“There’s no use doing a kindness if you do it a day too late.”

– Charles Kingsley

Jobs Update

Initial and Continuing Jobless Claims

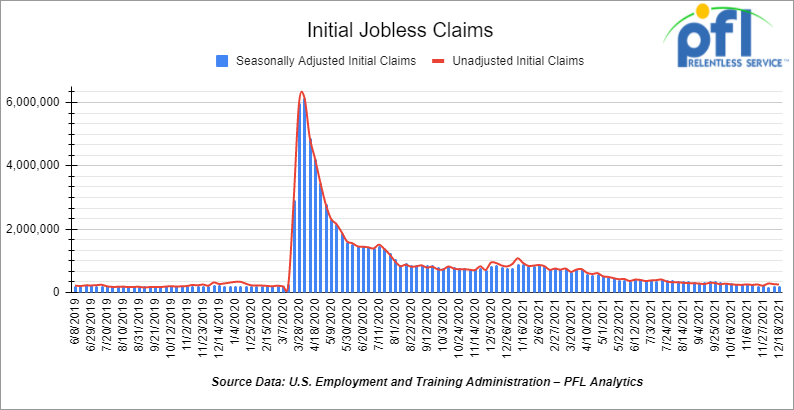

- Initial jobless claims for the week ending December 18th came in at 205,000, flat week over week.

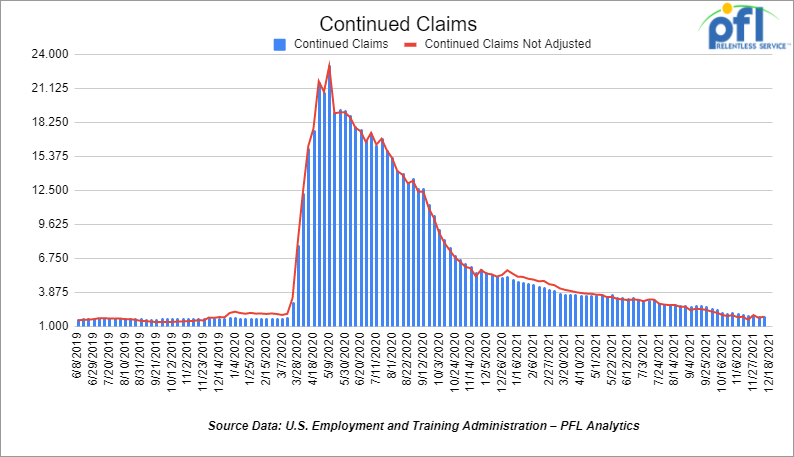

- Continuing claims came in at 1.859 million people versus the adjusted number of 1.867 million people from the week prior, down -8,000 people week over week.

Stocks closed higher on Thursday of last week and higher week over week

The DOW closed higher on Thursday of last week, up +196.67 points (+.55%), closing out the week at 35,950.60 points, up +585.60 points week over week. The S&P 500 closed higher on Thursday of last week, up +29.23 points (+.62 %) and closed out the week at 4,725.79, up +105.15 points week over week. The Nasdaq closed higher on Thursday of last week, up +131.48 points (+.85%) and closed out the week at 15,653.40, up +483.72 points week over week.

In overnight trading, DOW futures traded higher and are expected to open at 35,865 this morning up 33 points.

Oil closed up on Thursday of last week and up week over week

West Texas Intermediate (WTI) crude closed up +$1.03 a barrel on Thursday of last week, or +1.4% to settle at $73.79 per barrel up +$2.93 cents a barrel week over week, while Brent futures closed up +$1.56 per barrel, or up 2.1% to settle at +$76.85 per barrel, up $3.33 per barrel week over week.

U.S. commercial crude oil inventories (excluding those in the Strategic Petroleum Reserve) decreased by 4.7 million barrels week over week. At 423.6 million barrels, U.S. crude oil inventories are 8% below the five year average for this time of year.

Total motor gasoline inventories increased by 5.5 million barrels last week and are 4% below the five year average for this time of year.

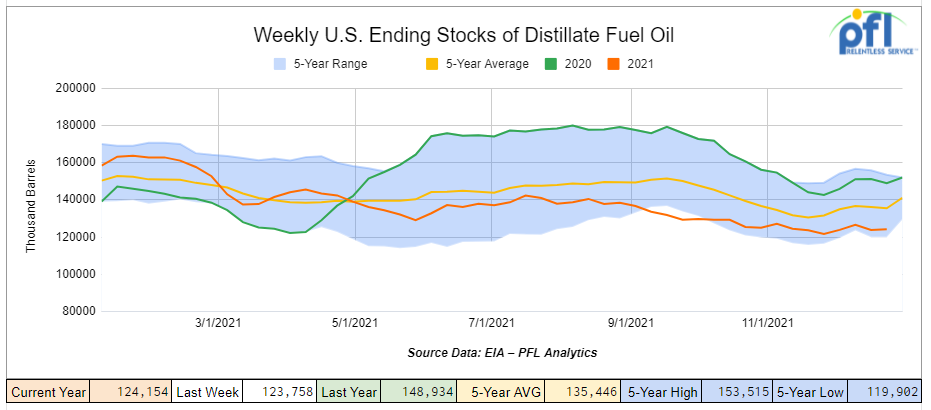

Distillate fuel inventories increased by 400,000 barrels week over week and are 8% below the five year average for this time of year.

Propane/propylene inventories decreased by 800,000 barrels week over week and are 8% below the five year average for this time of year.

Propane Prices – were flat week over week as inventories here in the U.S. continue to stabilize on warmer than normal winter weather so far this year.

Overall, total commercial petroleum inventories decreased by 7.0 million barrels last week.

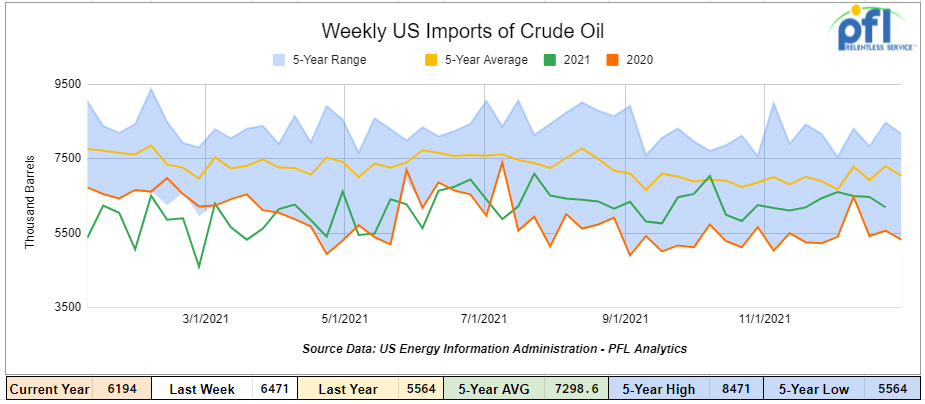

U.S. crude oil imports averaged 6.2 million barrels per day, down by 277,000 barrels per day for the week ending December 17, 2021. Over the past four weeks, crude oil imports averaged 6.4 million barrels per day, 12.7% more than the same four-week period last year. Total motor gasoline imports (including both finished gasoline and gasoline blending components) averaged 688,000 barrels per day, and distillate fuel imports averaged 203,000 barrels per day for the week ending December 17th.

U.S. crude oil refinery inputs averaged 15.8 million barrels per day during the week ending December 17, 2021 which was 148,000 barrels per day more than the previous week’s average. Refineries operated at 89.6% of their operable capacity last week.

As of the writing of this report, WTI is poised to open at 72.98 , down -$0.81 per barrel from Thursday’s close.

North American Rail Traffic

Total North American rail volumes were down 4.3% year over year in week 50 (U.S. -3.1%, Canada -9.7%, Mexico +4.0%) resulting in quarter to date volumes that are down 5.3% and year to date volumes that are up 4.8% year over year (U.S.+5.9%, Canada +1.0%, Mexico +4.3%). 6 of the AAR’s 11 major traffic categories posted year over year decreases with the largest declines coming from intermodal (-7.0%) and grain (-16.3%). The largest increase came from nonmetallic minerals (+13.8%).

In the East, CSX’s total volumes were down 0.6%, with the largest decrease coming from motor vehicles & parts (-23.2%). The largest increase came from intermodal (+3.0%). NS’s total volumes were down 1.6%, with the largest decreases coming from intermodal (-7.3%) and motor vehicles & parts (-20.5%). The largest increases came from coal (+15.3%) and petroleum (+55.8%).

In the West, BNSF’s total volumes were down 2.7%, with the largest decrease coming from intermodal (-6.7%). The largest increase came from stone sand & gravel (+40.7%). UP’s total volumes were down 4.4%, with the largest decreases coming from intermodal (-11.9%), grain (-20.8%) and motor vehicles & parts (-15.9%). The largest increases came from stone sand & gravel (+31.8%) and coal (+8.3%).

In Canada, CN’s total volumes were down 5.9%, with the largest decreases coming from intermodal (-11.5%) and metallic ores (-16.2%). The largest increases came from coal (+56.7%) and chemicals (+13.8%). Revenue per ton miles was down 3.8%. CP’s total volumes were down 10.0%, with the largest decreases coming from grain (-40.8%) and intermodal (-7.6%). Revenue per ton miles were down 10.0%.

KCS’s total volumes were up 2.5%, with the largest increase coming from intermodal (+15.5%). The largest decrease came from petroleum (-38.1%).

Source Data: Stephens

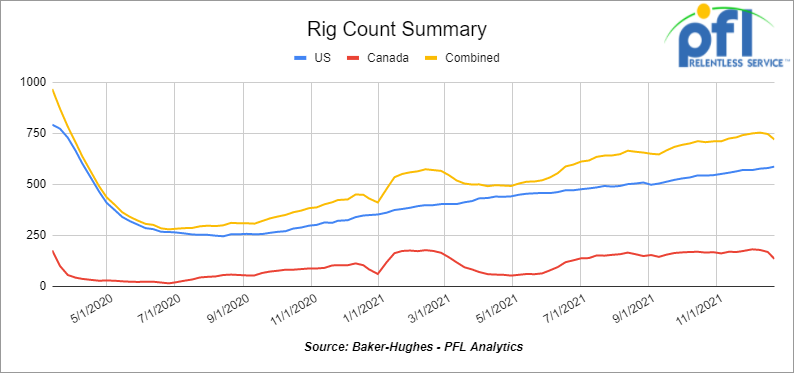

Rig Count

North American rig count is down by 27 rigs week over week. The U.S. rig count was up by 7 rigs week over week and up by 238 rigs year over year. The U.S. currently has 586 active rigs. Canada’s rig count was down by 34 rigs week over week but up by 51 rigs year over year and Canada’s overall rig count is 133 active rigs. Overall, year over year, we are up 289 rigs collectively.

North American Rig Count Summary

A few things we are keeping an eye on:

Petroleum Carloads

The four-week rolling average of petroleum carloads carried on the six largest North American railroads rose to 25,194 from 24,704, a gain of 490 rail cars week over week. Canadian volumes were down: CP volumes were down by 11.9% and CN volumes were down by 0.8 % week over week. U.S. volumes were mostly lower with the NS having the largest percentage increase (up by 18.6%) and the CSX having the largest percentage decrease (down by 10%).

DOE Awards Second Strategic Petroleum Reserve Exchange to Bolster Fuel Supply Chain

The U.S. Department of Energy (DOE) approved a second exchange of 250,000 barrels of crude oil for release to Marathon Petroleum Company from the Strategic Petroleum Reserve (SPR). This release falls under the authorization published in the DOE announcement on November 23, 2021.

DOE has provided over 5 million barrels of SPR crude oil to boost the nation’s fuel supply, including the first exchange awarded to ExxonMobil earlier in the month. As with all exchanges, companies that receive SPR crude oil through the exchange agree to return the amount of crude oil received, as well as an additional amount, depending upon the length of time in which they hold the oil.

Additional information about SPR exchanges can be found here. According to the IEA oil consumption is expected to trail the increase in supply rising by 3.3 million barrels of oil per day and 99.5 million of barrels of oil next year. That puts consumption at 3.5 million less than forecasted. Domestic production here in the US is poised to rise by 1.8 million barrels per day. Some are saying that we are over a short market and are poised to enter into one that is over supplied and the release of SPR was and is unnecessary. On that note US SPR Inventories Drop to Lowest in 19 Years. With the US pushing through with its planned SPR releases, the total stock of strategic crude reserves fell to 596 million barrels, the lowest it has been since November 2002.

Take a look at Canada: Supply output for 2022

With the addition of Enbridge’s 760,000 bpd line 3 replacement project that added 360,000 bpd of capacity exports out of that country to the U.S Canada is expected to add to the already existing 3.73 million of crude being exported through the first 9 months of 2021 (which was just 90,000 barrels per day beneath its peak) The Trans mountain expansion that is expected to finish sometime during 2022 will add 590,000 barrels per day will add significant and meaningful expansion. Cenovus and Suncor are both gearing up for it. Both citing production increases of at least 5%.

In related news Capline started interim service from Patoka, Illinois, to St James, Louisiana, December, 18th with full operations of an initial 102,000 b/d starting 1 January. The pipeline had previously been carrying up to 1.2mn bl of mostly crude imports northward to Chicago area refineries. The line is owned by Marathon Petroleum, Plains All American and BP. The reversed Capline is only carrying about 100,000 b/d initially, there is potential for it to expand to meet refinery demand. The line could also carry Bakken crude southward from Patoka.

We have been extremely busy at PFL with return on lease programs involving rail car storage instead of returning cars to a shop. A quick turnaround is what we all want and need. Railcar storage in general has been extremely active. Please call PFL now at 239-390-2885 if you are looking for rail car storage, want to trouble shoot a return on lease scenario or have storage availability. Whether you are a car owner, lessor or lessee or even a class 1 that wants to help out a customer we are here to “help you help your customer!”

Leasing and Subleasing has been brisk as economic activity picks up. Inquiries have continued to be brisk and strong Call PFL Today for all your rail car needs 239-390-2885

PFL is seeking:

- 50 25.5 Tanks C&I for heavy fuel oil in Texas dirty to dirty 1-2 years negotiable

- 20 pressure cars 340’s in SE clean or last in butane or propane 1-2 years Immediate Need

- 20 5200-6200 PD hoppers in the south for 1-2 years lined non-food grade negotiable

- 30 5800 and 6250 covered gons for sale

- 100 117Js Coiled and Insulated dirty to dirty service BNSF CN or CP

- 50, 5800cuft or larger Covered Hopper for the use in DDG needed in the Midwest for 3-4 years. Immediate need.

- 10 25-28K C&I tanks for veg oil needed in the south for 2 years negotiable

- 10-20 Covered hopper grain cars in the midwest 5200-5500 2-3 years

- 20-30, 19K Tank Cars for Caustic Soda needed in Texas off the UP or BN.

- Unit Train of 28.3K 117Js for use in Crude service off the CN or BN in MT, ND, or Alberta.

- 100-150 340 pressure cars for LPG service in Texas

- 70-90 Biodiesel cars C&I any type car in the midwest or TX 1-2 years

- 15-25, 23.5K cars for chem needed in the South for 1 Year.

- 50 117R 30K+ for gasoline in the midwest CSX or NS for 6 months negotiable

- 100 Moulton Sulfur cars for purchase – any location – negotiable

- 10 DOT111 or 1232 25.5K 286 GRL for Crude Glycerin anywhere in US 1 year lease

- 12 Plate F 286 GRL Boxcars 12’ plug doors midwest preferred for 1 year lease

- 30-50 Log Flats with stanchions 286K GRL in the midwest/east CSX NS 1-3 years negotiable

- 50 Ag Gons 2500-2800cuft 286k GRL in the east CSX for 5 years negotiable

- 25 Covered wood chip Gons 6000CF 286 GRL any location for 1-3 years negotiable

- 25 Boxcars for paper 6000CF 286 GRL 1-3 years anywhere

- 10-20 propane cars needed for a short term lease in ND off the CP.

- 100 15K Tanks 286 for Molten Sulfur in the Northeast CSX/NS for 6 months negotiable

- 200 117Js 28.3 C&I 286 in the North on the CN for 1 year Crude dirty to dirty Negotiable

- 20 5650 PD Hoppers 286s needed in Montana for talc BNSF for 3-5 years

- 100 Open Top Hoppers needed in the Midwest for coal BNSF 1 year

- 100, 5800 Covered Hoppers 286 can be West or East for Plastic 3-5 years

- 50-100, 4750 Covered Hoppers needed for Pet-coke. Can take in the South.

- 70, 117R or J needed for Ethanol for 3 years. Can take in the South.

- 30, 25.5’s or greater food grade Kosher veg oil cars for 6-12 months

- 50, 6500+ cu-ft Mill Gon or Open Top Hopper for wood chips in the Southeast for 5 Years.

- 25 bulkhead flats 286 any class one for up to 5 years Negotiable

- 10 open top hoppers 2400 C FT in Texas needed for stone on the UP 3-5 years

- 20, 19,000 Gal Stainless cars in Louisiana UP for nitric acid 1-3 years – Oct negotiable

- 10, 6,300CF or greater covered hoppers are needed in the Midwest.

- 2, 89’ Flat cars for purchase or lease – needed in TX off the BNSF

PFL is offering:

- Various tank cars for lease with dirty to dirty service including, nitric acid, gasoline, diesel, crude oil, Lease terms negotiable, clean service also available in various tanks and locations including Rs 111s, and Js – Selection is Dwindling. Call Today!

- 200 Clean C/I 25.5K 117J in Texas. Brand New Cars!

- 150 117R’s 31.8 clean for lease in Texas – negotiable

- 31.8K Tank Cars last in Diesel. Dirty to dirty in Texas

- 34 Clean C/I 25.5K CPC 1232’s located in PA.

- 200 117Js 29K OK and TX Clean and brand new – Lined- lease negotiable

- 142 111’s Clean last in gasoline in Texas for lease off the UP – negotiable

- 100 117Rs dirty last in Gasoline in Texas for lease Negotiable

- 90 117Rs 30K located in Alberta CN or CP Refined Products Dirty – negotiable

- 25 BRAND NEW 5161 Sugar Hoppers in Arkansas UP – negotiable

- 99 340W Pressure Cars various locations Butane and Propane dirty negotiable

- 100 73 ft 286 GRL riser less deck, center part for sale,

- 19 auto-max II automobile carrier racks – tri-49 for sale – negotiable

- 10 food grade stainless steel cars

- 20 20K Stainless cars in 3 locations in the south – negotiable

- 30 CPC 1232 25.5K C/I Pennsylvania NS clean negotiable

- 100-150 29K C/I 117J cars for lease. Dirty in Bakken crude and can be returned dirty.

- 100 29K C/I 1232 cars for lease. Dirty in Heavy Crude and can be returned dirty.

- 100 117Rs 29K clean last used in crude Washington State – price negotiable sale or lease

- 21 111s 29K tanks last in alcohol dirty on the CN in Wisconsin for lease price negotiable

- 100 111s of various volumes and locations last in fuel oil dirty price negotiable

- Various Hoppers for sale and lease 3000-5800 CF 263 and 286 multiple locations negotiable

- 45 Boxcars 60ft Plate F’s Located in Tenn CSX – Lease Negotiable

- 28 20K Veg oil cars for lease in Arkansas – Negotiable

- 100 3200 Covered Hoppers for sale price negotiable

- 100 Center beam Flats with risers 73ft in SD and Iowa for sale negotiable

Call PFL today to discuss your needs and our availability and market reach. Whether you are looking to lease cars, lease out cars, buy cars or sell cars call PFL today 239-390-2885

PFL offers turn-key solutions to maximize your profitability. Our goal is to provide a win/win scenario for all and we can handle virtually all of your railcar needs. Whether it’s loaded storage, empty storage, subleasing or leasing excess cars, filling orders for cars wanted, mobile railcar cleaning, blasting, mobile railcar repair, or scrapping at strategic partner sites, PFL will do its best to assist you. PFL also assists fleets and lessors with leases and sales and offers Total Fleet Evaluation Services. We will analyze your current leases, storage, and company objectives to draw up a plan of action. We will save Lessor and Lessee the headache and aggravation of navigating through this rapidly changing landscape.

PFL IS READY TO CLEAN CARS TODAY ON A MOBILE BASIS WE ARE CURRENTLY IN EAST TEXAS

Live Railcar Markets

| CAT | Type | Capacity | GRL | QTY | LOC | Class | Prev. Use | Offer | Note |

|---|