“Out of difficulties grow miracles.” – Jean de la Bruyere

Due to the Government Shutdown, we are unable to report last week’s Jobs Update. We apologize for the inconvenience.

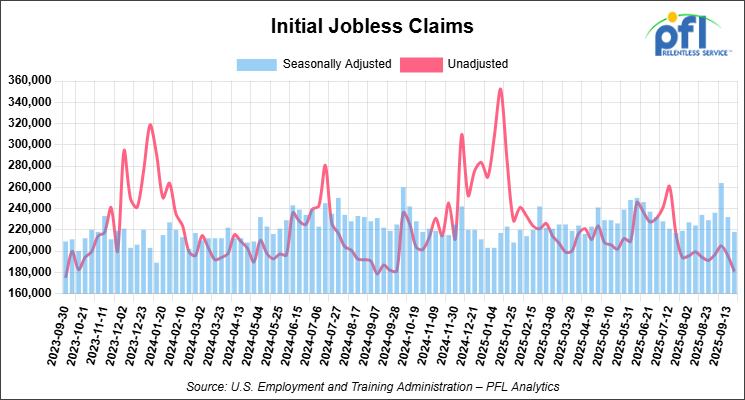

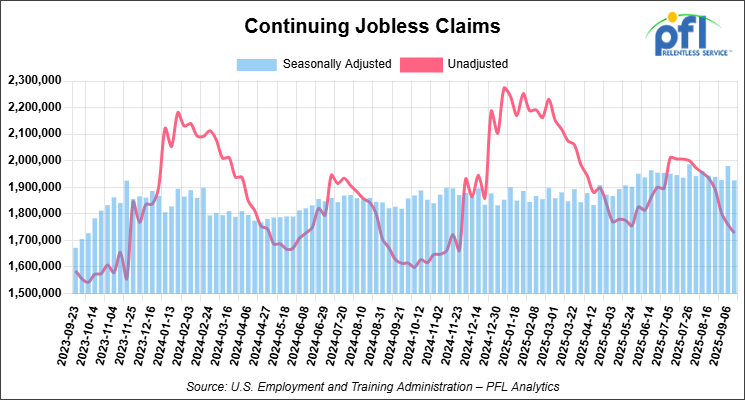

Jobs Update

• Initial jobless claims seasonally adjusted for the week ending September 20, 2025 came in at 218,000, versus the adjusted number of 232,000 people from the week prior, down 14,000 people week over week.

• Continuing jobless claims came in at 1,926,000, versus the adjusted number of 1,980,000 people from the week prior, down 54,000 week-over-week.

Stocks closed higher on Friday of last week and higher week-over-week

The DOW closed higher on Friday of last week, up 40.75 points (0.09%), closing out the week at 47,562.87, up 355.75 points week-over-week. The S&P 500 closed higher on Friday of last week, up 17.86 points (0.26%), and closed out the week at 6,840.20, up 48.51 points week-over-week. The NASDAQ closed higher on Friday of last week, up 143.81 points (0.61%), and closed out the week at 23,724.96, up 520.09 points week-over-week.

In overnight trading, DOW futures traded higher and are expected to open at 47,764 this morning, up 42 points from Friday’s close.

Crude oil closed higher on Friday of last week, but lower week-over-week

West Texas Intermediate (WTI) crude closed up +41 cents per barrel (0.68%), to close at $60.98 on Friday of last week, but down -52 cents week-over-week. Brent crude closed up +7 cents per barrel (0.11%), to close at $65.07, but down -87 cents week-over-week.

One Exchange WCS (Western Canadian Select) for December delivery settled on Friday of last week at US$11.90 below the WTI-CMA (West Texas Intermediate – Calendar Month Average). The implied value was US$48.20 per barrel.

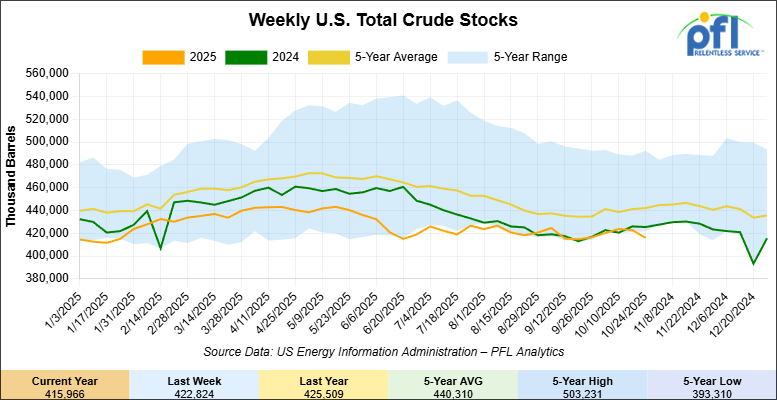

U.S. commercial crude oil inventories (excluding those in the Strategic Petroleum Reserve) decreased by 6.9 million barrels week-over-week. At 416.0 million barrels, U.S. crude oil inventories are 6% below the five-year average for this time of year.

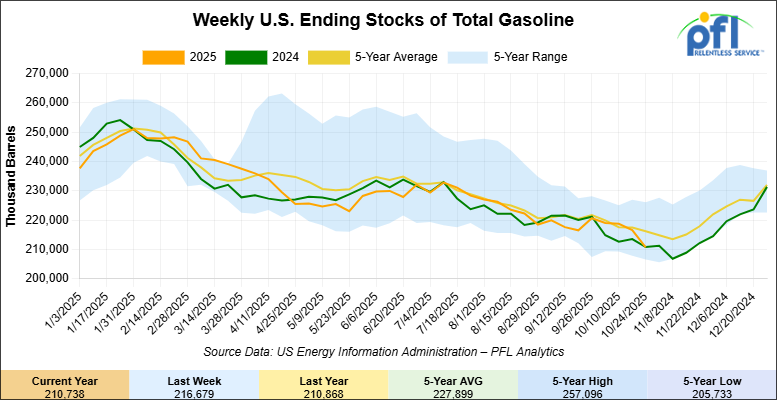

Total motor gasoline inventories decreased by 5.9 million barrels week-over-week and are 3% below the five-year average for this time of year.

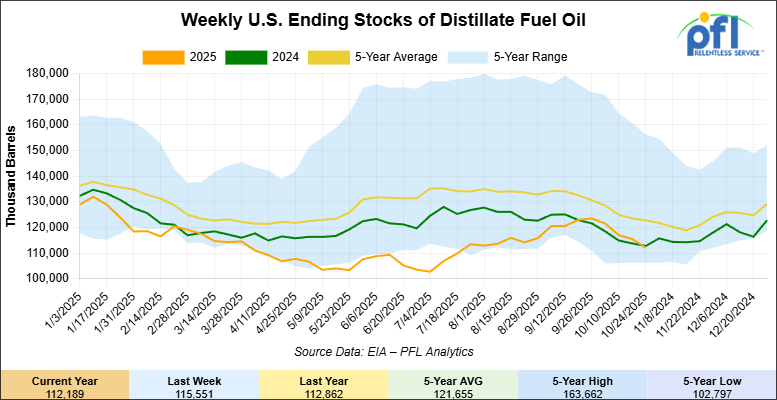

Distillate fuel inventories decreased by 3.4 million barrels week-over-week and are 8% below the five-year average for this time of year.

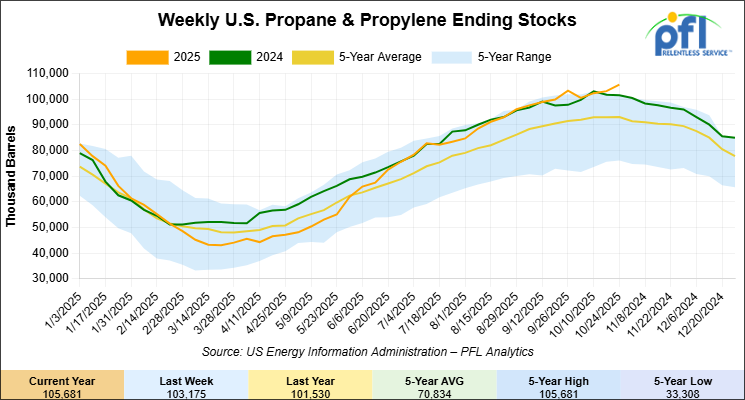

Propane/propylene inventories increased by 2.5 million barrels week-over-week and are 14% above the five-year average for this time of year.

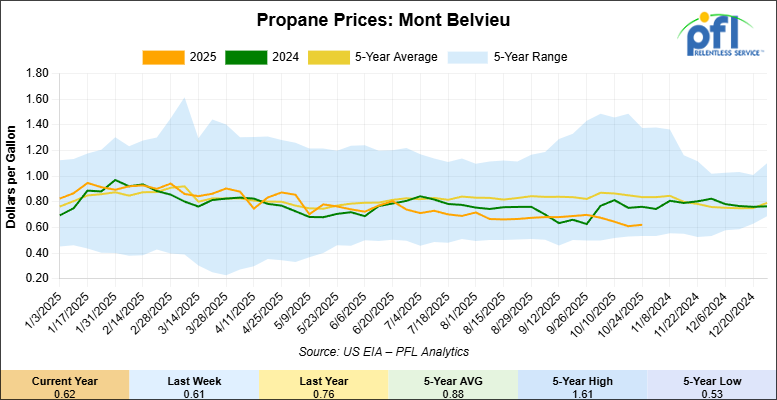

Propane prices closed at 62 cents per gallon on Friday of last week, up 1 cent per gallon week-over-week, but down by 14 cents per gallon year-over-year.

Overall, total commercial petroleum inventories decreased by 15.9 million barrels during the week ending October 24, 2025.

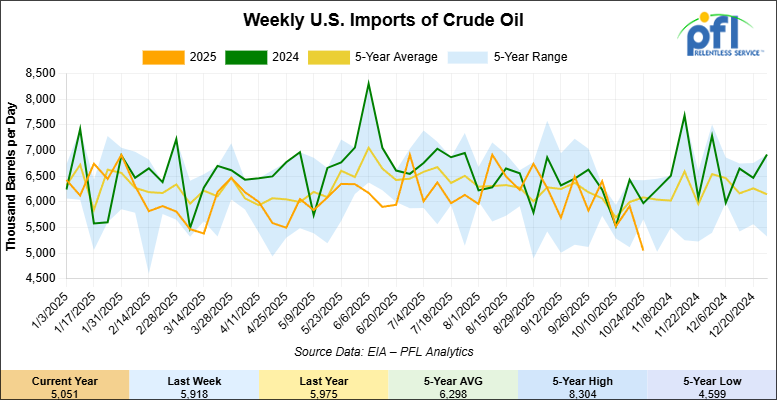

U.S. crude oil imports averaged 5.1 million barrels per day during the week ending October 24, 2025, a decrease of 867,000 barrels per day week-over-week. Over the past four weeks, crude oil imports averaged 5.7 million barrels per day, 5.3% less than the same four-week period last year. Total motor gasoline imports (including both finished gasoline and gasoline blending components) averaged 466,000 barrels per day, and distillate fuel imports averaged 109,000 barrels per day during the week ending October 24, 2025.

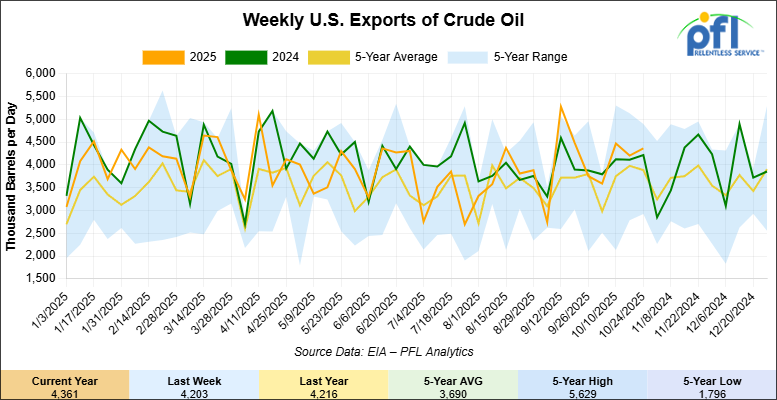

U.S. crude oil exports averaged 4.361 million barrels per day during the week ending October 24, 2025, an increase of 158,000 barrels per day week-over-week. Over the past four weeks, crude oil exports averaged 4.155 million barrels per day.

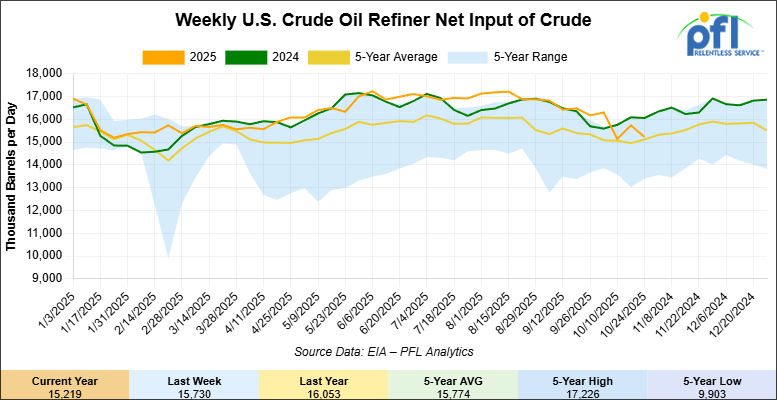

U.S. crude oil refinery inputs averaged 15.2 million barrels per day during the week ending October 24, 2025, which was 511,000 barrels per day less week-over-week.

WTI futures are poised to open at $61.12, up 14 cents from Friday’s close.

North American Rail Traffic

Week Ending October 25, 2025

The Association of American Railroads (AAR) reported total U.S. rail traffic for the week ending October 25, 2025, at 499,688 carloads and intermodal units, down 3.8% compared with the same week last year. Total carloads were 226,748, down 0.9%, while weekly intermodal volume totaled 272,940 containers and trailers, a decline of 6.1% from the same week in 2024.

Five of the ten major carload commodity groups posted year-over-year increases. The strongest gains were recorded in metallic ores and metals, up 1,470 carloads to 19,559; nonmetallic minerals, up 837 carloads to 32,940; and miscellaneous carloads, up 584 carloads to 9,056. The largest declines were in motor vehicles and parts, down 1,895 carloads to 14,556; coal, down 1,470 carloads to 58,652; and grain, down 1,125 carloads to 23,031.

For the first forty-three weeks of 2025, U.S. railroads reported a cumulative total of 9,552,801 carloads, up 1.9% from the same period last year, and 11,672,717 intermodal units, up 3.0% year-over-year. Combined U.S. rail traffic through week forty-three totaled 21,225,518 carloads and intermodal units, an overall increase of 2.5% compared with 2024.

Across North America, total rail traffic for the week reached 690,541 carloads and intermodal units, down 2.8% from the same week in 2024. Carloads totaled 331,250, down 1.7%, while intermodal volume declined 3.8% to 359,291 units. Cumulative North American traffic for the first forty-three weeks of 2025 stood at 29,223,874 carloads and intermodal units, up 2.1% year-over-year.

In Canada, total rail traffic for the week was 163,617 carloads and intermodal units, with carloads down 5.3% to 92,109 and intermodal traffic down 0.2% to 71,508. Year-to-date Canadian rail volume through week forty-three totaled 6,966,014 units, up 1.8% compared with the same period in 2024.

In Mexico, weekly rail activity continued to outperform year-ago levels. Mexican railroads handled 12,393 carloads, up 14.7%, and 14,843 intermodal units, up 33.0% from the same week in 2024, for a total of 27,236 units, up 24.0% year-over-year. Despite the strong weekly performance, cumulative Mexican rail volume through the first forty-three weeks of 2025 totaled 1,032,342 carloads and intermodal units, down 3.8% from the same point in 2024.

Automotives

The automotive supply chain, a cornerstone of North American rail freight, is now facing an immediate and escalating production crisis. The 11.5% year-over-year plunge in “Motor Vehicles & Parts” carloads seen in the Week 43 data is confirmed to be the leading edge of a severe supply shock, not a simple market fluctuation.

Last Friday the geopolitical dispute over chipmaker Nexperia escalated dramatically. The company suspended supplies to its own Chinese assembly plant, a critical link in the global supply chain. The impact is no longer theoretical. Honda has already cut production by half at its Alliston, Ontario plant, which builds the Civic and CR-V. Nissan and European manufacturers like Volkswagen, BMW, and Stellantis are warning they are just “days away” from full assembly line stoppages.

This Nexperia crisis, which MEMA warns could cause “significant impacts” at U.S. plants within weeks, is hitting an already volatile sector. The auto market is simultaneously grappling with a forecasted “collapse” in EV demand as federal tax credits expired at the end of September and a new, independent strike authorization by UAW members at Volkswagen’s Chattanooga plant. The 11.5% carload drop is the first statistical proof of a crisis that will directly and negatively impact rail volumes for the remainder of the quarter.

A Tale of Two Economies

The aggregate 0.9% dip in U.S. carloads for Week 43 masks a sharp, bifurcated market. Resilience in the industrial-facing economy, led by a strong 8.1% year-over-year gain in Metallic Ores & Metals, is being canceled out by the collapse in consumer-facing goods.

The 6.1% drop in U.S. intermodal traffic is a clear reflection of a cooling consumer economy and weaker import volumes. The October ITS Logistics Index confirms this, pointing to a continued downward trend in import volumes as many shippers front-loaded holiday freight earlier in the year to hedge against uncertainty. While this has eased congestion at rail ramps, it is creating a severe crisis at the first and last mile. The drayage market is facing a surge in bankruptcies among small- and mid-size carriers, threatening a future capacity crunch.

The drayage market’s structural crisis—with over 7,500 carriers exiting in Q2 and drayage-intensive Chicago seeing 33% of recent bankruptcy filings—is paradoxically supporting rail demand. Limited short-haul capacity is pushing shippers toward rail intermodal solutions for first/last mile gaps, potentially offsetting broader volume softness.

Mexican Boom

The geographic split in North America volumes is telling. While the U.S. (-3.8%) and Canadian (-3.1%) networks contracted, Mexican rail traffic posted an explosive, double-digit boom. Mexican carloads surged 14.7% and intermodal traffic skyrocketed 33.0% year-over-year. This weekly surge violently reverses a negative year-to-date trend for Mexican rail. This is not an anomaly; it is the first concrete statistical proof of the CPKC single-line merger thesis playing out, as freight is aggressively diverted to its new, seamless transnational network, a trend supported by reports of OEMs like Honda and Nissan increasing rail exports from Mexico.

The Mexico boom reflects permanent, structural supply chain regionalization, not temporary tariff dynamics. CPKC’s integrated single-line network, combined with infrastructure investments (Laredo bridge, Green Corridors automation), is positioning the carrier to capture outsized volume growth from OEM Mexican facility expansion and agricultural export growth (+$53B forecast by 2030). This is a multi-year tailwind, not a bounce.

Grains

The 4.7% year-over-year drop in U.S. grain carloads is not a story of poor supply. It is a story of demand displacement. A strong local corn harvest in the U.S. Southeast is satisfying regional feed demand, reducing the need for long-haul rail from the Midwest. This is confirmed by CSX’s new tariffs and its own forecast of lower domestic grain demand.

The Canadian network faces the exact opposite scenario: a supply surge. A record Canadian corn crop is forecast, along with strong yields for canola and barley in the prairie provinces. CPKC’s own data confirms this, showing that Week 43 was its seventh consecutive week moving over 600,000 metric tonnes of Canadian grain.

Class I Performance

The performance gap between Canada’s two Class I carriers is widening, and the market is paying close attention.

Canadian Pacific Kansas City (CPKC) continues to set the benchmark for fluid, resilient operation. Week 43 metrics underscore its strength: average train speed remained elevated at 19.9 MPH, and terminal dwell held at a low 8.7 hours. CPKC’s Q3 results were robust, and the network is absorbing rising agricultural volumes while aggressively expanding in the booming Mexico corridor. With seamless cross-border service and infrastructure upgrades, CPKC appears perfectly positioned to capitalize on multi-year structural trends in grain and intermodal flows.

Canadian National (CN), by contrast, is pivoting sharply from growth to defense. CN just announced the layoff of approximately 400 managers—about 6% of its non-union workforce—in the largest restructuring in its history. The timing coincides with sliding freight volumes, steep new tariffs on steel, autos, aluminum, and lumber, and persistent weakness in intermodal demand. Bulk shipments are not filling the gap. New leadership appointments (Patrick Whitehead as COO, Janet Drysdale as CCO) signal a realignment of both operations and customer strategy heading into 2026, but also underscore the urgency to maintain margins in a tough business climate.

Operational issues are compounding the challenge: CN’s average train speed fell by 6.0% year-over-year in Week 43, revenue ton-miles dropped 1.1%, and carloads declined 4.1%. Shippers are facing slower answers and fewer touchpoints as a result of the restructuring—raising concerns about customer service and responsiveness. While the company frames this as a “headcount adjustment,” the timing and scale suggest deeper retrenchment consistent with a downturn in cross-border trade and tariff-driven contraction.

As CN prepares to report Q3 earnings, the market will be watching for signs that this is a one-time correction—or the first step in a broader retrenchment. Rival CPKC reported profit growth despite similar challenges, highlighting CN’s struggles to maintain operational momentum. The Canadian Class I bifurcation is clear: CPKC remains on offense, while CN is forced into defensive maneuvers, risking further market share losses if operational execution does not quickly improve.

Source Data: AAR – PFL Analytics

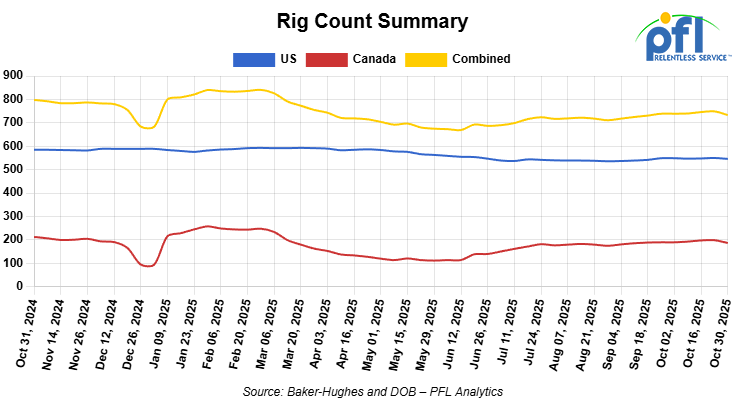

North American Rig Count Summary

Rig Count

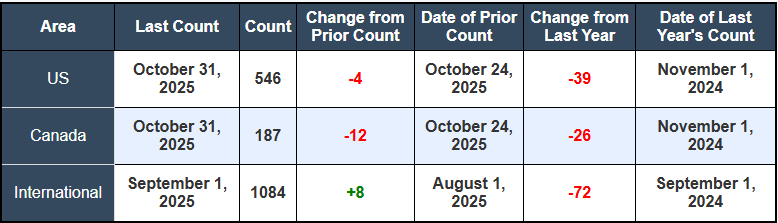

North American rig count was down by -16 rigs week-over-week. The US rig count was down by -4 rigs week-over-week, and down by -39 rigs year-over-year. The US currently has 546 active rigs. Canada’s rig count was down by -12 rigs week-over-week and down by -26 rigs year-over-year. Canada currently has 187 active rigs. Overall, year-over-year we are down by -65 rigs collectively.

We are watching a few things out there for you:

We are watching Petroleum Carloads

The four-week rolling average of petroleum carloads carried on the six largest North American railroads rose to 28,879 from 28,669, which was an increase of +210 rail cars week-over-week. Canadian volumes were higher. CPKC’s shipments were higher by +10.0% week over week, CN’s volumes were higher by +5.0% week-over-week. U.S. shipments were mostly lower. The NS was the sole gainer and was up by +5.0%. The CSX had the largest percentage decrease and was down by -9.0%.

We Continue to watch MEG Energy and Cenovus

Well folks, it look’s like the battle for MEG will be over with on Thursday of this week. Cenovus Energy Inc. is confident its proposed takeover of MEG Energy Corp. will gain shareholder approval on Thursday when voting resumes, president and chief executive officer Jon McKenzie said on Friday of last week.

“The delay is to give time for MEG to respond to a regulatory inquiry related to MEG’s consideration of the amended terms of the transaction,” said McKenzie at the company’s third quarter 2025 earnings call.

“The inquiry is associated with a complaint raised by a former employee of MEG who holds approximately 4,000 shares. We do not expect this inquiry to have any impact on the transaction.”

McKenzie said that there continues to be very strong support for the transaction from MEG shareholders, with 86 percent of shares voted in favor.

“We expect the vote to proceed as planned. Cenovus remains resolute in our commitment to this transaction.”

“When completed, this acquisition, combined with the organic growth we are already delivering across our business, is transformational to this company,” he added.

Subject to shareholder and court approval, Cenovus anticipates closing the transaction in November.

Total consideration for the transaction is expected to be a split of 50% cash and 50% Cenovus shares.

This equates to a maximum of approximately CAD$3.8 billion in cash in the issuance of 160 million shares on a fully-prorated basis, said the company.

We continue to watch Left-Wing Carney

Last week, left-wing Canadian Prime Minister Mark Carney found himself at the center of a diplomatic firestorm after he personally apologized to Donald Trump for a controversial Ontario government ad. The ad, which aired in major US TV markets and invoked Ronald Reagan’s anti-tariff rhetoric, infuriated Trump so deeply that he abruptly halted all trade negotiations with Canada and announced an additional 10% tariff on Canadian imports. In a move that some critics called “weak” and “misguided,” Carney told Ontario Premier Doug Ford not to run the ad—but Ford ignored his advice.

Carney admitted, “I’m the one who is responsible, in my role as Prime Minister, for the relationship with the president of the U.S.,” framing the entire incident as a federal failure to manage vital U.S.-Canada relations. While apologizing to Trump at the APEC summit, Carney emphasized the importance of the relationship but failed to secure any progress: trade talks remain frozen, and U.S. tariffs have only escalated.

For Canadian businesses—especially rail shippers and exporters—Carney’s approach has invited bipartisan criticism. His “diplomacy-by-apology” accomplished exactly nothing: higher tariffs, stalled negotiations, and an emboldened Ontario premier who openly defied federal wishes for cheap political points. With Carney under pressure to deliver generational investments in his upcoming budget, the trade gaffe is fueling doubts about his ability to stand up for Canada’s interests in a volatile global market.

This incident shows yet again why Carney’s political instincts are being questioned—he appears reactive, not proactive, and his deference to provincial leaders and foreign heads of state is costing Canada real economic pain. For rail and industrial sectors already struggling under American protectionism, this was the worst possible week to see Ottawa back down and fail to exert leverage when it counted.

We are Watching The “Green Old Deal”

The policy-driven “Green New Deal” model, which was forecast to create a new, high-value market for rail, is buckling under systemic economic pressure. In late October, Bill Gates, the world’s most prominent climate financier, signaled a major strategic pivot. In a new memo, he argued that while climate change is “serious,” it is “not civilization-ending,” and that the global focus must shift from emissions targets to adaptation and human welfare. Gates is backtracking on the method of mass-deploying current-gen renewables, shifting his focus to long-term innovation in nuclear power and clean steel.

This pivot validates the economic failures already unfolding. The 2023 cancellation of Ørsted’s massive Ocean Wind projects in New Jersey—which the developer blamed on high inflation, rising interest rates, and supply chain constraints—was just the start. This trend has now gone global. On October 31st, a major Dutch North Sea wind farm tender closed with zero bids, forcing the government to admit that government support is crucial. The same day, a key offshore wind contractor, Petrofac, entered administration, and in the U.S., Dominion Energy’s CEO confessed he was extremely disappointed in commissioning delays for the Charybdis, the first American-made installation vessel.

This economic collapse is fueling a political backlash, exemplified in the New Jersey governor’s race. With voters focused on “high utility bills,” Republican candidate Jack Ciattarelli is pledging to “ban wind farms” and “repeal unrealistic and unaffordable state mandates regarding electric vehicle sales,” pivoting instead to a “rational energy plan” that includes natural gas and nuclear. Nationally, 42 clean energy projects have been canceled or scaled back in 2025 alone, representing nearly $27 billion in lost investment. For rail customers, the promised boom market of shipping specialized rail-transportable blades is evaporating.

Instead, the U.S. Department of Energy (DOE) on Friday of last week issued a Notice of Funding Opportunity (NOFO) for up to $100 million in federal funding to refurbish and modernize the nation’s existing coal power plants. It follows the Department’s September announcement of its intent to invest $625 million to expand and reinvigorate America’s coal industry. The effort will support practical, high-impact projects that improve efficiency, extend plant lifetimes, and improve the performance of coal and natural gas use.

“For years, the Biden and Obama administrations relentlessly targeted America’s coal industry and workers, resulting in the closure of reliable power plants and higher electricity costs”, said U.S. Energy Secretary Chris Wright. “Thankfully, President Trump has ended the war on American coal and is restoring common-sense energy policies that put Americans first. These projects will help keep America’s coal plants operating and ensure the United States has the reliable and affordable power it needs to keep the lights on and power our future.”

This effort supports President Trump’s Executive Orders, Reinvigorating America’s Beautiful Clean Coal Industry and Strengthening the Reliability and Security of the United States Electric Grid, and advances his commitment to restore U.S. energy dominance.

This NOFO seeks applications for projects to design, implement, test, and validate three strategic opportunities for refurbishment and retrofit of existing American coal power plants to make them operate more efficiently, reliably, and affordably:

• Development, engineering, and implementation of advanced wastewater management systems capable of cost-effective water recovery and other value-added byproducts from wastewater streams.

• Engineering, design, and implementation of retrofit systems that enable fuel switching between coal and natural gas without compromising critical operational parameters.

• Deployment, engineering, and implementation of advanced coal-natural gas co-firing systems and system components, including highly fuel-flexible burner designs and advanced control systems, to maximize gas co-firing capacity to provide a low-cost retrofit option for coal plants while minimizing efficiency penalties.

DOE’s National Energy Technology Laboratory, under the purview of DOE’s Office of Fossil Energy, will manage projects selected under this NOFO.

The application deadline is January 7, 2026 by 5:00 PM ET.

We Continue to Watch the UP-NS Merger

A new, industry-shaping battle was declared on October 31st. CPKC and Canadian National have officially joined BNSF in publicly opposing the proposed $85 billion merger of Union Pacific and Norfolk Southern. The Canadian carriers launched websites detailing their concerns. CPKC warned the new UP Transcon would control an estimated 40% of all U.S. freight traffic and possess unrivaled leverage that would reduce the bargaining power of rail customers. BNSF’s messaging was more direct: “No customer is asking for a UP-NS merger to happen. It’s driven by Wall Street on the promise of a big shareholder payout”. This unified opposition from the other major Class I carriers signals the beginning of a major regulatory and public relations war over the future map of North American rail.

The unified Class I opposition to UP-NS is reshaping shipper negotiations. Carriers CPKC, CN, and BNSF are now incentivized to lock in customer commitments on rate stability and service levels before the merged UP-NS entity could extract concessions post-approval. Expect Q4 2025 and Q1 2026 to have aggressive customer capture campaigns, particularly for auto, grain, and intermodal volumes, which could mask underlying volume softness through contract switching rather than demand growth.

We are watching Key Economic Indicators

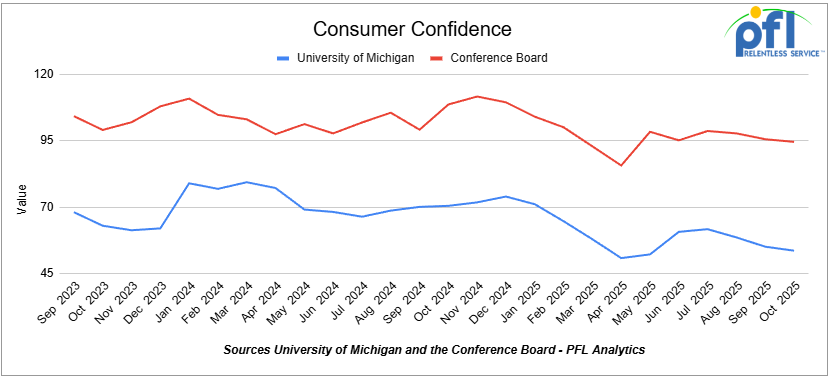

Consumer Confidence

The Index of Consumer Sentiment from the University of Michigan decreased from 55.1 in September to 53.6 in October.

The Conference Board Consumer Confidence Index decreased from 95.6 in September to 94.6 in October.

Lease Bids

- 30-50, 6000cf Steel Hopper located off of CSX or NS in East. For use in petcoke service. Period: 5 Years.

- 50, 5000CF Covered Hopper located off of UP or BN in Houston. For use in Fertilizer service. Period: 6 Months. Needed ASAP.

- 10, 2500CF Open Top Hopper located off of UP or BN in Texas. For use in aggregate service. Period: 5 years. Need Rapid Discharge Doors.

- 10, 25.5K Any Type Tank located off of CSX in Florida. For use in UCO service. Period: 2 Years.

- 15-20, 29K 117R Tank located off of NS or CSX in Ohio. For use in Ply Oil service. Period: 6-12 Months.

- 10, 30K 117R or 117J Tank located off of Any Class 1 in USA. For use in Glycerin service. Period: 1 year.

- 50, 23.5-25.5 DOT111 Tank located off of Any Class 1 in USA. For use in Asphalt service. Period: 5 years.

- 50-100, 33K 117J Tank located off of BN or UP in Bellview. For use in Butane/ service. Period: Sept-March.

- 4, 30K 117J Tank located off of Any Class 1 in Michigan. For use in Food Grade Ethanol service. Period: Multi year.

- 100, 21.9K 117J Tank located off of All Class 1s in Midwest. For use in CO2 service. Period: 6 months.

- 20, 25.5K Any Type Tank located off of UP in Point Comfort, TX. For use in Diethylene Glycol service. Period: 3-5 Years. No Lining Required.

- 100, 33K Pressure Tank located off of CN or CP in Canada. For use in Propane service. Period: Winter.

- 30-50, 30K Tank 117J located off of NS or CSX in Northeast. For use in C5 service. Period: 1 year.

Sales Bids

- 28, 3400CF Covered Hopper located off of UP BN in Texas. For use in Cement service.Cement Gates needed..

- 20, 17K Tank DOT111 located off of various class 1s in various locations. For use in corn syrup service.

- 120, Various Gondola Open-Top Aluminum Rotary located off of various class 1s in various locations. For use in Sulphur service.Built 2004 or later.

Lease Offers

- 60, 4750 Covered Hoppers located off of UP or BN in Eads, CO. Last used in Grain. Cars are currently clean. UP to 5 Years, 3 Hopper, Gravity Gate, Trough Hatches.

- 100, 6250 Covered Hoppers located off of UP in US. Last used in DDG. 1 Year term. Dirty to Dirty. Free move on UP..

- 25, 19.6K DOT111 Tanks located off of UP in US. Last used in Molases.

- 50, 20K DOT111 Tanks located off of UP or BN in Wichita Falls, TX. Last used in HCL.

- 50, 30K 117R Tanks located off of CSX, NS, or CN in Detroit. Last used in Diesel. Multiyear.

- 50, 20K 117J Tanks located off of All Class 1s in Multiple Locations. Last used in Styrene. Cars are currently moving.

- 22, 25.5K DOT111 Tanks located off of UP in Texas. Last used in Asphalt.

- 29, 25.5K 117J Tanks located off of BN or UP in Texas. Cars are currently clean.

- 40, 30K 117J Tanks located off of BNSF or UP in Houston. Cars are currently clean.

- 50, 5380 Covered Hoppers located off of BNSF or UP in Houston. Cars are currently clean. Available until Feburary.

- 21, 6351 Covered Hoppers located off of CN in Wisconsin. Last used in DDG. Available until February 2027.

- 29, 6500 Covered Hoppers located off of CN in Wisconsin. Last used in DDG. Available until February 2027.

- 100, 30K CPC1232 Tanks located off of UP or BN in Texas. Last used in Diesel.

- 100, 30K DOT117J Tanks located off of UP or BN in Texas. Last used in Gasoline.

- 100, 29K DOT117J Tanks located off of UP or BN in Texas. Last used in Gasoline. Coiled and Insulated.

Sales Offers

- 21, 50′ Boxcar Plate Cs located off of various class 1s in NM. End of Life.

- 3, 50′ Boxcar Plate Cs located off of various class 1s in multiple locations. End of Life.

- 27, 50′ Boxcar Plate Cs located off of various class 1s in PQ. End of Life.

- 100, 3250 Covered Hoppers located off of various class 1s in multiple locations. Sand Cars.

- 5, 2740 Mill Gondolas located off of various class 1s in NC. End of Life.

- 1, 2260 Mill Gondolas located off of various class 1s in AL. End of Life.

- 30, 2740 Mill Gondolas located off of various class 1s in multiple locations. End of Life.

- 21, 2740 Mill Gondolas located off of various class 1s in WA. End of Life.

- 9, 4750 Covered Hoppers located off of various class 1s in multiple locations. End of Life.

- 5, 4750 Covered Hoppers located off of various class 1s in multiple locations. End of Life.

- 50, 31.8K Tank CPC 1232s located off of UP or BN in TX. Requal Due in 2025.

- 100, 4600CF Open Top Hoppers located off of BN or CSX in Southeast.

Call PFL today to discuss your needs and our availability and market reach. Whether you are looking to lease cars, lease out cars, buy cars, or sell cars call PFL today at 239-390-2885

Live Railcar Markets

| CAT | Type | Capacity | GRL | QTY | LOC | Class | Prev. Use | Offer | Note |

|---|

PFL will be at the Following Conferences

- Where: Loews Arlington Hotel

- Attending: Brian Baker (239.297.4519), David Cohen (954-729-4774), and Curtis Chandler (239-405-3365)

- Conference Website

- Where: The Westin Galleria Dallas

- Attending: David Cohen (954-729-4774), and Curtis Chandler (239-405-3365)

- Conference Website

- Where: The Westin Galleria Dallas

- Attending: Brian Baker (239.297.4519)

- Conference Website