“Defeat may serve as well as victory to shake the soul and let the glory out.” –Edwin Markham

Jobs Update

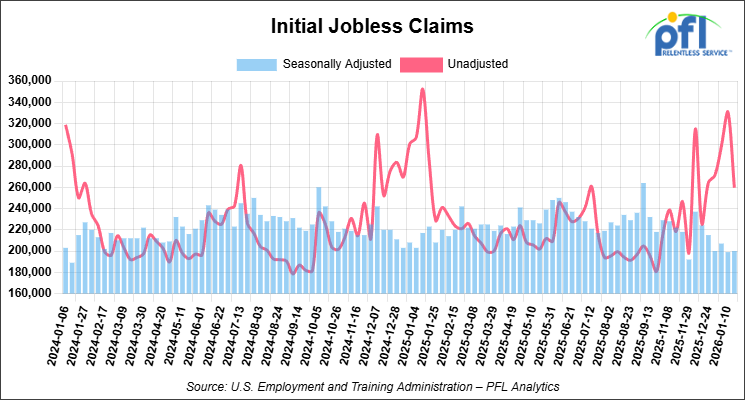

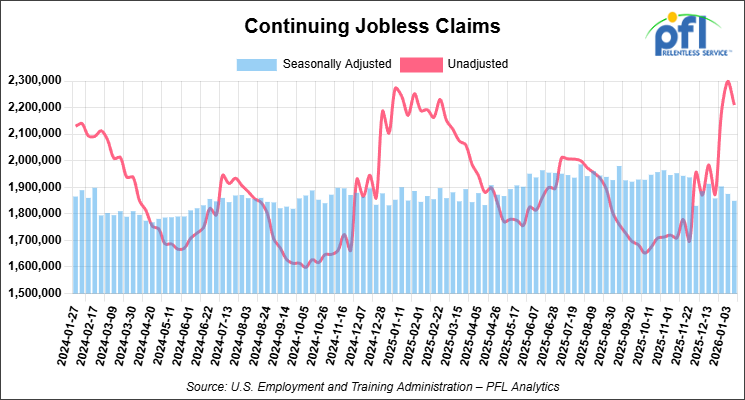

- Initial jobless claims seasonally adjusted for the week ending January 17, 2026 came in at 200,000, versus the adjusted number of 199,000 people from the week prior, up 1,000 people week over week.

- Continuing jobless claims came in at 1,849,000, versus the adjusted number of 1,875,000 people from the week prior, down 26,000 week-over-week.

Stocks closed mixed on Friday of last week and lower week-over-week

The DOW closed lower on Friday of last week, down -285.30 points (-0.58%), closing out the week at 49,098.71, down -260.62 points week-over-week. The S&P 500 closed higher on Friday of last week, up 2.26 points (0.03%), and closed out the week at 6,915.61, down -24.40 points week-over-week. The NASDAQ closed higher on Friday of last week, up 65.22 points (0.28%), and closed out the week at 23,501.24, down -14.15 points week-over-week.

In overnight trading, DOW futures traded lower and are expected to open at 49,244 this morning, down 19 points from Friday’s close.

In other market news, it was a crazy week last week. Gold and silver continued to surge as people are losing faith in the U.S. dollar it seems. Silver closed at $101.33 per ounce and Gold closed at $4,863.10 per ounce breaching $5,000 per ounce, at one point during the trading session on Friday of last week. Natural Gas surged closing at $5.275 per MMBU at Henry Hub on Friday of last week, as fear of the deep winter freeze and well shut-ins possibly weighed on market participants. If you need a mobile boiler call, PFL today we are here to help.

Crude oil closed higher on Friday of last week and higher week-over-week

West Texas Intermediate (WTI) crude closed up $1.71 per barrel (2.9%), to close at $61.07 on Friday of last week, and up $1.63 week-over-week. Brent crude closed up $1.82 per barrel (2.8%), to close at $65.88, and up $1.75 week-over-week.

One Exchange WCS (Western Canadian Select) for March delivery settled on Friday of last week at US$15.50 below the WTI-CMA (West Texas Intermediate – Calendar Month Average). The implied value was US$45.57 per barrel. Folks, Alberta is going to hit a wall real soon. Enbridge rejected 22% of heavy crude nominations for February delivery and Transmountain pipeline is almost 90% full. Canadian basis is taking a huge hit as Canadian barrels are now competing with imports from Venezuela barrels now trading at US$9.00 below the WTI-CMA (West Texas Intermediate – Calendar Month Average).

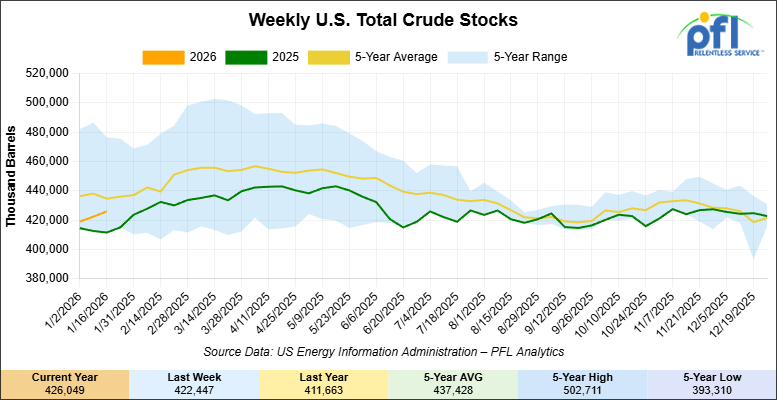

U.S. commercial crude oil inventories (excluding those in the Strategic Petroleum Reserve) increased by 3.6 million barrels week-over-week. At 426 million barrels, U.S. crude oil inventories are 2% below the five-year average for this time of year.

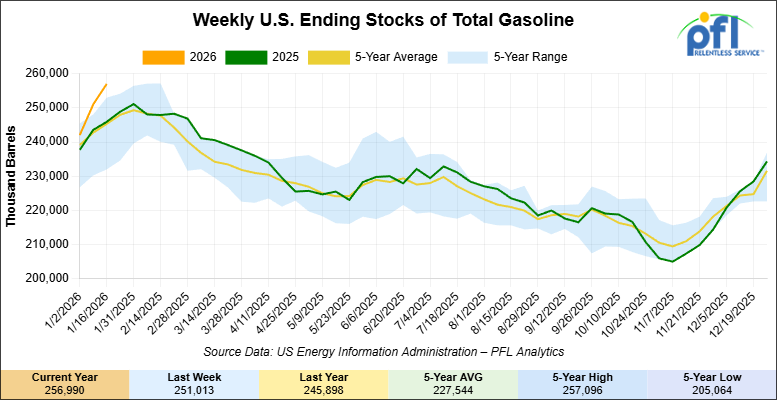

Total motor gasoline inventories increased by 6 million barrels week-over-week and are 5% above the five-year average for this time of year.

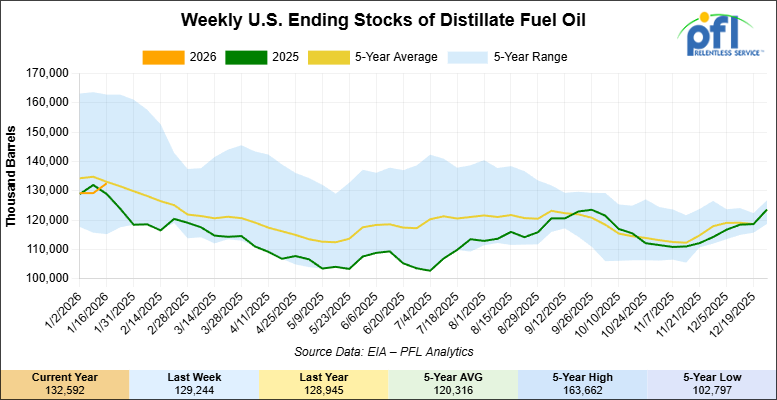

Distillate fuel inventories increased by 3.3 million barrels week-over-week and are 1% below the five-year average for this time of year.

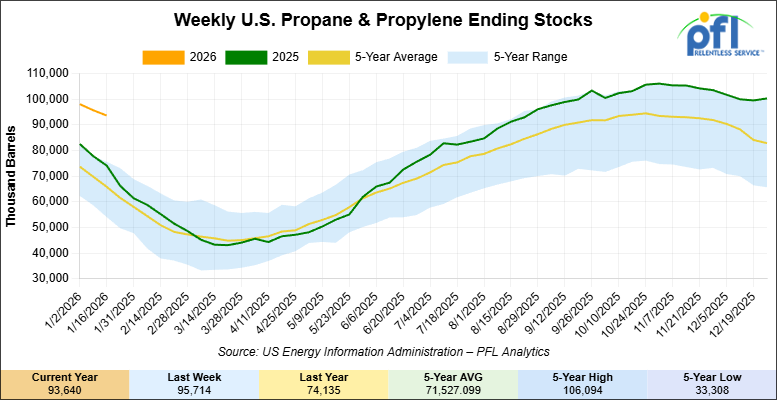

Propane/propylene inventories decreased 2.1 million barrels week-over-week and are 39% above the five-year average for this time of year.

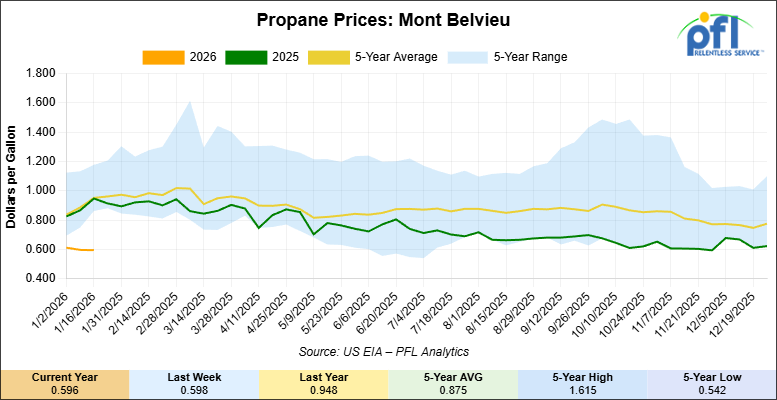

Propane prices closed at 59.6 cents per gallon on Friday of last week, down 0.2 cents per gallon week-over-week, and down 35.2 cents year-over-year.

Overall, total commercial petroleum inventories increased by 7.5 million barrels week-over-week, during the week ending January 16, 2026.

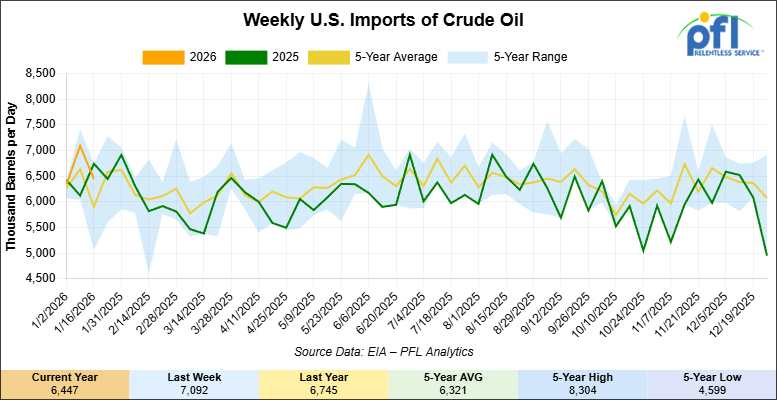

U.S. crude oil imports averaged 6.4 million barrels per day during the week ending January 16, 2026, a decrease of 645,000 barrels per day week-over-week. Over the past four weeks, crude oil imports averaged 6.2 million barrels per day, 5.3% less than the same four-week period last year. Total motor gasoline imports (including both finished gasoline and gasoline blending components) averaged 412,000 barrels per day, and distillate fuel imports averaged 215,000 barrels per day during the week ending January 16, 2026.

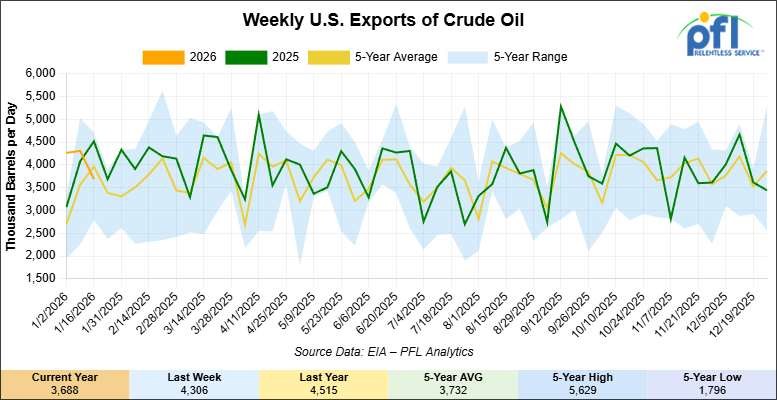

U.S. crude oil exports averaged 3.688 million barrels per day during the week ending January 16, 2026, a decrease of 618,000 barrels per day week-over-week. Over the past four weeks, crude oil exports averaged 3.924 million barrels per day.

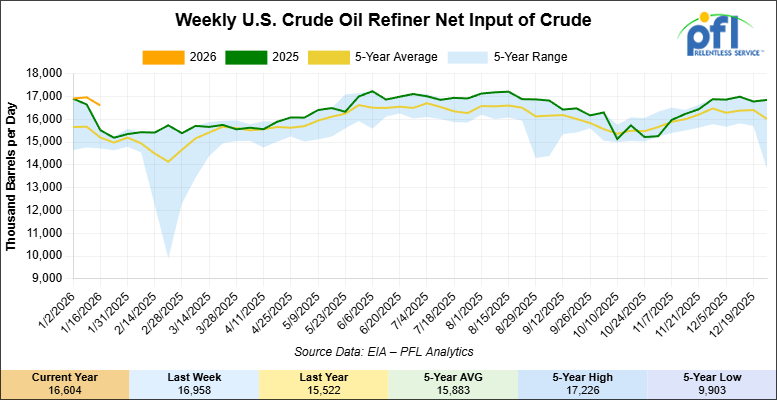

U.S. crude oil refinery inputs averaged 16.6 million barrels per day during the week ending January 16, 2026, which was 354,000 barrels per day less week-over-week.

WTI is poised to open at 61.22, up 16 cents per barrel from Friday’s close.

North American Rail Traffic

Week Ending January 21, 2026:

Total North American weekly rail volumes were down (-1.14%) in week 4, compared with the same week last year. Total Carloads for the week ending January 21, 2026 were 322,203, up (+1.31%) compared with the same week in 2024, while weekly Intermodal volume was 339,469, down (-3.37%) year over year. 8 of the AAR’s 11 major traffic categories posted year-over-year decreases. The largest decrease came from Forest Products (-22.62%), while the largest increase was Grain (+21.10%).

In the East, CSX’s total volumes were up (+1.25%), with the largest decrease coming from Forest Products (-12.07%), while the largest increase came from Grain (+17.17%). NS’s total volumes were up (+0.44%), with the largest increase coming from Nonmetallic Minerals (+17.12%), while the largest decrease came from Forest Products (-9.22%).

In the West, BNSF’s total volumes were up (+1.92%), with the largest increase coming from Grain (+26.20%), while the largest decrease came from Other (-27.91%). UP’s total volumes were down (-3.47%), with the largest increase coming from Grain (+20.05%), while the largest decrease came from Intermodal Units (-10.61%).

In Canada, CN’s total volumes were up (+2.47%), with the largest increase coming from Coal (+17.34%), while the largest decrease came from Motor Vehicles and Parts (-25.38%). CPKCS’s total volumes were down (-22.12%), with the largest increase coming from Grain (+28.00%), while the largest decrease came from Forest Products (-70.31%).

Source Data: AAR – PFL Analytics

North American Rig Count Summary

Rig Count

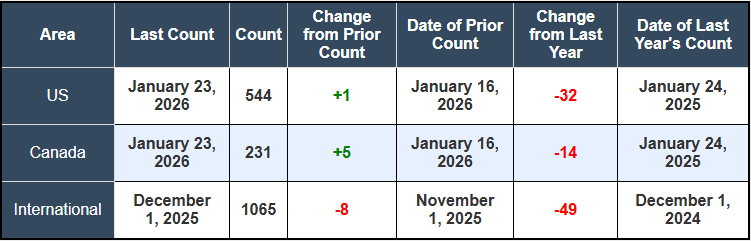

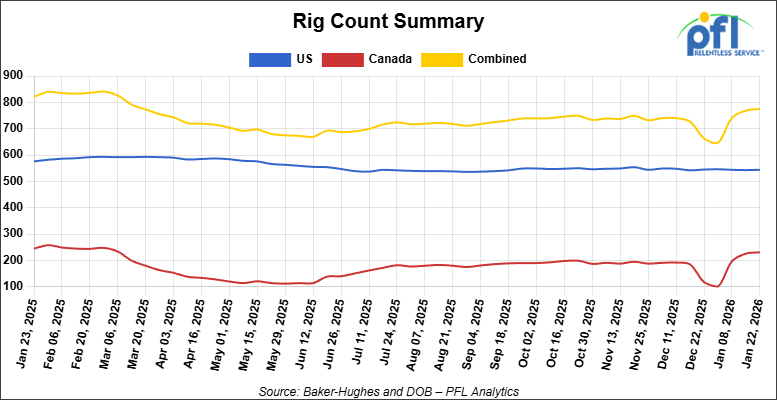

North American rig count was up by +6 rigs week-over-week. The U.S. rig count was up by +1 rig week-over-week, but down by -32 rigs year-over-year. The U.S. currently has 544 active rigs. Canada’s rig count was up by +5 rigs week-over-week, but down by -14 rigs year-over-year. Canada currently has 231 active rigs. Overall, year-over-year we are down by -46 rigs collectively.

We are watching a few things out there for you:

We are watching the Weather

Deadly winter storm set in over the weekend, halting rail operations across the country including a few PFL locations. Here is what we know:

Deadly cold: At least 11 people have died in the coldest temperatures of the winter. The brutal cold will linger into the week, with nearly 90 million people under Extreme Cold Watches or Warnings, raising fears for those without shelter or power for days.

• Crippling: More than 800,000 customers are still without power after damaging ice knocked it out. Here’s what to do if you’re without power.

•No travel, no school: Sunday was the worst day for flight cancellations since the pandemic. Over 19,000 flights were canceled during this storm. Schools in major cities have canceled classes or moved to remote learning for today.

• Snow: A staggering 15 states have seen snow pile up a foot or higher.

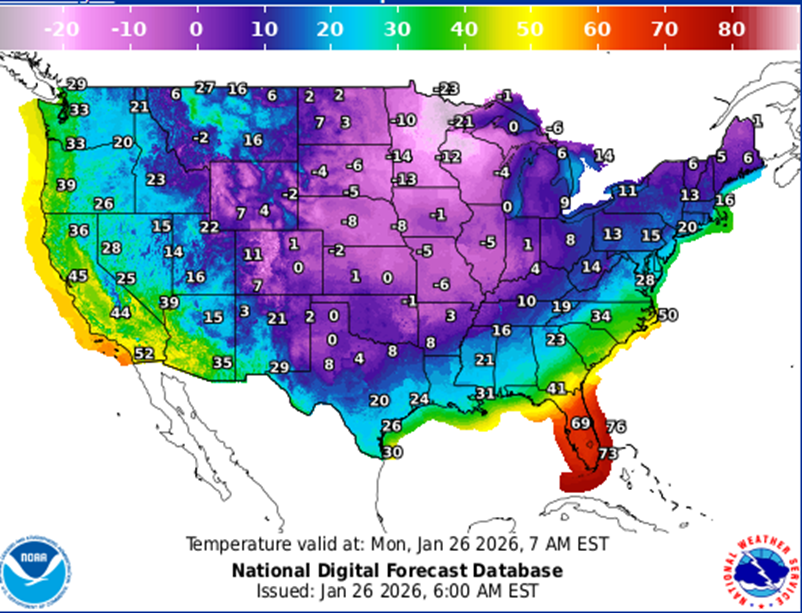

Today’s Forecast

Source: National Weather Service – PFL Analytics

Stay safe and stay warm out there. If you require any assistance call PFL now at 239-390-2885.

We are Watching Petroleum Carloads

The four-week rolling average of petroleum carloads carried on the six largest North American railroads fell to 28,558 from 28,731, which was a decrease of -173 rail cars week-over-week. Canadian volumes were lower. CPKC’s shipments were lower by -5.0% week-over-week, CN’s volumes were lower by -2.0% week-over-week. U.S. shipments were mostly lower. The BN had the largest percentage decrease and was down by -16.0%. The CSX was the sole gainer and was up by +4.0%.

We are watching Alberta Butane

Alberta’s butane market is now seeing impacts from an extended outage at Keyera’s AEF fractionation plant, which has been offline since early December 2025 and is expected to remain out of service until late March or early April 2026. While the outage itself is not new, its effects are becoming more visible as the market moves deeper into the downtime window.

AEF is a key component of Western Canada’s NGL system, producing purity products such as butane used largely for gasoline blending. With the facility down for roughly four months, Alberta butane supply has been reduced through the heart of winter, weighing on demand as blending economics soften and buyers adjust to lower availability.

Early in the outage, the market was able to manage the disruption using inventories and short-term logistical adjustments. As January turns to February, those buffers are thinning. That is when the impact starts to show up more clearly: in pricing relationships, storage behavior, and rail activity, making the outage increasingly relevant now for shippers and service providers.

Alberta butane pricing has weakened relative to other North American hubs, reflecting the loss of production rather than a demand-driven shift. The effect on U.S. markets has been limited. U.S. supply remains ample, and there is little indication that the outage is pulling incremental barrels south. Instead, Canadian volumes are effectively sidelined until AEF returns, leaving broader U.S. market fundamentals largely unchanged.

For rail, this is not a story about cross-border surges, it’s about reduced Western Canadian NGL movement during the outage period:

- No material increase in U.S.-bound Canadian butane traffic;

- Fewer outbound butane rail shipments tied to winter blending demand;

- Operational adjustments as shippers manage equipment and timing during the outage.

As the outage moves into its later stages in February and March, rail decisions around car placement, storage duration, and spring repositioning are becoming more active. Once the AEF plant returns to service, butane supply, and associated rail activity, is expected to recover relatively quickly.

Near-term NGL rail activity in Western Canada remains subdued pending the plant’s return to service later this spring.

PFL supports customers to help manage changing rail dynamics, whether that means adjusting dwell strategies, coordinating movements, or staying prepared for a restart when volumes return. Call PFL today, we are here to help.

We are Watching Grain

It is going to get real busy, folks. Grain-related rail activity across North America is starting to shift as the market looks past winter constraints and toward spring export and domestic demand programs. While volumes remain seasonally muted, rail positioning and planning activity picked up last week as elevators, traders, and railroads prepare for heavier movement later in Q1 and early Q2.

In both the U.S. and Canada, winter operating conditions have limited near-term velocity, particularly for covered hopper traffic moving through northern corridors. Even so, grain supply remains ample, and railroads are beginning to align equipment and network capacity ahead of the next demand window.

The transition is visible across major grain corridors served by BNSF Railway, Union Pacific, and Canadian Pacific Kansas City, where winter constraints are gradually giving way to early spring planning. While this is not yet a volume surge, it marks the point where railcar placement, routing, and cycle expectations begin to shift.

Export markets are a key driver. As river conditions, port programs, and international demand firm up, rail becomes increasingly important for positioning grain to coastal terminals and domestic processors. That dynamic is especially relevant for Canadian grain movements, where rail is the primary link between inland production and export facilities.

We are watching Left Wing Canadian Prime Minister Carney

Well, we knew that the trade deal that left-wing Carney cut with China to buy electric cars from China in exchange for Canada selling the Chinese canola wasn’t to go over well with President Trump and it didn’t. Trump reacted via truth Social over the weekend on Saturday threatening to impose a 100% tariff on goods imported from Canada if Carney went ahead with its trade deal with China.

Mr. Trump said in a social media post that if Canadian Prime Minister Mark Carney “thinks he is going to make Canada a ‘Drop Off Port’ for China to send goods and products into the United States, he is sorely mistaken.”

Mr. Trump initially had said that agreement was what Carney “should be doing and it’s a good thing for him to sign a trade deal.”

We Continue to Watch the UP and NS Merger

The STB issued a decision unanimously rejecting the merger application filed by UP and NS “because the STB says it does not contain certain information required by the board’s regulations. Which includes “future market share projections showing the combined effects of merger-related growth, diversions, and merger-influenced and other changes to market conditions that applicants anticipate.”

According to the STB, the submission from UP and NS includes their Agreement and Plan of Merger but does not include “certain schedules and documents that are expressly made part of the merger agreement and that define applicants’ obligations under it.” UP and NS have made no attempt to justify why these materials were withheld from the board, the STB says.

UP and NS have until February 17th to inform the STB if they intend to resubmit their application. On January 16th,UP and NS issued a brief statement confirming their intention to do so. Stay tuned to PFL for further updates. We are watching this one closely!

We Continue to Watch Safety and Operational Developments

The National Transportation Safety Board issued its preliminary report last Monday for its investigation of a December 13, 2025, CSX train collision and subsequent derailment in Alabama, which resulted in the death of a CSX conductor. The accident occurred near milepost 421.5 on CSX’s South and North Alabama subdivision near Calera, Alabama. At 2:13 a.m. local time, the conductor was riding on a rail car being shoved from the main track into an auxiliary track. The rail car collided with a second rail car that had been cut from the train and left on the main track.

The collision caused three railcars to derail, including the railcar the conductor was riding. That car overturned, causing the conductor’s death. NTSB’s ongoing investigation will focus on hazard identification and mitigation strategies, CSX’s rules and procedures related to leaving rail cars clear of adjacent tracks, and internal and external oversight. The Federal Railroad Administration, the Alabama Public Service Commission, CSX and two labor unions are parties to the investigation.

The incident highlights ongoing safety concerns in the rail industry at a time when the proposed UP-NS merger is drawing intense scrutiny over labor and safety implications. Earlier this month, the Federal Railroad Administration announced it had collected a record $15.4 million in civil penalties from Class I railroads under a new streamlined settlement process for safety violations, including defective wheels and other equipment issues. The intersection of safety enforcement, labor scrutiny, and merger oversight creates operational and regulatory uncertainty for the industry in 2026.

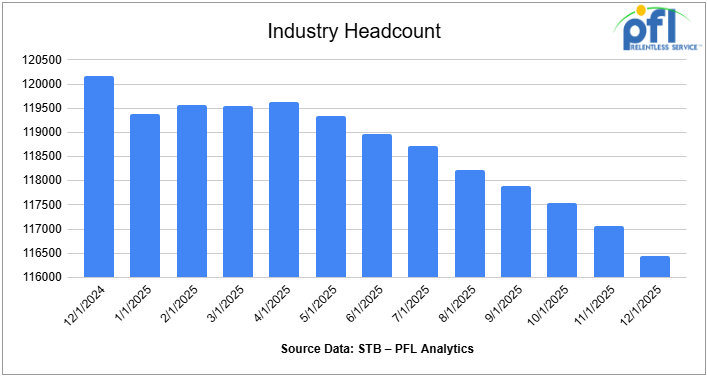

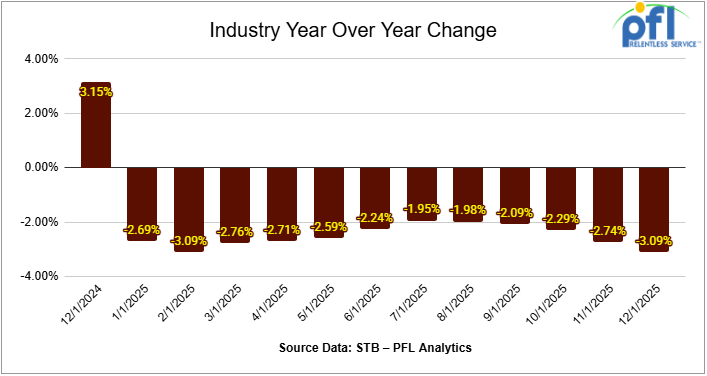

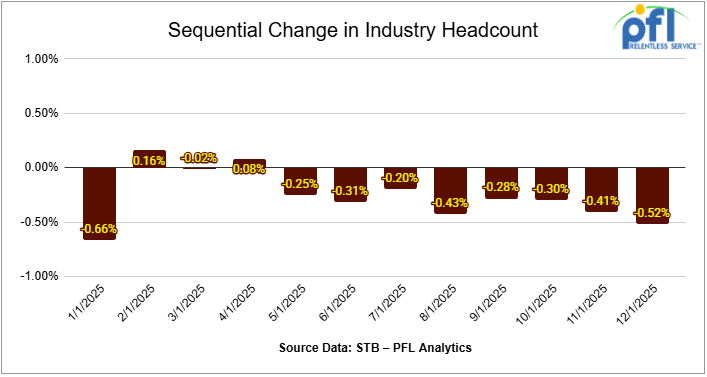

We are watching Class 1 Industry Headcount

Class I’s employed 116,451 workers in the United States in December, a -0.52% decrease from November 2025’s count and a -3.09% year-over-year decrease, according to Surface Transportation Board data.

Two of the six employment categories posted month-over-month increases between November and December. They were: executives, officials, and staff assistants, up 0.02% to 8,146 workers; and maintenance of equipment and stores, up 0.05% to 16,405.

Categories that posted month-over-month decreases were maintenance of way and structures, down -0.62% to 28,680; professional and administrative, down -0.13% to 8,932; transportation (other than train and engine), down -0.29% to 4,794; and transportation (train and engine), down -0.82% to 49,494.

Year-over-year, one category posted an employment gain: executives, officials, and staff assistants, up 3.86%.

Categories that registered year-over-year decreases in December were professional and administrative, -7.27%; transportation (other than train and engine), -4.94%; transportation (train and engine), -4.46%; maintenance of equipment and stores, -4.38%; and maintenance of way and structures, -0.04%.

We are Watching Key Economic Indicators

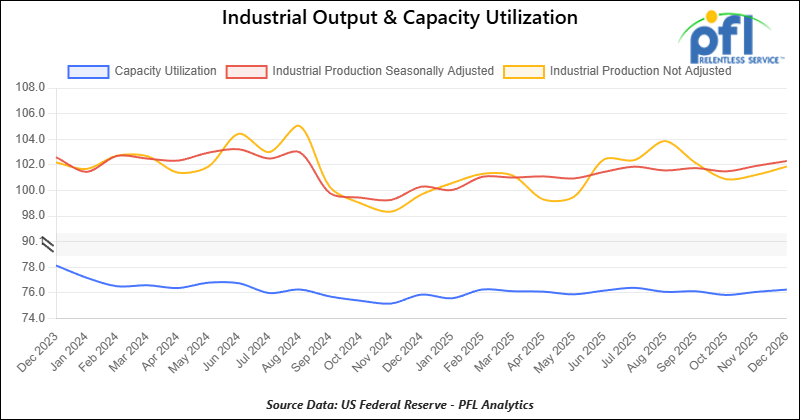

Industrial Output and Capacity Utilization

Manufacturing accounts for approximately 75% of total output. Manufacturing output in December was up 0.03% from November 2025.

Capacity utilization is a measure of how fully firms are using machinery and equipment. Capacity utilization was down -0.10% from November to December.

Lease Bids

- 30-50, 6000cf Steel Hopper located off of CSX or NS in East. For use in petcoke service. Period: 5 Years.

- 10, 2500CF Open Top Hopper located off of UP or BN in Texas. For use in aggregate service. Period: 5 years. Need Rapid Discharge Doors.

- 100, 21.9K 117J Tank located off of All Class 1s in Midwest. For use in CO2 service. Period: 6 months.

- 30-50, 30K 117J Tank located off of NS or CSX in Northeast. For use in C5 service. Period: 1 year.

- 60, 33K 340W Tank located off of BNSF in UT/AZ. For use in Propane service. Period: Trip Lease.

Sales Bids

- 28, 3400CF Hopper Covered located off of UP BN in Texas. For use in Cement service. Cement Gates needed.

- 20, 17K Tank DOT111 located off of various class 1s in various locations. For use in corn syrup service.

- 120, Various Gondola Open-Top Aluminum Rotary located off of various class 1s in various locations. For use in Sulphur service. Built 2004 or later.

- 30, 29K Tank DOT111 located off of various class 1s in Chicago. For use in Veg Oil service.

Lease Offers

- 100, 30K CPC1232 Tanks located off of UP or BN in Texas. Last used in Diesel.

- 100, 30K DOT117J Tanks located off of UP or BN in Texas. Last used in Gasoline.

- 100, 29K DOT117J Tanks located off of UP or BN in Texas. Last used in Gasoline. Coiled and Insulated.

- 36, 6351 Covered Hopper located off of CN in Wisconsin. Last used in Grain. through 2/27.

- 29, 6580 Covered Hopper located off of CN in Wisconsin. Last used in Grain. through 2/26.

- 18, 6580 Covered Hopper located off of CN in Wisconsin. Last used in Grain. through 2/27.

- 9, 5400 Covered Hopper located off of CN in Wisconsin. Last used in Grain. through 2/27.

- 21, 6351 Covered Hopper located off of CN in Wisconsin. Last used in DDG. Available until February 2027.

- 29, 6500 Covered Hopper located off of CN in Wisconsin. Last used in DDG. Available until February 2027.

- 50, 5380 Covered Hopper located off of UP or BN in Houston. Last used in Fertilizer. Cars are currently clean. Available until February.

- 50, 20K DOT117J Tank located off of All Class 1s in Moving. Last used in Styrene.

- 29, 25.5K DOT117J Tank located off of UP or BN in Texas. Cars are currently clean. Cars are currently clean.

- 90, 30K DOT117J Tank located off of UP or BN in Corpus Christie. Last used in Diesel.

Sales Offers

- 21, 50′ Boxcar Plate Cs located off of various class 1s in NM. End of Life.

- 3, 50′ Boxcar Plate Cs located off of various class 1s in multiple locations. End of Life.

- 27, 50′ Boxcar Plate Cs located off of various class 1s in PQ. End of Life.

- 100, 3250 Covered Hoppers located off of various class 1s in multiple locations. Sand Cars.

- 5, 2740 Mill Gondolas located off of various class 1s in NC. End of Life.

- 1, 2260 Mill Gondolas located off of various class 1s in AL. End of Life.

- 30, 2740 Mill Gondolas located off of various class 1s in multiple locations. End of Life.

- 21, 2740 Mill Gondolas located off of various class 1s in WA. End of Life.

- 9, 4750 Covered Hoppers located off of various class 1s in multiple locations. End of Life.

- 5, 4750 Covered Hoppers located off of various class 1s in multiple locations. End of Life.

- 50, 31.8K Tank CPC 1232s located off of UP or BN in TX. Requal Due in 2025.

- 100, 4600CF Open Top Hoppers located off of BN or CSX in Southeast.

Call PFL today to discuss your needs and our availability and market reach. Whether you are looking to lease cars, lease out cars, buy cars, or sell cars call PFL today at 239-390-2885

Live Railcar Markets

| CAT | Type | Capacity | GRL | QTY | LOC | Class | Prev. Use | Offer | Note |

|---|

PFL will be at the Following Conferences

- Where: La Quinta, CA

- Attending: David Cohen (954-729-4774)

- Conference Website

- Where: Hyatt Regency Dallas in Dallas, TX

- Attending:Curtis Chandler (239.405.3365), David Cohen (954-729-4774), Brian Baker (239.297.4519), Cyndi Popov(403) 402-5043

- Conference Website