“A creative man is motivated by the desire to achieve, not by the desire to beat others.” – Ayn Rand

Due to the Government Shutdown, we are unable to report last week’s Jobs Update. We apologize for the inconvenience.

Jobs Update

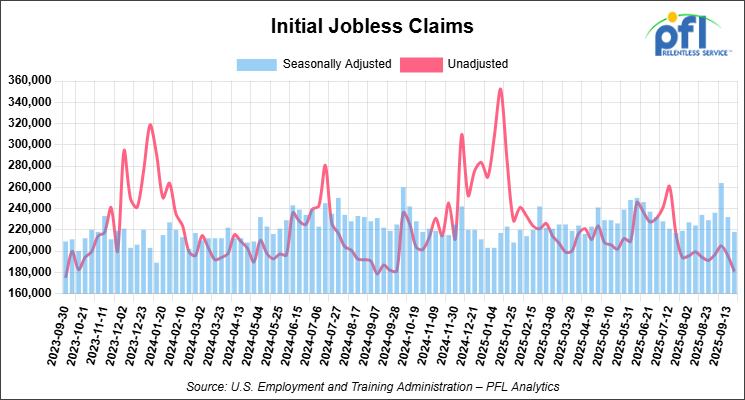

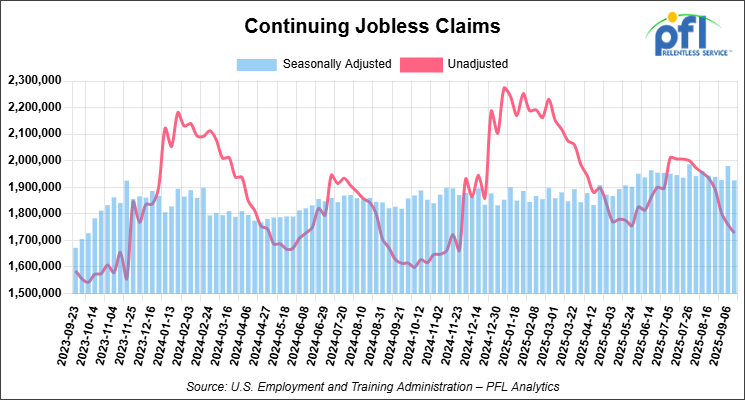

• Initial jobless claims seasonally adjusted for the week ending September 20, 2025 came in at 218,000, versus the adjusted number of 232,000 people from the week prior, down 14,000 people week over week.

• Continuing jobless claims came in at 1,926,000, versus the adjusted number of 1,980,000 people from the week prior, down 54,000 week-over-week.

Stocks closed higher on Friday of last week and higher week-over-week

The DOW closed higher on Friday of last week, up 238.37 points (0.52%), closing out the week at 46,190.61 up 711.01 points week-over-week. The S&P 500 closed higher on Friday of last week, up 34.94 points (0.53%), and closed out the week at 6,664.01, up 111.51 points week-over-week. The NASDAQ closed higher on Friday of last week, up 117.44 points (0.52%), and closed out the week at 22,679.97, up 475.54 points week-over-week.

In overnight trading, DOW futures traded higher and are expected to open at 46,466 this morning, up 85 points from Friday’s close.

Crude oil closed higher on Friday of last week, but lower week-over-week

West Texas Intermediate (WTI) crude closed up 8 cents per barrel (0.14%), to close at $57.54 on Friday of last week, down $1.36 week-over-week. Brent crude closed up 23 cents per barrel (0.38%), to close at $61.29, down $1.44 week-over-week.

One Exchange WCS (Western Canadian Select) for November delivery settled on Friday of last week at US$10.35 below the WTI-CMA (West Texas Intermediate – Calendar Month Average). The implied value was US$46.59 per barrel.

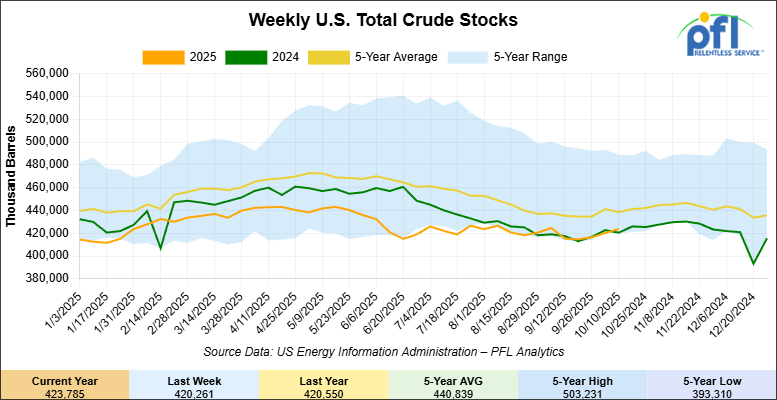

U.S. commercial crude oil inventories (excluding those in the Strategic Petroleum Reserve) increased by 3.5 million barrels week-over-week. At 423.8 million barrels, U.S. crude oil inventories are 4% below the five-year average for this time of year.

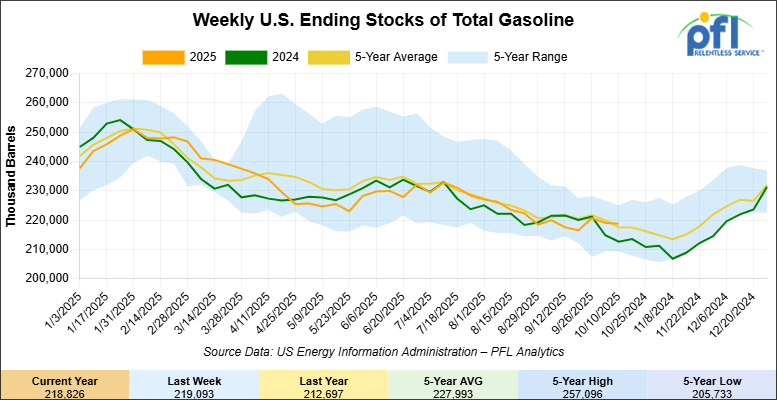

Total motor gasoline inventories decreased by 300,000 barrels week-over-week and are slightly below the five-year average for this time of year.

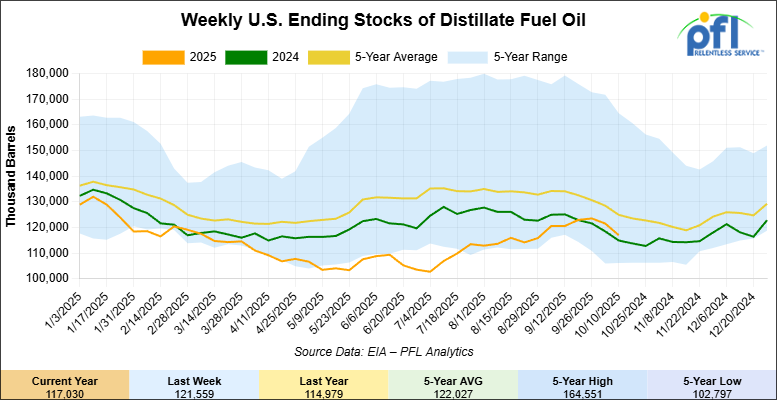

Distillate fuel inventories decreased by 4.5 million barrels week-over-week and are 7% below the five-year average for this time of year.

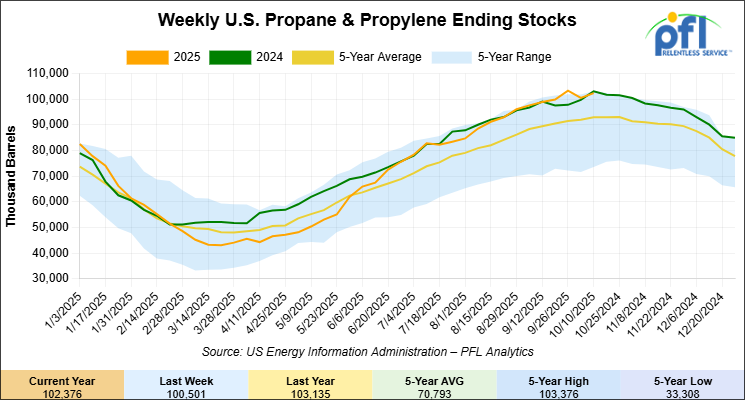

Propane/propylene inventories increased by 1.9 million barrels week-over-week and are 11% above the five-year average for this time of year.

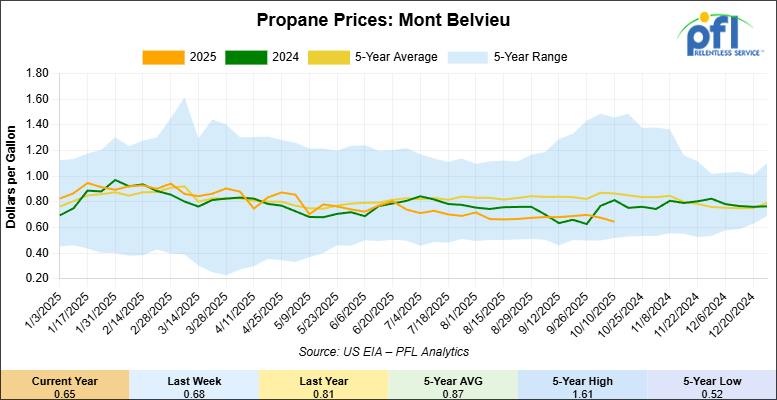

Propane prices closed at 65 cents per gallon on Friday of last week, down 3 cents week-over-week and down by 16 cents per gallon year-over-year.

Overall, total commercial petroleum inventories increased by 1.7 million barrels during the week ending October 10, 2025.

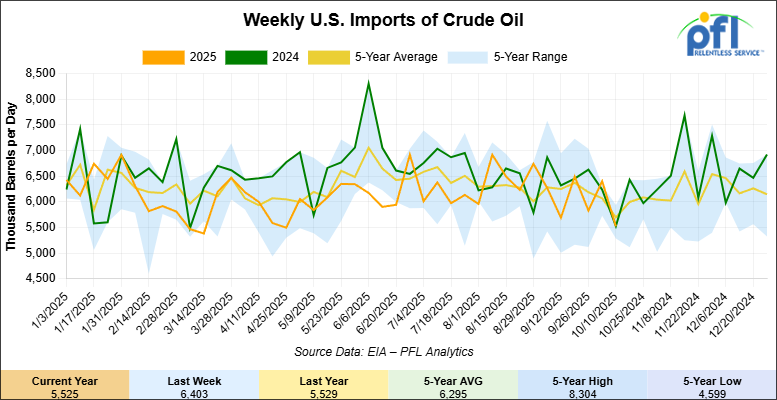

U.S. crude oil imports averaged 5.5 million barrels per day during the week ending October 10, 2025, a decrease of 878,000 barrels per day week-over-week. Over the past four weeks, crude oil imports averaged 6.1 million barrels per day, 2.4% less than the same four-week period last year. Total motor gasoline imports (including both finished gasoline and gasoline blending components) last week averaged 532,000 barrels per day, and distillate fuel imports averaged 160,000 barrels per day during the week ending October 10, 2025.

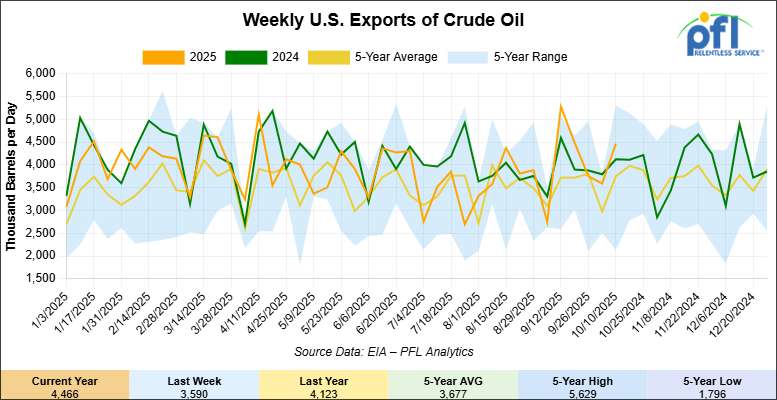

U.S. crude oil exports averaged 4.466 million barrels per day during the week ending October 10, 2025, an increase of 876,000 barrels per day week-over-week. Over the past four weeks, crude oil exports averaged 4.072 million barrels per day.

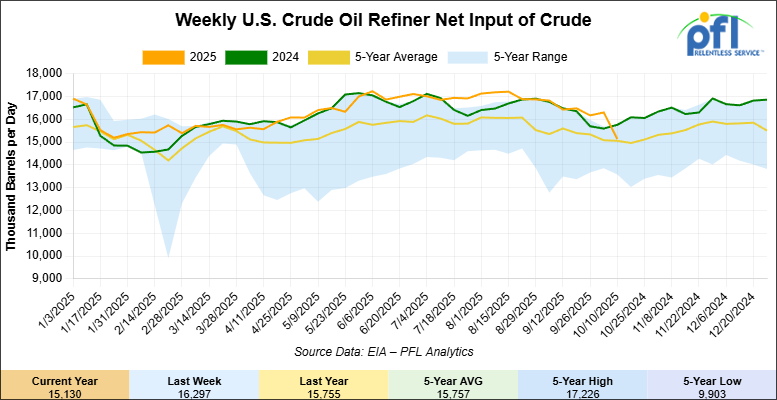

U.S. crude oil refinery inputs averaged 15.1 million barrels per day during the week ending October 10, 2025, which was 1.2 million barrels per day less week-over-week.

WTI futures are poised to open at $57.04, down 11 cents from Friday’s close.

North American Rail Traffic

Week Ending October 11, 2025

For the week ending on October 11, 2025, total North American rail traffic totaled 692,467 carloads and intermodal units, up 0.3% compared with the same week last year. Carloads increased 1.5%, while intermodal traffic slipped 0.8% year-over-year, reflecting modest softness in cross-border container movements.

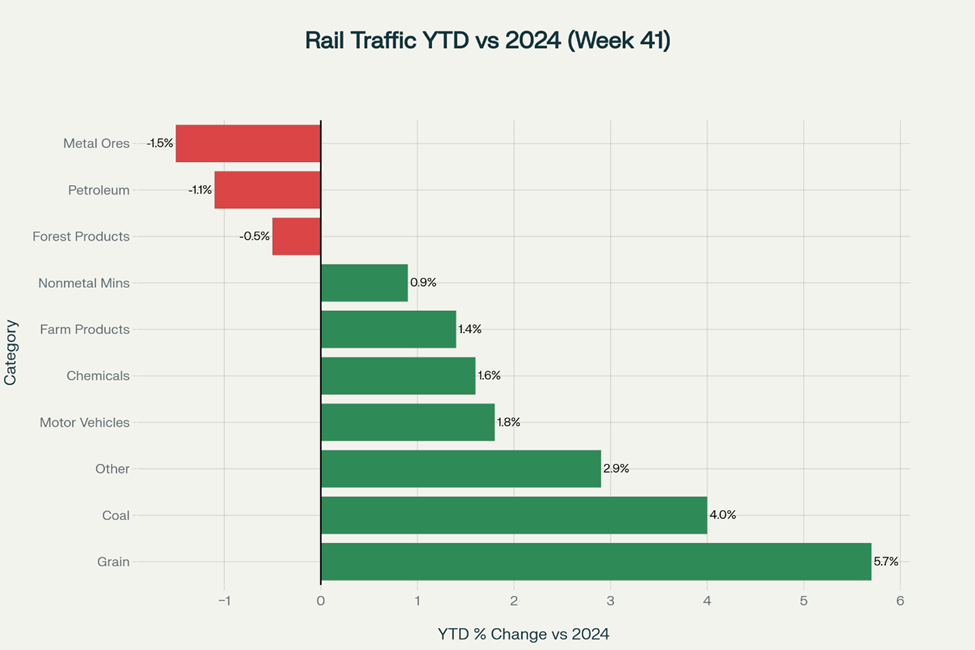

In the United States, total weekly rail traffic was 498,462 carloads and intermodal units, down 1.3% from the same week in 2024. Total carloads rose 1.2% to 224,562, while intermodal volume declined 3.3% to 273,900 containers and trailers. Of the ten major carload commodity groups tracked by the Association of American Railroads, five reported year-over-year increases.

The largest gains came from nonmetallic minerals, up by 1,985 carloads to 32,448. This strong performance points to robust activity in construction and infrastructure projects, which continue to be a key driver of freight demand. While broader economic reports indicate a sluggish manufacturing sector, the significant growth in this specific rail category suggests that capital-intensive construction is providing a solid foundation of demand for the freight network. Coal was up by 605 carloads to 58,858 and chemicals were also up by 548 carloads to 31,048.

Declines were led by metallic ores and metals, down 816 carloads to 18,456; miscellaneous carloads, down 324 to 8,923; and grain, down 85 to 23,434. Grain shipments presented a paradox in week 41, posting a slight decline of 0.4%, or 85 carloads, right in the middle of the peak harvest season. This dip is especially notable given that year-to-date grain volumes are exceptionally strong, up 6% over 2024. The disconnect is not a sign of a weak harvest but rather of shifting logistical patterns. A strong corn harvest in the Southeastern U.S. is satisfying local and regional demand, reducing the need for long-haul rail shipments from the Midwest. Concurrently, sluggish export demand for soybeans has created a capacity surplus in the secondary rail market, pushing freight costs to six-year lows and indicating lower-than-expected volumes are being tendered for shipment.

For the first 41 weeks of 2025, U.S. railroads reported cumulative volume of 9,101,809 carloads, up 2.1% from the same point in 2024, and 11,126,167 intermodal units, up 3.4%. Combined U.S. traffic totaled 20,227,976 carloads and intermodal units, an increase of 2.8% year-over-year.

In Canada, total rail traffic reached 165,594 carloads and intermodal units for the week, down 1.6% compared with last year. Canadian railroads handled 94,937 carloads, down 3.2%, and 70,657 intermodal units, up 0.8%. Cumulative Canadian volume through the first 41 weeks of 2025 stood at 6,639,159 units, up 1.9% from the same period in 2024.

Canadian Pacific Kansas City (CPKC) demonstrated exceptional operational execution in its grain franchise, a performance that was completely invisible in the national-level statistics. For the week ending October 11, CPKC transported a remarkable 766,871 metric tonnes of Canadian grain and grain products, the highest weekly volume the railroad has moved since October 2020. This record haul, up 23% from the same week last year, stands in stark contrast to the aggregate data for Canada, which showed a 3.2% decline in total Canadian carloads for the week. It’s a clear example of why carrier-specific performance is critical to watch in a mixed market.

In Mexico, rail activity surged compared with the prior year. Mexican railroads originated 13,506 carloads, up 70.7%, and 14,905 intermodal units, up 60.5%, for a total of 28,411 carloads and intermodal units, up 65.4% from last year. This performance is a statistical outlier that should be viewed with extreme caution, as it stands in direct opposition to the cumulative data for the first 41 weeks of 2025, which show that total Mexican volume is down 5.0% year-over-year. Such a sharp, single-week spike is highly unlikely to represent a fundamental market reversal. The most probable explanation is a “base effect,” where traffic in the same week of 2024 was exceptionally low, or a “recovery surge” from a prior disruption.

As mentioned in last week’s report, a new rule took effect in Mexico last week requiring all fuel tank trucks to display QR codes identifying the cargo’s legal origin and destination. This is part of a wider government crackdown on illegal fuel trade and signals increased regulatory scrutiny on the entire fuel supply chain. Despite the strong weekly gains, cumulative Mexican rail volume through the first 41 weeks of 2025 totaled 977,415 units, down 5.0% compared with the same point in 2024.

Source Data: AAR – PFL Analytics

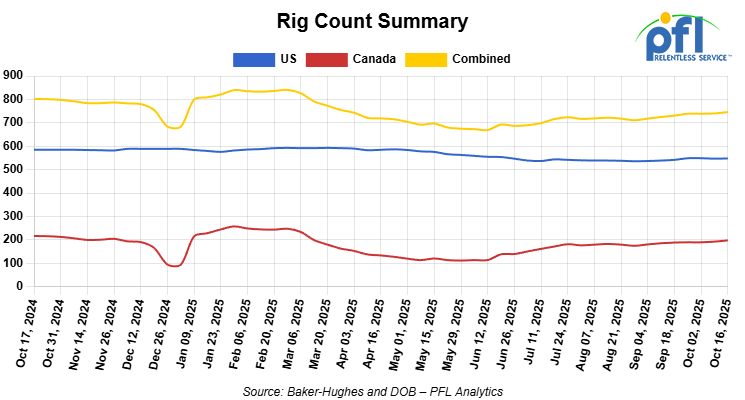

Rig Count

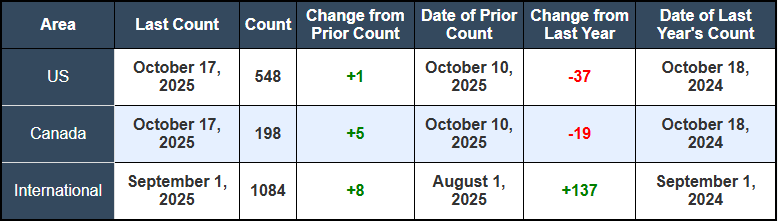

North American rig count was up by +6 rigs week-over-week. The US rig count was up by +1 rig week-over-week, but down by -37 rigs year-over-year. The U.S. currently has 548 active rigs. Canada’s rig count was up by +5 rigs week-over-week but down by -19 rigs year-over-year. Canada currently has 198 active rigs. Overall, year-over-year we are down by -56 rigs collectively.

North American Rig Count Summary

We are watching a few things out there for you:

PFL Attended Last Week’s Tank Car Committee Meeting

PFL attended the AAR Tank Car Committee (TCC) meetings in Addison, Texas last week, in full force – we had a table – Curtis Chandler, David Cohen, Brian Baker and Cyndi Popov were present representing PFL. Industry leaders reviewed active dockets and standards affecting the North American tank car fleet. While no immediate rule changes were adopted, several technical discussions signaled where standards may be heading — particularly around manway performance and bottom outlet equipment.

A significant portion of the agenda was dedicated to Docket T94.32 – Hinged-Bolted Manway Covers, which remains under evaluation due to ongoing operational concerns. Industry representatives raised recurring issues tied to:

- Gasket performance and risk of vapor leaks over time

- Lid behavior during opening, including incidents where hinged covers can swing or fall back unexpectedly

- Bolt torque and flange compression, especially on older car designs where uneven sealing can occur

A task force was established earlier this year to explore whether current M-1002 standards provide enough functional guidance – not just on dimensions, but on lid stability, opening angles, and required stop mechanisms. The goal is to ensure safer handling during loading and inspection without imposing unnecessary design overhauls.

Although the committee did not issue new circulars during this session, recent Circular CPC-1431 (July 2025) remained part of the broader conversation. That circular clarified requirements for bottom fittings protection and external ball valves, reinforcing AAR’s focus on containment integrity across all service equipment — manways included.

In parallel, Docket T100.22.2 continues to advance proposals for expanded component tracking, which would eventually require standardized documentation for critical fittings such as manways, valves, and relief devices. While still in discussion, this could signal future changes to reporting or qualification practices. Docket T94.32 changes will impact inspection procedures, gasket specifications, and retrofit expectations.

The direction of discussion was clear: The committee is prioritizing reliability at known leak points and evaluating long-term service practices across aging fleets.

PFL remains committed to supporting safe, compliant, and operationally efficient tank car service across North America. Further updates will follow upon release of official post-meeting records or circulars from AAR. Please call PFL if you want any more information as it relates to the latest AAR meeting.

We are Watching the CN

Canadian National (CN) is making strategic moves to reposition itself for future growth. The company announced a major partnership with Congebec, a specialist in refrigerated logistics, to expand its cold chain capabilities with a new state-of-the-art facility in Calgary. This investment in a high-value market occurred as reports emerged of a corporate restructuring and job cuts around October 8. The simultaneous moves signal a deliberate corporate pivot, reallocating capital and resources from legacy operations to fund investments in higher-margin ventures. On the regulatory front, CN also won a significant federal appeal that forces a review of how Canadian rail shipping rates are set, a decision that could have long-term positive impacts on the railway’s revenue and pricing power.

We are Still Watching the UP-NS Merger

Opposition to the proposed Union Pacific-Norfolk Southern merger continues to build. At an industry conference on October 14, a rail industry attorney questioned the railroads’ claims that their merger would enhance competition. The attorney pointed out that both UP and NS had previously argued against the “one-lump” theory—an economic doctrine supporting vertical integration—when they opposed the CPKC merger in 2023, a stance they now seem to be ignoring for their own transaction. This comes as BNSF, the nation’s second-largest carrier, has already publicly condemned the deal and stated it is not interested in merging with another railroad, raising concerns that a combined UP-NS would create a massive carrier with no real rival.

We are Watching Canadian Pipelines

The push to expand Canada’s energy export capacity is facing a classic battle between infrastructure investment and political uncertainty. Enbridge is moving forward with plans to add 150,000 b/d of capacity to its Mainline system by using drag-reducing agents on Lines 93 and 67, with a target completion of October 2027. This effort to optimize existing infrastructure comes as the industry grows increasingly frustrated with the federal government’s noncommittal stance on repealing the oil tanker ban on British Columbia’s northern coast. Alberta Premier Danielle Smith is championing a new 1 million barrel per day pipeline to the coast, but pipeline developers consider the project “a pipeline to nowhere” as long as the tanker ban remains in place, sidelining private capital.

We Continue to Watch Left Wing Carney

The political stalemate over Canada’s west coast energy export strategy continues, with left wing Prime Minister Mark Carney’s government remaining noncommittal on the future of the oil tanker ban on British Columbia’s northern coast. When asked on October 10 if his government was considering repealing the ban—a move the industry sees as essential for any new pipeline project—Carney’s response was simply, “It depends”. His government is attempting to balance the goal of becoming an “energy superpower” with its climate commitments, signaling that any new oil production must be offset by “material” carbon capture and storage.

The industry’s frustration is palpable. Enbridge CEO Greg Ebel pointed to the C$500 million his company lost on the doomed Northern Gateway project as a “scar” from past attempts to build nation-building projects, emphasizing that “winning requires decisions, urgent, confident, investible decisions”.

We are watching The Green Old Deal and the UN

Folks, you are not going to believe this one, but the UN was going to impose a carbon tax on shipping, but instead postponed a vote on the global carbon tax after a Trump-led pushback.

The President vowed that America will not adhere to a proposed carbon tax ‘in any way, shape, or form.’

The United Nations has postponed a vote on a proposal to impose the world’s first global carbon tax on shipping, delaying the decision by one year.

The rule was expected to come up for a vote last week as part of the U.N. International Maritime Organization’s (IMO) “Net-Zero Framework.” But a majority of member nations voted to defer it after failing to reach consensus amid U.S. opposition.

Backed by the European Union and Brazil, the plan seeks to raise billions from carriers that exceed new emissions limits, channeling the revenue toward climate adaptation and clean-fuel projects in developing nations.

Washington and Riyadh led the opposition. Saudi Arabia introduced a motion Friday of last week to delay discussions for one year, which passed with 57 countries in favor and 49 opposed.

The Trump administration came out forcefully against the measure last week, calling it an “unconstitutional global tax” that would drive up energy and consumer prices. In a series of statements, President Donald Trump, Secretary of State Marco Rubio, and U.S. ambassador to the U.N. Mike Waltz vowed that the United States would vote a “hard no” when delegates met in London on Friday and urged allies to do the same.

Leading up to the vote the President wrote on Truth Social “I am outraged that the International Maritime Organization is voting in London this week to pass a global Carbon Tax.” “The United States will NOT stand for this Global Green New Scam Tax on Shipping, and will not adhere to it in any way, shape, or form. We will not tolerate increased prices on American Consumers OR the creation of a Green New Scam Bureaucracy to spend YOUR money on their Green dreams. Stand with the United States, and vote NO in London tomorrow!”

Administration officials argue the framework would give unelected international bureaucrats the power to tax U.S. companies and consumers while doing little to cut global emissions.

Lease Bids

- 30-50, 6000cf Steel Hopper located off of CSX or NS in East. For use in petcoke service. Period: 5 Years.

- 50, 5000CF Covered Hopper located off of UP or BN in Houston. For use in Fertilizer service. Period: 6 Months. Bid: Negotiable.Needed ASAP.

- 10, 2500CF Open Top Hopper located off of UP or BN in Texas. For use in aggregate service. Period: 5 years. Bid: Negotiable.Need Rapid Discharge Doors.

- 10, 25.5K Any Type Tank located off of CSX in Florida. For use in UCO service. Period: 2 Years. Bid: Negotiable.

- 15-20, 29K 117R Tank located off of NS or CSX in Ohio. For use in Ply Oil service. Period: 6-12 Months. Bid: Negotiable.

- 10, 30K 117R or 117J Tank located off of Any Class 1 in USA. For use in Glycerin service. Period: 1 year. Bid: Negotiable.

- 50, 23.5-25.5 DOT111 Tank located off of Any Class 1 in USA. For use in Asphalt service. Period: 5 years. Bid: Negotiable.

- 50-100, 33K 117J Tank located off of BN or UP in Bellview. For use in Butane/ service. Period: Sept-March. Bid: Negotiable.

- 4, 30K 117J Tank located off of Any Class 1 in Michigan. For use in Food Grade Ethanol service. Period: Multi year. Bid: Negotiable.

- 100, 21.9K 117J Tank located off of All Class 1s in Midwest. For use in CO2 service. Period: 6 months. Bid: Negotiable.

- 20, 25.5K Any Type Tank located off of UP in Point Comfort, TX. For use in Diethylene Glycol service. Period: 3-5 Years. Bid: Negotiable.No Lining Required.

- 100, 33K Tank Pressure located off of CN or CP in Canada. For use in Propane service. Period: Winter. Bid: Negotiable.

Sales Bids

- 28, 3400CF Covered Hopper located off of UP BN in Texas. For use in Cement service. Bid: Negotiable.Cement Gates needed..

- 20, 17K Tank DOT111 located off of various class 1s in various locations. For use in corn syrup service. Bid: Negotiable.

- 120, Various Gondola Open-Top Aluminum Rotary located off of various class 1s in various locations. For use in Sulphur service. Bid: Negotiable.Built 2004 or later.

Lease Offers

- 60, 4750 Covered Hoppers located off of UP or BN in Eads, CO. Last used in Grain. Cars are currently clean. Offer: Negotiable. UP to 5 Years, 3 Hopper, Gravity Gate, Trough Hatches.

- 100, 6250 Covered Hoppers located off of UP in US. Last used in DDG. Offer: Negotiable. 1 Year term. Dirty to Dirty. Free move on UP..

- 25, 19.6K DOT111 Tanks located off of UP in US. Last used in Molases. Offer: Negotiable.

- 50, 20K DOT111 Tanks located off of UP or BN in Wichita Falls, TX. Last used in HCL. Offer: Negotiable.

- 50, 30K 117R Tanks located off of CSX, NS, or CN in Detroit. Last used in Diesel. Offer: Negotiable. Multiyear.

- 50, 20K 117J Tanks located off of All Class 1s in Multiple Locations. Last used in Styrene. Offer: Negotiable. Cars are currently moving.

- 22, 25.5K DOT111 Tanks located off of UP in Texas. Last used in Asphalt. Offer: Negotiable.

- 29, 25.5K 117J Tanks located off of BN or UP in Texas. Cars are currently clean. Offer: Negotiable.

- 40, 30K 117J Tanks located off of BNSF or UP in Houston. Cars are currently clean. Offer: Negotiable.

- 50, 5380 Covered Hoppers located off of BNSF or UP in Houston. Cars are currently clean. Offer: Negotiable. Available until Feburary.

Sales Offers

- 21, 50′ Boxcar Plate Cs located off of various class 1s in NM. Offer: Negotiable. End of Life.

- 3, 50′ Boxcar Plate Cs located off of various class 1s in multiple locations. Offer: Negotiable. End of Life.

- 27, 50′ Boxcar Plate Cs located off of various class 1s in PQ. Offer: Negotiable. End of Life.

- 100, 3250 Covered Hoppers located off of various class 1s in multiple locations. Offer: Negotiable. Sand Cars.

- 5, 2740 Mill Gondolas located off of various class 1s in NC. Offer: Negotiable. End of Life.

- 1, 2260 Mill Gondolas located off of various class 1s in AL. Offer: Negotiable. End of Life.

- 30, 2740 Mill Gondolas located off of various class 1s in multiple locations. Offer: Negotiable. End of Life.

- 21, 2740 Mill Gondolas located off of various class 1s in WA. Offer: Negotiable. End of Life.

- 9, 4750 Covered Hoppers located off of various class 1s in multiple locations. Offer: Negotiable. End of Life.

- 5, 4750 Covered Hoppers located off of various class 1s in multiple locations. Offer: Negotiable. End of Life.

- 50, 31.8K Tank CPC 1232s located off of UP or BN in TX. Offer: Negotiable. Requal Due in 2025.

- 100, 4600CF Open Top Hoppers located off of BN or CSX in Southeast. Offer: Negotiable. N/A.

Call PFL today to discuss your needs and our availability and market reach. Whether you are looking to lease cars, lease out cars, buy cars, or sell cars call PFL today at 239-390-2885

Live Railcar Markets

| CAT | Type | Capacity | GRL | QTY | LOC | Class | Prev. Use | Offer | Note |

|---|

PFL will be at the Following Conferences

- Where: Loews Arlington Hotel

- Attending: Brian Baker (239.297.4519), David Cohen (954-729-4774), and Curtis Chandler (239-405-3365)

- Conference Website

- Where: The Westin Galleria Dallas

- Attending: David Cohen (954-729-4774), and Curtis Chandler (239-405-3365)

- Conference Website

- Where: The Westin Galleria Dallas

- Attending: Brian Baker (239.297.4519)

- Conference Website