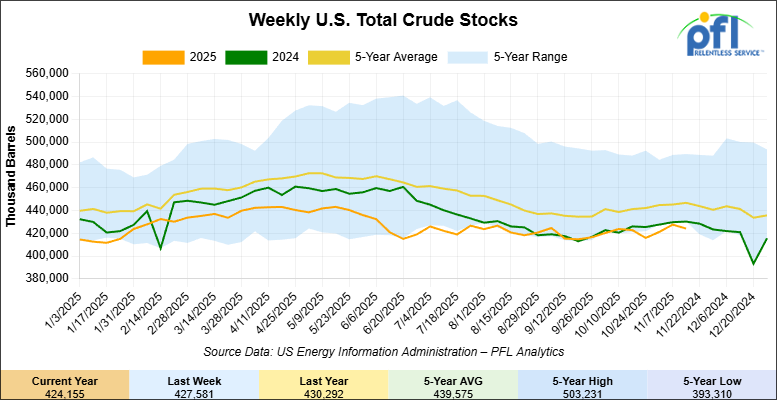

U.S. commercial crude oil inventories (excluding those in the Strategic Petroleum Reserve) decreased by 3.4 million barrels week-over-week. At 424.2 million barrels, U.S. crude oil inventories are 5% below the five-year average for this time of year.

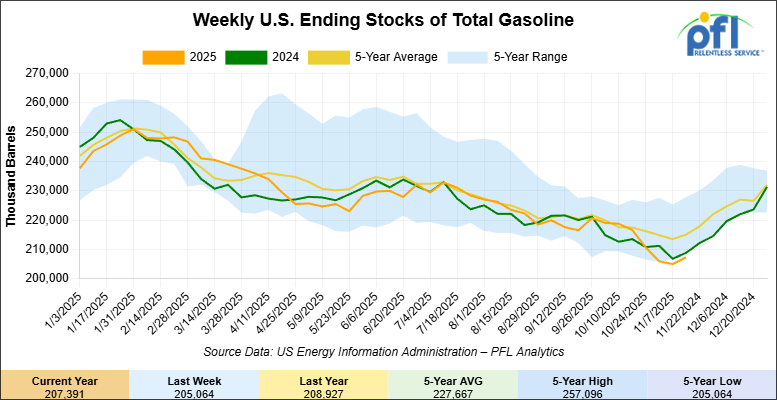

Total motor gasoline inventories increased by 2.3 million barrels week-over-week and are 3% below the five-year average for this time of year.

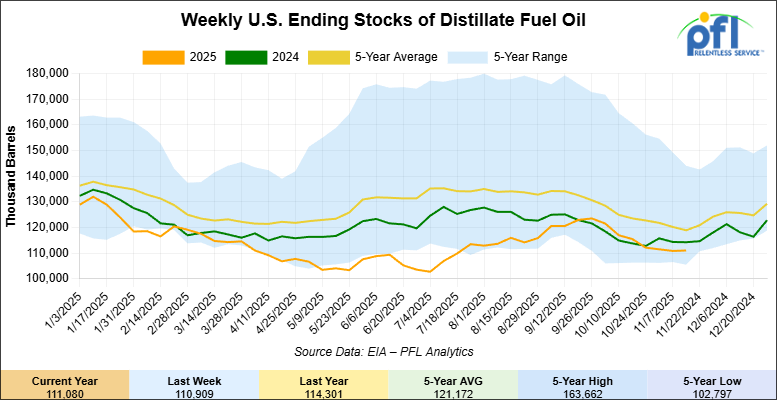

Distillate fuel inventories increased by 200,000 barrels week-over-week and are 7% below the five-year average for this time of year.

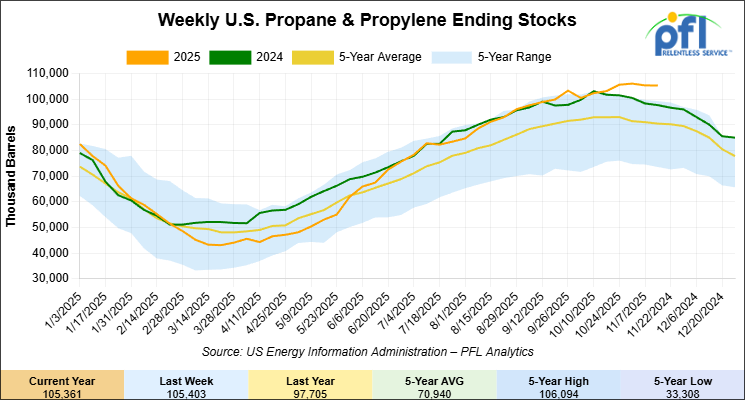

Propane/propylene inventories were unchanged week-over-week and are 16% above the five-year average for this time of year.

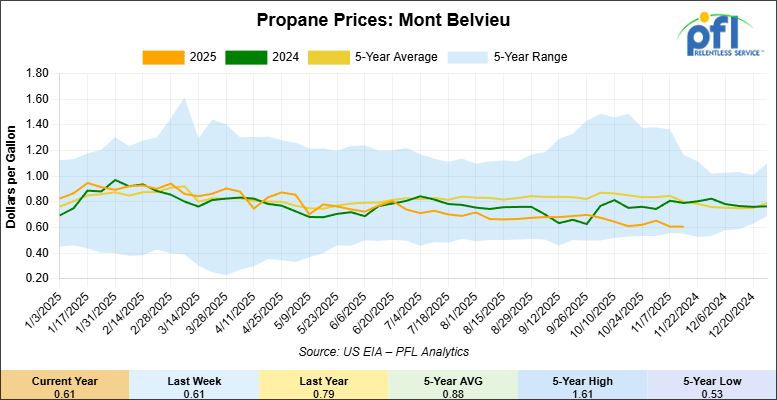

Propane prices closed at 61 cents per gallon on Friday of last week, flat week-over-week, but down by 18 cents per gallon year-over-year.

Overall, total commercial petroleum inventories decreased by 2.7 million barrels week-over-week during the week ending November 14, 2025.

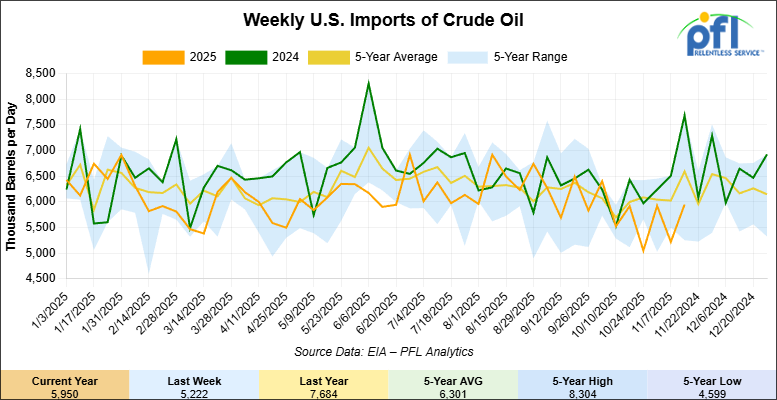

U.S. crude oil imports averaged 6 million barrels per day during the week ending November 14, 2025, an increase of 729,000 barrels per day week-over-week. Over the past four weeks, crude oil imports averaged about 5.5 million barrels per day, 16.1% less than the same four-week period last year. Total motor gasoline imports (including both finished gasoline and gasoline blending components) last week averaged 648,000 barrels per day, and distillate fuel imports averaged 88,000 barrels per day during the week ending November 7, 2025.

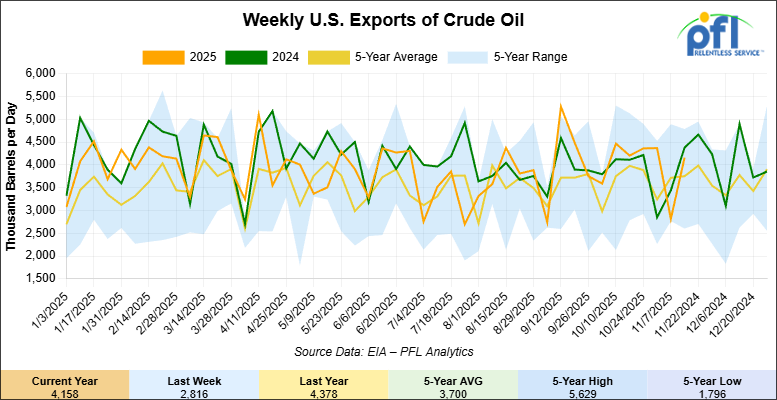

U.S. crude oil exports averaged 4.158 million barrels per day during the week ending November 14, 2025, an increase of 1.342 million barrels per day week-over-week. Over the past four weeks, crude oil exports averaged 3.926 million barrels per day.

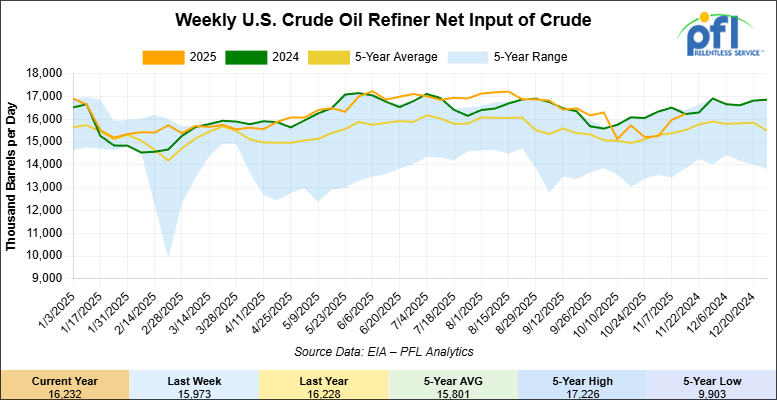

U.S. crude oil refinery inputs averaged 16.2 million barrels per day during the week ending November 14, 2025, which was 258,000 barrels per day more week-over-week.

WTI futures are poised to open at $58.04, down 2 cents from Friday’s close.

North American Rail Traffic

Week Ending November 19, 2025:

Total North American weekly rail volumes were down (-5.59%) in week 47, compared with the same week last year. Total Carloads for the week ending November 19, 2025 were 318,412, down (-3.08%) compared with the same week in 2024, while weekly Intermodal volume was 328,875, down (-7.90%) year over year. 7 of the AAR’s 11 major traffic categories posted year-over-year decreases. The largest decrease came from Forest Products (-19.89%), while the largest increase was Nonmetallic Minerals (+6.21%).

In the East, CSX’s total volumes were down (-4.41%), with the largest decrease coming from Metallic Ores and Metals (-18.68%), while the largest increase came from Other (+6.72%). NS’s total volumes were down (-5.83%), with the largest increase coming from Petroleum & Petroleum Products (+17.28%), while the largest decrease came from Grain (-12.61%).

In the West, BNSF’s total volumes were down (-5.88%), with the largest increase coming from Grain (+17.17%), while the largest decrease came from Motor Vehicles and Parts (-21.86%). UP’s total volumes were down (-4.17%), with the largest increase coming from Nonmetallic Minerals (+20.48%), while the largest decrease came from Intermodal Units (-12.59%).

In Canada, CN’s total volumes were down (-1.07%), with the largest increase coming from Intermodal Units (+65.25%), while the largest decrease came from Metallic Ores and Metals (-19.80%). CPKCS’s total volumes were down (-19.63%), with the largest increase coming from Coal (+31.75%), while the largest decrease came from Forest Products (-69.57%).

Source Data: AAR – PFL Analytics

North American Rig Count Summary

Rig Count

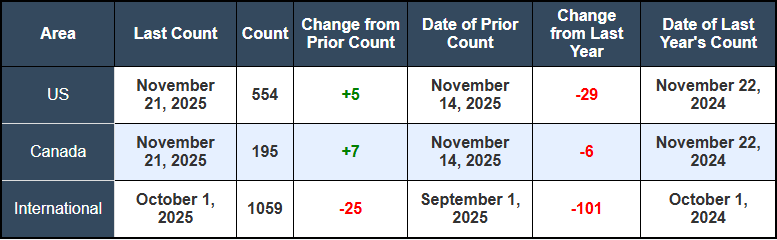

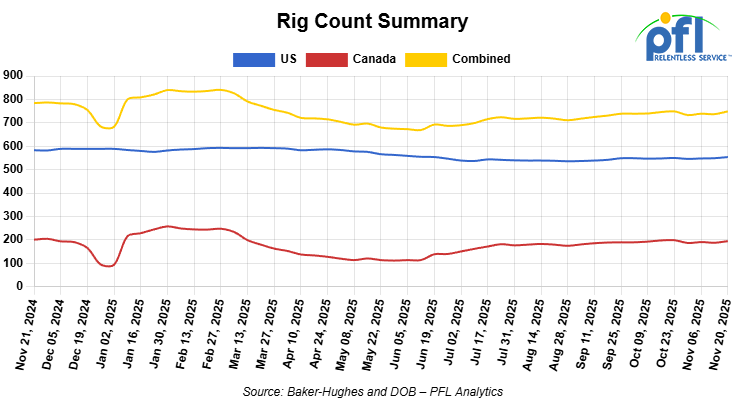

North American rig count was up by +12 rigs week-over-week. The U.S. rig count was up by +5 rigs week-over-week, but down by -29 rigs year-over-year. The U.S. currently has 554 active rigs. Canada’s rig count was up by +7 rigs week-over-week, but down by -6 rigs year-over-year. Canada currently has 195 active rigs. Overall, year-over-year we are down by -35 rigs collectively.

We are watching a few things out there for you:

We are watching Petroleum Carloads

The four-week rolling average of petroleum carloads carried on the six largest North American railroads rose to 29,584 from 29,313 which was an increase of +271 rail cars week-over-week. Canadian volumes were lower. CPKC’s shipments were lower by -4.0% week-over-week, CN’s volumes were lower by -12.0% week-over-week. U.S. shipments were mostly lower. The BNSF had the largest percentage decrease and was down by -7.0%.The UP was the sole gainer and was up by +5.0%.

North American petroleum carloads hit a 9-month high last week, but the geographic and commodity breakdown reveals a critical divergence: U.S. railroads are gaining share while Canadian crude-by-rail is being priced out of long-haul arbitrage economics. Union Pacific led the rallies with weekly petroleum carloads up 5%, leveraging strong U.S. domestic refinery demand into the Gulf coast region supported by favorable crack spreads. CSX held steady and Norfolk Southern was flat.

Canada’s two Class I railroads moved sharply lower. CPKC’s weekly petroleum shipments fell 4% and Canadian National’s dropped 12%—the latter’s sharpest weekly decline in months. The culprit: Western Canadian Select widened its discount to December NYMEX by 65¢/barrel in a single week to $12.40 per barrel under the benchmark. This compression of the WCS-to-Cushing arbitrage window essentially priced out long haul crude by rail to the U.S. Gulf for Canadian heavy grades. When WCS trades at steep discounts to deliverable crude at U.S. hubs, the per-barrel transportation cost—whether by rail or pipeline—becomes the deciding factor (right now pipe is cheaper).

Alberta’s crude production surged to 4.2 million barrels per day following second-quarter maintenance turnarounds, tightening capacity on Enbridge’s 3.1 million barrel per day Mainline and triggering apportionment for both heavy and light crudes. Enbridge rejected 7% of December heavy crude nominations and 11% of light crude nominations at Kerrobert, Saskatchewan, for December flow. With production high and fewer volumes moving offshore via Trans Mountain (which is struggling with weaker Asian demand), shippers are competing intensely for whatever pipeline space remains. That competition price-checks crude-by-rail out of the equation.

Interestingly, U.S. Bakken crude-by-rail to Philadelphia and New York remains economically viable at $10.50/barrel and $10.55/barrel respectively, reflecting strong demand from U.S. Gulf Coast refineries that are increasing runs as fall turnarounds wind down. However, Canadian heavy crude by rail to the U.S. Gulf Coast stands at $15.31/barrel—a spread differential that now makes even premium U.S. locations uncompetitive for Canadian grades when pipeline diluent requirements (which rise in winter) and WCS discounts are factored in.

For Canadian tank car operators and lessors, this is the inverse problem: the North American fleet sits at 250,037 cars (down 0.5% from four weeks prior), yet Canadian crude by rail demand is dwindling. This creates utilization pressure on a per-car basis even as total North American volumes remain strong. It also reinforces the structural story that emerged weeks ago and we have been reporting on: pipeline optimization (Mainline Optimization Phase 1 adding 150,000 b/d by October 2027, plus TransMountain expansion) will continue to crowd out marginal crude by rail economics, particularly for Canadian heavy grades in winter months when diluent requirements balloon. The tank car fleet may hold steady in headcount, but utilization rates—and therefore lease prices—face downward pressure as pipeline capacity growth outpaces crude volumes needing rail solutions.

We are Watching Left Wing Carney Spend Money

The Canadian government announced last Thursday a CAD $6 billion investment over seven years in trade and transportation infrastructure, with significant implications for rail operators moving export cargo. Transport Minister Steven MacKinnon and International Trade Minister Maninder Sidhu unveiled two funds: a CAD $5 billion Trade Diversification Corridors Fund to strengthen ports, rail and roads, and a $1 billion Arctic Infrastructure Fund for dual-use civilian and defense transportation projects. The initiatives are designed to help Canada double non-U.S. exports over the next decade and could generate $300 billion in additional exports.

The announcement comes as Canada and Mexico are strengthening trade ties ahead of the USMCA review scheduled for July 2026, with both countries working to diversify away from U.S. dependence amid ongoing tariff uncertainty. Canadian Pacific Kansas City CEO Keith Creel has been promoting the railroad’s role as a “land bridge” between Canada and Mexico that bypasses U.S. tariffs, noting that “trade between the nations has been modest” but that “Canada and Mexico see each other in a way they’ve never seen each other before.” CPKC’s 32,000-kilometre network across all three countries was specifically designed to benefit from North American integration, though Trump’s tariff threats have accelerated interest in direct Canada-Mexico routing.

The Trade Diversification Corridors Fund will be delivered by Transport Canada in partnership with the Canada Infrastructure Bank, which saw its statutory appropriation limit raised from $35 billion to $45 billion in Budget 2025. Minister MacKinnon stated the investments will “create skilled, well-paid jobs, strengthen regional economies, and help Canadian businesses get their goods to new markets.” For railcar operators, the infrastructure spending signals increased government support for export-oriented rail capacity, particularly for critical minerals, clean technologies, agri-food and manufactured goods moving to non-U.S. destinations.

The $1 billion Arctic Infrastructure Fund will support airports, seaports, all-season roads and potentially rail connections that strengthen Canadian sovereignty while opening new northern trade gateways. The combination of infrastructure investment and trade diversification strategy creates tailwinds for Class I railroads and short lines serving export corridors, though the benefits are years away given the seven-year funding timeline. The USMCA renegotiation and potential U.S. tariff escalation are creating urgency around Canada-Mexico trade corridors that CPKC is positioned to exploit. The $6 billion commitment signals government backing for export infrastructure, which is positive for rail, but the seven-year horizon means benefits don’t materialize until 2032.

We are Watching Trump and Coal

The Trump Administration’s effort to prop up coal demand collided last week with the industry’s inability to respond to even existing requirements, creating policy uncertainty for coal car operators. Energy Secretary Chris Wright issued his third consecutive 90-day emergency order on November 18 to keep Michigan’s J.H. Campbell coal-fired power plant running, forcing the facility to remain open through mid-February despite its planned May 2025 closure. The 60-year-old plant was scheduled for early decommissioning by owner Consumers Energy, which had projected the closure would save regional customers $600 million through 2040 by eliminating an expensive, inefficient facility.

The emergency orders have cost electricity ratepayers in 11 Midwestern states over $80 million through September—more than $600,000 per day—with Consumers Energy seeking to recover mounting costs from customers. Michigan Attorney General and environmental groups are suing to overturn the orders, arguing no emergency exists and that the administration is illegally forcing consumers to bail out uneconomic coal plants. Wright has stated bluntly that “this administration’s policy is going to be to stop the closure of coal plants,” and has threatened to use emergency powers to save additional facilities.

Meanwhile, the Senate voted 51-43 last Thursday to reverse the Biden administration’s ban on new coal leasing in Wyoming’s Powder River Basin, which supplies roughly 40% of U.S. coal. The bill, H.J. Res. 130, heads to President Trump for signature and would restore access to an estimated 48 billion short tons of federal coal reserves. However, the legislation arrives amid severe market headwinds: Powder River Basin production has fallen from 400 million tons to 200 million tons over the past decade, and recent federal coal auctions have drawn either no bids or bids too low for the government to accept.

The contradiction is stark. October 2025 recorded the lowest coal carloads for any October since Association of American Railroads records began in 1988, according to AAR data. U.S. coal producers are struggling to meet even current demand due to labor shortages, aging equipment and geological challenges, with coal mining employment falling to 40,300 in August—the lowest level in over three years. Alliance Resource Partners further reduced its 2025 sales outlook in October to 32.5-33.3 million short tons, down 500,000 tons from July guidance, due primarily to mining setbacks and elevated production costs at Appalachian operations including the Mettiki mine in West Virginia.

Alliance CEO Joe Craft has argued that data center electricity demand will drive 4-6% annual growth in PJM, reducing gas-to-coal competition. Yet even if that thesis proves correct, the industry lacks the workforce, equipment and capital to respond—a structural problem that Senate votes and emergency orders cannot solve. Forced plant operations provide temporary utilization support, but the underlying trajectory remains negative: structural decline in production, record-low carloads, and producers already sold out for the rest of 2025 with no ability to ramp output. The emergency orders are legally questionable bailouts unlikely to survive sustained court challenges, while restored Powder River Basin leasing faces a market with no bidders for federal coal at acceptable prices.

We are Watching CP and CN

Canadian National and Canadian Pacific Kansas City are actively positioning themselves to capture regulatory concessions from the proposed Union Pacific-Norfolk Southern merger ahead of the STB application expected in early December. Speaking at the Scotiabank investor conference on November 18, CN CEO Tracy Robinson told analysts that approval will require “pretty serious concessions,” signaling that Canadian Class I railroads see strategic opportunities in whatever remedies the Surface Transportation Board imposes. The merger’s regulatory calculus has tightened considerably last week, as the STB is now operating under 2001 rules that require merging Class I railroads to affirmatively demonstrate that their combination enhances competition, not merely preserves it – a higher bar than previous merger reviews.

Robinson said concessions could include “opportunities for us around being able to drive deeper into the U.S. market,” though she declined to specify before UP files its application. CPKC’s CFO Nadeem Velani similarly flagged that “there are going to be conditions placed if this deal goes through, there’s no doubt, whether it’s trackage rights or interchange opportunities or divestitures.” More specifically, Velani signaled that CPKC would have capital available to acquire divested segments – a clear message to the STB that even forced divestitures could be absorbed by competing carriers.

The regulatory environment has darkened further for UP-NS. On November 20, FERC voted unanimously to propose new pipeline tariff rules, restricting the ability of major crude pipelines to raise rates starting July 2026. FERC’s new index formula will use the annual average PPI-FG minus 1.42% (versus the old formula of PPI-FG minus 0.21%), effectively capping pipeline rate increases at roughly 2% annually versus the 14% increases that formulas yielded in 2023. While this primarily affects crude pipelines, the broader regulatory environment signals that 2026 will bring tighter controls on transportation pricing across modes – rail included.

A bipartisan coalition of 54 Republican state lawmakers warned the STB on November 17th that the UP-NS merger could “negatively affect America’s ability to compete with China“ and could give the combined railroad “dominant market share in critical commodity sectors” including chemicals, metals, agricultural products, and scrap metal. The coalition directly contradicts Trump’s public support for the deal, demonstrating genuine policy discord even within his party. Nine Republican state attorneys general also separately filed warnings about market concentration and reduced shippers’ competitive options.

We are Watching the BNSF and the CSX

BNSF and CSX launched expanded intermodal service on November 17th linking Los Angeles with Ohio Valley and Northeast destinations, cutting transit times by 22 to 52 hours depending on destination. The new five-day-per-week schedules from BNSF’s Hobart terminal reach CSX destinations including Northwest Ohio (89 hours), Chambersburg, Pennsylvania (123 hours, improved by 28 hours), Columbus, Louisville, Philadelphia, South Kearny, Syracuse and Springfield. The partnership, which began in August with Southwest-Southeast lanes, has already converted over-the-highway loads to intermodal and captured business previously handled by Norfolk Southern, according to BNSF customer advisories.

The expansion represents a direct competitive response to the proposed Union Pacific-Norfolk Southern merger announced in July. Norfolk Southern executives acknowledged on their October earnings call that they expected to lose market share as rival railroads create new services in reaction to the merger proposal. Intermodal analyst Larry Gross noted the merger has already reversed a 20-year trend of declining interline intermodal moves, as railroads historically avoided pre-blocking trains for interchange due to cost concerns without easily traced revenue offsets.

The new schedules offer customers “immediate value by increasing speed, flexibility and optionality while delivering integrated service for freight moving across the U.S.,” according to BNSF. Industry observers expect further route expansions as BNSF and CSX leverage their combined network to compete for transcontinental business against the proposed UP-NS system. This is exactly the type of network optimization the Class I industry has historically avoided due to interchange costs, but the merger threat has forced competitors to collaborate.

We are Watching the Brotherhood

The Brotherhood of Locomotive Engineers and Trainmen reached a tentative five-year national agreement with freight railroads represented by the National Carriers’ Conference Committee on November 2, covering 11,000 BLET members at BNSF, Norfolk Southern, Canadian National, and some smaller railroads. The agreement follows the industry-wide pattern established by other unions: 18.8% compounded wage increases over five years, a one-time $500 payment, and health care improvements with no increase in employee contributions (premiums remain at $308/month versus national average of $500+).

The NCCC stated that upon ratification—results expected in December—nearly 95% of union-represented freight rail employees at railroads participating in national handling will be covered by collective bargaining agreements following the industry pattern. BLET President Mark Wallace said the union “attempted to move beyond the pattern” but railroads were unwilling without concessions to work rules and other protections. CPKC separately announced tentative five-year agreements with BLET covering approximately 300 locomotive engineers on its Soo Line property in Illinois, Indiana, Minnesota, North Dakota and Wisconsin.

The 2025 bargaining round has been characterized by “historic collaboration” between freight rail carriers and unions, with the NCCC chairman calling it “one of the most productive in modern freight rail history.” The settlements provide wage certainty and avoid the potential for service disruptions that characterized the contentious 2022 negotiations. With BLET ratification expected by year-end, railroads can move into 2026 with stable labor costs and headcount certainty—important for capital planning and operational forecasting.

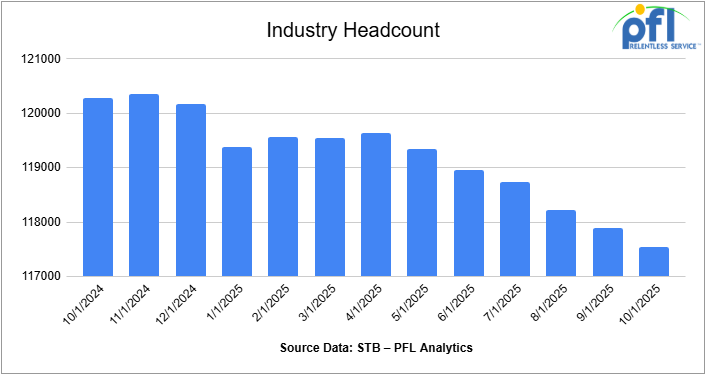

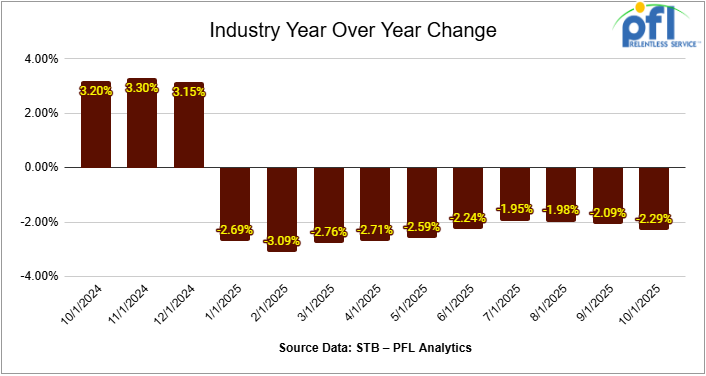

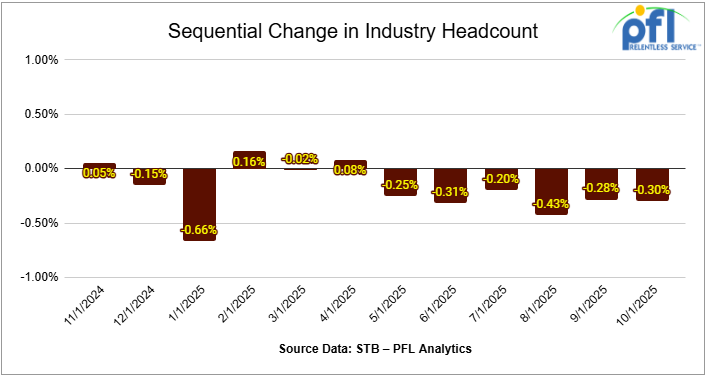

We are Watching Class 1 Head Count

Class I railroads employed 117,540 workers in the United States in October 2025, a -0.30% decrease from September 2025’s count of 117,888 and a -2.29% year-over-year decrease from October 2024’s total of 120,290, according to Surface Transportation Board data.

None of the six employment categories posted month-over-month increases between September and October. All categories declined over the month.

The categories that posted month-over-month decreases were Executives, officials, and staff assistants, down -0.16% to 8,146 workers; Professional and administrative, down -0.33% to 9,001 workers; Maintenance of way and structures, down -0.25% to 29,012 workers; Maintenance of equipment and stores, down –0.36% to 16,444 workers; Transportation (other than train and engine), down -0.86% to 4,847 workers; and Transportation (train and engine), down -0.26% to 50,090 workers.

Year over year, two categories posted an employment gain, which were Executives, officials, and staff assistants up 3.68%, and Maintenance of way and structures up 0.35%.

Categories that registered year-over-year decreases in October were Professional and administrative down -7.05%; Maintenance of equipment and stores down -4.13%; Transportation (other than train and engine) down -3.98%; and Transportation (train and engine) down -3.00%.

We are watching Key Economic Indicators

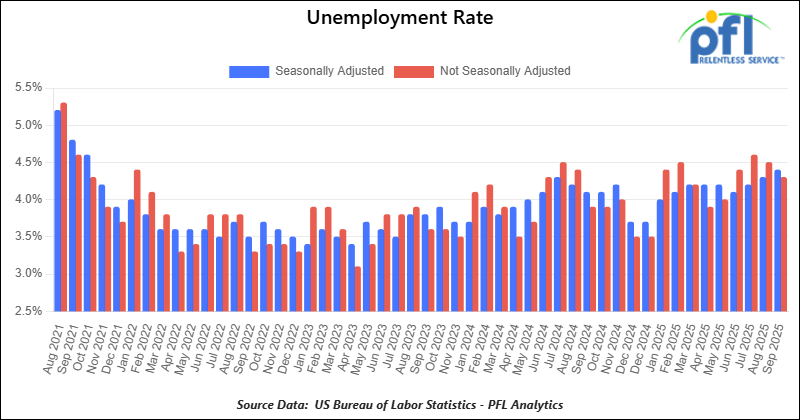

U.S Unemployment

On November 20 2025, the Bureau of Labor Statistics reported that a preliminary 119,000 net new jobs were created in September 2025. Figures for prior months were revised downward — August was revised to a loss of 4,000 jobs and July to 72,000 new jobs.

According to the BLS, so far this year net new job gains total approximately 598,000. The official unemployment rate was 4.4% in September, up 0.1 percentage point from August.

Lease Bids

- 30-50, 6000cf Steel Hopper located off of CSX or NS in East. For use in petcoke service. Period: 5 Years.

- 10, 2500CF Open Top Hopper located off of UP or BN in Texas. For use in aggregate service. Period: 5 years. Need Rapid Discharge Doors.

- 10, 25.5K Any Type Tank located off of CSX in Florida. For use in UCO service. Period: 2 Years.

- 50, 23.5-25.5 DOT111 Tank located off of Any Class 1 in USA. For use in Asphalt service. Period: 5 years.

- 100, 21.9K 117J Tank located off of All Class 1s in Midwest. For use in CO2 service. Period: 6 months.

- 100, 33K Pressure Tank located off of CN or CP in Canada. For use in Propane service. Period: Winter.

- 30-50, 30K 117J Tank located off of NS or CSX in Northeast. For use in C5 service. Period: 1 year.

Sales Bids

- 28, 3400CF Covered Hopper located off of UP BN in Texas. For use in Cement service.Cement Gates needed..

- 20, 17K Tank DOT111 located off of various class 1s in various locations. For use in corn syrup service.

- 120, Various Gondola Open-Top Aluminum Rotary located off of various class 1s in various locations. For use in Sulphur service.Built 2004 or later.

Lease Offers

- 60, 4750 Covered Hoppers located off of UP or BN in Eads, CO. Last used in Grain. Cars are currently clean. UP to 5 Years, 3 Hopper, Gravity Gate, Trough Hatches.

- 100, 6250 Covered Hoppers located off of UP in US. Last used in DDG. 1 Year term. Dirty to Dirty. Free move on UP..

- 25, 19.6K DOT111 Tanks located off of UP in US. Last used in Molases.

- 50, 20K DOT111 Tanks located off of UP or BN in Wichita Falls, TX. Last used in HCL.

- 50, 30K 117R Tanks located off of CSX, NS, or CN in Detroit. Last used in Diesel. Multiyear.

- 50, 20K 117J Tanks located off of All Class 1s in Multiple Locations. Last used in Styrene. Cars are currently moving.

- 22, 25.5K DOT111 Tanks located off of UP in Texas. Last used in Asphalt.

- 29, 25.5K 117J Tanks located off of BN or UP in Texas. Cars are currently clean.

- 40, 30K 117J Tanks located off of BNSF or UP in Houston. Cars are currently clean.

- 50, 5380 Covered Hoppers located off of BNSF or UP in Houston. Cars are currently clean. Available until Feburary.

- 21, 6351 Covered Hoppers located off of CN in Wisconsin. Last used in DDG. Available until February 2027.

- 29, 6500 Covered Hoppers located off of CN in Wisconsin. Last used in DDG. Available until February 2027.

- 100, 30K CPC1232 Tanks located off of UP or BN in Texas. Last used in Diesel.

- 100, 30K DOT117J Tanks located off of UP or BN in Texas. Last used in Gasoline.

- 100, 29K DOT117J Tanks located off of UP or BN in Texas. Last used in Gasoline. Coiled and Insulated.

- 36, 6351 Covered Hopper located off of CN in Wisconsin. Last used in Grain. through 2/27.

- 29, 6580 Covered Hopper located off of CN in Wisconsin. Last used in Grain. through 2/26.

- 18, 6580 Covered Hopper located off of CN in Wisconsin. Last used in Grain. through 2/27.

- 9, 5400 Covered Hopper located off of CN in Wisconsin. Last used in Grain. through 2/27.

Sales Offers

- 21, 50′ Boxcar Plate Cs located off of various class 1s in NM. End of Life.

- 3, 50′ Boxcar Plate Cs located off of various class 1s in multiple locations. End of Life.

- 27, 50′ Boxcar Plate Cs located off of various class 1s in PQ. End of Life.

- 100, 3250 Covered Hoppers located off of various class 1s in multiple locations. Sand Cars.

- 5, 2740 Mill Gondolas located off of various class 1s in NC. End of Life.

- 1, 2260 Mill Gondolas located off of various class 1s in AL. End of Life.

- 30, 2740 Mill Gondolas located off of various class 1s in multiple locations. End of Life.

- 21, 2740 Mill Gondolas located off of various class 1s in WA. End of Life.

- 9, 4750 Covered Hoppers located off of various class 1s in multiple locations. End of Life.

- 5, 4750 Covered Hoppers located off of various class 1s in multiple locations. End of Life.

- 50, 31.8K Tank CPC 1232s located off of UP or BN in TX. Requal Due in 2025.

- 100, 4600CF Open Top Hoppers located off of BN or CSX in Southeast.

Call PFL today to discuss your needs and our availability and market reach. Whether you are looking to lease cars, lease out cars, buy cars, or sell cars call PFL today at 239-390-2885

Live Railcar Markets

| CAT | Type | Capacity | GRL | QTY | LOC | Class | Prev. Use | Offer | Note |

|---|

PFL will be at the Following Conferences

- Where: La Quinta, CA

- Attending: David Cohen (954-729-4774)

- Conference Website

- Where: Hyatt Regency Dallas in Dallas, TX

- Attending:Curtis Chandler (239.405.3365), David Cohen (954-729-4774), Brian Baker (239.297.4519), Cyndi Popov(403) 402-5043

- Conference Website