“You can’t cross the sea merely by standing and staring at the water.” – Rabindranath Tagore

Jobs Update

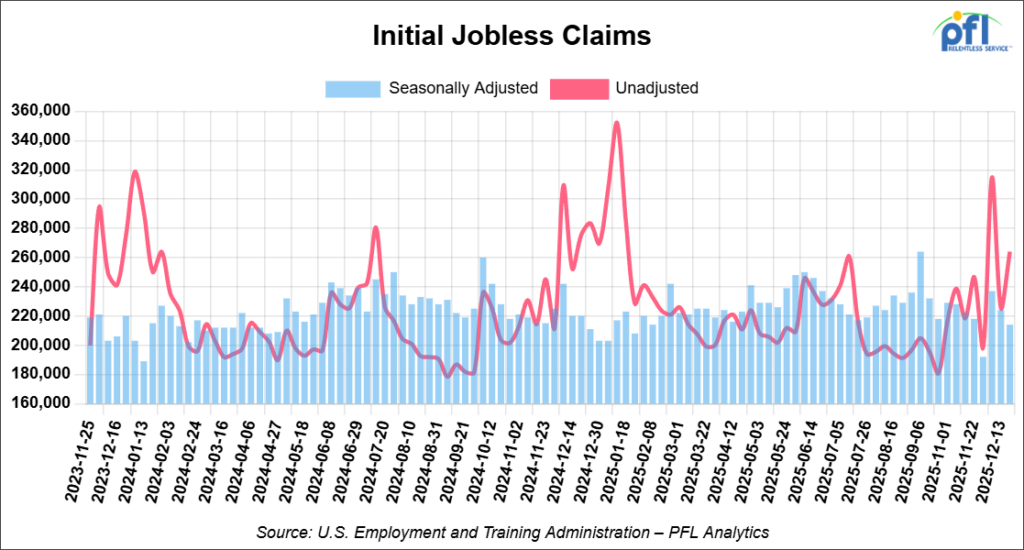

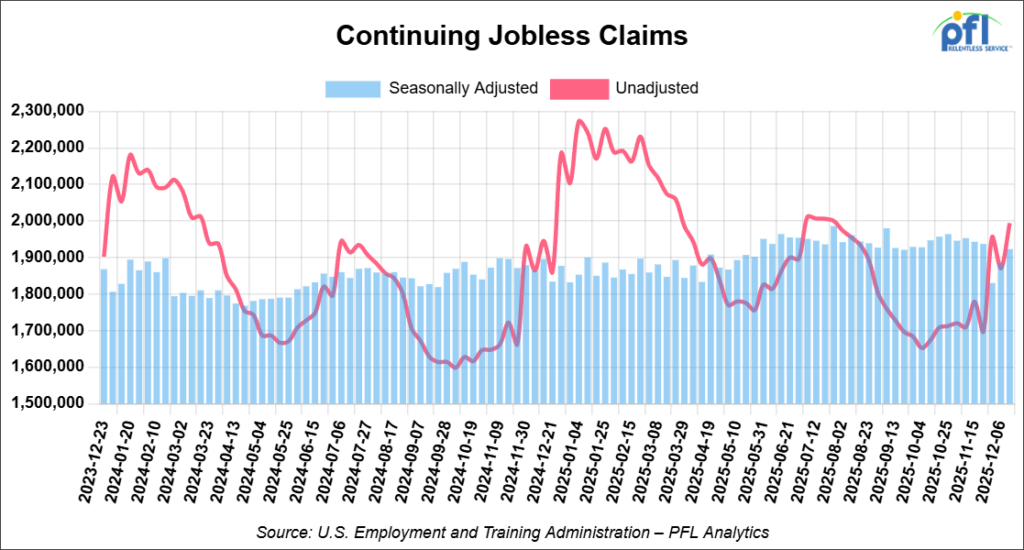

- Initial jobless claims seasonally adjusted for the week ending December 24, 2025 came in at 214,000, versus the adjusted number of 224,000 people from the week prior, down 10,000 people week-over-week.

- Continuing jobless claims came in at 1,923,000, versus the adjusted number of 1,885,000 people from the week prior, up 38,000 week-over-week.

Stocks closed lower on Friday of last week, but higher week-over-week

The DOW closed lower on Friday of last week, down -20.19 points (-0.04%), closing out the week at 48,710.97, up 576.39 points week-over-week. The S&P 500 closed lower on Friday of last week, down -2.11 points (-0.03%), and closed out the week at 6,929.94, up 95.23 points week-over-week. The NASDAQ closed lower on Friday of last week, down -20.21 points (-0.09%), and closed out the week at 23,593.10, up 285.48 points week-over-week.

In overnight trading, DOW futures traded lower and are expected to open at 48,995 this morning, down -3 points from Friday’s close.

Crude oil closed lower on Friday of last week, but higher week-over-week

West Texas Intermediate (WTI) crude closed down -1.61 per barrel (-2.8%), to close at $56.74 on Friday of last week, but up 8 cents week-over-week. Brent crude closed down -1.60 per barrel (-2.6%), to close at $60.64, but up 17 cents week-over-week.

One Exchange WCS (Western Canadian Select) for February delivery settled on Wednesday of last week at US$13.50 (markets were closed Thursday and Friday for Christmas and Boxing Day in Canada last week) below the WTI-CMA (West Texas Intermediate – Calendar Month Average). The implied value with WTI closing at $56.74 on Friday of last week would put WSC at US$43.24 per barrel.

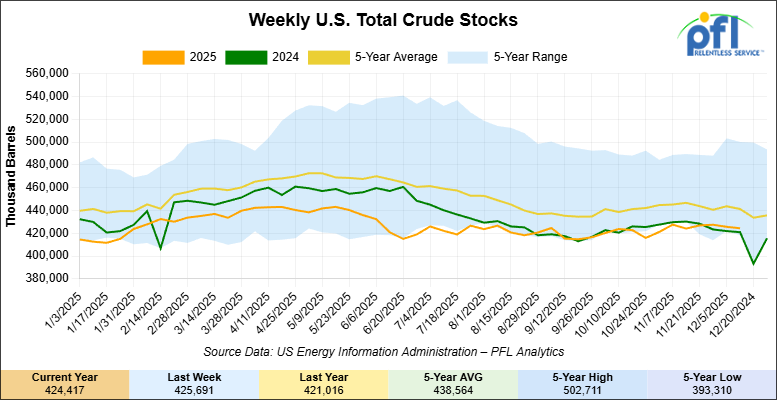

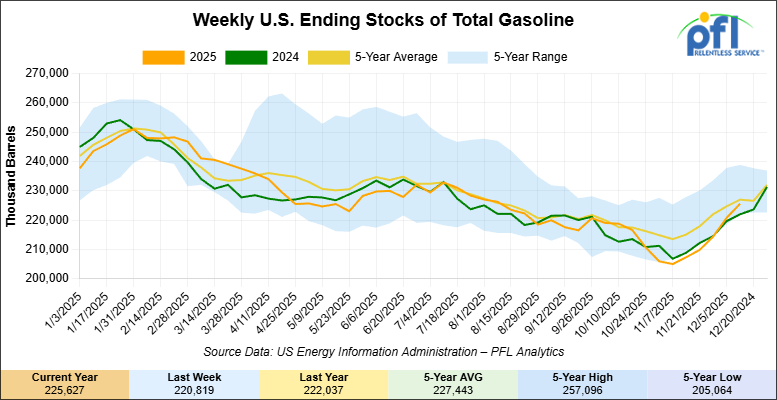

Please Note Closing Stocks are for the week ending December 12, 2025 – Next EPA Data Release is 12/31

U.S. commercial crude oil inventories (excluding those in the Strategic Petroleum Reserve) decreased by 1.3 million barrels week-over-week. At 424.4 million barrels, U.S. crude oil inventories are 4% below the five-year average for this time of year.

Total motor gasoline inventories increased by 4.8 million barrels week-over-week and are slightly below the five-year average for this time of year.

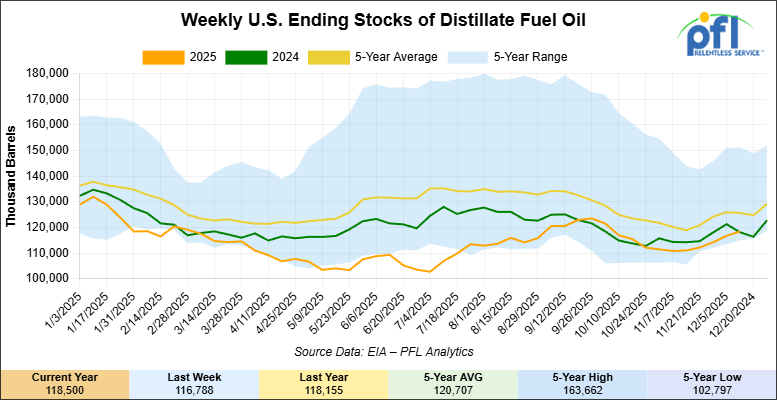

Distillate fuel inventories increased by 1.7 million barrels week-over-week and are 6% below the five-year average for this time of year.

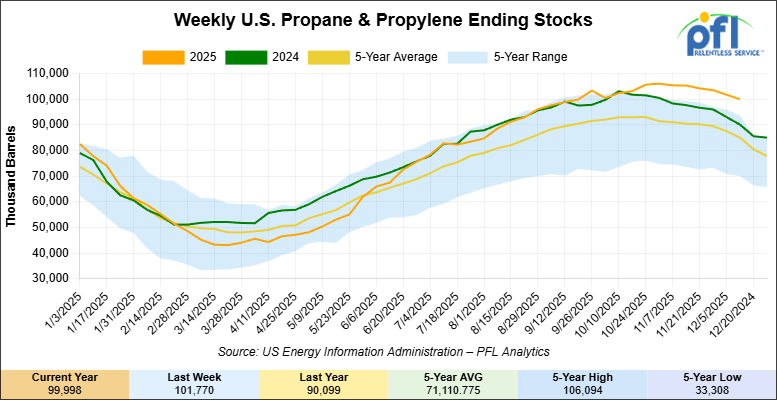

Propane/propylene inventories decreased 1.8 million barrels week-over-week and are 17% above the five-year average for this time of year.

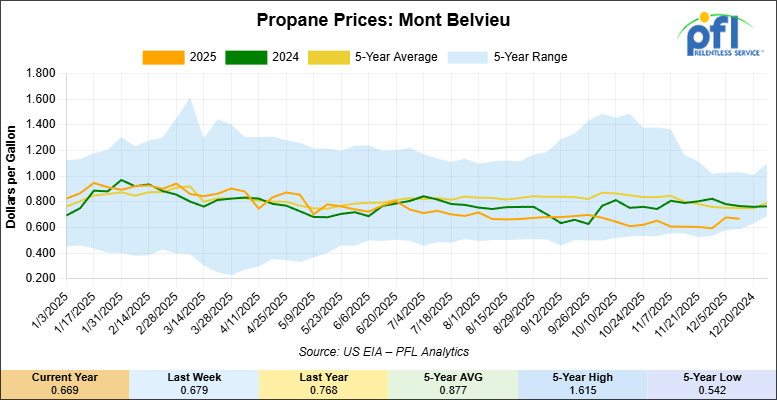

Propane prices closed at 66.9 cents per gallon on Friday of last week, down 1 cent per gallon week-over-week, and down 9.9 cents per gallon year-over-year.

Overall, total commercial petroleum inventories increased by 2.1 million barrels week-over-week during the week ending December 12, 2025.

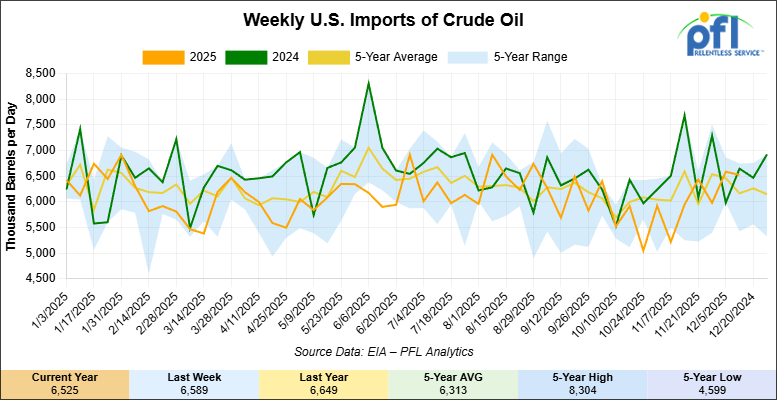

U.S. crude oil imports averaged 6.5 million barrels per day during the week ending December 12, 2025, a decrease of 64,000 barrels per day week-over-week. Over the past four weeks, crude oil imports averaged 6.4 million barrels per day, 1.8% less than the same four-week period last year. Total motor gasoline imports (including both finished gasoline and gasoline blending components) averaged 834,000 barrels per day, and distillate fuel imports averaged 268,000 barrels per day during the week ending December 12, 2025.

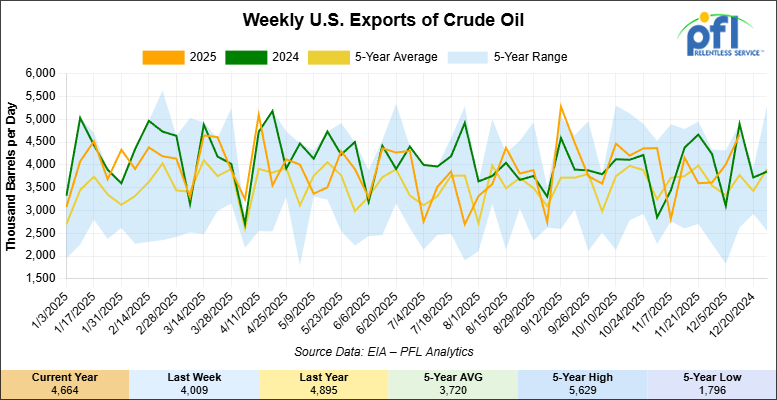

U.S. crude oil exports averaged 4.664 million barrels per day during the week ending December 12, 2025, an increase of 655,000 barrels per day week-over-week. Over the past four weeks, crude oil exports averaged 3.971 million barrels per day.

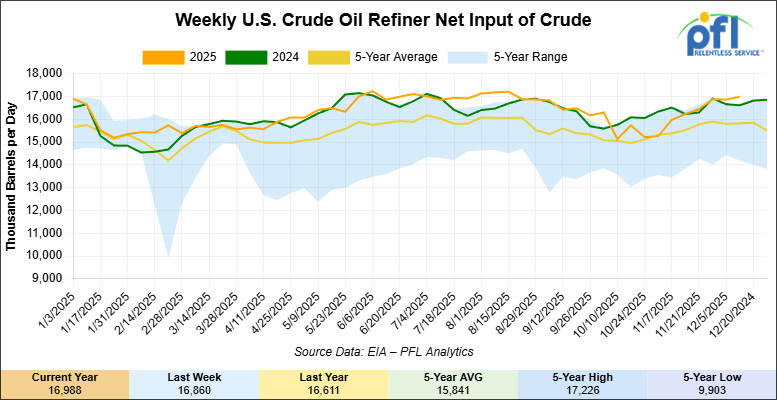

U.S. crude oil refinery inputs averaged 17 million barrels per day during the week ending December 12, 2025, which was 129,000 barrels per day more week-over-week.

WTI futures are poised to open at $57.97, up $1.23 from Friday’s close.

North American Rail Traffic

Week Ending December 17, 2025:

Total North American weekly rail volumes were down (-2.93%) in week 51, compared with the same week last year. Total Carloads for the week ending December 17, 2025 were 318,120, down (-2.73%) compared with the same week in 2024, while weekly Intermodal volume was 356,352, down (-3.10%) year over year. 9 of the AAR’s 11 major traffic categories posted year-over-year decreases. The largest decrease came from Forest Products (-19.12%), while the largest increase was Coal (+9.63%).

In the East, CSX’s total volumes were up (+1.76%), with the largest decrease coming from Metallic Ores and Metals (-17.47%), while the largest increase came from Intermodal Units (+8.04%). NS’s total volumes were down (-0.19%), with the largest increase coming from Petroleum & Petroleum Products (+25.32%), while the largest decrease came from Grain (-26.65%).

In the West, BNSF’s total volumes were down (-2.47%), with the largest increase coming from Other (+9.65%), while the largest decrease came from Metallic Ores and Metals (-24.33%). UP’s total volumes were down (-4.52%), with the largest increase coming from Coal (+22.13%), while the largest decrease came from Grain (-20.06%).

In Canada, CN’s total volumes were down (-4.34%), with the largest increase coming from Other (+134.27%), while the largest decrease came from Chemicals (-16.71%). CPKC’s total volumes were down (-22.63%), with the largest increase coming from Coal (+14.06%), while the largest decrease came from Forest Products (-65.33%).

Source Data: AAR – PFL Analytics

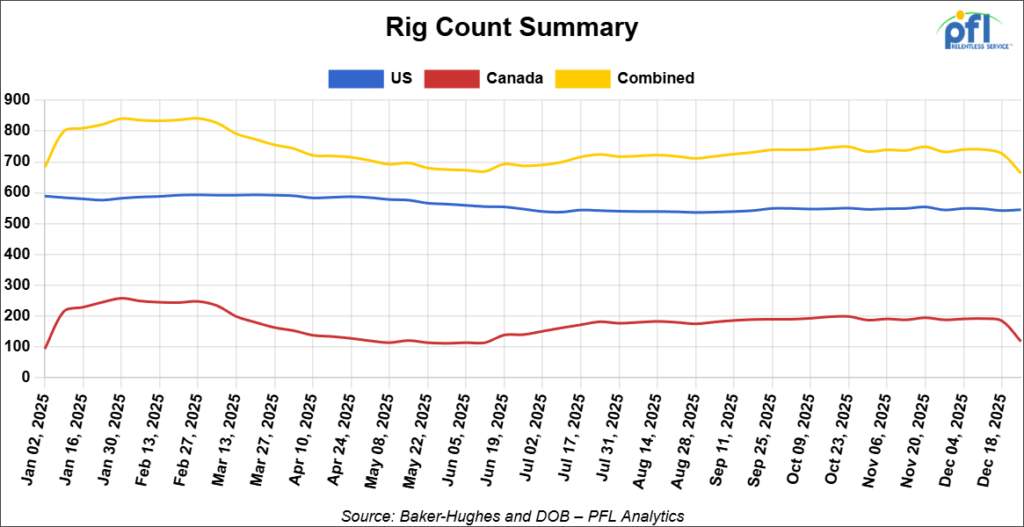

North American Rig Count Summary

Rig Count

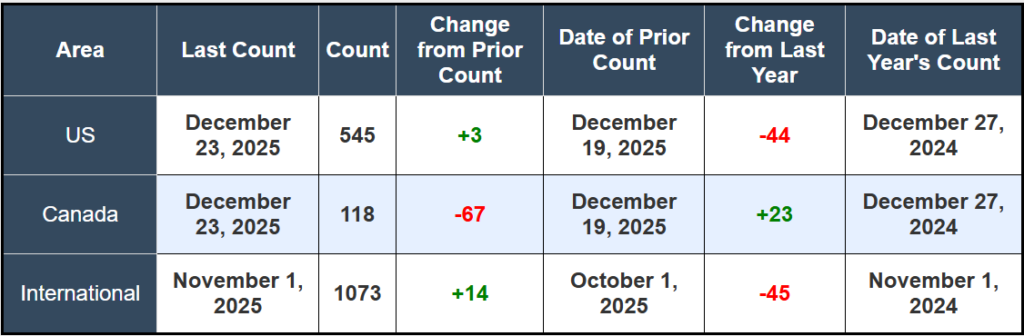

North American rig count was down by -64 rigs week-over-week. The US rig count was up by +3 rigs week-over-week, and down by -44 rigs year-over-year. The US currently has 545 active rigs. Canada’s rig count was down by -67 rigs week-over-week and up by +23 rigs year-over-year. Canada currently has 118 active rigs. Overall, year-over-year we are down by -21 rigs collectively.

We are watching a few things out there for you:

PFL was watching the CSX and the CPKC’s Holiday Trains

We hope that everyone had a fantastic Christmas!

As the year winds down, rail talk quickly turned to inventories, storage, and what Q1 might bring. Before that reset fully sets in, two long-running holiday train programs wrapped up their 2025 runs, a reminder that rail has always been about more than freight.

Different in scale and style, both programs put a human face on the network and the communities railroads continue to serve.

Canadian Pacific Kansas City Holiday Train

The CPKC Holiday Train finished its late-December run across the U.S. and Canada, closing out another multi-week tour through Midwest towns and major rail hubs. Since launching in 1999, the program has become a familiar year-end moment in many communities, one that blends rail visibility with local giving.

Source: CKPC – PFL Analytics

2025 Holiday Train – by the numbers

- Raised over $2 million for food banks

- Collected more than 175,000 pounds of food

- Made stops across dozens of U.S. and Canadian communities

Across the upper midwest, people line the tracks, kids climb onto shoulders, donations are handed over, concerts are enjoyed by stage car, and for a few minutes rail becomes something personal rather than something that simply passes through town. Behind the scenes, it’s also a reminder of what rail workers know well: getting anything done reliably in December still takes planning, coordination, and a lot of people showing up in tough winter conditions.

CSX Transportation Santa Train

Further east, CSX marked another season of a very different tradition. The CSX Santa Train, now more than 80 years old, once again ran through Appalachia, serving communities along a defined corridor in Kentucky, southwest Virginia, and Tennessee.

2025 Santa Train – by the numbers

- Covered a 110-mile route

- Distributed more than 15 tons of gifts

- Reached dozens of Appalachian communities along the line

There’s no stage car or concert involved here. The Santa Train is about continuity. Employees, volunteers, and partners return to the same towns year after year, many with deep, multi-generation ties to the railroad. For many communities, the Santa Train isn’t a special event, it’s simply part of the season.

Source: Echoes of Appalachia – PFL Analytics

We are Watching the STB

The Surface Transportation Board’s first procedural move following the December 19th merger of the NS and UP filing sets the tone for months ahead. The STB has established the deadline for public comments on whether the 7,000-page application is complete for December 29thtoday. This initial step is critical; if the STB finds gaps or insufficient detail, it can pause the statutory review clock until applicants provide additional information.

Industry stakeholders have been mobilizing. The American Chemistry Council (ACC) issued a statement warning that the deal could create a “coast-to-coast monopoly”, while Canadian rivals CPKC and CN warned of “extraordinary risks” to network competition. The merger has support from over 2,000 stakeholders, including the SMART-TD union and President Trump.

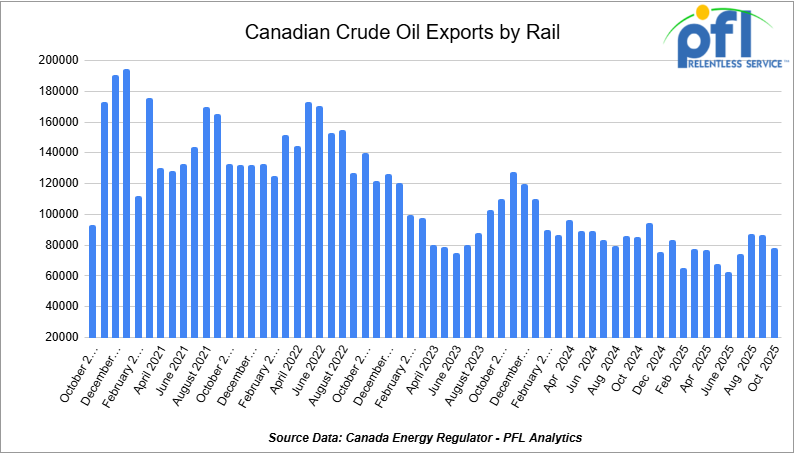

We are watching Canadian Crude by Rail

Crude by rail out of Canada decreased month-over-month. The Canadian Energy regulator reported on December 24, that 78,117 barrels were exported per day during the month of October 2025, down from 86,711 barrels in September of 2025, a decrease of -8,594 barrels per day and its second straight month over-month decline.

Crude by rail will always be necessary out of Canada for stranded oil not connected by pipelines. Raw bitumen, which is shipped as a non-haz product and is not able to flow in pipelines, is competitive with pipeline tolls and is a growing market to keep an eye on, particularly in light of Strathcona and Gibson announcing new projects. Other factors would be existing long-term contractual commitments and basis – we really need to see basis WTI-CMA (West Texas Intermediate – Calendar Month Average) blowout to -18 per barrel for sustained periods of time to make economic sense. Current rail rates from Alberta to the U.S. Gulf Coast have averaged $15.36 per barrel, making rail competitive whenever WCS-WTI spreads exceed $18 per barrel, including quality adjustments.

We are Watching Enbridge’s Line 5

A federal district judge ruled last week that the U.S. Pipeline Safety Act pre-empts Michigan’s attempts to shut down Enbridge’s Line 5 pipeline. This decision secures the continued flow of 540,000 barrels per day of light crude and NGLs to Sarnia and Midwest refineries. For tank car markets, the ruling prevents what would have been a chaotic scramble for rail capacity. Industry analysis indicates rail could only absorb roughly 50,000 bpd of displaced volume—less than 10% of the pipeline’s throughput—leaving a massive shortfall that would have crippled refinery operations.

The next legal front shifts to Wisconsin, where the Bad River Band is suing the Army Corps of Engineers over permits for the Line 5 reroute.

We are Watching Canadian Grain

Western Canadian grain shipments posted a strong finish to the 2024–25 crop year, with railways moving 49 million tonnes – a 12.1% increase compared to the prior year’s 43.7 million tonnes. This surge is significant for hopper car demand, indicating sustained appetite for covered hoppers across both CN and CPKC fleets.

Looking ahead, both major railways have released their 2025–26 grain transportation plans. CN is prepared to move between 27–29.5 million tonnes during the upcoming crop year, down from its record 31 million tonnes in 2024–25, but still robust. CPKC has committed to supplying capacity for up to 34 million tonnes of Canadian grain and grain products, subject to market demand, with weekly capacity targets of 685,000 tonnes during open navigation season at Thunder Bay and 525,000 tonnes during winter months.

The Canadian Transportation Agency (CTA) also issued its year-end determination on December 19th: CPKC exceeded its maximum grain revenue entitlement for 2024–25 by $2.66 million, requiring payment to the Western Grains Research Foundation. CN came in approximately $5.9 million below its entitlement. The robust volume growth—despite CPKC’s revenue ceiling breach—underscores the continued strength of Canadian grain exports and the steady demand for rail equipment in this sector.

We are watching the Pacific North West

Rail operations stabilized this week following earlier disruptions in the Pacific Northwest. BNSF reported that the “persistent weather pattern” bringing historic rainfall and flooding to the region has largely abated, with most subdivisions back in service. However, shipments moving between December 24 and January 3 may experience delays of 24 – 48 hours due to lighter train starts and reduced connecting carrier activity during the holiday period.

We are Watching “Air Cars” Help Capacity

While broader markets focus on headline velocity metrics, the real capacity battle this winter is being fought with air pressure. CN has strategically deployed its fleet of specialized distributed air braking cars—modified boxcars equipped with high-capacity air compressors—across Prairie corridors as temperatures approach the critical -25°C threshold that triggers operational restrictions.

This technology solves the single biggest capacity killer in extreme cold: brake line pressure loss. When temperatures plunge, rubber gaskets stiffen and metal couplings contract, causing air leakage that makes it impossible to maintain safe braking pressure at the tail end of a standard 10,000-foot train. Without these air cars, railroads are forced by physics and regulation to slash train lengths by up to 30% to maintain safety margins.

CN invested over $1 million to overhaul 20 of its distributed air braking cars in 2024, replacing air compressors and other major components specifically for this winter season. The railway operates a total fleet of approximately 100 such units, which it deploys strategically during the coldest months to reduce the need to shorten trains.

For shippers, the deployment of these units is a quiet bullish signal. An air car positioned mid-train acts as a mobile compressor station, allowing the railroad to run full-length consists even in a deep freeze. Every long train that successfully departs Winnipeg or Edmonton this week represents “ghost capacity”—tonnage that moved without requiring an extra crew start or additional locomotive. By keeping train lengths intact, CN protects its crew base from exhaustion and maintains asset velocity when other carriers might be cutting consists.

If CN’s winter service holds up better than expected in January, this specific hardware deployment will likely be a contributing factor. PFL will continue to monitor distributed air car utilization as a leading indicator of network capacity resilience.

We are watching Economic Indicators

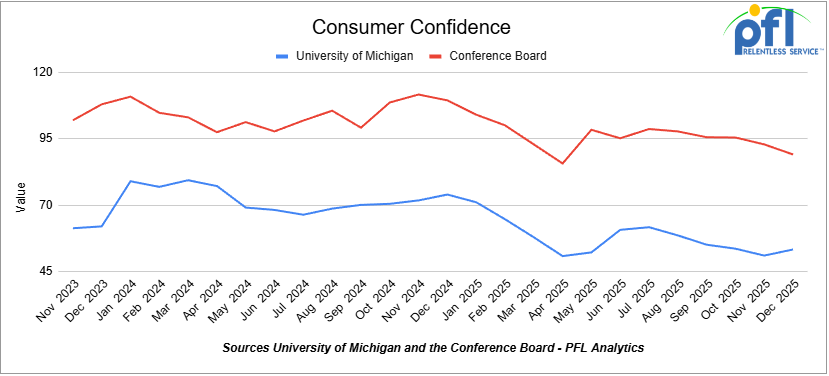

Consumer Confidence

The Index of Consumer Sentiment from the University of Michigan decreased from 92.9 in November to 89.1 in December.

The Conference Board Consumer Confidence Index increased from 51 in November to 53.3 in December.

Lease Bids

- 30-50, 6000cf Steel Hopper located off of CSX or NS in East. For use in petcoke service. Period: 5 Years.

- 10, 2500CF Open Top Hopper located off of UP or BN in Texas. For use in aggregate service. Period: 5 years. Need Rapid Discharge Doors.

- 50, 23.5-25.5 DOT111 Tank located off of Any Class 1 in USA. For use in Asphalt service. Period: 5 years.

- 100, 21.9K 117J Tank located off of All Class 1s in Midwest. For use in CO2 service. Period: 6 months.

- 30-50, 30K 117J Tank located off of NS or CSX in Northeast. For use in C5 service. Period: 1 year.

Sales Bids

- 28, 3400CF Hopper Covered located off of UP BN in Texas. For use in Cement service.Cement Gates needed.

- 20, 17K Tank DOT111 located off of various class 1s in various locations. For use in corn syrup service.

- 120, Various Gondola Open-Top Aluminum Rotary located off of various class 1s in various locations. For use in Sulphur service.Built 2004 or later.

- 30, 29K Tank DOT111 located off of various class 1s in Chicago. For use in Veg Oil service.

Lease Offers

- 100, 30K CPC1232 Tanks located off of UP or BN in Texas. Last used in Diesel.

- 100, 30K DOT117J Tanks located off of UP or BN in Texas. Last used in Gasoline.

- 100, 29K DOT117J Tanks located off of UP or BN in Texas. Last used in Gasoline. Coiled and Insulated.

- 36, 6351 Covered Hopper located off of CN in Wisconsin. Last used in Grain. through 2/27.

- 29, 6580 Covered Hopper located off of CN in Wisconsin. Last used in Grain. through 2/26.

- 18, 6580 Covered Hopper located off of CN in Wisconsin. Last used in Grain. through 2/27.

- 9, 5400 Covered Hopper located off of CN in Wisconsin. Last used in Grain. through 2/27.

- 21, 6351 Covered Hopper located off of CN in Wisconsin. Last used in DDG. Available until February 2027.

- 29, 6500 Covered Hopper located off of CN in Wisconsin. Last used in DDG. Available until February 2027.

- 50, 5380 Covered Hopper located off of UP or BN in Houston. Last used in Fertilizer. Cars are currently clean. Available until February.

- 50, 20K DOT117J Tank located off of All Class 1s in Moving. Last used in Styrene.

- 29, 25.5K DOT117J Tank located off of UP or BN in Texas. Cars are currently clean. Cars are currently clean.

- 90, 30K DOT117J Tank located off of UP or BN in Corpus Christie. Last used in Diesel.

Sales Offers

- 21, 50′ Boxcar Plate Cs located off of various class 1s in NM. End of Life.

- 3, 50′ Boxcar Plate Cs located off of various class 1s in multiple locations. End of Life.

- 27, 50′ Boxcar Plate Cs located off of various class 1s in PQ. End of Life.

- 100, 3250 Covered Hoppers located off of various class 1s in multiple locations. Sand Cars.

- 5, 2740 Mill Gondolas located off of various class 1s in NC. End of Life.

- 1, 2260 Mill Gondolas located off of various class 1s in AL. End of Life.

- 30, 2740 Mill Gondolas located off of various class 1s in multiple locations. End of Life.

- 21, 2740 Mill Gondolas located off of various class 1s in WA. End of Life.

- 9, 4750 Covered Hoppers located off of various class 1s in multiple locations. End of Life.

- 5, 4750 Covered Hoppers located off of various class 1s in multiple locations. End of Life.

- 50, 31.8K Tank CPC 1232s located off of UP or BN in TX. Requal Due in 2025.

- 100, 4600CF Open Top Hoppers located off of BN or CSX in Southeast. N/A.

Call PFL today to discuss your needs and our availability and market reach. Whether you are looking to lease cars, lease out cars, buy cars, or sell cars call PFL today at 239-390-2885

Live Railcar Markets

| CAT | Type | Capacity | GRL | QTY | LOC | Class | Prev. Use | Offer | Note |

|---|

PFL will be at the Following Conferences

- Where: Loews Arlington Hotel

- Attending: Brian Baker (239.297.4519), David Cohen (954-729-4774), and Curtis Chandler (239-405-3365)

- Conference Website

- Where: The Westin Galleria Dallas

- Attending: David Cohen (954-729-4774), and Curtis Chandler (239-405-3365)

- Conference Website

- Where: The Westin Galleria Dallas

- Attending: Brian Baker (239.297.4519)

- Conference Website