“If opportunity doesn’t knock, build a door.” – Milton Berle

Due to the Government Shutdown, we are unable to report last week’s Jobs Update. We apologize for the inconvenience.

Jobs Update

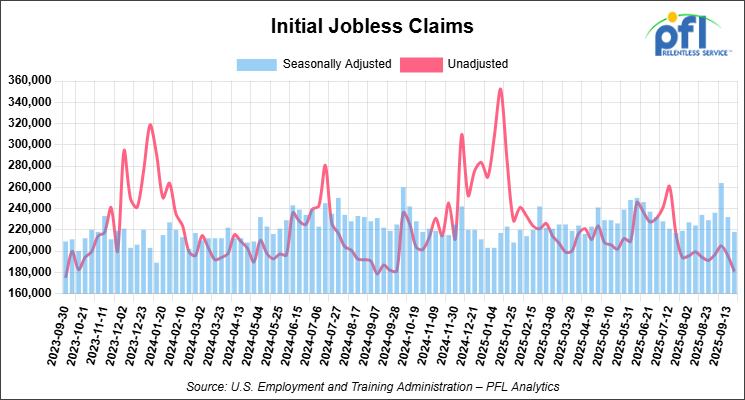

• Initial jobless claims seasonally adjusted for the week ending September 20, 2025 came in at 218,000, versus the adjusted number of 232,000 people from the week prior, down 14,000 people week over week.

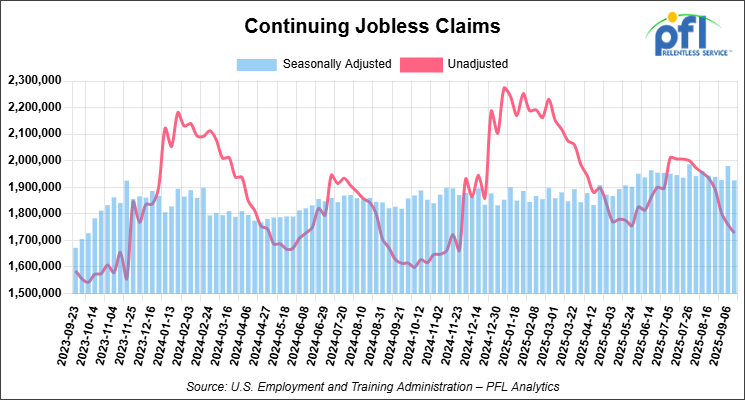

• Continuing jobless claims came in at 1,926,000, versus the adjusted number of 1,980,000 people from the week prior, down 54,000 week-over-week.

Stocks closed lower on Friday of last week and lower week-over-week

The DOW closed lower on Friday of last week, down -878.82 points (-1.90%), closing out the week at 45,479.60, down -1,278.68 points week-over-week. The S&P 500 closed lower on Friday of last week, down -182.61 points (-2.71%), and closed out the week at 6,552.51, down -163.29 points week-over-week. The NASDAQ closed lower on Friday of last week, down -820.20 points (-3.56%), and closed out the week at 22,204.43, down -576.38 points week-over-week.

In overnight trading, DOW futures traded higher and are expected to open at 46,158 this morning, up 452 points from Friday’s close.

Crude oil closed lower on Friday of last week and lower week-over-week

West Texas Intermediate (WTI) crude closed down -2.61 per barrel (-4.24%), to close at $58.90 on Friday of last week, and down $1.98 week-over-week. Brent crude closed down -2.49 per barrel (-3.82%), to close at $62.73, and down $1.80 week-over-week.

One Exchange WCS (Western Canadian Select) for November delivery settled on Friday of last week at US$10.55 below the WTI-CMA (West Texas Intermediate – Calendar Month Average). The implied value was US$50.39 per barrel.

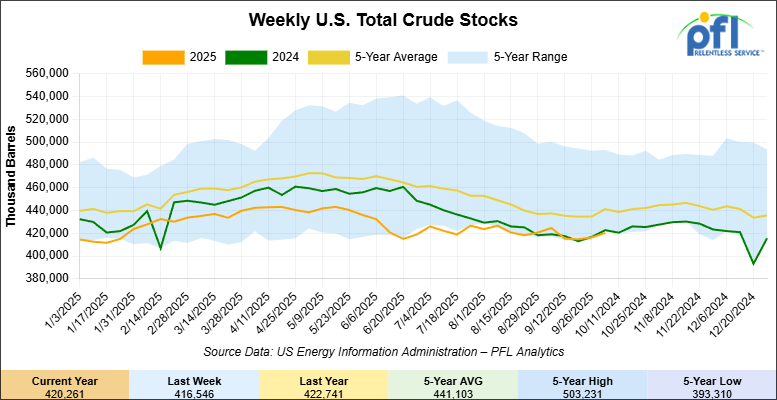

U.S. commercial crude oil inventories (excluding those in the Strategic Petroleum Reserve) increased by 3.7 million barrels week-over-week. At 420.3 million barrels, U.S. crude oil inventories are 4% below the five-year average for this time of year.

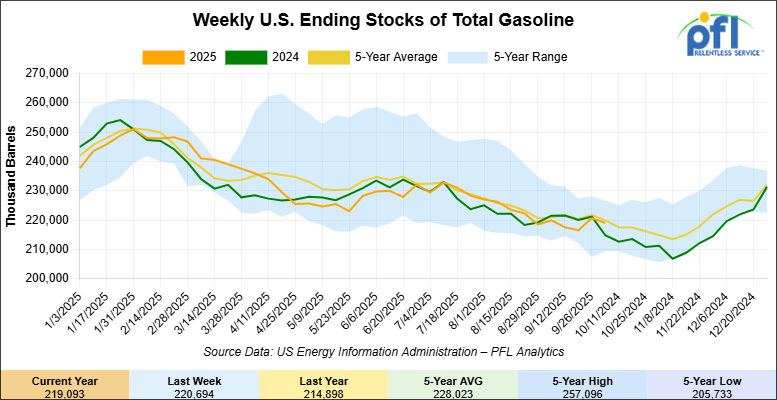

Total motor gasoline inventories decreased by 1.6 million barrels week-over-week and are 1% below the five-year average for this time of year.

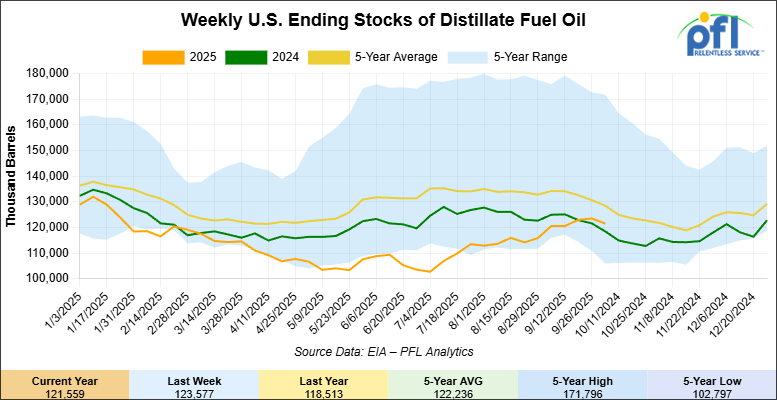

Distillate fuel inventories decreased by 2 million barrels week-over-week and are 6% below the five-year average for this time of year.

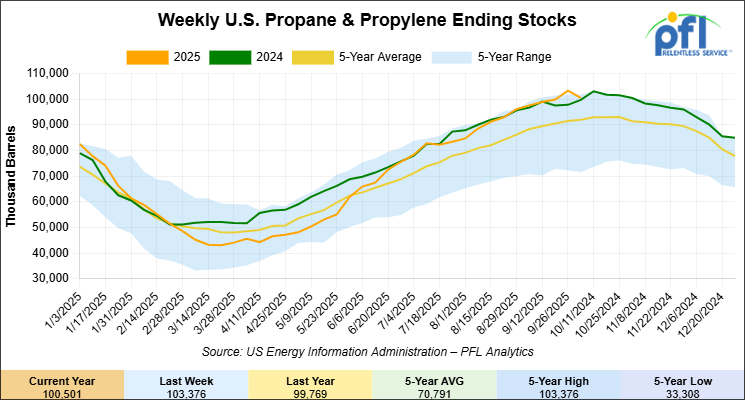

Propane/propylene inventories decreased by 2.9 million barrels week-over-week and are 9% above the five-year average for this time of year.

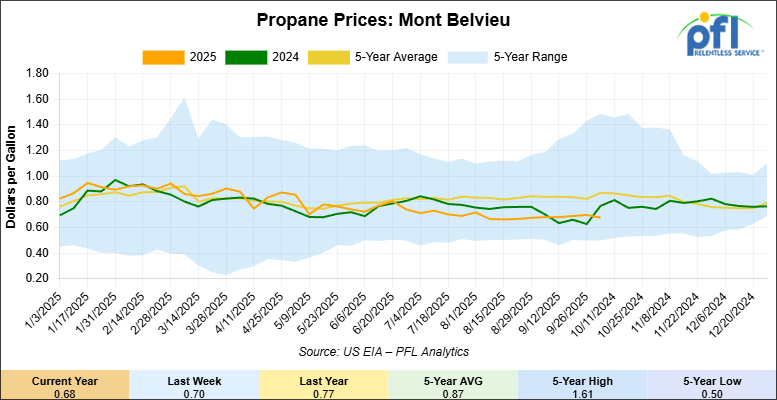

Propane prices closed at 68 cents per gallon on Friday of last week, down 2 cents week-over-week and down by 9 cents per gallon year-over-year.

Overall, total commercial petroleum inventories decreased by 1.2 million barrels during the week ending October 3, 2025.

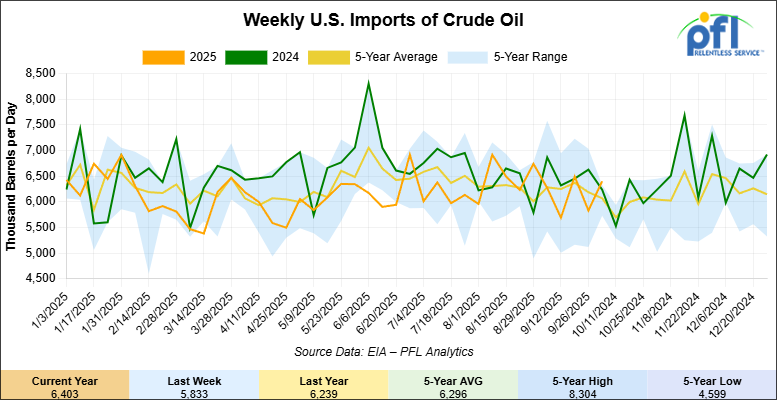

U.S. crude oil imports averaged 6.4 million barrels per day during the week ending October 3, 2025, an increase of 570,000 barrels per day week-over-week. Over the past four weeks, crude oil imports averaged 6.1 million barrels per day, 4.8% less than the same four-week period last year. Total motor gasoline imports (including both finished gasoline and gasoline blending components) averaged 627,000 barrels per day, and distillate fuel imports averaged 132,000 barrels per day during the week ending October 3, 2025.

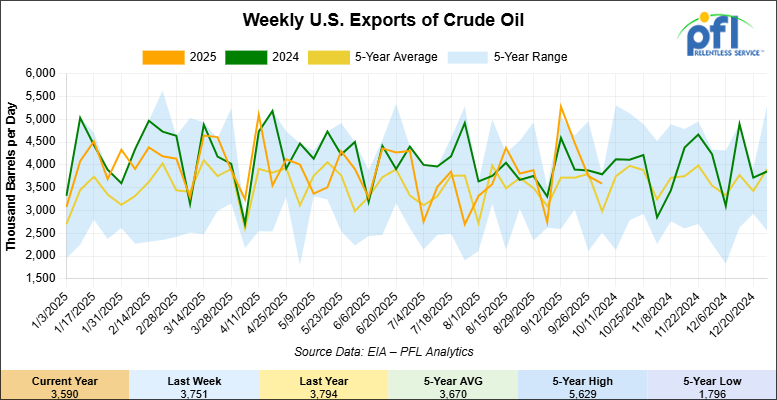

U.S. crude oil exports averaged 3.59 million barrels per day during the week ending October 3, 2025, a decrease of 161,000 barrels per day week-over-week. Over the past four weeks, crude oil exports averaged 4.276 million barrels per day.

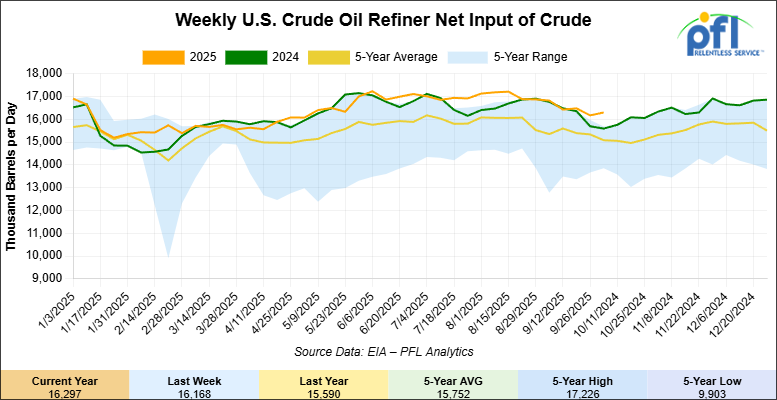

U.S. crude oil refinery inputs averaged 16.3 million barrels per day during the week ending October 3, 2025, which was 130,000 barrels per day more week-over-week.

WTI futures are poised to open at $59.96, up $1.06 from Friday’s close.

Due to the Government Shutdown we are unable to report last week’s Rail Traffic Data. We apologize for the inconvenience.

North American Rail Traffic

Week Ending September 24, 2025:

Total North American weekly rail volumes were down (-3.62%) in week 39, compared with the same week last year. Total Carloads for the week ending September 24, 2025 were 324,445, down (-2.05%) compared with the same week in 2024, while weekly Intermodal volume was 340,982, down (-5.06%) year over year. 9 of the AAR’s 11 major traffic categories posted year-over-year decreases. The largest decrease came from Forest Products (-18.02%), while the largest increase was Grain (+5.54%).

In the East, CSX’s total volumes were up (+1.93%), with the largest decrease coming from Forest Products (-17.17%), while the largest increase came from Intermodal Units (+7.61%). NS’s total volumes were down (-5.00%), with the largest increase coming from Motor Vehicles and Parts (+7.78%), while the largest decrease came from Coal (-25.51%).

In the West, BNSF’s total volumes were down (-1.11%), with the largest increase coming from Coal (+35.31%), while the largest decrease came from Chemicals (-9.02%). UP’s total volumes were down (-5.81%), with the largest increase coming from Grain (+42.44%), while the largest decrease came from Intermodal Units (-15.62%).

In Canada, CN’s total volumes were down (-2.59%), with the largest increase coming from Coal (+35.31%), while the largest decrease came from Other (-32.65%). CPKCS’s total volumes were down (-19.55%), with the largest increase coming from Nonmetallic Minerals (+5.77%), while the largest decrease came from Forest Products (-65.54%).

Source Data: AAR – PFL Analytics

Rig Count

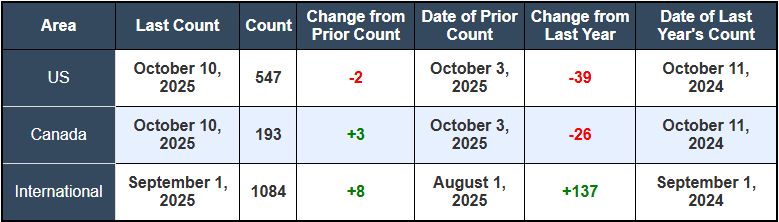

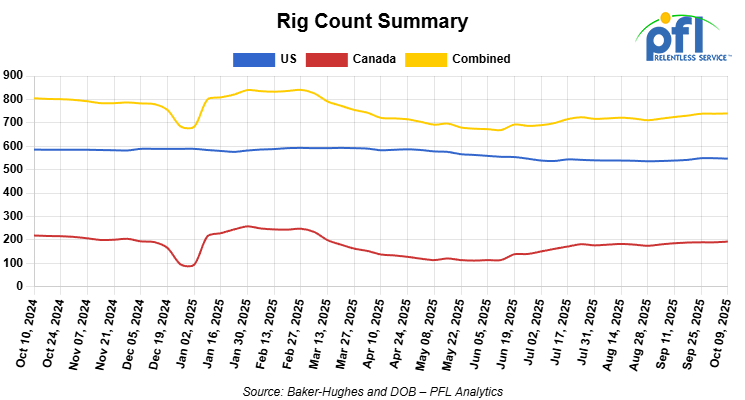

North American rig count was up by +1 rig week-over-week. The US rig count was down by -2 rigs week-over-week, and down by -39 rigs year-over-year. The US currently has 547 active rigs. Canada’s rig count was up by +3 rigs week-over-week and down by -26 rigs year-over-year. Canada currently has 193 active rigs. Overall, year-over-year we are down by -65 rigs collectively.

North American Rig Count Summary

We are watching a few things out there for you:

We are watching Petroleum Carloads

The four-week rolling average of petroleum carloads carried on the six largest North American railroads rose to 28,441 from 28,337 which was an increase of +104 rail cars week-over-week. Canadian volumes were higher. CPKC’s shipments were higher by +5.0% week over week, CN’s volumes were higher by 1.0% week-over-week. The BN had the largest percentage increase and was up by +7.0%. The NS had the largest percentage decrease and was down by -4%.

We are Watching FourPoint Resources

FourPoint Resources announced on October 9 it will double crude-by-rail capacity at Energy Transfer’s Price River terminal by Q4 2026. The terminal expansion will feature a newly constructed continuous loop track to streamline rail logistics and a railcar load rack capable of loading 140,000/bpd. The expansion will also add 140,000/bbls of heated storage and nine new rail loading arms at eastern Utah’s only major crude transloading facility.

This expansion comes alongside the official launch and rebranding of the crude previously known as Uinta Wax or Yellow Wax. Going forward, FourPoint will market the crude as American Premium Uinta (APU). “As volatility continues to disrupt foreign crude imports, APU offers American refineries a premium, domestic alternative. This terminal expansion strengthens our ability to deliver that product consistently and at scale – supporting energy independence and fueling the production of American-made goods with American crude.” said George Solich, Chief Executive Officer and Chairman of FourPoint.

The Uinta Basin has emerged as one of the few regions in the Lower 48 positioned for meaningful production growth. Unlike other major U.S. basins facing declining output, the Uinta Basin is a uniquely resource-rich region with a long runway of remaining tier-one drilling locations. Operators in the region attest that the Basin has many similar characteristics to the Permian – with one key meaningful difference for rail. Eastern Utah’s crude lacks direct pipeline access to refineries, making rail the primary transport option. Energy Transfer’s expansion is necessary because Uinta Basin Waxy crude is very difficult to transport via pipeline and pipeline development cannot match production growth in remote basins. This additional crude-by-rail capacity will compete for the same coiled and insulated tank car fleet serving other markets.

The project represents the infrastructure investment paradox facing energy markets: billions invested in rail terminals while the tank car fleet remains constrained by regulations, rising costs, financing limits, and other market uncertainties.

We are Watching Ethanol Production Surge

Spot Ethanol markets were falling into the first week of October as physical trading remained slow. Then, newly released EIA data midweek showed a big uptick in Ethanol production which sent spot prices tumbling further. Spot prices at Argo dipped as low as 1.785/gal, down 23.5 cts/gal week over week, the lowest level since August. Ethanol shipping by Rail under Rule 11 railcar terms from Argo was fetching $1.96/gal at the beginning of the week and sank to about $1.75/gal by Thursday. Railed ethanol prices fell elsewhere, including ethanol shipping from Nebraska and Iowa as well as delivered Ethanol to Nevada and New Mexico.

Ethanol production increases were largely expected headed into October, but the EIA reported a production jump of 7.6% week-over-week as Ethanol plants collectively averaged 1.071 MM/bpd in fuel grade production. This print put U.S. Ethanol production about 8% above its weekly output average.

The production spike reversed three consecutive weeks of declines and immediately stressed Midwest rail networks already operating near capacity. Unlike petroleum with multiple transport options, Ethanol depends very largely on rail due to its specialized handling requirements. The production surge demonstrates rail’s role as essential surge capacity, but also highlights the volatility risks when biofuel production rapidly increases.

We are Watching UP and the NS

Merger drama continues to heat up as opposition to the proposed Union Pacific-Norfolk Southern merger intensified significantly last week, with BNSF Railway publicly condemning the deal as “costly, unnecessary, anti-competitive, and bad for the U.S. economy” during an October 6 industry conference. The criticism marked the most direct attack yet from a competing railroad and signaled that the industry’s second-largest carrier would actively oppose the consolidation.

BNSF argued that a combined UP-NS network would control approximately 45% of the U.S. freight rail market and create thousands of “captive shippers” with no competitive transportation alternatives. The company’s public opposition carried significant weight given BNSF’s own substantial market position and Warren Buffett’s Berkshire Hathaway ownership, which can provide financial resources to sustain a prolonged regulatory challenge.

Regulatory challenges typically extend review timelines by 12-18 months, maintaining the current competitive structure where shippers could play railroads against each other for better rates and service. Extended uncertainty would also limit the railroads’ ability to implement service changes that might reduce overall capacity utilization.

Shipper groups intensified their opposition with the October 16th STB comment deadline approaching. The American Chemistry Council and Rail Customer Coalition prepared extensive filings arguing that past rail mergers had resulted in 40% higher freight rates over 20-year periods. These groups represent the largest users of tank car services, suggesting their opposition would focus heavily on energy and chemical transportation impacts.

We are Watching Mexico

Folks, shipping cars into Mexico isn’t easy and it’s about to get a little more difficult. Mexico’s National Energy Commission dropped new compliance requirements late last month that hit cross-border energy transport with GPS tracking and QR code mandates. All hydrocarbon transportation units, including rail tank cars, must now install real-time monitoring systems and display regulatory verification codes.

The new rules cover all non-pipeline petroleum and LPG transportation methods. Rail tank cars crossing between Mexico and the United States have been under tremendous strain these last few months and now face additional documentation hurdles and potential border delays while operators scramble to implement these compliance systems. Specifically, the new order states that “each unit should display labeling consisting of high-durability reflective seals that include, among others, a unique QR code to be issued by the CNE to identify the permit holder, vehicle and product transported. Moreover, the Order establishes that the QR code shall be readable by standard mobile devices.”

Fuel deliveries to Mexico have been ripe with fraud as smaller importers have mislabeled shipments in order to circumvent local taxes. This is just another step taken by the Mexican government to crack down on these bad actors and will likely not be the last. Please call PFL today for more details about these requirements.

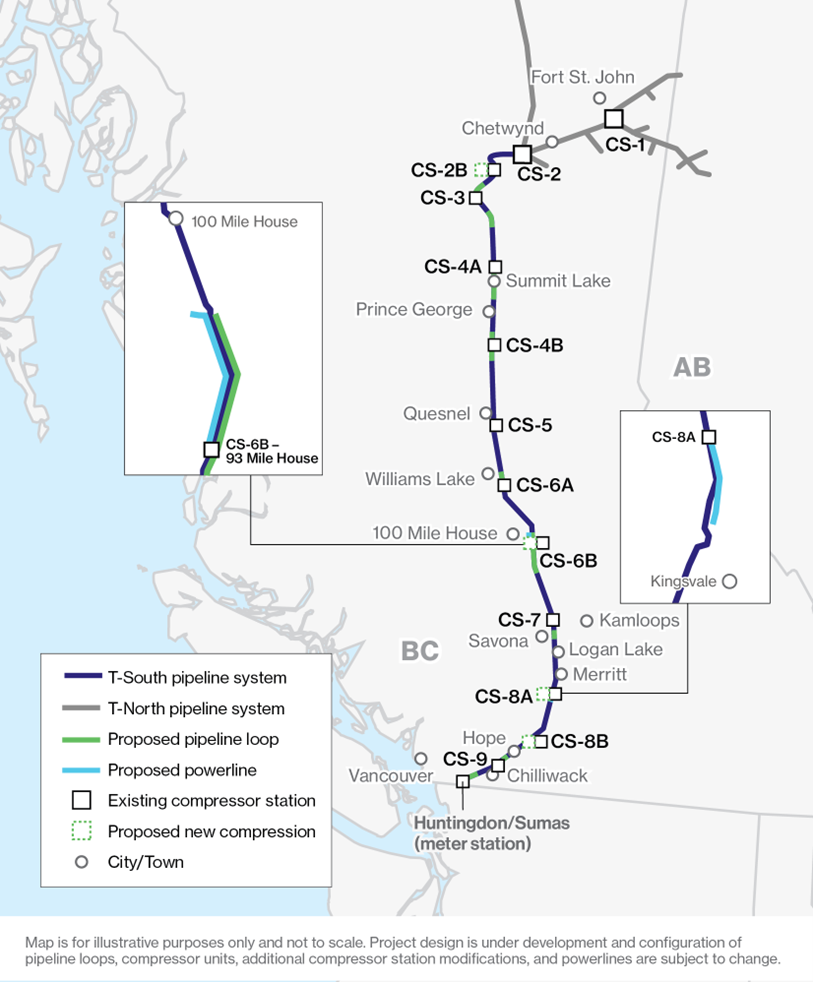

We are Watching Enbridge

Enbridge’s proposed T-South pipeline expansion gained urgency last week as the company advanced its $4 billion application for 300 million cubic feet per day of additional natural gas capacity from northeastern British Columbia to the Lower Mainland. The Canadian Energy Regulator is expected to issue its decision in early 2026, with the expanded system targeted for service in late 2028.

Source: Enbridge Inc, PFL analytics

The expansion was driven by Woodfibre LNG’s requirement for 250 mmcf/d starting in 2027, creating a two-year gap where existing pipeline infrastructure would be insufficient to serve growing demand. Current T-South utilization has exceeded 90% since 2016, demonstrating the chronic capacity constraints that have limited regional energy development and forced producers to seek alternative transportation methods.

The pipeline expansion timeline creates immediate opportunities for rail transport of natural gas liquids and condensate. During the 2026-2028 construction period, producers will need flexible transportation alternatives to reach markets, particularly for associated petroleum products that cannot move through the constrained pipeline system. Rail transport offers the primary viable option for maintaining production during the infrastructure transition.

Even after the pipeline expansion, incremental production growth beyond the new 300 mmcf/d capacity will require rail transport for surge volumes. The regulatory timeline adds uncertainty that favors rail transport’s inherent flexibility. Pipeline projects face 3-4 year development cycles with significant regulatory risk, while rail capacity can be deployed within months in an effort to serve immediate market needs.

We Continue to watch Left Wing Canadian Prime Minister Carney

Mark Carney’s flagship Net Zero Banking Alliance voted to cease operations on October 3, marking the spectacular failure of the Prime Minister’s signature climate finance initiative. The alliance, which Carney co-founded during his tenure as Bank of England Governor, lost all six major Canadian banks in January 2025 when RBC, BMO, Scotiabank, TD, CIBC, and National Bank fled en masse citing “regulatory uncertainty and legal risks.”

The collapse came just months after Carney touted the alliance as essential for financing Canada’s net-zero transition, including rail infrastructure modernization. Instead of delivering green capital for freight rail improvements, the alliance’s 18-month death spiral left tank car operators and rail infrastructure projects without access to coordinated climate financing precisely when pipeline capacity constraints demand rail system upgrades.

The irony was not lost on industry observers. While Carney’s banking initiative collapsed, his government extended the Canada Strong Pass program on October 9, committing another $6.6 million in VIA Rail subsidies for passenger travel through summer 2026. The program has generated over 50,000 subsidized bookings, demonstrating Ottawa’s willingness to fund passenger rail convenience while freight rail operators struggle with compliance costs and infrastructure financing gaps.

The timing proved particularly damaging for shippers facing mounting regulatory burdens. Carney maintained industrial carbon pricing at $65 per ton in 2025, rising to $170 per ton by 2030, while repealing consumer carbon charges in April. The policy shift forced rail carriers like CN to adjust fuel surcharges and compliance costs without access to the green financing mechanisms that Carney’s failed banking alliance was supposed to provide. The Prime Minister’s preference for subsidizing passenger rail over supporting freight infrastructure financing revealed the typical Carney approach: grand promises on climate action paired with policies that penalize the very industries essential for any economic transition in the country.

We are Watching an End to the Brawl Over MEG

The battle for MEG Energy ended decisively this weekend after Strathcona Resources officially withdrew its hostile takeover bid, clearing the path for Cenovus Energy’s now-sweetened acquisition proposal. On October 9, Strathcona announced the termination of its MEG offer, citing unprecedented actions by the MEG board and Cenovus to extend shareholder voting and allow additional share purchases, deeming any improved competing offer impractical. The MEG shareholder vote on the Cenovus deal, originally set for October 9, was postponed to October 22 to allow shareholders more time to assess the revised terms.

Cenovus’s final “best and last” proposal values MEG at approximately $8.6 billion — or about $29.79 per share, a blended mix of cash and Cenovus stock. The MEG board urged shareholders to support this improved agreement, which received backing from major proxy advisory firms and effectively ended the risk of a bidding war with Strathcona. If ratified, the deal is expected to close by late October.

The outcome concentrates even more oil sands output and transportation leverage in Cenovus’s hands. The consolidated company will control over 550,000 barrels per day of production with substantial, long-term pipeline contracts—particularly on Enbridge’s Flanagan South and Trans Mountain. While rail utilization may decrease for baseline shipments, unpredictability of Western Canadian pipeline egress means that demand for railcars should persist, especially during market disruptions and periods of strong crude pricing.

We are watching Chevron

A big explosion hit Chevron’s El Segundo refinery near Los Angeles on October 2, 2025. The fire broke out in a jet fuel processing unit and could be seen for miles. Thankfully, no one was hurt, but several parts of the refinery were shut down, and fuel production dropped. This refinery is a major supplier for Southern California, producing about 20% of the region’s gasoline and around 40% of its jet fuel. With the plant running at lower capacity, it’s already starting to affect how fuel is moved and supplied across the area. Some crude oil and fuel that normally move by rail are now being delayed or rerouted, which is creating headaches for shippers and distributors.

The slowdown also puts pressure on other fuel sources. Rail lines may have to pick up more of the slack moving fuel in and out of the region while Chevron works to get its equipment back online. That means longer travel times and higher costs for gasoline, diesel, and jet fuel deliveries.

Gas prices, especially locally, could have a short term bump as a result—some say 5 to 15 cents a gallon—if repairs take longer than expected. Airlines at LAX are also watching closely since a large portion of their jet fuel comes from El Segundo. For now, supply is stable, but any extended downtime could cause shortages in some areas. In short, the Chevron explosion is more than just a local fire—it’s a hit to California’s fuel supply chain that is already strained due to the State’s Green New Deal policies. Until the refinery is fully back online, rail and truck deliveries will be working overtime to keep up with demand.

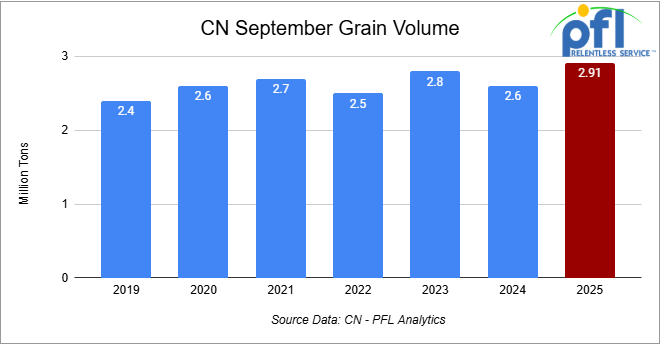

We are Watching the CN

Canadian National Railway broke its September grain record on October 9, moving 2.91 million metric tons – 80,000 tons above its previous best. The achievement came while Canadian railways failed to meet the Agriculture Transport Coalition’s 90% performance threshold for the fifth straight week and Mississippi River barge transport remained crippled by low water levels.

CN’s 12% year-over-year surge demonstrated rail’s ability to capture market share when competing modes hit capacity walls. The record volumes flowed through the same network infrastructure that serves energy transportation, creating scheduling tensions but proving rail’s asset optimization capabilities across multiple commodity sectors. The timing was telling. Peak harvest season coincided with persistent grain elevator storage pressures and constrained barge alternatives, forcing additional volumes toward rail. CN’s network absorbed the surge demand that pipelines and waterways couldn’t handle – exactly the dynamic driving increased rail car utilization across North American commodity markets.

Lease Bids

- 30-50, 6000cf Steel Hopper located off of CSX or NS in East. For use in petcoke service. Period: 5 Years.

- 50, 5000CF Covered Hopper located off of UP or BN in Houston. For use in Fertilizer service. Period: 6 Months. Bid: Negotiable.Needed ASAP.

- 10, 2500CF Open Top Hopper located off of UP or BN in Texas. For use in aggregate service. Period: 5 years. Bid: Negotiable.Need Rapid Discharge Doors.

- 10, 25.5K Any Type Tank located off of CSX in Florida. For use in UCO service. Period: 2 Years. Bid: Negotiable.

- 15-20, 29K 117R Tank located off of NS or CSX in Ohio. For use in Ply Oil service. Period: 6-12 Months. Bid: Negotiable.

- 10, 30K 117R or 117J Tank located off of Any Class 1 in USA. For use in Glycerin service. Period: 1 year. Bid: Negotiable.

- 50, 23.5-25.5 DOT111 Tank located off of Any Class 1 in USA. For use in Asphalt service. Period: 5 years. Bid: Negotiable.

- 50-100, 33K 117J Tank located off of BN or UP in Bellview. For use in Butane/ service. Period: Sept-March. Bid: Negotiable.

- 4, 30K 117J Tank located off of Any Class 1 in Michigan. For use in Food Grade Ethanol service. Period: Multi year. Bid: Negotiable.

- 100, 21.9K 117J Tank located off of All Class 1s in Midwest. For use in CO2 service. Period: 6 months. Bid: Negotiable.

- 20, 25.5K Any Type Tank located off of UP in Point Comfort, TX. For use in Diethylene Glycol service. Period: 3-5 Years. Bid: Negotiable.No Lining Required.

- 100, 33K Tank Pressure located off of CN or CP in Canada. For use in Propane service. Period: Winter. Bid: Negotiable.

Sales Bids

- 28, 3400CF Covered Hopper located off of UP BN in Texas. For use in Cement service. Bid: Negotiable.Cement Gates needed..

- 20, 17K Tank DOT111 located off of various class 1s in various locations. For use in corn syrup service. Bid: Negotiable.

- 120, Various Gondola Open-Top Aluminum Rotary located off of various class 1s in various locations. For use in Sulphur service. Bid: Negotiable.Built 2004 or later.

Lease Offers

- 60, 4750 Covered Hoppers located off of UP or BN in Eads, CO. Last used in Grain. Cars are currently clean. Offer: Negotiable. UP to 5 Years, 3 Hopper, Gravity Gate, Trough Hatches.

- 100, 6250 Covered Hoppers located off of UP in US. Last used in DDG. Offer: Negotiable. 1 Year term. Dirty to Dirty. Free move on UP..

- 25, 19.6K DOT111 Tanks located off of UP in US. Last used in Molases. Offer: Negotiable.

- 50, 20K DOT111 Tanks located off of UP or BN in Wichita Falls, TX. Last used in HCL. Offer: Negotiable.

- 50, 30K 117R Tanks located off of CSX, NS, or CN in Detroit. Last used in Diesel. Offer: Negotiable. Multiyear.

- 50, 20K 117J Tanks located off of All Class 1s in Multiple Locations. Last used in Styrene. Offer: Negotiable. Cars are currently moving.

- 22, 25.5K DOT111 Tanks located off of UP in Texas. Last used in Asphalt. Offer: Negotiable.

- 29, 25.5K 117J Tanks located off of BN or UP in Texas. Cars are currently clean. Offer: Negotiable.

- 40, 30K 117J Tanks located off of BNSF or UP in Houston. Cars are currently clean. Offer: Negotiable.

- 50, 5380 Covered Hoppers located off of BNSF or UP in Houston. Cars are currently clean. Offer: Negotiable. Available until Feburary.

Sales Offers

- 21, 50′ Boxcar Plate Cs located off of various class 1s in NM. Offer: Negotiable. End of Life.

- 3, 50′ Boxcar Plate Cs located off of various class 1s in multiple locations. Offer: Negotiable. End of Life.

- 27, 50′ Boxcar Plate Cs located off of various class 1s in PQ. Offer: Negotiable. End of Life.

- 100, 3250 Covered Hoppers located off of various class 1s in multiple locations. Offer: Negotiable. Sand Cars.

- 5, 2740 Mill Gondolas located off of various class 1s in NC. Offer: Negotiable. End of Life.

- 1, 2260 Mill Gondolas located off of various class 1s in AL. Offer: Negotiable. End of Life.

- 30, 2740 Mill Gondolas located off of various class 1s in multiple locations. Offer: Negotiable. End of Life.

- 21, 2740 Mill Gondolas located off of various class 1s in WA. Offer: Negotiable. End of Life.

- 9, 4750 Covered Hoppers located off of various class 1s in multiple locations. Offer: Negotiable. End of Life.

- 5, 4750 Covered Hoppers located off of various class 1s in multiple locations. Offer: Negotiable. End of Life.

- 50, 31.8K Tank CPC 1232s located off of UP or BN in TX. Offer: Negotiable. Requal Due in 2025.

- 100, 4600CF Open Top Hoppers located off of BN or CSX in Southeast. Offer: Negotiable. N/A.

Call PFL today to discuss your needs and our availability and market reach. Whether you are looking to lease cars, lease out cars, buy cars, or sell cars call PFL today at 239-390-2885

Live Railcar Markets

| CAT | Type | Capacity | GRL | QTY | LOC | Class | Prev. Use | Offer | Note |

|---|

PFL will be at the Following Conferences

- Where: Loews Arlington Hotel

- Attending: Brian Baker (239.297.4519), David Cohen (954-729-4774), and Curtis Chandler (239-405-3365)

- Conference Website

- Where: The Westin Galleria Dallas

- Attending: David Cohen (954-729-4774), and Curtis Chandler (239-405-3365)

- Conference Website

- Where: The Westin Galleria Dallas

- Attending: Brian Baker (239.297.4519)

- Conference Website