The greatest use of a life is to spend it on something that will outlast it.

-William James

Jobs Update

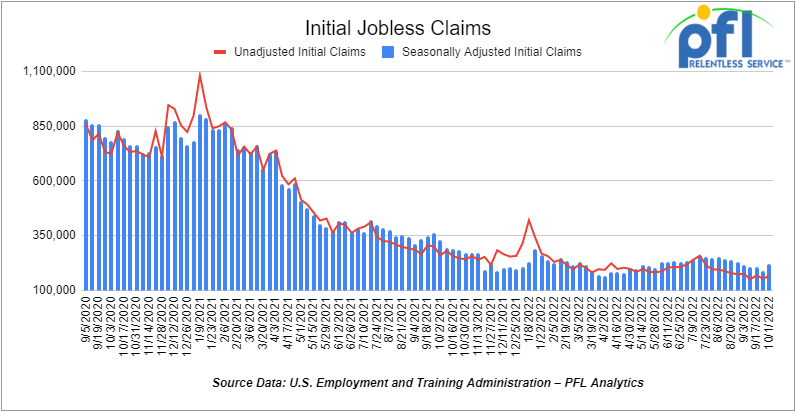

- Initial jobless claims for the week ending October 1st, 2022 came in at 219,000, up +29,000 people week-over-week.

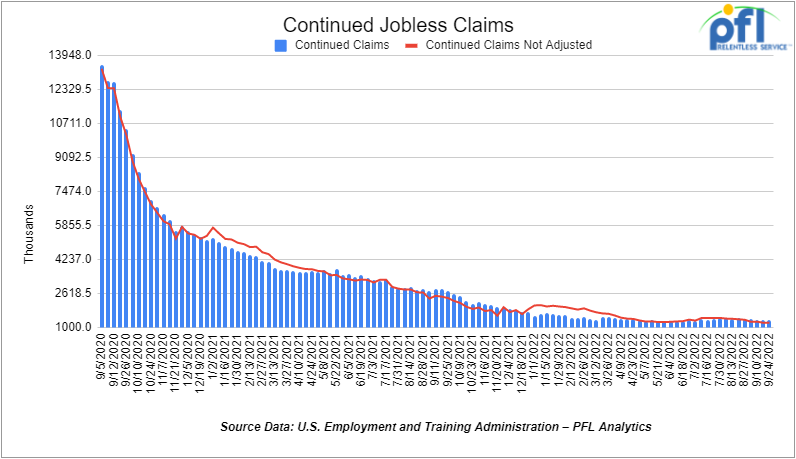

- Continuing jobless claims came in at 1.361 million people, versus the adjusted number of 1.346 million people from the week prior, up +15,000 people week over week.

Stocks closed lower on Friday of last week and mixed week over week

The DOW closed lower on Friday of last week, down -630.15 points (-2.11%),closing out the week at 29,296.79, down -194.1 points week over week. The S&P 500 closed lower on Friday of last week, down -104.86 points (-2.8%) and closed out the week at 3,639.66, down -38.77 points week over week. The NASDAQ closed lower on Friday of last week, down -420.91 points (-3.89%), and closed the week at 10,652.4, down -163.04 points week over week.

In overnight trading, DOW futures traded lower and are expected to open at 29,316 this morning down -37 points.

Oil closed higher on Friday of last week and up week over week

Oil prices rallied on Friday of last week to five-week highs, trading up every single day during last week. WTI was up last week by 17% week over week. The rise in crude was on the back of OPEC+s decision to make its largest supply cut since 2020 of 2 million barrels per day. The US expressed disappointment with the decision for OPEC+ announcing the cutting of crude production and are looking at all alternatives to reduce prices (hopefully not selling more of our strategic reserves – that helped so much last time). Both crude contracts (WTI and Brent) had their highest close since August and heating oil futures also rallied last week to its highest close on record due to low inventory going into the heating season. WTI traded up $4.19 per barrel (+4.7%) to close at $92.64 per barrel on Friday of last week, up $13.15 per barrel week over week. Brent traded up US$3.50 per barrel (+3.7%) on Friday of last week to close at US$97.92 per barrel, up $12.78 per barrel week over week.

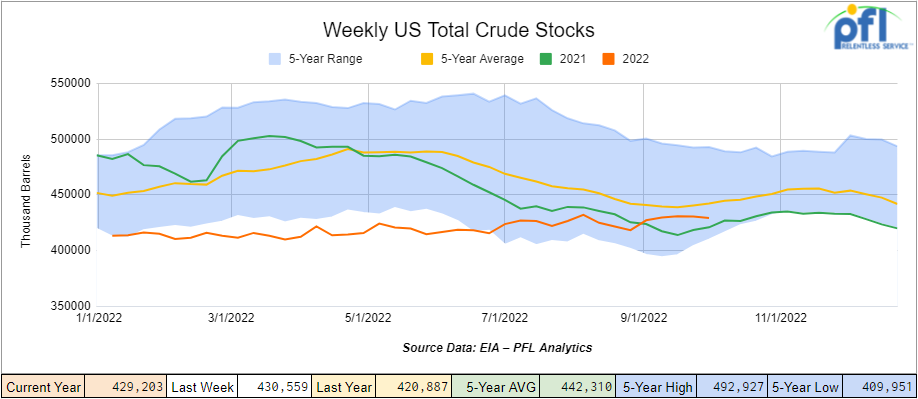

U.S. commercial crude oil inventories (excluding those in the Strategic Petroleum Reserve) decreased by 1.4 million barrels week over week. At 429.2 million barrels, U.S. crude oil inventories are 3% below the five-year average for this time of year.

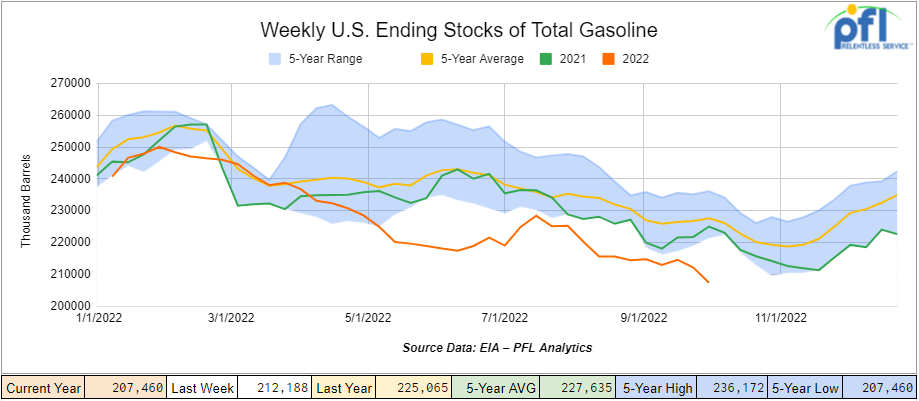

Total motor gasoline inventories decreased by 4.7 million barrels week over week and are 9% below the five-year average for this time of year.

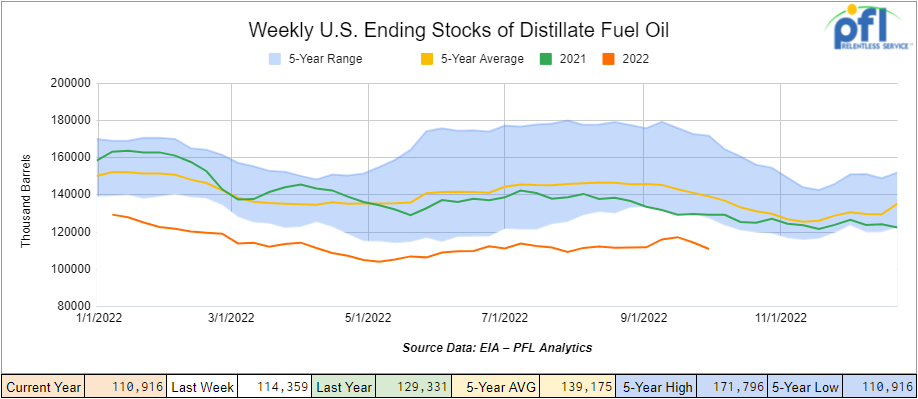

Distillate fuel inventories decreased by 3.4 million barrels week over week and are 21% below the five-year average for this time of year.

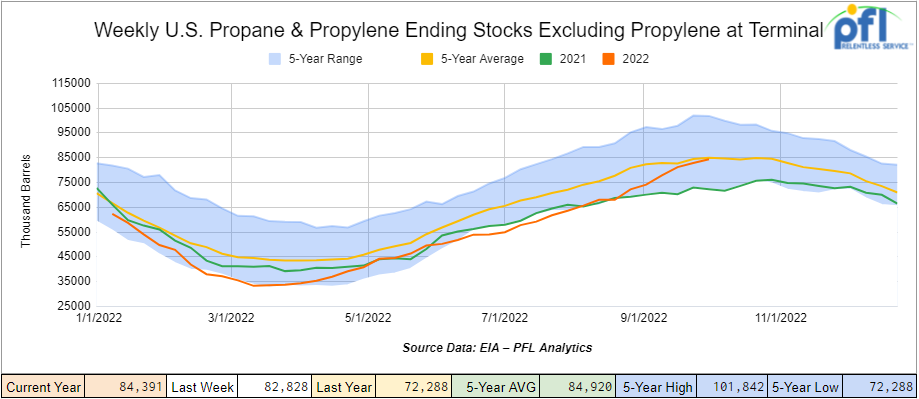

Propane/propylene inventories increased by 1.6 million barrels week over week and are at the five-year average for this time of year.

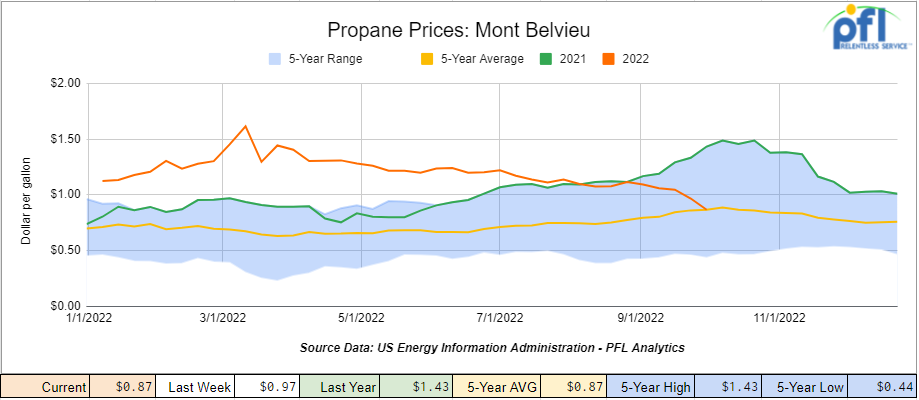

Folks, with inventories rising to the 5 year average propane prices have been coming of hard as of late. Propane prices were down 10 cents per gallon week over week closing at 87 cents per gallon on Friday of last week, which is off a whopping 60 cents per gallon year over year.

Overall, total commercial petroleum inventories decreased by 10 million barrels week over week.

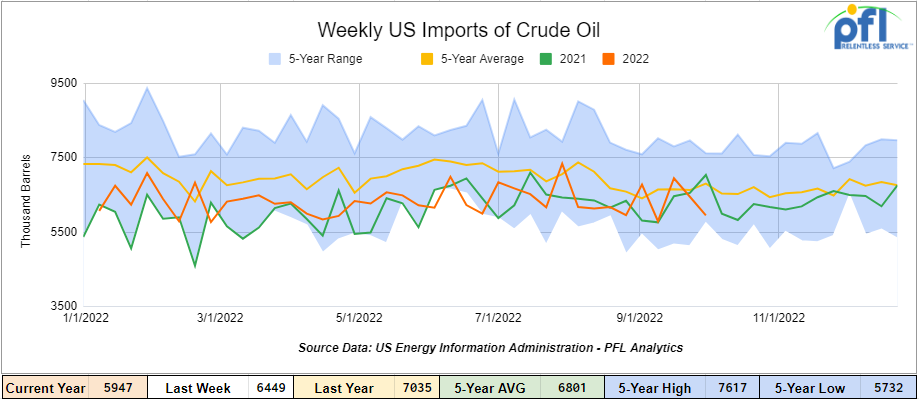

U.S. crude oil imports averaged 5.9 million barrels per day during the week ending September 30th, 2022, a decrease of 500,000 barrels per day week over week. Over the past four weeks, crude oil imports averaged 6.3 million barrels per day, 2.6% less than the same four-week period last year. Total motor gasoline imports (including both finished gasoline and gasoline blending components) averaged 480,000 barrels per day, and distillate fuel imports averaged 81,000 barrels per day during the week ending September 30th, 2022.

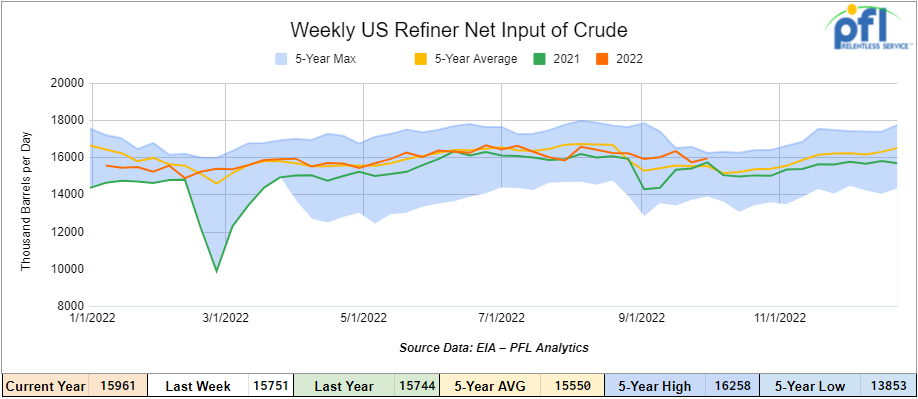

U.S. crude oil refinery inputs averaged 16 million barrels per day during the week ending September 30, 2022 which was 210,000 barrels more per day week over week.

As of the writing of this report, WTI is poised to open at $91.73, down -$0.91 per barrel from Friday’s close.

North American Rail Traffic

Week Ending September 24th, 2022.

Total North American weekly rail volumes were down (-2.43%) in week 39 compared with the same week last year. Total carloads for the week ending October 1st were 354,709, down (-0.39%) compared with the same week in 2021, while Weekly intermodal volume was 333,360, down (-4.51%) compared to 2021. 7 of the AAR’s 11 major traffic categories posted year-over-year decreases with the most significant decrease coming from Grains (-11.29%). The largest increase was from Motor Vehicles and Parts (+17.9%).

In the east, CSX’s total volumes were down (-2.27%), with the largest decrease coming from Nonmetallic Minerals (-22.28%) and the largest increase from Coal (+28.71%). NS’s volumes were down (-5.11%), with the largest decrease coming from Chemicals (-17.73%) and the largest increases from Petroleum and petroleum Products (+39.86%).

In the west, BN’s total volumes were down (-6.53%), with the largest decreases coming from Grain (-21%) and Metallic Ores and Minerals (-20.55%), and the largest increase coming from Motor Vehicles and Parts (+15.90%). UP’s total rail volumes were up (+2.7%) with the largest decrease coming from Other (-10.55%) and the largest increase coming from Motor Vehicles and Parts (+27.78%).

In Canada, CN’s total rail volumes were up (+1.75%) with the largest decrease coming from Other (-11.25%) and the largest increase coming from Motor Vehicles and Parts (+35.01%). CP’s total rail volumes were down -0.96% with the largest decrease coming from Metallic Ores and Metals (-52.52%) and the largest increase coming from Nonmetallic Minerals (+31.15%).

KCS’s total rail volumes were up (+1.2%) with the largest decrease coming from Farm Products (-19.01%) and largest increase coming from Motor Vehicles and Parts (+72.6%).

Source Data: AAR – PFL Analytics

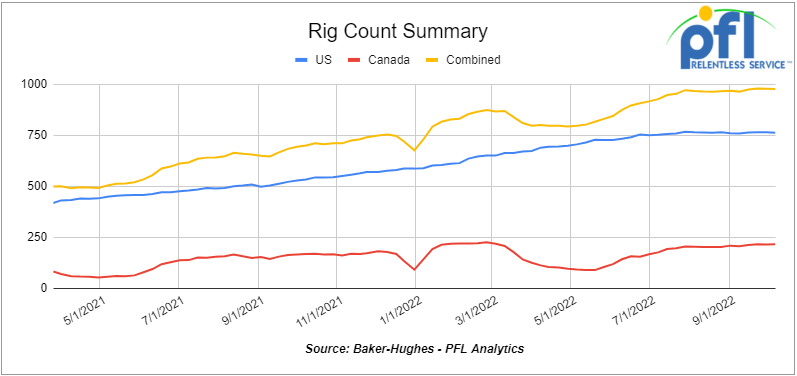

Rig Count

North American rig count was down by -1 week over week. U.S. rig count was down by -3 rigs week-over-week and up by 229 rigs year over year. The U.S. currently has 762 active rigs. Canada’s rig count was up by +2 rigs week-over-week, and up by 48 rigs year-over-year. Canada’s overall rig count is 215 active rigs. Overall, year over year, we are up +277 rigs collectively.

International rig count, which is reported monthly, was up by +19 rigs month over month and up +92 rigs year over year. Internationally, there are 879 active rigs.

North American Rig Count Summary

A few things we are keeping an eye on:

We are Watching Alberta vs. Canada – Could Get Interesting Folks.

On Thursday of last week there was a vote on who was going to be the next Premier of Alberta. This position is like the Governor of a State here in the U.S. The former Premier Jason Kenny whose ambition was to be the next Prime Minister (President) of CANADA and was a federalist – putting the country first at the expense of Alberta no matter what the cost was to Alberta. The people of Alberta did not like this, and he was forced to resign and a new leader for Alberta emerged, and that leader is Danielle Smith. You may want to compare her to Ron DeSantis the Governor of Florida who puts the State of Florida first. Things in Alberta are going to change real fast. She will have a massive impact on Alberta’s Oil and gas production and crude by rail for that matter opening the taps and Justin Trudeau the current leader of CANADA will not be able to push Alberta around anymore, at least that is the word on the street.

Alberta’s incoming premier Danielle Smith pledged to work for a prosperous oil-rich province without asking the federal government for permission to produce and export energy.

The new premier, who was elected to lead Alberta’s ruling United Conservative Party (UCP), told party members on Thursday of last week, “Today marks a new beginning in the Alberta story.”

“Today we start putting Alberta First!!!” Smith tweeted on Friday on last week. Her campaign has focused on an ‘Alberta First’ slogan and against the outreach of the federal government. The new premier could put Alberta on a collision course with Canada’s Prime Minister Justin Trudeau, a vocal supporter of the fight against climate change and plans to reduce emissions.

“No longer will Alberta ask permission from Ottawa to be prosperous and free … we will not have our resources landlocked or our energy phased out of existence by a virtue-signaling prime minister,” Smith said at a meeting of the UCP party.

Alberta, CANADA’s oil-rich province, has been looking to boost the production of oil and gas, while CANADA’s federal government has adopted in recent years legislation aiming to reduce emissions and make Canada a net-zero economy by 2050.

So far this year, Alberta’s oil production and economy have benefited from the high oil and gas prices, but the province still wants additional export outlets for its hydrocarbon resources, most of which have been stymied at the federal level or by other provinces.

Crude oil production in Alberta reached a record high in the first half of the year at 3.6 million barrels per day (bpd), which was 100,000 bpd higher than the average output for the first half of 2021. In terms of oil and gas income, higher oil and gas prices are expected to lead to a surplus of some $9.6 billion (C$13.2 billion) for Alberta this fiscal year. Stay tuned to PFL we are watching this one folks.

We are watching Petroleum Carloads

The four-week rolling average of petroleum carloads carried on the six largest North American railroads rose to 23,257 from 23,003 which was a gain of 254 railcars week-over-week. The rise in petroleum car loads snapped a nine week period of week over week declines. Canadian volumes were mixed, CP’s shipments rose by +6.4% week over week, and CN’s volumes were down by -1.8% week over week. U.S. shipments were mostly higher. The BN had the largest percentage increase, up by 28%, and the UP was the sole decliner and was down by -10%

Some Key Economic Indicators

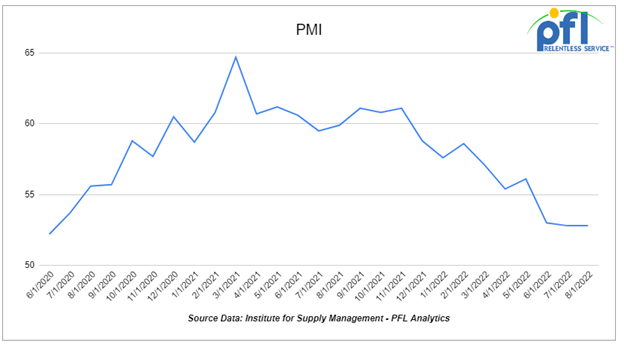

Purchasing Managers Index (“PMI”) – The PMI (which covers manufacturing) and the Services PMI (covering services) are both from the Institute for Supply Management. They are based on surveys of supply managers around the country. The surveys track the direction of changes in business activity. An index reading above 50% indicates expansion; below 50% means contraction. The more above or below 50, the faster the pace of change.

The PMI was down month over month at 50.9% in September This is the lowest level since May of 2020. The new orders component of the PMI fell month over month, coming in at 47.1 from 51.3% in August making it a contraction month.

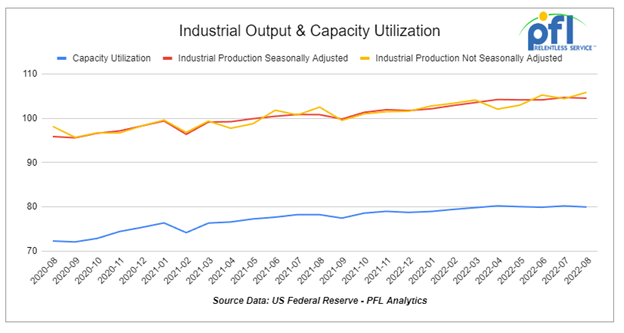

Industrial Output and Capacity Utilization – According to the Federal Reserve, preliminary seasonally adjusted total U.S. industrial output fell 0.2% in August 2022 from July 2022 on the back of a 2.3% weather related utility output decline. The decline in total output in August was only the second so far. Total output in August 2022 was 3.7% higher than in August 2021.

Output in manufacturing, which accounts for 75% of total output, was up a preliminary 0.1% in August. It too has been generally flat in recent months. Manufacturing output was 3.3% higher in August 2022 than in August 2021.

In August, output at petroleum refineries rose 3.6% from July, bringing it close to its highest point this year. Iron and steel output in August 2022 fell slightly from July 2022 and was down 6.5% from August 2021. Output of motor vehicles and parts fell in August from July, as did output of grain mill products, agricultural chemicals, and railroad rolling stock. Motor vehicle assemblies were an annualized 10.5 million in August 2022, the most since December 2020 and a reflection of lower supply chain constraints for automakers. Manufacturing output excluding autos was flat in August.

Overall capacity utilization was a preliminary 80.0% in August, down from 80.2% in July and roughly the same as it’s been for the past five months. For manufacturing, capacity utilization in August was a preliminary 79.6%, the same as in July. Utilization levels above 82% are generally considered “tight” and portend price increases or supply shortages in the near future. The farther below this level, the more slack there is in the economy or a particular sector.

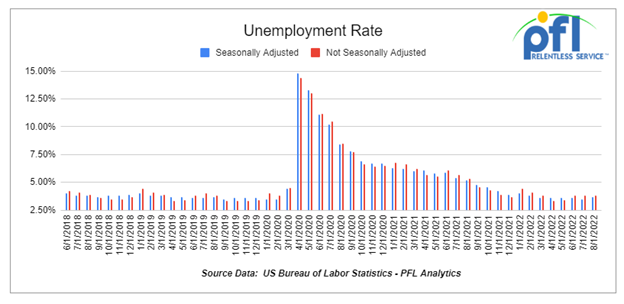

U.S. job growth was down month over month, but the unemployment rate ticked lower.

The Bureau of Labor Statistics reported on October 7th that a preliminary 263,000 net new jobs were created in September 2022. That’s down from 315,000 in July and 567,000 in July.

The official overall unemployment rate ticked down to 3.5% down 0.2% month over month matching the lowest level it has been at in 50 years.

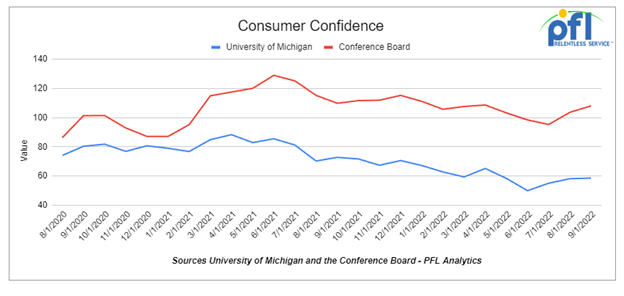

Surprisingly good news is that Consumer Confidence continued to move higher in August. The Conference Board’s Index rose to 108.0, up from 103.6 in August. That’s the second increase after three straight monthly declines.

The University of Michigan’s index of consumer sentiment rose too, albeit slightly, up to 58.6 in September from 58.2 in August.

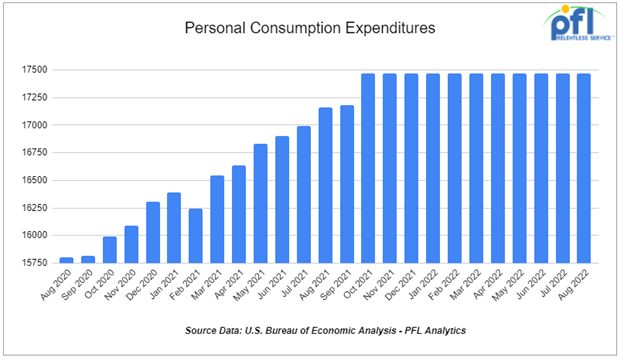

Total consumer spending not adjusted for inflation rose a preliminary 0.4% in August 2022 over July 2022. That’s the eighth straight month-to-month gains.

Spending on goods only rose 0.1% in August from July, an increase month over month, but beats the decline of 0.02% we had the month prior.

Spending on goods is falling behind spending on services. In August 2022, spending on goods fell 0.5%, echoing the fall of 0.7% from June to July (which was the largest drop since December 2021). Falling gasoline prices are behind some of the recent decline in spending on goods however, that looks as though it may change real soon.

We have been extremely busy at PFL with return on lease programs involving rail car storage instead of returning cars to a shop. A quick turnaround is what we all want and need. Railcar storage in general has been extremely active. Please call PFL now at 239-390-2885 if you are looking for rail car storage, want to troubleshoot a return on lease scenario, or have storage availability. Whether you are a car owner, lessor or lessee, or even a class 1 that wants to help out a customer we are here to “help you help your customer!”

Leasing and Subleasing has been brisk as economic activity picks up. Inquiries have continued to be brisk and strong Call PFL Today for all your rail car needs 239-390-2885

PFL is seeking:

- 5, 20K unlined tanks needed in Texas for 2 years BNSF – more needed by year end

- 100-200, 340W Pressure cars for a 12 month term for propane. Can take in various locations, needed ASAP

- 30-50, Asphalt cars needed in Wisconsin on the CN for 6 months. Dirty to Dirty.

- 10-15, 25.5K-27k Gallon pressure cars for various commodities 5-8 year term

- 20-25, CPC 1232 28.3K C/I Tank Cars for Feedstock in the Midwest off the CN for 6 months. Dirty to Dirty. Needed September/October.

- 50, 340W Pressure cars needed for Winter lease starting in October for Propane. Can take in Texas.

- 50, 30K 117J needed in Texas or Louisiana for condensate. 6 month term, Dirty to Dirty. Can take last in Crude.

- 100 Coiled and insulated cars for Crude. Needed in Canada for 6 months. Dirty to Dirty

- 50 117Js with magrods in the east – 10 for immediate trip lease – 40 for longer term

- 50 6350 covered hoppers in the midwest with most class ones for up to 5 years for DDG

- Up to 40 5500 Covered Gons 286 unlined CSX/NS preferred but will consider other

- 4 Lined tanks for glycerin to run from Arkansas to Georgia 1-3 years

- 30 boxcars on UP or CP for 3 years to run from TX to Edmonton – negotiable

- 100, 2480 CU-FT Ag Gons needed in Texas off of the UP for 1-3 Years.

- 50, 117J 30K+ Tank cars are needed in several locations. Can take in various locations off various Class 1’s. Can have prior Ethanol heel or Gasoline heel

- Various Hoppers 286 GRL 4200-7000 CU FT in several locations negotiable

- 300 5800 Covered hoppers needed for plastic – 5-year lease – negotiable

- 50, 5800cuft or larger Covered Hopper for use in DDG needed in the Midwest for 3-4 years. Immediate need.

- 10-20 Covered hopper grain cars in the midwest 5200-5500 2-3 years

- 100 Moulton Sulfur cars for purchase – any location – negotiable

- 50 Ag Gons 2500-2800cuft 286k GRL in the east for 5 years negotiable

- 100 15K Tanks 286 for Molten Sulfur in the Northeast CSX/NS for 6 months negotiable

- 100, 5800 Covered Hoppers 286 can be West or East for Plastic 3-5 years

- 70, 117R or J needed for Ethanol for 3 years. Can take in the South.

- 50, 6500+ cu-ft Mill Gon or Open Top Hopper for wood chips in the Southeast for 5 Years.

- 20, 19,000 Gal Stainless cars in Louisiana UP for nitric acid 1-3 years – Oct negotiable

- 10, 6,300CF or greater covered hoppers are needed in the Midwest.

PFL is offering:

- 50, 30K 117Js Last in Diesel. Free move on the UP or BN. Can return Dirty

- 120, 30K 117Rs Last in Diesel. Free move on the UP or BN. Can return Dirty

- 25 117Rs for sublease dirty to dirty service BN/UP – negotiable

- 25, 31.8K CPC 1232 last in Crude in New Mexico. Dirty to Dirty.

- 200 Clean C/I 25.5K 117J in Texas. Brand New Cars!

- 150 DOT 111s last in ethanol in the Midwest with free move.

- Up to 500 sand cars for sale or lease at various locations and class ones – Great Price!

- 150 117R’s 31.8 clean for lease in Texas KCS – for sale or lease – negotiable

- 31.8K Tank Cars last in Diesel. Dirty to dirty in Texas

- 200 117Js 29K in the Midwest. Lined and brand new- lease negotiable

- 100 117Rs dirty last in Gasoline in Texas for lease Negotiable

- Various Hoppers for lease 263 and 268 multiple locations negotiable

- 300W pressure cars located in various locations.

- 200 117Js 29K OK and TX Clean and brand new – Lined- lease negotiable

- Various tank cars for lease with dirty to dirty service including, nitric acid, gasoline, diesel, crude oil, Lease terms negotiable, clean service also available in various tanks and locations including Rs 111s, and Js.

Call PFL today to discuss your needs and our availability and market reach. Whether you are looking to lease cars, lease out cars, buy cars or sell cars call PFL today at 239-390-2885

PFL offers turn-key solutions to maximize your profitability. Our goal is to provide a win/win scenario for all and we can handle virtually all of your railcar needs. Whether it’s loaded storage, empty storage, subleasing or leasing excess cars, filling orders for cars wanted, mobile railcar cleaning, blasting, mobile railcar repair, or scrapping at strategic partner sites, PFL will do its best to assist you. PFL also assists fleets and lessors with leases and sales and offers Total Fleet Evaluation Services. We will analyze your current leases, storage, and company objectives to draw up a plan of action. We will save Lessor and Lessee the headache and aggravation of navigating through this rapidly changing landscape.

Live Railcar Markets

| CAT | Type | Capacity | GRL | QTY | LOC | Class | Prev. Use | Offer | Note |

|---|