“The finest steel has to go through the hottest fire.” – Richard M. Nixon

Due to the Government Shutdown, we are unable to report last week’s Jobs Update. We apologize for the inconvenience.

Jobs Update

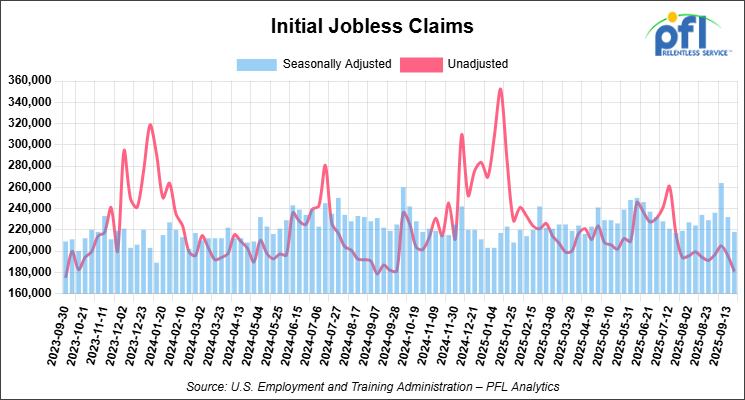

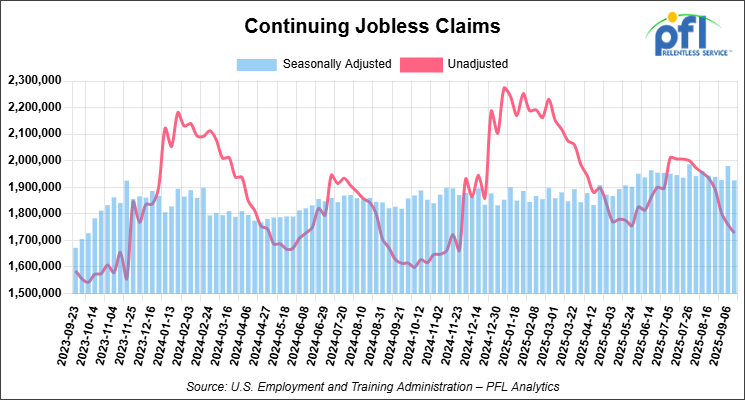

• Initial jobless claims seasonally adjusted for the week ending September 20, 2025 came in at 218,000, versus the adjusted number of 232,000 people from the week prior, down 14,000 people week over week.

• Continuing jobless claims came in at 1,926,000, versus the adjusted number of 1,980,000 people from the week prior, down 54,000 week-over-week.

Stocks closed higher on Friday of last week and higher week-over-week

The DOW closed higher on Friday of last week, up 472.51 points (1.01%), closing out the week at 47,207.12, up 1,016.51 points week-over-week. The S&P 500 closed higher on Friday of last week, up 53.25 points (0.79%), and closed out the week at 6,791.69, up 127.68 points week-over-week. The NASDAQ closed higher on Friday of last week, up 263.07 points (1.15%), and closed out the week at 23,204.87, up 524.90 points week-over-week.

In overnight trading, DOW futures traded higher and are expected to open at 47,658 this morning, up 262 points from Friday’s close.

Crude oil closed lower on Friday of last week and higher week-over-week

West Texas Intermediate (WTI) crude closed down -0.29 per barrel (-0.5%), to close at $61.50 on Friday of last week, but up $3.96 week-over-week. Brent crude closed down -0.05 per barrel (-0.1%), to close at $65.94, but up $4.65 week-over-week.

One Exchange WCS (Western Canadian Select) for December delivery settled on Friday of last week at US$11.95 below the WTI-CMA (West Texas Intermediate – Calendar Month Average). The implied value was US$49.04 per barrel.

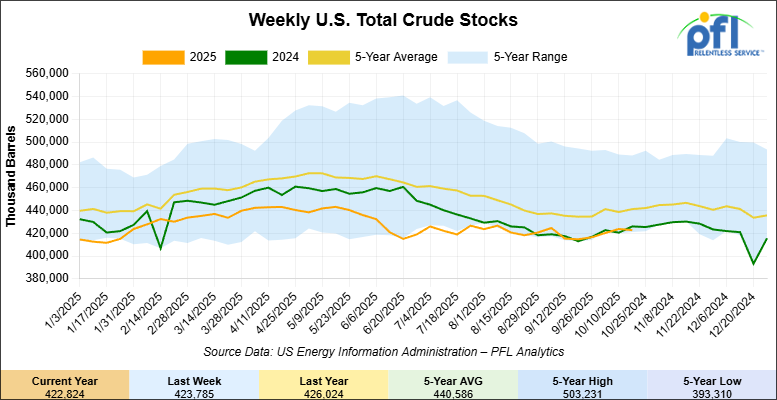

U.S. commercial crude oil inventories (excluding those in the Strategic Petroleum Reserve) decreased by 1 million barrels week-over-week. At 422.8 million barrels, U.S. crude oil inventories are 4% below the five-year average for this time of year.

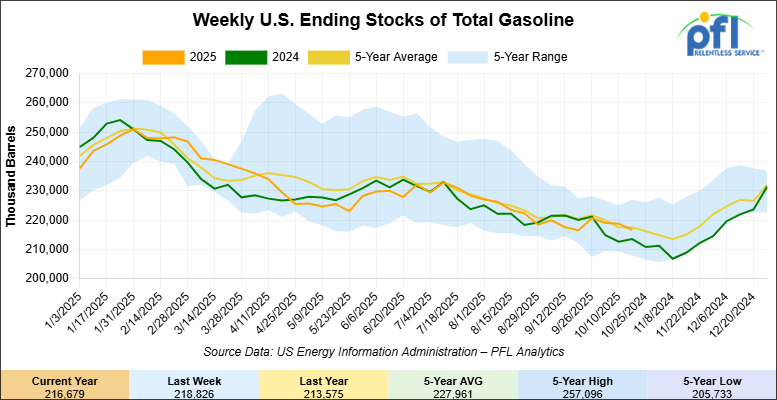

Total motor gasoline inventories decreased by 2.1 million barrels week-over-week and are slightly below the five-year average for this time of year.

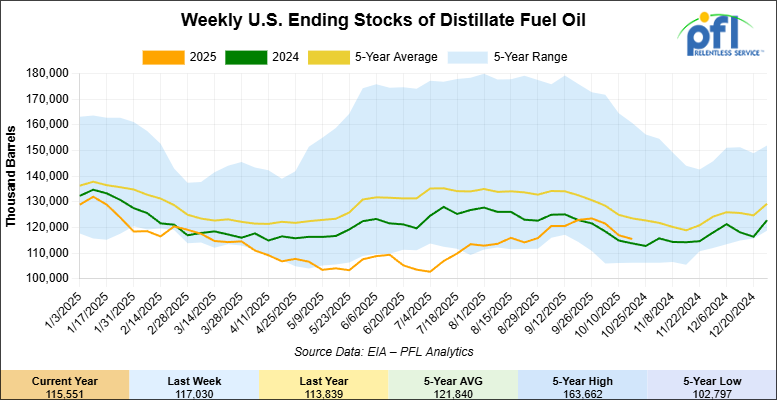

Distillate fuel inventories decreased by 1.5 million barrels week-over-week and are 7% below the five-year average for this time of year.

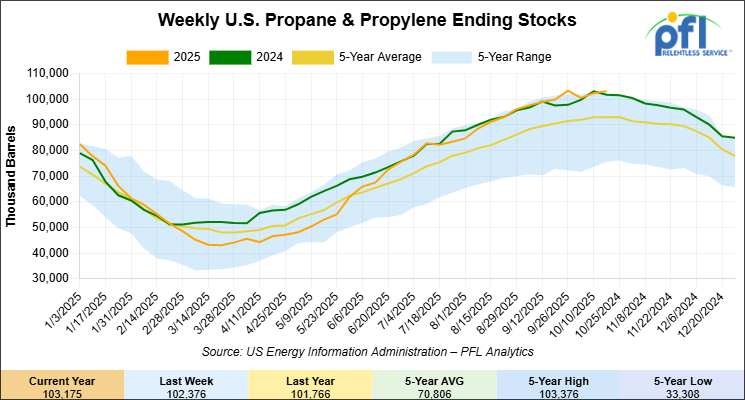

Propane/propylene inventories increased by 800,000 barrels week-over-week and are 12% above the five-year average for this time of year.

The EIA reported total U.S. propane/propylene inventories had a build of 800,000 barrels for the week ending October 17th, which was greater than industry expectations for an increase of 400,000 barrels and contrasts with the average draw of 324,000 barrels typically seen during this week.

Total U.S. propane/propylene stocks now stand at 103.2 million barrels, 1.4 million barrels (1%) higher than the same week in 2024 and 744,000 barrels (1%) above the five-year maximum. Inventories are also 10.6 million barrels (12%) above the five-year average, indicating that overall stocks remain strong compared with historical levels.

Weekly propane exports averaged 1.9 million barrels per day, down 242,000 barrels per day from the previous week. Exports were above the year-to-date average of 1.85 million barrels per day, but below both the four-week average of 1.98 million barrels per day and the 1.92 million barrels per day reported in the same week last year. Overall, export activity remains steady despite the week-over-week decline.

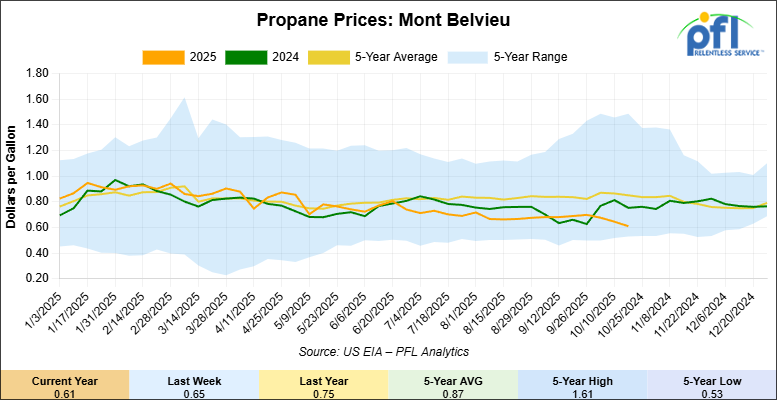

Propane prices closed at 61 cents per gallon on Friday of last week, down 4 cents week-over-week and down by 14 cents per gallon year-over-year.

Overall, total commercial petroleum inventories decreased by 4.2 million barrels during the week ending October 17, 2025.

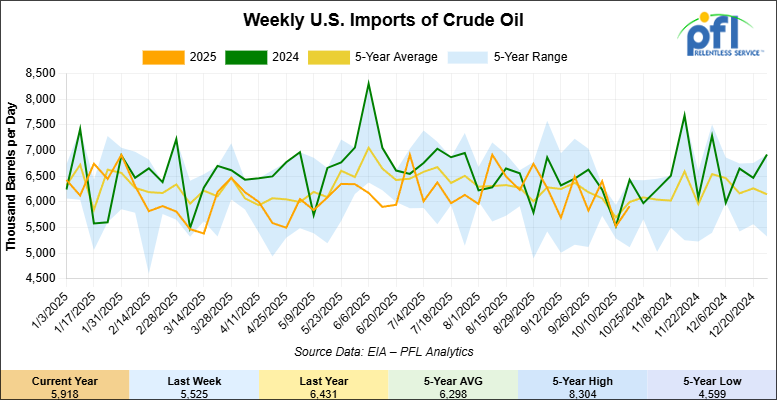

U.S. crude oil imports averaged 5.9 million barrels per day during the week ending October 17, 2025, an increase of 393,000 barrels per day week-over-week. Over the past four weeks, crude oil imports averaged 5.9 million barrels per day, 4.6% less than the same four-week period last year. Total motor gasoline imports (including both finished gasoline and gasoline blending components) averaged 505,000 barrels per day, and distillate fuel imports averaged 76,000 barrels per day during the week ending October 17, 2025.

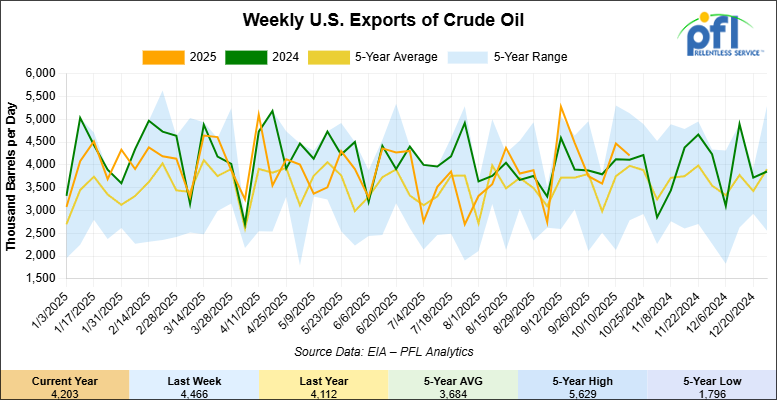

U.S. crude oil exports averaged 4.203 million barrels per day during the week ending October 17, 2025, a decrease of 263,000 barrels per day week-over-week. Over the past four weeks, crude oil exports averaged 4.003 million barrels per day.

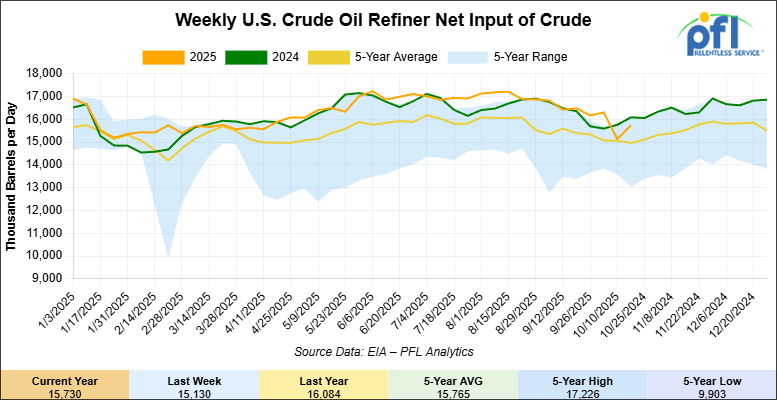

U.S. crude oil refinery inputs averaged 15.7 million barrels per day during the week ending October 17, 2025, which was 601 million barrels per day more week-over-week.

WTI futures are poised to open at $50.83, down 67 cents from Friday’s close.

North American Rail Traffic

Week Ending October 18, 2025

The Association of American Railroads (AAR) reported total U.S. rail traffic for the week ending October 18, 2025, at 497,854 carloads and intermodal units, down -2.6% compared with the same week last year. Total carloads for the week were 224,244, up 0.3%, while weekly intermodal volume totaled 273,610 containers and trailers, down -4.8% year-over-year.

Five of the ten major carload commodity groups posted gains compared with the same week in 2024. The largest increases were seen in nonmetallic minerals, up 3,253 carloads to 33,517; metallic ores and metals, up 1,461 carloads to 20,355; and chemicals, up 970 carloads to 32,046. Declines were led by grain, down 2,364 carloads to 21,011; miscellaneous carloads, down 1,521 to 8,413; and coal, down 1,057 to 57,604.

For the first forty-two weeks of 2025, U.S. railroads reported a cumulative volume of 9,326,053 carloads, up 2.0% compared with the same period last year. Intermodal shipments reached 11,399,777 units, an increase of 3.2% year-over-year. Combined U.S. rail traffic through the same period totaled 20,725,830 carloads and intermodal units, up 2.7% versus 2024.

Across North America, total rail traffic for the week ending October 18, 2025, amounted to 688,783 carloads and intermodal units, down 1.0% compared with last year. Carloads were unchanged at 330,151, while intermodal units fell 1.9% to 358,632. For the first forty-two weeks of the year, total North American rail volume reached 28,533,333 units, up 2.2% from 2024.

In Canada, total rail traffic for the week was 163,238 carloads and intermodal units, with carloads down -2.9% to 92,310 and intermodal traffic up +5.2% to 70,928. Cumulative Canadian rail traffic through week forty-two stood at 6,802,397 units, up 1.9% year-over-year.

In Mexico, rail traffic remained notably strong. Mexican railroads reported 13,597 carloads, up 19.2%, and 14,094 intermodal units, up 33.9% compared with the same week in 2024. Total weekly traffic in Mexico reached 27,691 units, up 26.2%. Despite these gains, cumulative Mexican rail volume through the first forty-two weeks of 2025 totaled 1,005,106 units, down 4.4% from the same point last year.

Source Data: AAR – PFL Analytics

North American Rig Count Summary

Rig Count

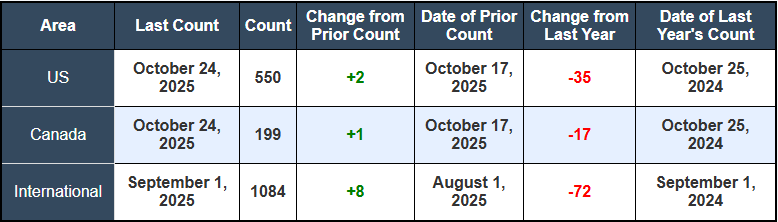

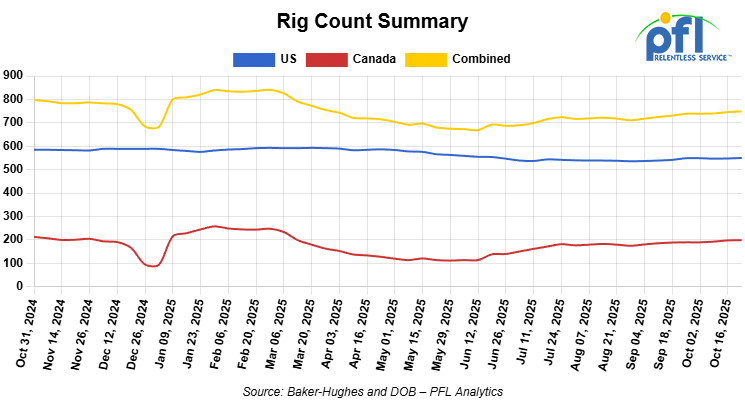

North American rig count was up by +3 rigs week-over-week. The US rig count was up by +2 rigs week-over-week, but down by -35 rigs year-over-year. The U.S. currently has 550 active rigs. Canada’s rig count was up by +1 rig week-over-week but down by -17 rigs year-over-year. Canada currently has 199 active rigs. Overall, year-over-year we are down by -52 rigs collectively.

We are watching a few things out there for you:

PFL Attended last week’s SEARS Meeting

PFL attended last week’s Southeast Association of Rail Shippers (SEARS) Fall Meeting in Buckhead, Georgia, joining industry peers, shippers, and rail partners from across the Southeast. The two-day event featured strong attendance with upwards of 400 attendees and valuable networking opportunities, with sessions covering topics such as shipper visibility, railcar leasing, government relations, and market outlooks. Keynote speakers included leaders from GMXT U.S.A., Union Pacific, GATX, and CSX, each sharing insights on rail performance and evolving supply-chain dynamics. Attendees also heard from analysts at FTR Transportation Intelligence and author Jim Davidson, who delivered an engaging motivational close to the conference. The event fostered meaningful discussions around efficiency, collaboration, and safety within the rail industry. PFL was proud to participate and remains committed to strengthening partnerships and delivering Relentless Service™ across North America. For more information as it relates to SEARS, contact PFL today.

We are Watching Cathcart

In a strategic move that signals a new chapter, Cathcart Rail is rebranding to Guardian Rail. The new name reflects a shift in the company’s philosophy and a renewed commitment to its core values of collaboration, consistency, integrity, and transparency. The change comes following the appointment of Scott Driggers on October 2, 2025. We had the pleasure of speaking with Scott about the changes he is making to the company on Thursday of last week.

The choice of the name “Guardian” is a deliberate one, meant to encapsulate the company’s vision of being a protector of its customers’ critical assets. “We see ourselves as standing watch over the safety, the safe operation, the effective operation, the quality, and the uptime of the railcars,” Scott explained in a recent phone call with PFL. The rebranding is more than just a name change; it represents a material move in how the company will deliver its services, with a deep focus on its role as a trusted service provider in the rail industry. Scott is a hands-on person and frequents all Cathcart shops from Jacksonville, FL.

Currently, Cathcart Rail operates one of the largest independent repair facility networks in the country, with over 110 locations across 30 states. Their services are comprehensive, positioning them as a one-stop solution for rail services and transportation, including repair facilities, field services, and rail operations.

Looking ahead, Guardian Rail plans to build on this strong foundation. The company’s immediate focus is on optimizing its existing operations and strengthening its repair facilities and field services. However, they are also actively exploring opportunities for expansion, including new shop locations and a potential move into the Canadian market if conditions are right. This forward-looking strategy, combined with a renewed focus on the values embodied in the “Guardian” name, positions the company in a new era of growth and enhanced customer experience.

We are watching Petroleum Carloads

The four-week rolling average of petroleum carloads carried on the six largest North American railroads rose to 28,669 from 28,516, which was an increase of +153 rail cars week-over-week. Canadian volumes were lower. CPKC’s shipments were lower by -3.0% week over week, CN’s volumes were lower by -5.0% week-over-week. U.S. shipments were mostly lower across the board. The NS was the sole gainer and was up by +3.0%. The CSX had the largest percentage decrease and was down by -7.0%.

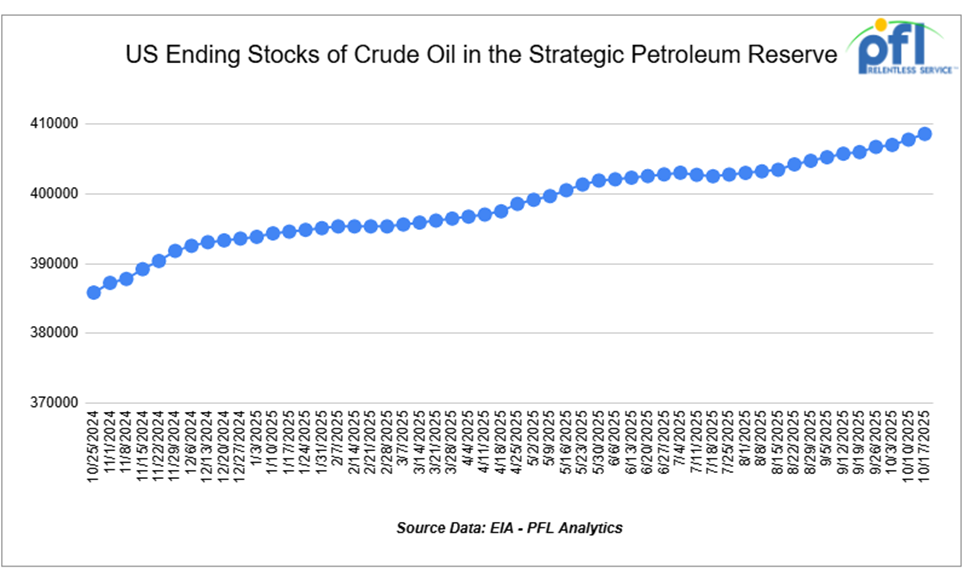

We are watching our Strategic Petroleum Reserves

The U.S. Department of Energy (DOE) announced last week a new solicitation to purchase one million barrels of crude oil for delivery to the Strategic Petroleum Reserve (SPR) at the Bryan Mound site. The solicitation is in accordance with the Working Families Tax Cut, which President Trump signed into law earlier this year. The legislation appropriated $171 million to begin refilling the SPR.

“After the previous administration recklessly drained the SPR for political purposes, President Trump promised to refill and manage this national security asset more responsibly,” said Secretary Wright. “Thanks to the President and Congress, we are able to begin the process of refilling the SPR. While this process won’t be complete overnight, these actions are an important step in strengthening our energy security and reversing the costly and irresponsible energy policies of the last administration.”

This announcement delivers on President Trump’s promise to rebuild America’s strategic strength and restore the reserve to full operational capacity. Currently, the SPR holds just over 400 million barrels of its 700-million-barrel capacity.

According to the White House, the SPR was severely weakened by the previous administration’s reckless 180-million-barrel drawdown in 2022, which incurred nearly $280 million in costs, delayed critical infrastructure maintenance, and put unprecedented wear and tear on storage and injection facilities.

The solicitation invites bids for an initial purchase of one million barrels of oil through a spot-price-indexed contract, with deliveries scheduled for December 2025 and January 2026. All notices of acquisition limit purchases to U.S. companies or U.S. subsidiaries of international companies with crude oil sourced from domestic production.

Bids for the solicitation are due no later than 11:00 A.M. CT on October 28, 2025.

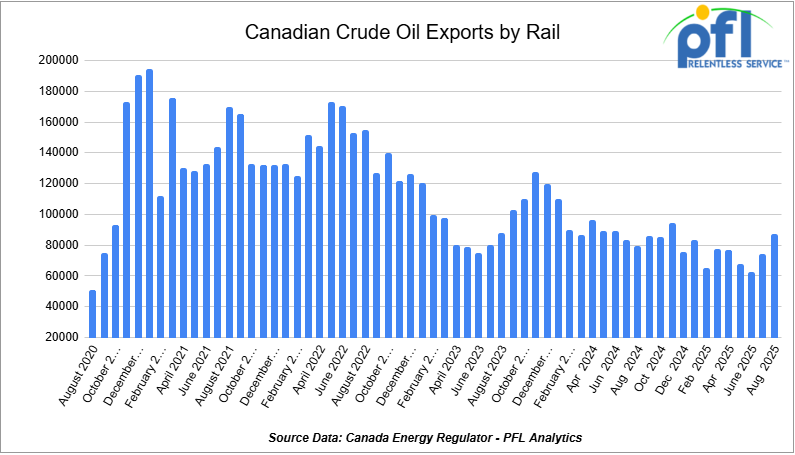

We are watching Canadian Crude by Rail

Crude by rail out of Canada increased month over month. The Canadian Energy regulator reported on October 24, that 87,141 barrels were exported per day during the month of August 2025, up from 74,031 barrels in July of 2025, an increase of 13,110 barrels per day, month over month and the largest volume exported by Canada since November of 2024 where 94,188 barrels per day were exported by Canada to the United States.

Crude by rail will always be necessary out of Canada for stranded oil not connected by pipelines. Raw bitumen, which is shipped as a non-haz product and is not able to flow in pipelines, is competitive with pipeline tolls and is a growing market to keep an eye on. Other factors would be existing long-term contractual commitments and basis – we really need to see basis WTI-CMA (West Texas Intermediate – Calendar Month Average) blowout to -18 per barrel for sustained periods of time to make economic sense. Current rail rates from Alberta to the U.S. Gulf Coast has averaged $15.36 per barrel, making rail competitive whenever WCS-WTI spreads exceed $18 per barrel, including quality adjustments.

Tank car lease rates for non-pressurized units remained stable, despite increased crude oil activity. This suggests adequate equipment supply for current market conditions.

Though there may be some slack in the system right now, room remains on the Transmountain pipeline, and production continues to grow in Alberta. At some point, we will hit a wall where crude will be trapped. When you ask? We don’t know, but are watching this one very closely.

We continue to watch Left Wing Carney

President Donald Trump abruptly ended all trade negotiations with Canada on Thursday of last week, citing what he called fraudulent and dishonest advertising by Ontario’s provincial government. The controversy centers on a television ad featuring former President Ronald Reagan that criticized tariffs, which ran during the World Series and cost approximately $75,000.

“Based on their egregious behavior, ALL TRADE NEGOTIATIONS WITH CANADA ARE HEREBY TERMINATED,” Trump wrote on Truth Social, accusing Canada of using the “FAKE” advertisement to interfere with U.S. Supreme Court decisions on tariffs.

The collapse of talks represents a significant failure for Prime Minister Carney, who was elected in April specifically on his promise to manage relations with Trump and secure relief from punishing 25% tariffs on Canadian automobiles and heavy-duty trucks. When asked if he would meet Carney during his Asia trip, Trump replied bluntly, “No, I don’t have any plan to”.

Ontario Premier Doug Ford announced Friday he would pause the ad on Monday to allow trade talks to resume, but the damage appears done. Before Trump’s announcement, Carney had already admitted that a trade deal was “no longer within reach” and relief on tariffs would be pushed to 2026 at the earliest.

The tariff impasse has cost thousands of Canadian jobs. Stellantis announced plans to move Jeep Compass production from Brampton to Illinois, eliminating 3,000 positions. GM halted electric vehicle production in Ingersoll, laying off hundreds, while Paccar announced 300 layoffs in Quebec. Oshawa’s GM plant will scale back production this fall with 700-1,000 additional layoffs.

Critics note Stellantis received $105 million from Ottawa to retool Ontario plants plus another $529 million in 2022 for EV modernization—only to take the money and shift production to the U.S.. Quebec ministers now promise to examine whether they can sue to recover taxpayer funds, though the jobs are unlikely to return.

Carney’s “Sacrifices” Speech Falls Flat

On Wednesday of last week, left-wing Carney delivered a primetime address to university students, announcing Canada must make “sacrifices” and promising to double non-U.S. exports over the next decade. He pledged to balance the operating budget in three years through spending cuts, but refused to specify what those cuts would be.

“We’ll have a budget and all aspects of the budget will reveal that,” Carney said when pressed on Thursday of last week.

The Parliamentary Budget Officer warned last month that Carney’s spending is “unsustainable,” with the deficit increasing to $68.5 billion this year—excluding major announcements like the $13 billion housing bureaucracy. The PBO’s Director stated bluntly: “This is not a funny fiscal outlook. It’s a really serious fiscal outlook. We don’t lightly use the word ‘unsustainable'”.

Carney has already broken his promise to “spend less,” with spending up 8% from Trudeau levels despite Canada posting the fastest-shrinking economy in the G7. Federal debt has doubled from $1.1 trillion in 2014/15 to a projected $2.2 trillion.

Over the weekend, President Donald Trump announced he’s adding an extra 10% tariff on Canadian imports.

We are Watching Russian Oil Sanctions

The U.S. Treasury on October 22nd, imposed blocking sanctions on Russia’s two largest oil companies, Rosneft and Lukoil, along with 34 subsidiaries. The companies account for over 55% of Russia’s oil production and approximately 5% of global oil supply.

“Given President Putin’s refusal to end this senseless war, Treasury is sanctioning Russia’s two largest oil companies that fund the Kremlin’s war machine,” said Treasury Secretary Scott Bessent. The action followed President Trump’s cancellation of a planned summit with Putin after productive discussions failed to yield progress toward ending the Ukraine conflict.

Companies have until November 21st to wind down transactions with the sanctioned entities. Foreign firms risk being sanctioned if they continue supporting the designated entities, potentially cutting them off from U.S. capital markets.

Oil markets reacted sharply. WTI crude surged nearly 6% above $60 per barrel, while Brent settled near $63. Indian refiners, who rely on Rosneft and Lukoil for approximately 60% of their Russian oil purchases, began moving to slash imports immediately. Chinese state oil majors also suspended purchases.

The sanctions were coordinated with allies. The UK targeted both companies last week, while the EU announced its 19th sanctions package on October 23, including a ban on Russian LNG imports.

With approximately 5% of the global oil supply potentially disrupted, analysts expect continued price volatility. Higher oil prices could boost crude-by-rail economics while increasing operating costs through higher diesel prices.

We Continue to watch MEG Energy and Cenovus

Just when you thought the battle for MEG between Strathcona and Cenovus was over. Last week MEG’s Shareholder Meeting was postponed from October 21, 2025, shareholders meeting.

The special meeting of holders of common shares of MEG Energy Corp. to vote on Cenovus Energy Inc.’s proposed acquisition of MEG has been postponed, pursuant to Cenovus exercising its contractual postponement right. The meeting will now be held on Oct. 30, 2025.

As of this morning, Cenovus has entered into a second amending agreement in a bid to acquire MEG. Under the new structure, each MEG shareholder can elect to receive either $30.00 in cash per share or 1.255 Cenovus common shares — subject to pro-ration based on a total cap of $3.8 billion in cash and 159.6 million Cenovus shares.

The pro-rated mix equates to roughly 50 percent cash and 50 percent Cenovus shares, or about $15.00 in cash and 0.6275 of a Cenovus share per MEG share. Based on Cenovus’s October 24, 2025 closing price, the offer values MEG shares at approximately $30.00 each.

In a major boost for the deal, Strathcona has signed a voting support agreement pledging to vote its MEG shares in favor of the transaction.

The deadline for submitting proxies has been extended to October 29, 2025, at 9 a.m. (Calgary time).

At the time of the postponement, approximately 63 percent of the MEG common shares represented by proxy or expected to be voted in person at the meeting are for the approval of the transaction, or over 75 percent excluding Strathcona Resources Ltd., which is assumed to have voted against, Cenovus noted.

The transaction is conditional upon, among other things, the approval by MEG shareholders holding at least 66 and two-thirds per cent of the MEG shares represented in person or by proxy at the meeting. We continue to watch this one.

We are Still Watching the UP-NS Merger

Opposition is growing on the merger, folks -The American Chemistry Council (ACC), whose members are major users of freight-rail service, last week sent a letter to President Trump and federal regulators asking that they scrutinize the proposed $85 billion merger of Union Pacific Railroad and Norfolk Southern Railway when the Class Is’ application reaches the Surface Transportation Board.

40 CEOs of chemical manufacturing companies who signed the letter warned that merging two of the nation’s largest railroads would harm competition by resulting in a huge concentration of power. Presently, only four major railroads control 90% of U.S. freight-rail traffic. Two of the four are UP and NS.

“Fewer railroads will mean fewer transportation options, and the merger threatens to make our U.S. manufacturing sites less competitive with the rest of the world,” the letter states. The letter cites major service disruptions that occurred after previous railroad mergers.

“The chemical industry is a cornerstone of American manufacturing and global trade,” said ACC President and CEO Chris Jahn in a press release. “Our facilities require dependable, competitive rail service to deliver essential materials across the country.”

Specifically, the ACC and its member companies called on the STB to adhere to rejecting any deal that fails to substantially enhance rail-to-rail competition and improve service. The UP-NS merger will be the largest railroad merger ever to go before the STB.

Last month, Trump indicated his support for the merger a week after meeting with UP CEO Jim Vena at the White House.

Both Railroads Report Strong Q3 2025 Earnings

Union Pacific reported third-quarter net income of $1.8 billion, or adjusted $3.08 per diluted share, up 12% from $2.75 in Q3 2024. Operating revenue of $6.2 billion grew 3%, driven by solid core pricing gains. Most notably, UP achieved a record-low adjusted operating ratio of 58.5%, an improvement of 180 basis points.

“Our third quarter results serve as a proof point that we are successfully executing on our strategy,” said Vena. “We have a historic opportunity with Norfolk Southern to create America’s first transcontinental railroad.”

Norfolk Southern reported Q3 railway operating revenue of $3.1 billion, up 2%. Adjusted diluted EPS grew 2% to $3.30, while the adjusted operating ratio improved to 63.3% from 63.4% in Q3 2024. The company achieved an all-time record in fuel efficiency.

Both railroads demonstrated operational efficiency gains and solid pricing power, strengthening the financial case for the proposed merger as they prepare for an extensive STB review.

We are Watching the CN

Canadian National Railway announced significant executive changes on October 20, naming Patrick Whitehead as Chief Operating Officer and Janet Drysdale as Chief Commercial Officer, effective immediately. Whitehead’s appointment follows the departure of Derek Taylor, ending CN’s unique dual-COO structure that had been in place since 2023.

Whitehead, 50, brings over 30 years of railroad experience and previously served as Executive Vice President and Chief Network Operating Officer since October 2023. Drysdale has nearly 30 years at CN and has been serving as interim Chief Commercial Officer since July 2025.

Concurrent with the leadership changes, CN is reportedly cutting approximately 400 managerial positions across Canada and the U.S. Notifications began around October 8, with additional terminations expected in the coming weeks.

The moves come as CN navigates challenging market conditions. In July, the company lowered its full-year outlook to “mid to high single-digit adjusted diluted EPS growth” for 2025, down from previous guidance of 10-15% growth.

We are watching Key Economic Indicators

Inflation

U.S. consumer prices rose less than expected in September, according to the latest Bureau of Labor Statistics report, keeping the door open for another Federal Reserve rate cut next week.

The Consumer Price Index (CPI) increased 0.3% for the month and 3.0% year-over-year, slightly below expectations of 0.4% and 3.1%. The annual reading marked a modest uptick from August’s 2.9%. Excluding food and energy, core CPI rose 0.2% on the month and 3.0% from a year ago, both undershooting forecasts and easing from prior 0.3% monthly gains in July and August.

Energy prices provided the biggest lift, with gasoline up 4.1% on the month, while food rose 0.2%. On an annual basis, energy prices gained 2.8%, food increased 3.1%, and shelter costs—which make up about one-third of the index—were up 3.6% year-over-year after a 0.2% monthly rise. Prices for new vehicles rose 0.8%, while used cars and trucks fell 0.4%.

Despite the jump in energy, inflation pressures remain moderate overall. Investors interpreted the softer CPI reading as reinforcing expectations for a quarter-point Fed rate cut at next week’s meeting, bringing the target range below the current 4.00%–4.25%.

Market reaction was positive: equities extended gains, while Treasury yields edged lower. Analysts noted that while inflation is no longer surprising to the upside, it remains comfortably below levels that would deter the Fed from further policy easing.

The report also serves as the final key inflation data before the Fed’s upcoming policy decision and provides a rare window into the economy amid the ongoing government shutdown. The BLS released the figures early to support Social Security cost-of-living adjustments (COLA) calculations.

Lease Bids

- 30-50, 6000cf Steel Hopper located off of CSX or NS in East. For use in petcoke service. Period: 5 Years.

- 50, 5000CF Covered Hopper located off of UP or BN in Houston. For use in Fertilizer service. Period: 6 Months. Bid: Negotiable.Needed ASAP.

- 10, 2500CF Open Top Hopper located off of UP or BN in Texas. For use in aggregate service. Period: 5 years. Bid: Negotiable.Need Rapid Discharge Doors.

- 10, 25.5K Any Type Tank located off of CSX in Florida. For use in UCO service. Period: 2 Years. Bid: Negotiable.

- 15-20, 29K 117R Tank located off of NS or CSX in Ohio. For use in Ply Oil service. Period: 6-12 Months. Bid: Negotiable.

- 10, 30K 117R or 117J Tank located off of Any Class 1 in USA. For use in Glycerin service. Period: 1 year. Bid: Negotiable.

- 50, 23.5-25.5 DOT111 Tank located off of Any Class 1 in USA. For use in Asphalt service. Period: 5 years. Bid: Negotiable.

- 50-100, 33K 117J Tank located off of BN or UP in Bellview. For use in Butane/ service. Period: Sept-March. Bid: Negotiable.

- 4, 30K 117J Tank located off of Any Class 1 in Michigan. For use in Food Grade Ethanol service. Period: Multi year. Bid: Negotiable.

- 100, 21.9K 117J Tank located off of All Class 1s in Midwest. For use in CO2 service. Period: 6 months. Bid: Negotiable.

- 20, 25.5K Any Type Tank located off of UP in Point Comfort, TX. For use in Diethylene Glycol service. Period: 3-5 Years. Bid: Negotiable.No Lining Required.

- 100, 33K Tank Pressure located off of CN or CP in Canada. For use in Propane service. Period: Winter. Bid: Negotiable.

Sales Bids

- 28, 3400CF Covered Hopper located off of UP BN in Texas. For use in Cement service. Bid: Negotiable.Cement Gates needed..

- 20, 17K Tank DOT111 located off of various class 1s in various locations. For use in corn syrup service. Bid: Negotiable.

- 120, Various Gondola Open-Top Aluminum Rotary located off of various class 1s in various locations. For use in Sulphur service. Bid: Negotiable.Built 2004 or later.

Lease Offers

- 60, 4750 Covered Hoppers located off of UP or BN in Eads, CO. Last used in Grain. Cars are currently clean. Offer: Negotiable. UP to 5 Years, 3 Hopper, Gravity Gate, Trough Hatches.

- 100, 6250 Covered Hoppers located off of UP in US. Last used in DDG. Offer: Negotiable. 1 Year term. Dirty to Dirty. Free move on UP..

- 25, 19.6K DOT111 Tanks located off of UP in US. Last used in Molases. Offer: Negotiable.

- 50, 20K DOT111 Tanks located off of UP or BN in Wichita Falls, TX. Last used in HCL. Offer: Negotiable.

- 50, 30K 117R Tanks located off of CSX, NS, or CN in Detroit. Last used in Diesel. Offer: Negotiable. Multiyear.

- 50, 20K 117J Tanks located off of All Class 1s in Multiple Locations. Last used in Styrene. Offer: Negotiable. Cars are currently moving.

- 22, 25.5K DOT111 Tanks located off of UP in Texas. Last used in Asphalt. Offer: Negotiable.

- 29, 25.5K 117J Tanks located off of BN or UP in Texas. Cars are currently clean. Offer: Negotiable.

- 40, 30K 117J Tanks located off of BNSF or UP in Houston. Cars are currently clean. Offer: Negotiable.

- 50, 5380 Covered Hoppers located off of BNSF or UP in Houston. Cars are currently clean. Offer: Negotiable. Available until Feburary.

- 21, 6351 Hoppers Covered located off of CN in Wisconsin. Last used in DDG. Offer: Negotiable. Available until February 2027.

- 29, 6500 Hoppers Covered located off of CN in Wisconsin. Last used in DDG. Offer: Negotiable. Available until February 2027.

Sales Offers

- 21, 50′ Boxcar Plate Cs located off of various class 1s in NM. Offer: Negotiable. End of Life.

- 3, 50′ Boxcar Plate Cs located off of various class 1s in multiple locations. Offer: Negotiable. End of Life.

- 27, 50′ Boxcar Plate Cs located off of various class 1s in PQ. Offer: Negotiable. End of Life.

- 100, 3250 Covered Hoppers located off of various class 1s in multiple locations. Offer: Negotiable. Sand Cars.

- 5, 2740 Mill Gondolas located off of various class 1s in NC. Offer: Negotiable. End of Life.

- 1, 2260 Mill Gondolas located off of various class 1s in AL. Offer: Negotiable. End of Life.

- 30, 2740 Mill Gondolas located off of various class 1s in multiple locations. Offer: Negotiable. End of Life.

- 21, 2740 Mill Gondolas located off of various class 1s in WA. Offer: Negotiable. End of Life.

- 9, 4750 Covered Hoppers located off of various class 1s in multiple locations. Offer: Negotiable. End of Life.

- 5, 4750 Covered Hoppers located off of various class 1s in multiple locations. Offer: Negotiable. End of Life.

- 50, 31.8K Tank CPC 1232s located off of UP or BN in TX. Offer: Negotiable. Requal Due in 2025.

- 100, 4600CF Open Top Hoppers located off of BN or CSX in Southeast. Offer: Negotiable. N/A.

Call PFL today to discuss your needs and our availability and market reach. Whether you are looking to lease cars, lease out cars, buy cars, or sell cars call PFL today at 239-390-2885

Live Railcar Markets

| CAT | Type | Capacity | GRL | QTY | LOC | Class | Prev. Use | Offer | Note |

|---|

PFL will be at the Following Conferences

- Where: Loews Arlington Hotel

- Attending: Brian Baker (239.297.4519), David Cohen (954-729-4774), and Curtis Chandler (239-405-3365)

- Conference Website

- Where: The Westin Galleria Dallas

- Attending: David Cohen (954-729-4774), and Curtis Chandler (239-405-3365)

- Conference Website

- Where: The Westin Galleria Dallas

- Attending: Brian Baker (239.297.4519)

- Conference Website