“Today’s mighty oak is just yesterday’s nut that held its ground.”

– David Icke

Due to the Government Shutdown, we are unable to report last week’s Jobs Update. We apologize for the inconvenience.

Jobs Update

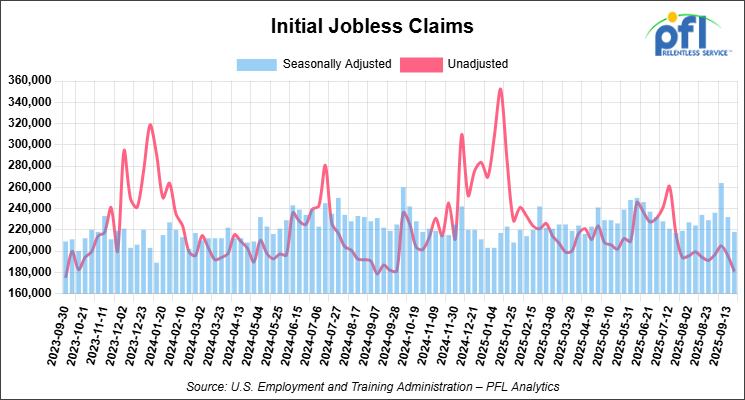

• Initial jobless claims seasonally adjusted for the week ending September 20, 2025 came in at 218,000, versus the adjusted number of 232,000 people from the week prior, down 14,000 people week over week.

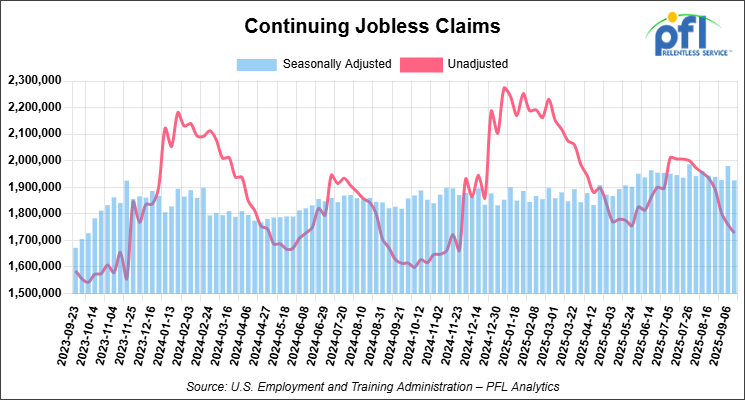

• Continuing jobless claims came in at 1,926,000, versus the adjusted number of 1,980,000 people from the week prior, down 54,000 week-over-week.

Stocks closed mixed on Friday of last week and mixed week-over-week

The DOW closed lower on Friday of last week, down -309.74 points (-0.65%), closing out the week at 47,147.48, but up 160.38 points week-over-week. The S&P 500 closed lower on Friday of last week, down -3.38 points (-0.05%), and closed out the week at 6,734.11, up 5.31 points week-over-week. The NASDAQ closed higher on Friday of last week, up 30.23 points (0.13%), and closed out the week at 22,900.59, down -103.95 points week-over-week.

In overnight trading, DOW futures traded lower and are expected to open at 47,193 this morning, down 38 points from Friday’s close.

Crude oil closed higher on Friday of last week and higher week-over-week

West Texas Intermediate (WTI) crude closed up $1.40 per barrel (2.39%), to close at $60.06 per barrel Friday of last week, and up $0.31 per barrel week-over-week. Brent crude closed up $1.38 per barrel (2.19%), to close at $64.39 per barrel, up $0.76 week-over-week.

One Exchange WCS (Western Canadian Select) for December delivery settled on Friday of last week at US$11.65 below the WTI-CMA (West Texas Intermediate – Calendar Month Average). The implied value was US$46.95 per barrel.

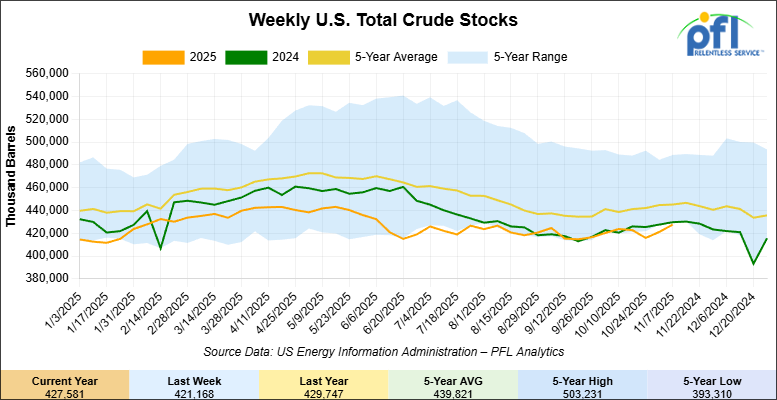

U.S. commercial crude oil inventories (excluding those in the Strategic Petroleum Reserve) increased by 6.4 million barrels week-over-week. At 427.6 million barrels, U.S. crude oil inventories are 4% below the five-year average for this time of year.

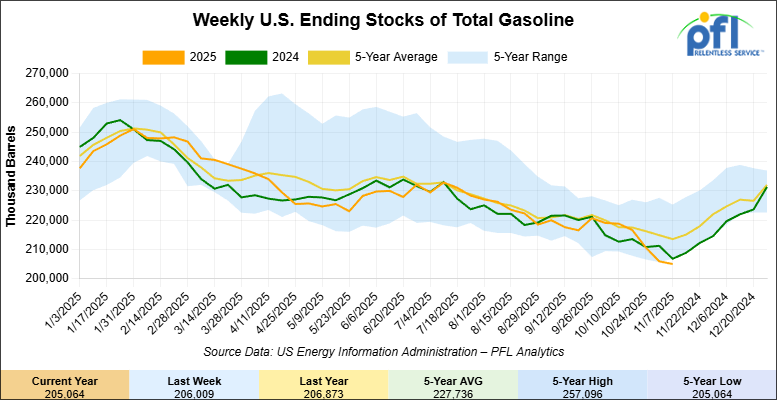

Total motor gasoline inventories decreased by 900,000 barrels week-over-week and are 4% below the five-year average for this time of year.

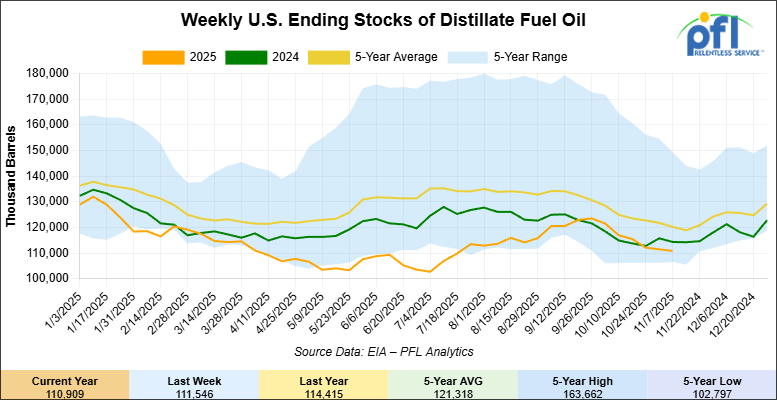

Distillate fuel inventories decreased by 600,000 barrels week-over-week and are 8% below the five-year average for this time of year.

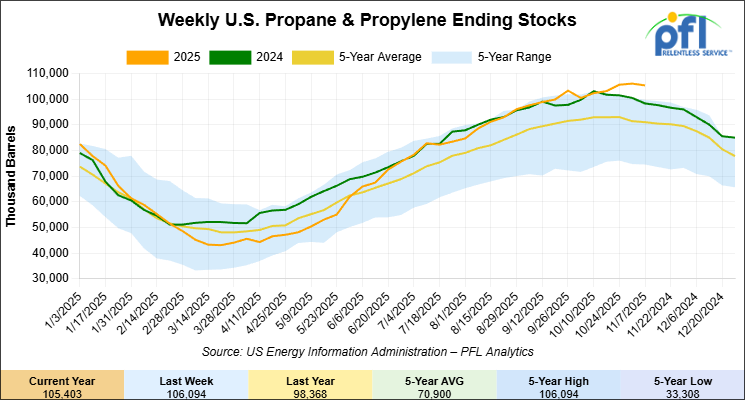

Propane/propylene inventories decreased by 700,000 barrels week-over-week and are 16% above the five-year average for this time of year.

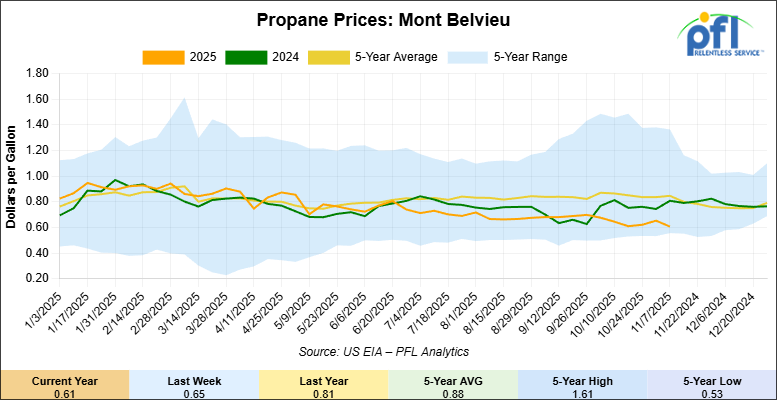

Propane prices closed at 61 cents per gallon on Friday of last week, down 4 cents per gallon week-over-week, and down by 10 cents per gallon year-over-year.

Overall, total commercial petroleum inventories increased by 2.5 million barrels during the week ending November 7, 2025.

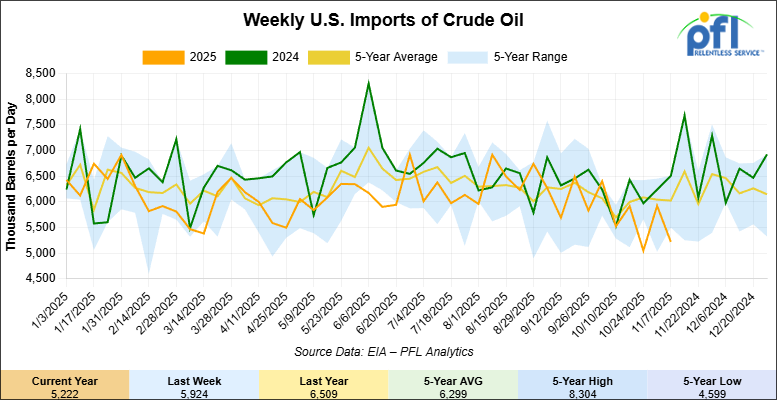

U.S. crude oil imports averaged 5.2 million barrels per day during the week ending November 7, 2025, a decrease of 703,000 barrels per day week-over-week. Over the past four weeks, crude oil imports averaged 5.5 million barrels per day, 12.1% less than the same four-week period last year. Total motor gasoline imports (including both finished gasoline and gasoline blending components) averaged 548,000 barrels per day, and distillate fuel imports averaged 167,000 barrels per day during the week ending November 7, 2025.

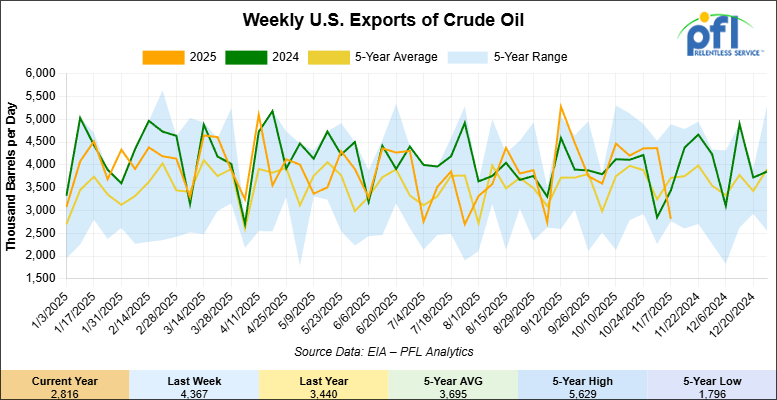

U.S. crude oil exports averaged 2.816 million barrels per day during the week ending November 7, 2025, a decrease of 1.551 million barrels per day week-over-week. Over the past four weeks, crude oil exports averaged 3.937 million barrels per day.

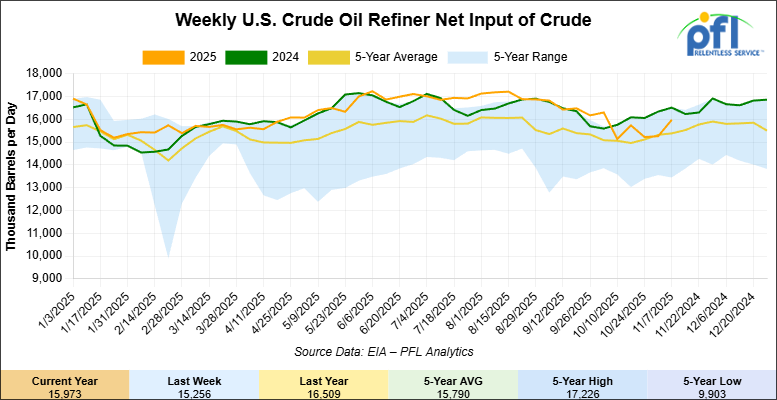

U.S. crude oil refinery inputs averaged 16 million barrels per day during the week ending November 7, 2025, which was 717,000 barrels per day more week-over-week.

WTI futures are poised to open at $60.08, down 1 cent from Friday’s close.

North American Rail Traffic

Week Ending November 8, 2025

The Association of American Railroads (AAR) reported total U.S. rail traffic for the week ending November 8, 2025, at 493,493 carloads and intermodal units, down 4.9% from the same week last year. Total carloads were 224,651, essentially flat at +0.1%, while weekly intermodal volume totaled 268,842 containers and trailers, a decline of 8.7% compared with 2024.

Four of the ten major carload commodity groups posted year-over-year gains. The largest increases were in nonmetallic minerals, up 3,753 carloads to 32,939; grain, up 809 carloads to 24,291; and miscellaneous carloads, up 659 carloads to 8,469. The steepest declines were seen in motor vehicles and parts, down 1,436 carloads to 13,840; metallic ores and metals, down 1,355 carloads to 19,056; and coal, down 1,207 carloads to 57,352.

For the first forty-five weeks of 2025, U.S. railroads reported cumulative volume of 10,004,661 carloads, up 1.8% from the same point last year, and 12,211,278 intermodal units, up 2.5%. Combined U.S. rail traffic through week 45 totaled 22,215,939 carloads and intermodal units, an overall increase of 2.2% compared with 2024.

Across North America, total rail traffic for the week reached 679,267 carloads and intermodal units, down 0.1% from the same week last year. Carloads totaled 327,995, down 0.8%, while intermodal volume rose 0.5% to 351,272 units. Cumulative North American traffic for the first forty-five weeks of 2025 was 30,593,085 carloads and intermodal units, up 1.9% year-over-year.

In Canada, total rail traffic for the week amounted to 160,576 carloads and intermodal units, with carloads down 2.6% to 91,232 and intermodal traffic surging 65.4% to 69,344. Cumulative Canadian rail volume through week 45 stood at 7,293,052 units, up 2.1% from the same period in 2024.

In Mexico, weekly rail activity declined compared with last year. Mexican railroads originated 12,112 carloads, down 4.2%, and 13,086 intermodal units, down 0.1%, for a total of 25,198 carloads and intermodal units, down 2.3% year-over-year. Cumulative Mexican rail volume through the first forty-five weeks of 2025 totaled 1,084,094 units, down 3.7% compared with the same point last year.

Source Data: AAR – PFL Analytics

North American Rig Count Summary

Rig Count

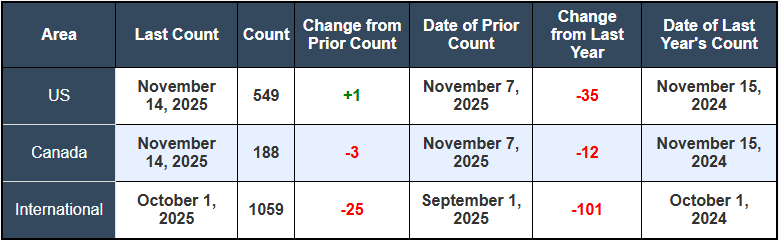

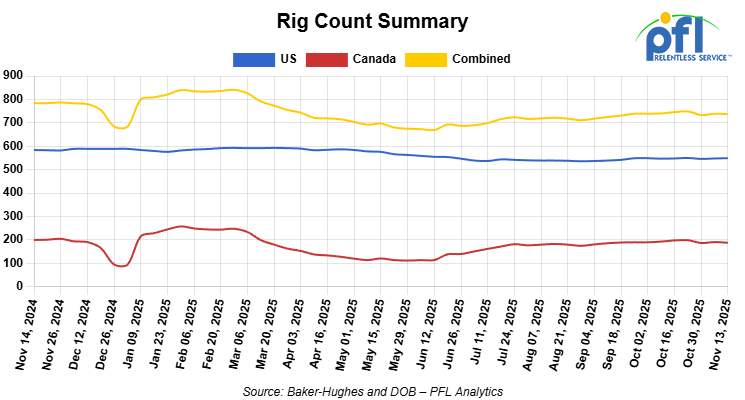

North American rig count was down by -2 rigs week-over-week. The US rig count was up by +1 rig week-over-week, but down by -35 rigs year-over-year. The U.S. currently has 549 active rigs. Canada’s rig count was down by -3 rigs week-over-week and down by -12 rigs year-over-year. Canada currently has 188 active rigs. Overall, year-over-year we are down by -47 rigs collectively.

We are watching a few things out there for you:

We are watching Petroleum Carloads

The four-week rolling average of petroleum carloads carried on the six largest North American railroads rose to 29,313 from 28,913, which was an increase of +400 rail cars week-over-week. Canadian volumes were higher. CPKC’s shipments were higher by +10.0% week over week, CN’s volumes were higher by +26.0% week-over-week. U.S. shipments were mixed. The NS had the largest percentage loss and was down by -5.0%.The CSX had the largest percentage increase and was up by +10.0%.

We are watching MEG and Cenovus

The $6.1 billion acquisition of MEG Energy by Cenovus is now final, concluding a dramatic, months-long takeover battle. After MEG shareholders approved the deal with 86% support last week, the transaction received its final order from the Court of King’s Bench of Alberta on November 12.

Cenovus confirmed it has received all key regulatory approvals, including from the Canadian Competition Bureau and the U.S. Federal Trade Commission. MEG’s shares were scheduled to be delisted from the Toronto Stock Exchange at the close of market on November 14.

The deal’s approval ends a contentious saga that included a hostile bid from Strathcona Resources and three separate vote delays. The stalemate broke only after Cenovus sweetened its offer and struck a side-deal to sell C$150 million in assets to Strathcona, which in turn agreed to vote its 14.2% MEG stake in favor of the acquisition.

The industrial logic is compelling: Cenovus and MEG operate adjacent, side-by-side thermal properties at Christina Lake. The merger immediately adds MEG’s 110,000 b/d of production, which Cenovus plans to boost to 150,000 b/d by 2028 by integrating the assets. This is part of a broader plan to grow total company output to 850,000 boe/d by 2028.

We are Watching The “Green Old Deal”

A federal judge has issued a preliminary injunction stopping the California Air Resources Board (CARB) from enforcing its Clean Truck Partnership (CTP) against truck OEMs. The ruling throws California’s aggressive emissions regulations and ZEV timelines for the trucking industry into disarray.

The CTP was a 2023 deal in which major OEMs—including Daimler, PACCAR, and Volvo—agreed not to challenge CARB’s other emissions rules, such as the Advanced Clean Truck (ACT) regulation, in court. In exchange, CARB agreed to ease certain NOx emissions standards.

The injunction was triggered by CARB’s own legal strategy. Judge Dena Coggins ruled that a recent countersuit filed by CARB in state court (in response to a Federal suit filed) – which sought to force OEM compliance with the CTP—constitutes irreparable harm to the manufacturers. The judge stated that because of CARB’s own lawsuit, the harms identified by the OEMs are no longer speculative.

We Continue to Watch the NS and UP

Shareholders at Union Pacific and Norfolk Southern delivered the biggest rail development of the week on Friday of last week, voting overwhelmingly to approve their proposed $85 billion merger. UP reported 99.5% support, while NS came in just under 99%. With those votes, the deal officially enters the next, and most difficult, phase: a full Surface Transportation Board review expected to dominate 2026.

If ultimately approved, the combined railroad would create a 50,000-mile, coast-to-coast Class I network across 43 states. NS shareholders will receive one UP share plus $88.82 in cash per NS share. The carriers are promoting the deal as a single-line system capable of shaving one to two days off transcontinental transit times while capturing close to $3 billion in annual efficiencies.

UP CEO Jim Vena indicated on Friday of last week the company plans to file its formal STB application in late November or early December—ahead of the original January 2026 target.

Opposition Intensifies

Hours after the shareholder vote, nine Republican state attorneys general, led by Tennessee’s Jonathan Skrmetti and Kansas’s Kris Kobach, sent a letter to the STB warning the merger “will result in undue market concentration that stifles competition” and raise prices for consumers. This marks a notable rift with President Trump, who told reporters in September the deal “sounds good to me” after meeting with Vena.

Earlier in the week, BNSF CEO Katie Farmer issued pointed comments on Tuesday, noting that UP historically “raises rates on competing interchange partners to the point of making those lanes economically uncompetitive” in prior mergers. Farmer cited UP’s own filings during the CP-KCS merger review, where UP argued against reducing competitive options at gateways.

The chemical industry continues its opposition, with 40 manufacturing CEOs warning in October that reduced rail competition will drive up rates and make their companies less competitive globally. However, labor support remains strong following groundbreaking job protection agreements with SMART-TD and the National Conference of Firemen and Oilers, guaranteeing workers will not face involuntary furloughs from the merger.

The Regulatory Gauntlet

The STB faces a high bar: it must determine whether the merger “enhances competition” under stringent rules established in 2001 after service disruptions from previous consolidations. The review is expected to conclude by early 2027, with UP agreeing to pay a $2.5 billion breakup fee if the STB rejects the deal or imposes unacceptable conditions.

If approved, industry observers believe CSX will need to find a merger partner to remain competitive, potentially triggering a wave of Class I consolidation, not seen in over two decades.

We are Watching Weak Imports

New data on container volumes signals a weak peak season and a potentially difficult start to 2026 for intermodal. U.S. container import volumes in October posted a 0.1% decline compared to September, a rare event that breaks a typical seasonal uptick. This marks only the second time in the past decade that October volumes have fallen month-over-month.

This weakness is attributed to shippers front-loading imports earlier in 2025 to get ahead of tariff anxiety. Data from the National Retail Federation (NRF) and Hackett Associates confirms the trend, showing September volumes fell 9.3% from August and 7.4% year-over-year.

The NRF’s forecast calls for the decline to accelerate, with November volumes projected to fall 14.4% y/y and December volumes to plummet 17.9% y/y. Looking ahead, Hackett Associates founder Ben Hackett predicts a further, larger decline in the first quarter of 2026.

We are Watching Left Wing Carney

The “generational” investment promises in Left Wing Prime Minister Mark Carney’s first federal budget, tabled November 5, are facing a reality check as key details are contradicted by project authorities and industry stakeholders.

The budget’s flagship infrastructure promise, the Alto high-speed rail line, is at the center of the disconnect. The budget promises new legislation to streamline approvals and “enable construction of the project to start in four years,” cutting an original eight-year timeline in half. This political promise is in direct conflict with Alto’s own official corporate documents. The project’s website states the current design and development phase alone is “expected to last around 5 years,” with Alto’s CEO indicating phased construction is expected to start in 2029 or 2030, not four years from now.

Reaction from key rail-served industries has also been lukewarm. The Canadian Automobile Dealers Association (CADA) said the budget delivered a mixed picture, welcoming a new investment tax deduction but criticizing the failure to revisit the vehicle luxury tax. Ontario’s Finance Minister, Peter Bethlenfalvy, was more critical, calling the budget “tinkering” and stating it falls short on tariff relief for the auto sector.

Furthermore, the budget’s “green steel” industrial strategy is already facing headwinds. Reports this week indicate that ArcelorMittal Dofasco’s massive decarbonization project in Hamilton—a poster child for the new policy—is stalled, having missed 2023 and 2024 milestones, with construction yet to begin.

In case you missed it, No More Penny

The last penny was minted for the last time on Wednesday of last week at the U.S. Mint in Philadelphia, overseen by U.S. Treasurer Brandon Beach. President Donald Trump announced via social media in February that he instructed the Mint to stop making the once-popular coin, citing the cost of production.

Beach said Wednesday of last week that the final coins pressed will be auctioned off and that the actual last pennies put into circulation from the US Mint were struck in June.

The penny outlived its sibling, the half-penny, by 168 years. It’s survived by the nickel, dime, quarter, and rarely seen half-dollar and dollar coins.

Despite its demise, the penny will remain legal tender.

Lease Bids

- 30-50, 6000cf Steel Hopper located off of CSX or NS in East. For use in petcoke service. Period: 5 Years.

- 10, 2500CF Open Top Hopper located off of UP or BN in Texas. For use in aggregate service. Period: 5 years. Need Rapid Discharge Doors.

- 10, 25.5K Any Type Tank located off of CSX in Florida. For use in UCO service. Period: 2 Years.

- 50, 23.5-25.5 DOT111 Tank located off of Any Class 1 in USA. For use in Asphalt service. Period: 5 years.

- 100, 21.9K 117J Tank located off of All Class 1s in Midwest. For use in CO2 service. Period: 6 months.

- 100, 33K Pressure Tank located off of CN or CP in Canada. For use in Propane service. Period: Winter.

- 30-50, 30K 117J Tank located off of NS or CSX in Northeast. For use in C5 service. Period: 1 year.

Sales Bids

- 28, 3400CF Covered Hopper located off of UP BN in Texas. For use in Cement service.Cement Gates needed..

- 20, 17K Tank DOT111 located off of various class 1s in various locations. For use in corn syrup service.

- 120, Various Gondola Open-Top Aluminum Rotary located off of various class 1s in various locations. For use in Sulphur service.Built 2004 or later.

Lease Offers

- 60, 4750 Covered Hoppers located off of UP or BN in Eads, CO. Last used in Grain. Cars are currently clean. UP to 5 Years, 3 Hopper, Gravity Gate, Trough Hatches.

- 100, 6250 Covered Hoppers located off of UP in US. Last used in DDG. 1 Year term. Dirty to Dirty. Free move on UP..

- 25, 19.6K DOT111 Tanks located off of UP in US. Last used in Molases.

- 50, 20K DOT111 Tanks located off of UP or BN in Wichita Falls, TX. Last used in HCL.

- 50, 30K 117R Tanks located off of CSX, NS, or CN in Detroit. Last used in Diesel. Multiyear.

- 50, 20K 117J Tanks located off of All Class 1s in Multiple Locations. Last used in Styrene. Cars are currently moving.

- 22, 25.5K DOT111 Tanks located off of UP in Texas. Last used in Asphalt.

- 29, 25.5K 117J Tanks located off of BN or UP in Texas. Cars are currently clean.

- 40, 30K 117J Tanks located off of BNSF or UP in Houston. Cars are currently clean.

- 50, 5380 Covered Hoppers located off of BNSF or UP in Houston. Cars are currently clean. Available until Feburary.

- 21, 6351 Covered Hoppers located off of CN in Wisconsin. Last used in DDG. Available until February 2027.

- 29, 6500 Covered Hoppers located off of CN in Wisconsin. Last used in DDG. Available until February 2027.

- 100, 30K CPC1232 Tanks located off of UP or BN in Texas. Last used in Diesel.

- 100, 30K DOT117J Tanks located off of UP or BN in Texas. Last used in Gasoline.

- 100, 29K DOT117J Tanks located off of UP or BN in Texas. Last used in Gasoline. Coiled and Insulated.

- 36, 6351 Covered Hopper located off of CN in Wisconsin. Last used in Grain. through 2/27.

- 29, 6580 Covered Hopper located off of CN in Wisconsin. Last used in Grain. through 2/26.

- 18, 6580 Covered Hopper located off of CN in Wisconsin. Last used in Grain. through 2/27.

- 9, 5400 Covered Hopper located off of CN in Wisconsin. Last used in Grain. through 2/27.

Sales Offers

- 21, 50′ Boxcar Plate Cs located off of various class 1s in NM. End of Life.

- 3, 50′ Boxcar Plate Cs located off of various class 1s in multiple locations. End of Life.

- 27, 50′ Boxcar Plate Cs located off of various class 1s in PQ. End of Life.

- 100, 3250 Covered Hoppers located off of various class 1s in multiple locations. Sand Cars.

- 5, 2740 Mill Gondolas located off of various class 1s in NC. End of Life.

- 1, 2260 Mill Gondolas located off of various class 1s in AL. End of Life.

- 30, 2740 Mill Gondolas located off of various class 1s in multiple locations. End of Life.

- 21, 2740 Mill Gondolas located off of various class 1s in WA. End of Life.

- 9, 4750 Covered Hoppers located off of various class 1s in multiple locations. End of Life.

- 5, 4750 Covered Hoppers located off of various class 1s in multiple locations. End of Life.

- 50, 31.8K Tank CPC 1232s located off of UP or BN in TX. Requal Due in 2025.

- 100, 4600CF Open Top Hoppers located off of BN or CSX in Southeast.

Call PFL today to discuss your needs and our availability and market reach. Whether you are looking to lease cars, lease out cars, buy cars, or sell cars call PFL today at 239-390-2885

Live Railcar Markets

| CAT | Type | Capacity | GRL | QTY | LOC | Class | Prev. Use | Offer | Note |

|---|

PFL will be at the Following Conferences

- Where: Loews Arlington Hotel

- Attending: Brian Baker (239.297.4519), David Cohen (954-729-4774), and Curtis Chandler (239-405-3365)

- Conference Website

- Where: The Westin Galleria Dallas

- Attending: David Cohen (954-729-4774), and Curtis Chandler (239-405-3365)

- Conference Website

- Where: The Westin Galleria Dallas

- Attending: Brian Baker (239.297.4519)

- Conference Website