“Yesterday is not ours to recover, but tomorrow is ours to win or lose.” – Lyndon B. Johnson

Jobs Update

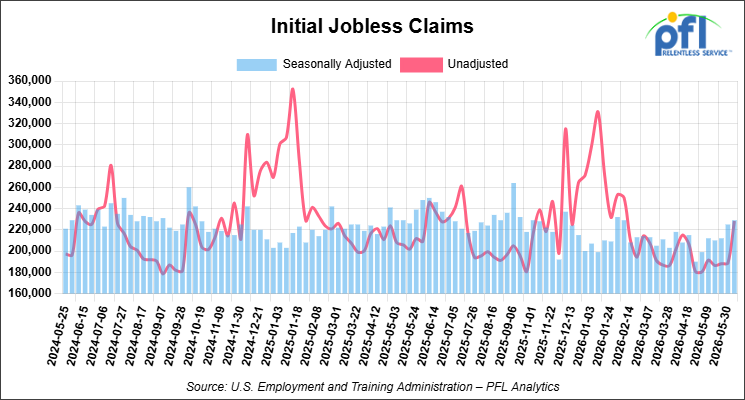

Initial jobless claims seasonally adjusted for the week ending June 6, 2026 came in at 229,000, versus the adjusted number of 225,000 people from the week prior, up 4,000 people week over week.

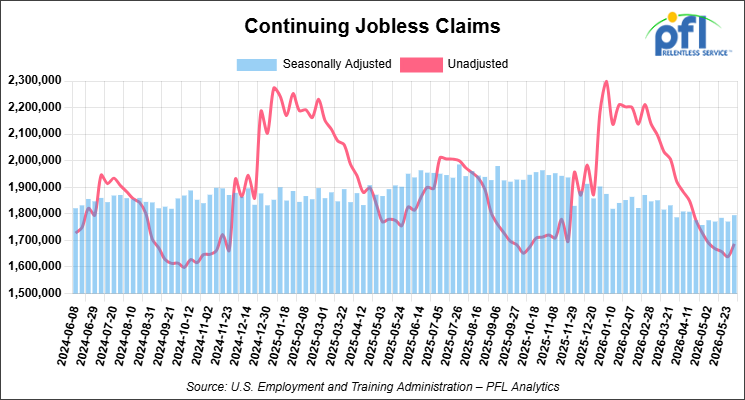

Continuing jobless claims came in at 1,795,000, versus the adjusted number of 1,771,000 people from the week prior, up 24,000 week-over-week.

Stocks closed higher on Friday of last week and higher week-over-week

The DOW closed higher on Friday of last week, up 353.51 points (0.70%), closing out the week at 51,202.26, up 335.48 points week-over-week. The S&P 500 closed higher on Friday of last week, up 37.16 points (0.50%), and closed out the week at 7,431.46, up 47.62 points week-over-week. The NASDAQ closed higher on Friday of last week, up 49.18 points (0.31%), and closed out the week at 25,888.81, up 179.38 points week-over-week.

In overnight trading, DOW futures traded higher and are expected to open at 52,021 this morning, up 416 points from Friday’s close.

Crude oil closed lower on Friday of last week and lower week-over-week

West Texas Intermediate (WTI) crude closed down -2.83 per barrel (-3.23%), to close at $84.88 on Friday of last week, and down $5.66 week-over-week. Brent crude closed down -3.05 per barrel (-3.37%), to close at $87.33, and down $5.76 week-over-week.

One Exchange WCS (Western Canadian Select) for July settled on Friday of last week at US$11.65 below the WTI-CMA (West Texas Intermediate – Calendar Month Average). The implied value was US$73.97 per barrel.

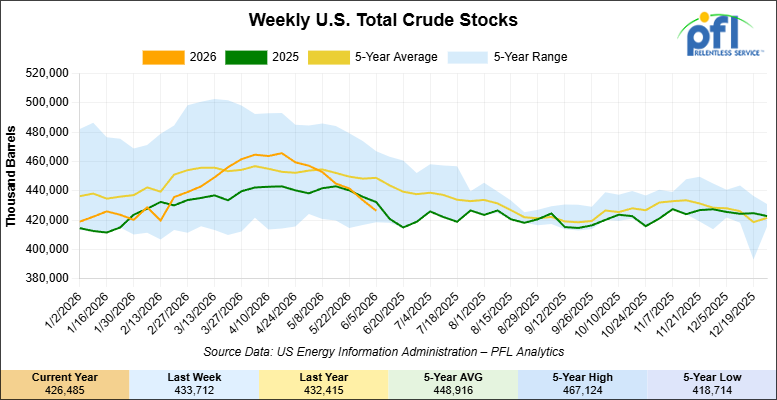

U.S. commercial crude oil inventories (excluding those in the Strategic Petroleum Reserve) decreased by 7.2 million barrels week-over-week. At 426.5 million barrels, U.S. crude oil inventories are 5% below the five-year average for this time of year.

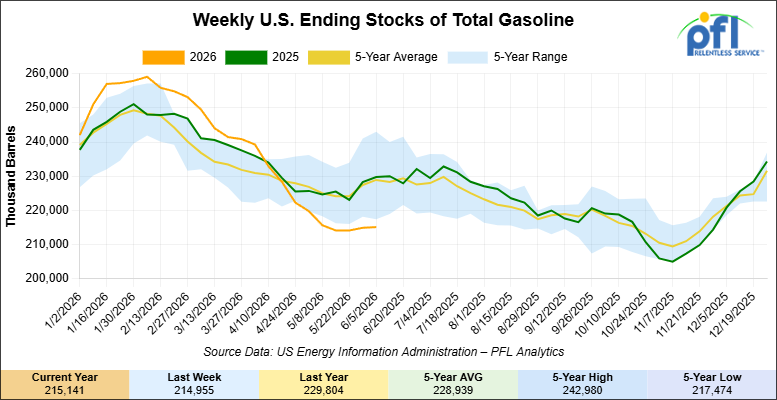

Total motor gasoline inventories increased by 200,000 barrels week-over-week and are 6% below the five-year average for this time of year.

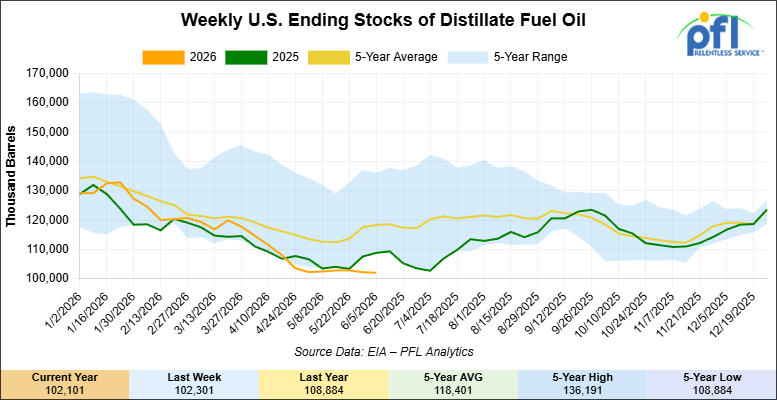

Distillate fuel inventories decreased by 200,000 barrels week-over-week and are 13% below the five-year average for this time of year.

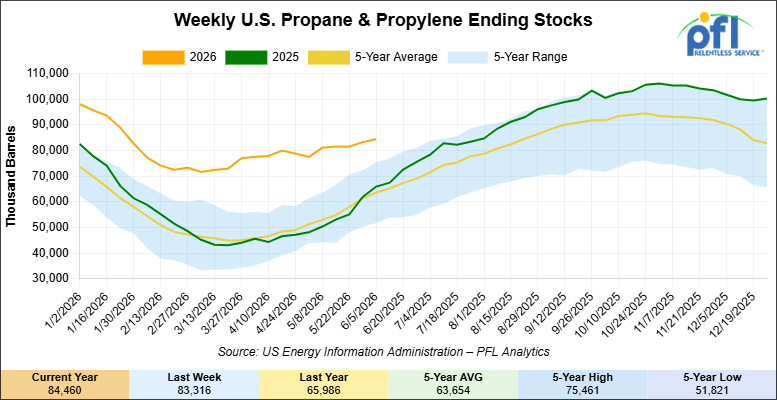

Propane/propylene inventories increased by 1.1 million barrels week-over-week and are 35% above the five-year average for this time of year.

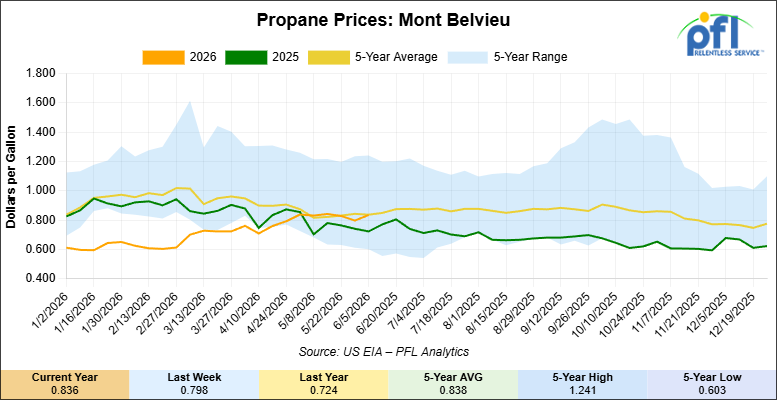

Propane prices closed at 83.6 cents per gallon on Friday of last week, up 3.8 cents per gallon week-over-week, and up 11.2 cents year-over-year.

Overall, total commercial petroleum inventories decreased by 5.6 million barrels week-over-week during the week ending June 5, 2026.

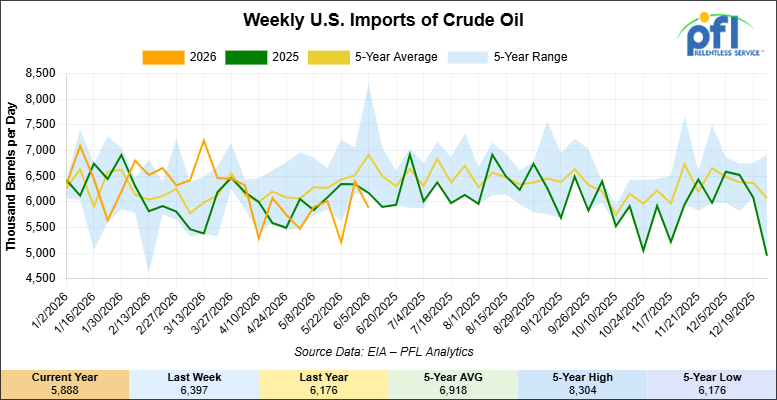

U.S. crude oil imports averaged 5.9 million barrels per day during the week ending June 5, 2026, a decrease of 0.5 million barrels per day week-over-week. Over the past four weeks, crude oil imports averaged 5.9 million barrels per day, 5.8% less than the same four-week period last year. Total motor gasoline imports (including both finished gasoline and gasoline blending components) averaged 714,000 barrels per day, and distillate fuel imports averaged 130,000 barrels per day during the week ending June 5, 2026.

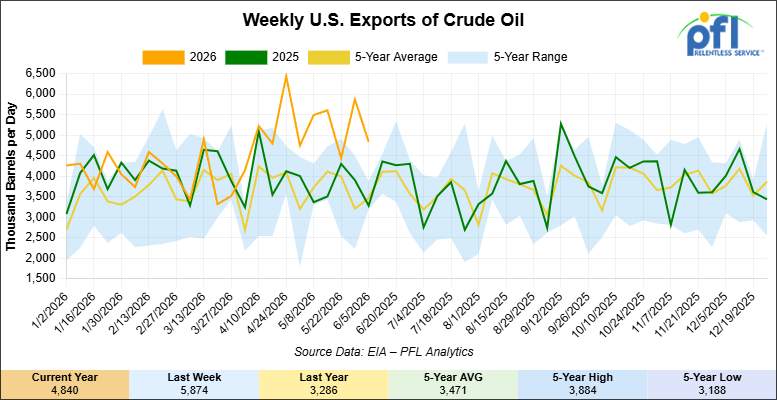

U.S. crude oil exports averaged 4.84 million barrels per day during the week ending June 5, 2026, a decrease of 1.034 million barrels per day week-over-week. Over the past four weeks, crude oil exports averaged 5.19 million barrels per day.

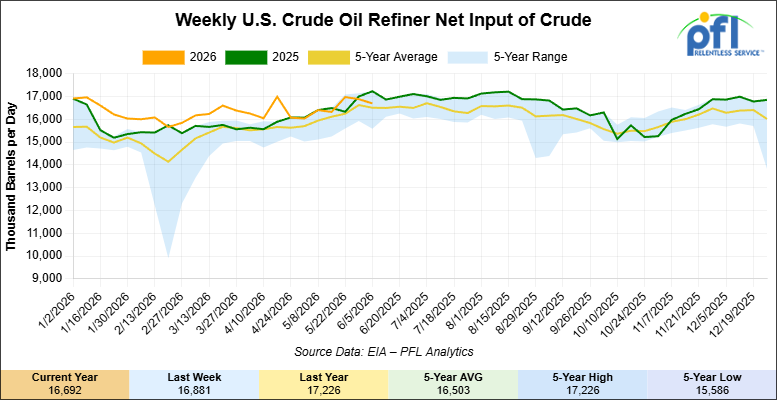

U.S. crude oil refinery inputs averaged 17 million barrels per day during the week ending June 5, 2026, which was 80,000 barrels per day more week-over-week.

WTI is poised to open at $80.15, down -$4.73 per barrel from Friday’s close.

North American Rail Traffic

Week Ending June 10, 2026:

Total North American weekly rail volumes were up (+7.56%) in week 24, compared with the same week last year. Total Carloads for the week ending June 10, 2026 were 331,687, up (+2.79%) compared with the same week in 2025, while weekly Intermodal volume was 354,205, up (+12.44%) year over year. 9 of the AAR’s 11 major traffic categories posted year-over-year increases. The largest decrease came from Coal (-7.69%). The largest increase was Metallic Ores and Metals (+14.54%).

In the East, CSX’s total volumes were up (+6.55%), with the largest decrease coming from Chemicals (-8.70%), while the largest increase came from Other (+20.47%). NS’s total volumes were up (+5.85%), with the largest increase coming from Petroleum & Petroleum Products (+14.64%), while the largest decrease came from Grain (-14.55%).

In the West, BNSF’s total volumes were up (+13.59%), with the largest increase coming from Coal (+55.26%), while the largest decrease came from Chemicals (-5.65%). UP’s total volumes were up (+5.64%), with the largest increase coming from Grain (+21.33%), while the largest decrease came from Coal (-26.68%).

In Canada, CN’s total volumes were up (+7.12%), with the largest increase coming from Coal (+55.26%), while the largest decrease came from Nonmetallic Minerals (-11.07%). CPKCS’s total volumes were down (-0.60%), with the largest increase coming from Metallic Ores and Metals (+36.42%), while the largest decrease came from Coal (-42.16%).

Source Data: AAR – PFL Analytics

North American Rig Count Summary

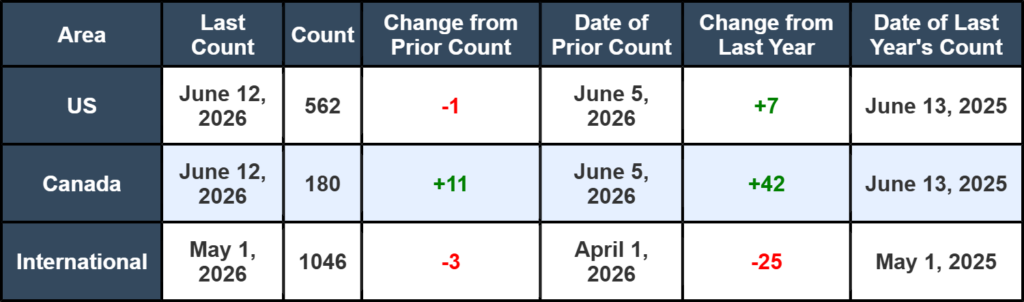

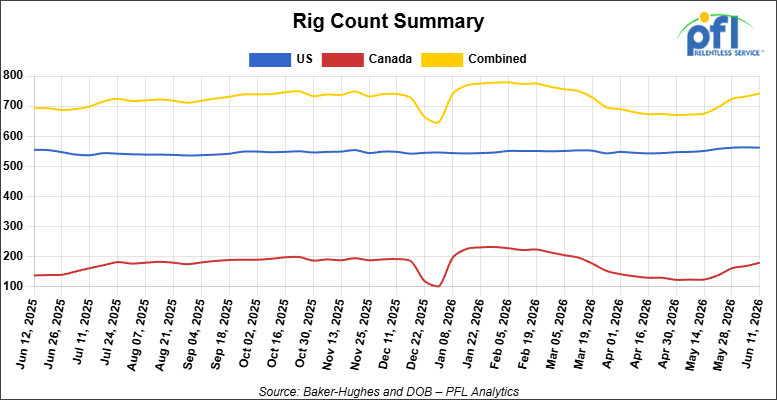

North American rig count was up by +10 rigs week-over-week. The US rig count was down by -1 rig week-over-week, but up by +7 rigs year-over-year. The US currently has 562 active rigs. Canada’s rig count was up by +11 rigs week-over-week and up by +42 rigs year-over-year. Canada currently has 180 active rigs. Overall, year-over-year we are up by +49 rigs collectively.

We are watching a few things out there for you:

We Are Watching Petroleum Carloads

The four-week rolling average of petroleum carloads carried on the six largest North American railroads fell to 29,424 from 29,665 which was an decrease of -241 rail cars week-over-week. Canadian volumes were lower. CN’s shipments were lower by -8.0% week-over-week, CPKC’s volumes were lower by -1.0% week-over-week. U.S. shipments were mostly higher. The BNSFwas the sole decliner and was down by -1.0%. The UP had the largest percentage increase and was up by +7.0% week-over-week.

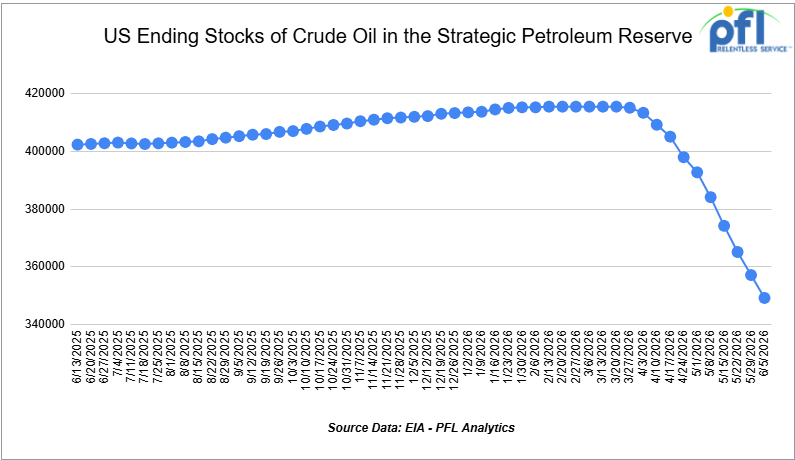

We Continue to Watch Our Strategic Petroleum Reserves

The ongoing emergency drawdown of the U.S. Strategic Petroleum Reserve (SPR) remains a major component of global efforts to offset crude oil supply disruptions stemming from the conflict involving Iran and the continued restrictions on oil shipments through the Strait of Hormuz. Since March, the Department of Energy (DOE) has awarded exchanges covering more than 80 million barrels of crude oil, with additional releases expected as part of a broader international response coordinated through the International Energy Agency (IEA).

The United States committed to making up to 172 million barrels available from the SPR under the IEA’s collective plan to inject roughly 400 million barrels into global energy markets. Officials have argued that the releases are necessary to help stabilize crude supplies and limit further increases in fuel prices as refiners compete for replacement barrels amid ongoing transportation disruptions.

As releases have accelerated, inventories in the SPR have declined to 349.112 million barrels, down sharply from levels above 450 million barrels earlier this year and reaching their lowest level since January 2024. Recent weekly withdrawals have ranked among the largest on record, highlighting the scale of the government’s intervention in oil markets. On average, since the war started with Iran, the United States has withdrawn approximately 1.05 million barrels per day from the SPR through the week ending June 5, 2026.

Global petroleum inventories have also tightened considerably. The IEA has reported substantial draws in commercial crude and refined-product stockpiles across major consuming nations, underscoring the strain that the conflict has placed on world energy markets. Agency officials have indicated that further coordinated actions remain possible should supply disruptions persist or intensify.

The Administration continues to emphasize that the current program consists primarily of exchange agreements, rather than outright sales. Under these arrangements, companies receiving crude oil today are required to return the borrowed barrels in the future along with additional volumes as a premium. Energy Secretary Chris Wright has stated that the objective is to eventually restore the SPR to levels above those that existed prior to the current emergency releases.

Meanwhile, energy prices remain elevated compared with pre-conflict levels, keeping fuel costs a focus for consumers, businesses, and policymakers alike. Market participants continue to monitor developments in the Middle East, future IEA actions, and the pace of SPR releases as key factors influencing oil prices through the remainder of the year.

We Are Watching Canada

Canada is officially in a technical recession. Two consecutive quarters of negative GDP growth. Right now, a CPKC signals strike is active, three major labor contracts expire in the next 18 months, and Vancouver is running out of container capacity. The timing of this could not be worse.

A Journal of Commerce and S&P Global webinar last week that PFL participated in highlighted these realities, How Policy and Ports Are Shaping the Freight Future, laid out the state of Canada’s freight infrastructure in detail. The data is worth paying attention to, as well as the backdrop it was presented against.

Freight is still moving, and that is the surprising part. Vancouver set a container volume record in 2025 and is up another 5% this year. Prince Rupert is up 11%. The ports are busy, however, busy and healthy are two different things, and the gap between them is getting harder to ignore. Vancouver will need additional container handling capacity by 2029. The next major expansion, Roberts Bank Terminal 2, does not open until the mid-2030s. That is a long runway with no room for error.

The labor picture is the most immediate concern and the CN is the one to watch most closely. CN engineers and conductors reach contract expiry December 31, 2026. CPKC’s follow at the end of 2027. The longshore agreement at Vancouver and Prince Rupert expires March 2027. Canada has had three significant rail and port work stoppages in the last three years — and each time, freight that diverted did not fully come back. But, here is the detail that sharpens the risk: Prince Rupert is sole-served by CN. If CN goes on strike, Prince Rupert goes dark entirely, Canada’s closest port to Asia, up 11% year to date, shuts down completely. A recession puts workers and management in a harder negotiating position, not an easier one.

Tariffs are quietly reshaping the whole system, and it has been happening longer than most people realize. The mix of Canada/U.S. freight moving through Vancouver has already fallen from roughly 25% in 2010 to 8% today. With U.S. trade relationships under further strain from tariffs, Canadian shippers are now actively accelerating that shift toward Asia and Europe. National container demand is forecast to grow from 6.9 million TEUs in 2025 to 10.2 million TEUs by 2040. That freight has to move somewhere, and if even a fraction of it redirects away from the U.S., East Coast ports face a 33% volume increase before Montreal’s Contrecoeur expansion is ready. Montreal is projected to operate above capacity between 2026 and 2029 if trade diversification materializes. That bottleneck is not getting much attention yet, but it should be. Rail is central to all of it, every container moving through Vancouver or Prince Rupert moves by CN or CPKC rail to get there.

And then there is the UP-NS merger sitting in the background. If it closes, a BNSF-CSX merger is widely expected to follow. North American rail consolidation does not stop at the U.S. border, and Canadian carriers know it.

Canada’s freight network is not broken but it is carrying more weight than it was built for, at a moment when the economy is contracting, labor agreements are stacking up, and the political environment on both sides of the border is unpredictable. That is a combination worth watching closely. Stay tuned to PFL for further updates.

We Are Watching Alberta

PFL attended Alberta Premier Danielle Smith’s dinner event in Calgary on Friday June 5th and she announced to a crowd of 2,000 that Alberta is targeting to export 8 million barrels of oil production per day by 2035. That is double what the province exports today. She repeated those comments before the Global Energy Show in Calgary last week.

The timing of the announcement is not a coincidence. The Iran conflict has accelerated the global search for stable, reliable oil supply. Asia’s need energy, and they need a supplier they can count on. Smith’s message was direct: global demand for oil and gas is not going away, Canada has what the world needs, and the only question is whether left wing Ottawa can get out of the way fast enough to let Alberta produce it.

The political environment seems to be moving in the right direction. Trump signed the Bridger Pipeline permit in April. The Canada-Alberta MOU is in place but weak – producers do not like the carbon tax. We will see if all this talk leads to shovels in the ground. Smith has been pushing and the world’s energy needs are now making the argument for her.

But, pipelines take years to build, 8 million barrels per day needs egress that does not yet exist. Trans Mountain hit full capacity at 890,000 barrels per day. Enbridge Mainline is apportioned. Every major pipeline corridor out of Alberta is running at or near its limit right now. Going from 4 million to 8 million barrels per day means finding takeaway capacity for an additional 4 million barrels every single day. No single pipeline solves that. A combination of new pipelines expanded existing capacity, and sustained crude-by-rail seem to be all required.

Rail is the most responsive part of that equation. PFL will continue to watch this one as the basis widens between WCS and WTI and it will. We will see if and when producers are ready to lock into long term leases and long term class one service. Understandably everyone is a little gun shy with the last crude by rail crash leaving the producer with huge costs of having to store cars and very expensive return on lease car returns.

We Are Watching Tank Cars

New tank car orders have been running well below the fleet replacement rate, on the order of 20,000 cars a year, and the industry backlog has fallen from roughly 61,000 cars in late 2022 to about 26,000. At the Wells Fargo Industrials and Materials Conference last Tuesday, lessors made clear that the slide has not reversed. Customers are choosing to hold and re-lease the cars they already have rather than commit to new builds while tariff costs and trade terms remain unsettled.

The reason that calculus has shifted sits in the Section 232 schedule. The order carries a 25% tariff on imported tank cars and a 25% tariff on a broad list of rail componentry, including couplers, axles, air brakes and wheels, layered on top of the standing 50% duty on steel and aluminum and a 50% tariff on rail itself. Adding a tariff premium to both the finished car and its key components, widens the gap between ordering new equipment and keeping a serviceable car in the rotation.

Tank cars landed on the Section 232 list in April after Senator Bill Cassidy pressed the administration to include them, framing the move as protection for Union Tank Car’s plant in Alexandria, Louisiana, the last facility still building tank cars in the United States, and the roughly 350 jobs tied to it. Not everyone in the build chain wanted the inclusion: Greenbrier objected that the duties raise its domestic steel costs while rivals that shifted tank car production to Mexico sell freely into the U.S. market, and Nucor sought to pull tank car codes off the list entirely.

For PFL’s customers, the practical question is no longer whether to chase new builds, it is how to get the most out of the existing fleet. Leasing companies and car owners are holding the line on five-year commitments, the supply of 117J crude cars remains thin, and the tariff premium now sitting on every new car and component only sharpens the case for refurbishment, re-marking and disciplined lease management. Stay tuned to PFL for further updates.

We Continue to Watch the UP and NS

The Surface Transportation Board accepted Union Pacific and Norfolk Southern’s revised merger application as complete on May 28, then immediately held the proceeding in abeyance. The Board ordered the applicants to file supplemental information by July 27th and required a full environmental impact statement before substantive review begins. The headline reads as forward motion, but the multi-year review clock still has not started.

The Board found the revised filing still unclear in material respects, which is why it declined to set a procedural schedule and instead sent the applicants back for more detail. BNSF, Canadian National, Canadian Pacific Kansas City and CSX all remain on record against the deal, with CSX adding its opposition earlier in the spring.

The July 27th filing and the environmental review push any decision well into the future, which leaves shippers with corridor or interchange exposure a continued window to file notices of intent to participate and document where the combined network would touch their movements. PFL is working with clients on exactly that mapping, and we will keep watching the docket as the supplemental filing comes due.

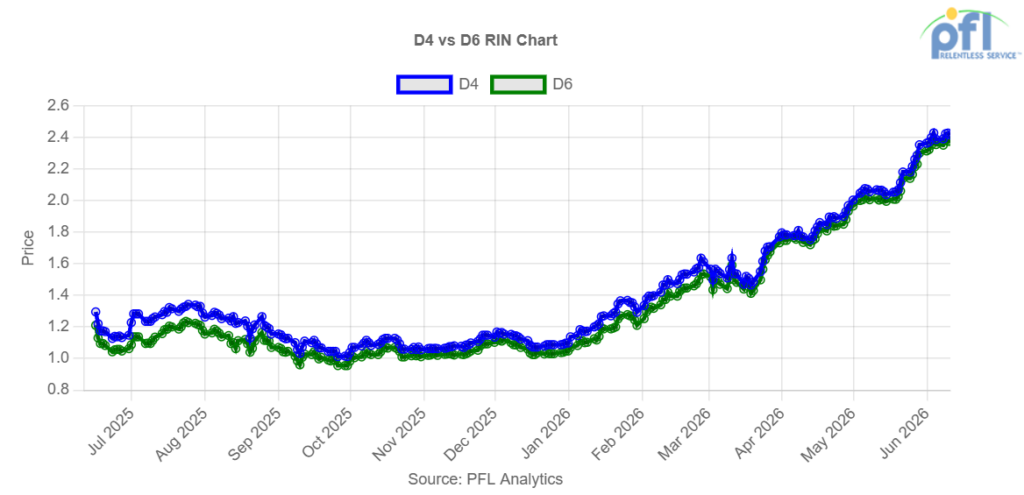

We continue to watch RINs

D4 RINs closed out the day, and the week, on Friday of last week, at $2.42 per RIN, up 1 cent per RIN day-over-day, and up 3 cents per RIN week-over-week. D6 RINs closed at $2.38 per RIN, up 1 cent per RIN day-over-day, and up 4 and ½ cents per RIN week-over-week.

Both vintages are within reach of the record highs set in 2021, according to data the EIA published last week. Both credits have roughly doubled in value since the start of the year.

The move traces back to the higher Renewable Fuel Standard volumes finalized in March, which set obligations well above 2025 levels and pulled RIN prices up to reflect the requirements obligated parties need to hit. Because a gallon of biodiesel or renewable diesel generates 1.5 to 1.7 RINs, those fuels are now throwing off more than $3.50 a gallon in credits, while a gallon of ethanol generates one.

For the rail side, the read is straightforward. Ethanol moves almost entirely in tank cars, and the dominant renewable diesel feedstocks, soybean oil and other vegetable oils, are heavy tank car commodities as well. Mandate-driven RIN strength of this size is a clear pull on ethanol and vegetable-oil car demand, and it lands while plants that idled in 2025 are restarting. PFL helps shippers position ethanol and feedstock fleets against exactly this kind of demand signal.

We are Watching Economic Indicators

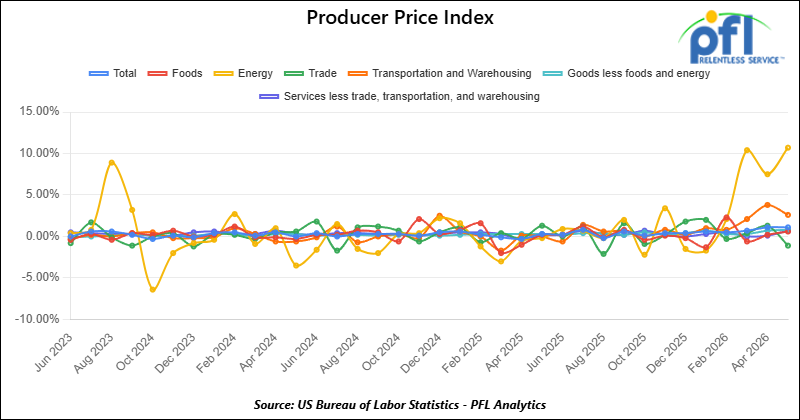

Producer Price Index

In May 2026, the Producer Price Index (PPI) for final demand rose 1.1% month-over-month, following a 1.4% increase in April and reflecting a significant acceleration in upstream price pressures driven largely by energy costs. Core PPI (final demand less foods and energy) increased 0.8% month over month, the strongest gain since 2022, indicating that inflation pressures broadened beyond energy-related categories. The monthly increase was driven by both goods and services. Within goods, energy prices surged sharply amid disruptions to global oil markets, while food prices also increased modestly. Core goods prices rose as higher transportation, chemical, and industrial input costs filtered through supply chains. Within services, transportation and warehousing remained a major source of inflationary pressure, while trade margins also increased, suggesting businesses continued to pass higher costs through to customers.

In May 2026, the Consumer Price Index (CPI) increased 0.5% month-over-month, slowing slightly from April’s 0.6% gain, and was up 4.2% year over year. Core CPI (all items less food and energy) rose 0.2% month-over-month and was up 2.9% year-over-year. Energy prices remained the primary driver of headline inflation, accounting for more than 60% of the monthly increase as gasoline and other fuel costs continued to climb. Shelter also increased and remained a significant contributor to inflation, while food prices rose modestly. Despite elevated headline inflation, core inflation remained comparatively contained, suggesting that much of the recent inflationary pressure continued to stem from energy-related factors.

Lease Bids

- 100, 21.9K 117J Tanks located off of All Class 1s in the Midwest. For use in CO2 service. Period: 6 months.

- 30-50, 30K 117J Tanks located off of NS or CSX in the Northeast. For use in C5 service. Period: 1 year.

- 20-50, 4000-5000 Covered Hoppers located off of UP or BNSF in Houston. For use in Urea, Potash, and Ammonium Sulfate service. Period: 6-12 Months.

- 200, 33K Pressure Tanks located off of CSX or NS in Ohio. For use in Propylene service. Period: 18 Months.

- 30-50, 25.5K DOT 111 Tanks located off of All Class 1s in various locations. For use in Asphalt service. Period: 1-3 Years.

- 40, 33K Pressure Tanks located off of UP in Eunice, LA. For use in Propane service. Period: 1 Year.

- 40, 29K DOT 111 Tanks located off of UP or BNSF in the Midwest. For use in Veg Oil service. Period: 5 Year.

- 70, 30K DOT 117 Tanks located off of NS or CSX in Ohio. For use in Diesel service. Period: 3 months.

- 20, DOT 117J Tanks located off of NS, CSX, CN, or CPKC in various locations. For use in C5 service. Period: 1 year. Need gauge rods.

- 300, 5200CF Covered Hoppers located off of CP or CM in Canada. For use in Petcoke service. Period: 3 Year.

- 10, 30K 117J Tanks located off of BNSF in Canada. For use in Propane or Butane service. Period: 3 Year.

- 20, 28K or larger 117J Tanks located off of BNSF or UP in California. For use in Crude service. Period: 6 months.

- 75, 30K 117 Tanks located off of NS in Ohio. For use in Condensate service. Period: 6-12 Months. Mag Rods Not Needed.

- 100, 28.3K DOT 111 or 117 Tanks located off of CP or CN in Canada. For use in VGO service. Period: 1-3 Years.

- 5, 28.3K DOT 111 or 117 Tanks located off of CN in Canada. For use in Bitumen service. Period: Trip Lease.

Sales Bids

- 28, 3400CF Covered Hoppers located off of UP or BNSF in Texas. For use in Cement service. Cement Gates needed.

- 20, 17K DOT111 Tanks located off of various class 1s in various locations. For use in corn syrup service.

- 120, Various Open-Top Aluminum Rotary Gondolas located off of various class 1s in various locations. For use in Sulphur service. Built 2004 or later.

Lease Offers

- 21, 6351 Covered Hoppers located off of CN in Wisconsin. Last used in DDG. Available until February 2027.

- 29, 6500 Covered Hoppers located off of CN in Wisconsin. Last used in DDG. Available until February 2027.

- 50, 20K DOT117J Tanks located off of all class 1s in Moving. Last used in styrene.

- 29, 25.5K DOT117J Tanks located off of UP or BNSF in Texas. Cars are currently clean.

- 200, 340W DOT 112J Tanks located off of all class 1s in Multiple Locations. Last used in propane and butane. Cars are currently clean.

- 15, 6200CF Covered Hoppers located off of all class 1s in Wisconsin. Last used in plastic. Cars are currently clean.

- 30, 6500CF Covered Hoppers located off of all class 1s in Wisconsin. Last used in plastic. Cars are currently clean.

- 6, 21K Stainless Steel Tanks located off of UP in Texas / Mexico Border. Last used in surfactant. Cars are currently clean.

- 100, 28.4K DOT 117J Tanks located off of UP or BNSF in Beaumont, TX. Cars are currently clean.

- 50, 30K DOT117J Tanks located off of UP or BNSF in the South. Last used in ethanol.

- 30, 30K DOT 117R Tanks located off of BNSF in Washington. Last used in renewable jet fuel.

- 80, 30K DOT 117R Tanks located off of BNSF in Washington. Last used in renewable diesel.

- 10, 30K DOT 117R Tanks located off of BNSF in Washington. Last used in renewable naphtha.

- 10, 29K DOT 117R Tanks located off of BNSF and UP in Texas. Last used in gasoline additive. Coiled and Insulated.

- 39, 31K CPC1232 Tanks located off of All Class 1s in Iowa. Last used in diesel.

- 99, 31K CPC1232 Tanks located off of BNSF and UP in Texas. Last used in diesel.

- 1, 31K CPC1232 Tanks located off of BNSF and UP in Texas. Last used in naphtha.

- 2, 30K DOT 117R Tanks located off of BNSF and UP in Texas. Last used in giesel.

- 1, 30K DOT 117R Tanks located off of BNSF and UP in Texas. Last used in gas blend stock.

- 3, 30K DOT 117R Tanks located off of BNSF and UP in Texas. Last used in gasoline.

- 36, 31K CPC1232 Tanks located off of CPKC in Texas. Last used in diesel.

- 6, 31K CPC1232 Tanks located off of CPKC in Texas. Last used in naphtha.

Sales Offers

- 81, 31.8K CPC1232 Tanks located off of UP or BNSF in TX. Last used in Multiple Services. Requal Due in 2025.

- 35, 3400CF Covered Hoppers located off of UP or BNSF in the Midwest. Last used in Sand.

- 25, 30K 117J Tanks located off of CSX in Jackson, TN. Last used in Fuels. Newly Requalified.

Call PFL today to discuss your needs and our availability and market reach. Whether you are looking to lease cars, lease out cars, buy cars, or sell cars call PFL today at 239-390-2885

Live Railcar Markets

| CAT | Type | Capacity | GRL | QTY | LOC | Class | Prev. Use | Offer | Note |

|---|

PFL will be at the Following Conferences

- Where: Calgary

- Attending: David Cohen (954-729-4774), Curtis Chandler(239-405-3365), Cyndi Popov (403-402-5043)

- Where: Grand Geneva Resort

- Attending: Brian Baker (239.297.4519)

- Conference Website