“It is never too late to be what you might have been,” – George Eliot

Due to the Government Shutdown, we are unable to report last week’s Jobs Update. We apologize for the inconvenience.

Jobs Update

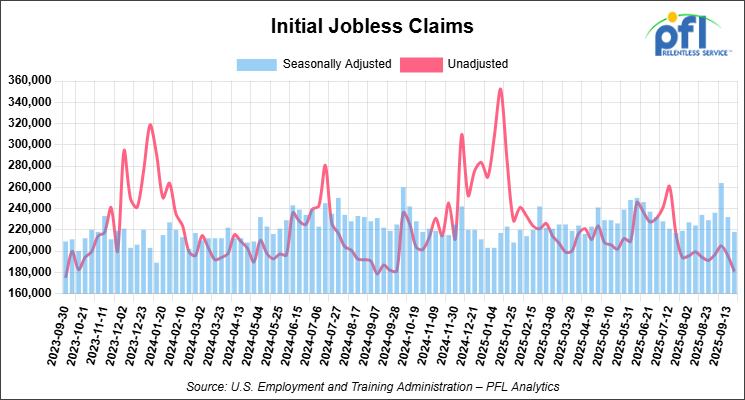

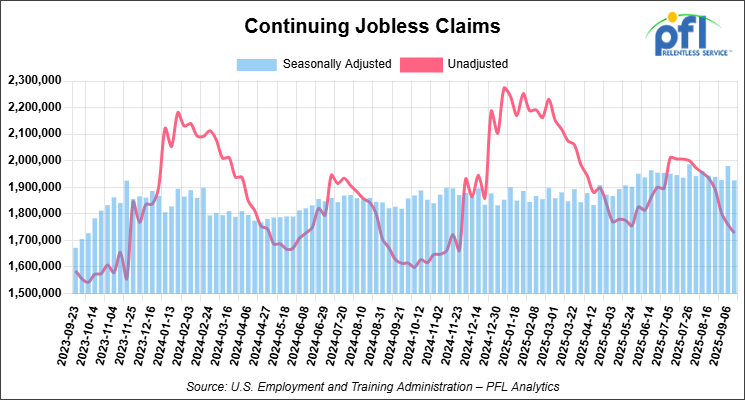

• Initial jobless claims seasonally adjusted for the week ending September 20, 2025 came in at 218,000, versus the adjusted number of 232,000 people from the week prior, down 14,000 people week over week.

• Continuing jobless claims came in at 1,926,000, versus the adjusted number of 1,980,000 people from the week prior, down 54,000 week-over-week.

Stocks closed mixed on Friday of last week and higher week-over-week

The DOW closed higher on Friday of last week, up 238.56 points (0.51%), closing out the week at 46,758.28, up 510.99 points week-over-week. The S&P 500 closed higher on Friday of last week, up 0.44 points (0.01%) and closed out the week at 6,715.79, up 72.09 points week-over-week. The NASDAQ closed lower on Friday of last week, down -63.54 points (-0.28%), and closed out the week at 22,780.81, up 296.74 points week-over-week.

In overnight trading, DOW futures traded higher and are expected to open at 47,126 this morning, up 95 points from Friday’s close.

Crude oil closed higher on Friday of last week and lower week-over-week

West Texas Intermediate (WTI) crude closed up 40 cents per barrel (0.7%), to close at $60.88 on Friday of last week, but down $4.84 week-over-week. Brent crude closed up 42 cents per barrel (0.7%), to close at $64.53, but down $5.60 week-over-week..

One Exchange WCS (Western Canadian Select) for November delivery settled on Friday of last week at US$11.05 below the WTI-CMA (West Texas Intermediate – Calendar Month Average). The implied value was US$49.05 per barrel.

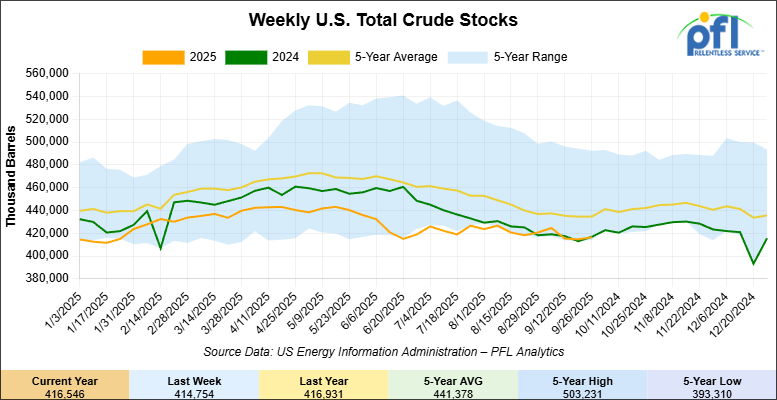

U.S. commercial crude oil inventories (excluding those in the Strategic Petroleum Reserve) increased by 1.8 million barrels week-over-week. At 416.5 million barrels, U.S. crude oil inventories are 4% below the five-year average for this time of year

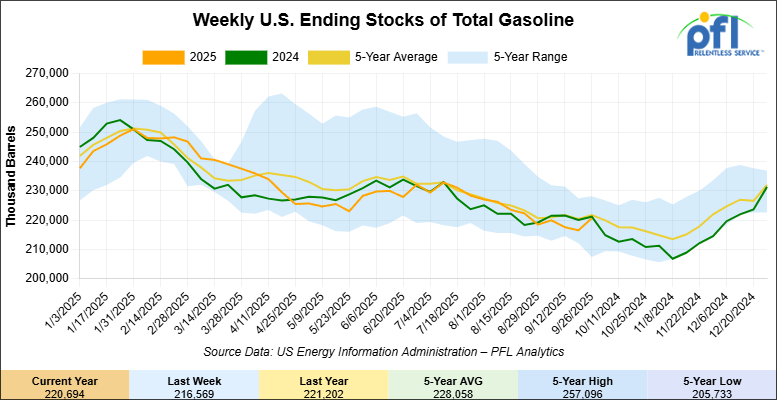

Total motor gasoline inventories increased by 4.1 million barrels week-over-week and are slightly lower than the five-year average for this time of year.

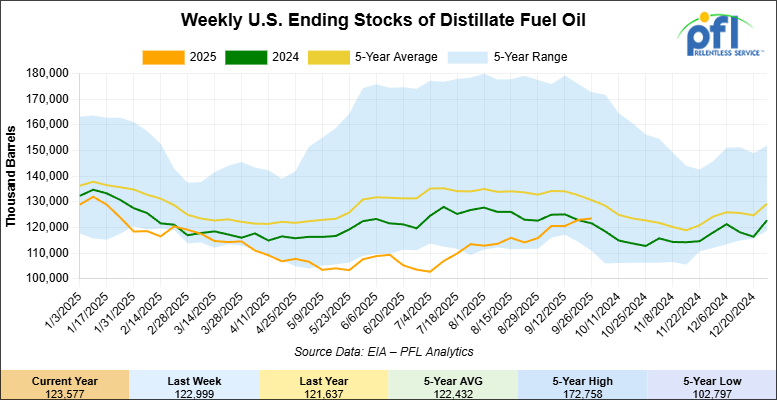

Distillate fuel inventories increased by 600,000 barrels week-over-week and are 6% below the five-year average for this time of year

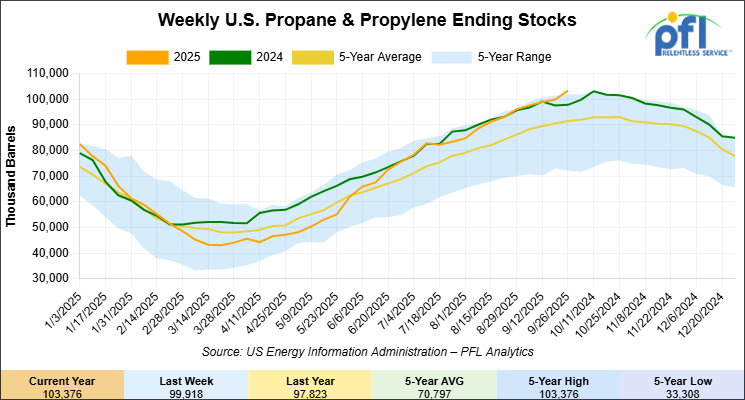

Propane/propylene inventories increased by 3.5 million barrels week-over-week and are 13% above the five-year average for this time of year.

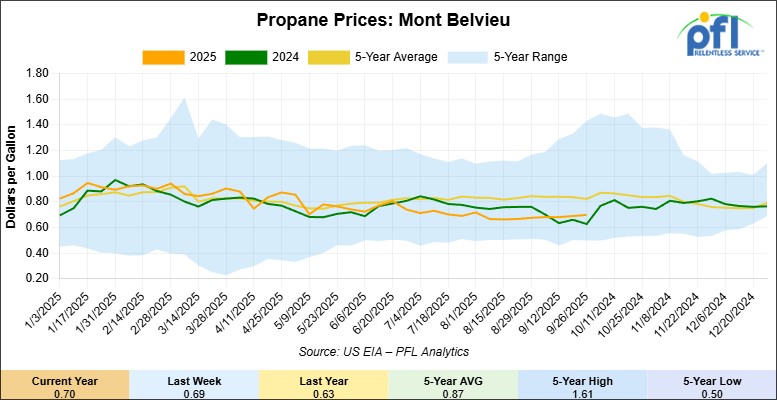

Propane prices closed at 70 cents per gallon on Friday of last week, up 1 cent week-over-week and up 7 cents per gallon year-over-year.

Overall, total commercial petroleum inventories increased by 6.4 million barrels during the week ending September 26, 2025.

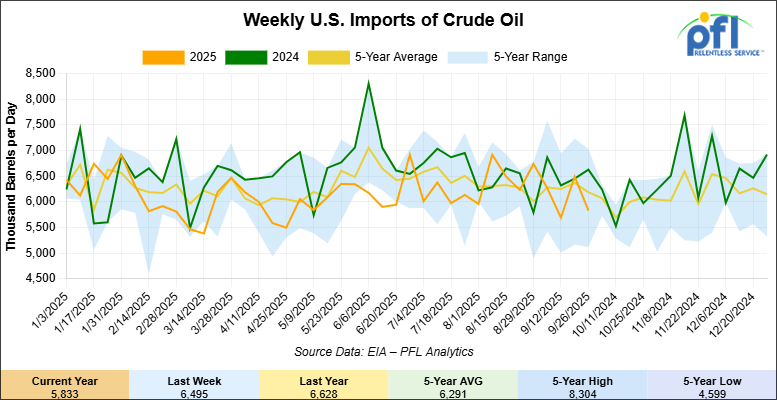

U.S. crude oil imports averaged 5.8 million barrels per day during the week ending September 26, 2025, a decrease of 662,000 barrels per day week-over-week. Over the past four weeks, crude oil imports averaged 6.1 million barrels per day, 7.5% less than the same four-week period last year. Total motor gasoline imports (including both finished gasoline and gasoline blending components) averaged 668,000 barrels per day, and distillate fuel imports averaged 118,000 barrels per day during the week ending September 26, 2025.

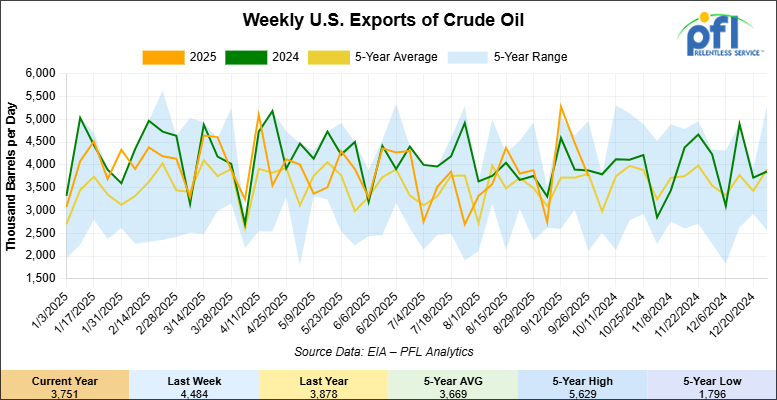

U.S. crude oil exports averaged 3.751 million barrels per day during the week ending September 26, 2025, a decrease of -733,000 barrels per day week-over-week. Over the past four weeks, crude oil exports averaged 4.064 million barrels per day.

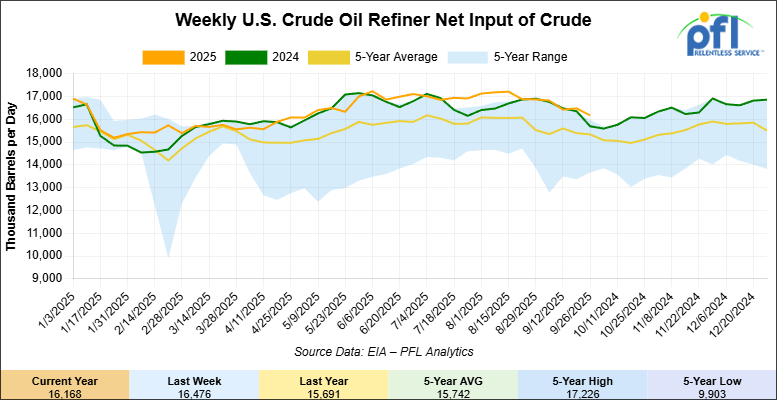

U.S. crude oil refinery inputs averaged 16.2 million barrels per day during the week ending September 26, 2025, which was 308,000 barrels per day less week-over-week.

WTI futures are poised to open at $62.01, up $1.13 from Friday’s close.

Due to the Government Shutdown we are unable to report last week’s Rail Traffic Data. We apologize for the inconvenience.

North American Rail Traffic

Week Ending September 24, 2025:

Total North American weekly rail volumes were down (-3.62%) in week 39, compared with the same week last year. Total Carloads for the week ending September 24, 2025 were 324,445, down (-2.05%) compared with the same week in 2024, while weekly Intermodal volume was 340,982, down (-5.06%) year over year. 9 of the AAR’s 11 major traffic categories posted year-over-year decreases. The largest decrease came from Forest Products (-18.02%), while the largest increase was Grain (+5.54%).

In the East, CSX’s total volumes were up (+1.93%), with the largest decrease coming from Forest Products (-17.17%), while the largest increase came from Intermodal Units (+7.61%). NS’s total volumes were down (-5.00%), with the largest increase coming from Motor Vehicles and Parts (+7.78%), while the largest decrease came from Coal (-25.51%).

In the West, BNSF’s total volumes were down (-1.11%), with the largest increase coming from Coal (+35.31%), while the largest decrease came from Chemicals (-9.02%). UP’s total volumes were down (-5.81%), with the largest increase coming from Grain (+42.44%), while the largest decrease came from Intermodal Units (-15.62%).

In Canada, CN’s total volumes were down (-2.59%), with the largest increase coming from Coal (+35.31%), while the largest decrease came from Other (-32.65%). CPKCS’s total volumes were down (-19.55%), with the largest increase coming from Nonmetallic Minerals (+5.77%), while the largest decrease came from Forest Products (-65.54%).

Source Data: AAR – PFL Analytics

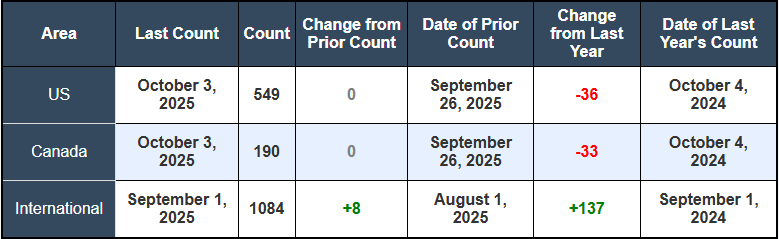

Rig Count

North American rig count was unchanged week-over-week. The US rig count was unchanged week-over-week, but down by -36 rigs year-over-year. The US currently has 549 active rigs. Canada’s rig count was unchanged week-over-week, but down by -33 rigs year-over-year. Canada currently has 190 active rigs. Overall, year-over-year we are down by -69 rigs collectively.

International rig count, which is reported monthly, was up by +8 rigs month-over-month and up by +137 rigs year-over-year. Internationally, there are 1,084 active rigs

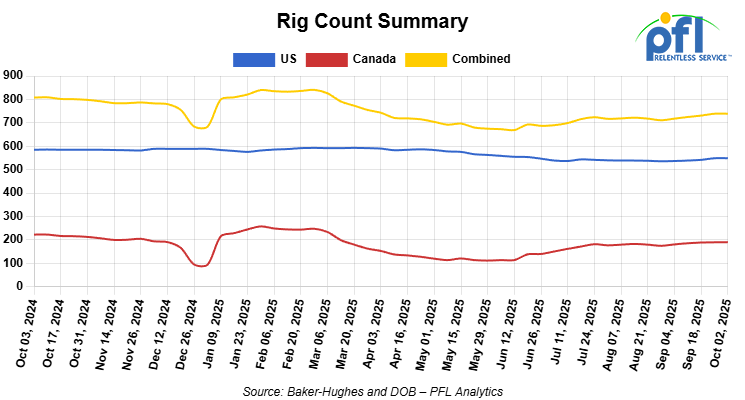

North American Rig Count Summary

We are watching a few things out there for you:

We attended last Week’s SWARS Conference

David Cohen and Curtis Chandler from PFL attended last week’s SWARS conference at the Renaissance Phoenix Hotel in Phoenix, Arizona. The conference was semi-well attended with 603 registered participants. Speakers included Kenny Rocker, Executive Vice President, Marketing and Sales at Union Pacific who was very upbeat and honed in on the UP/NS merger and of course was extremely positive on the proposed merger and cited only four overlaps in service across the entire network. It seems based on industry chatter and with the President’s support of the merger, that it is going to go through.

Michael McBride, Partner at Van Ness Feldman LLP reinforced the uncertainty that we all feel in regard to trade and the regulatory landscape that are challenges for us every day. Finally, Ken Carter, Author Educator and Inspiration of the film Coach Carter starring Samuel L. Jackson, gave us all a motivational boost!

Despite potential headwinds, people were upbeat – looking to get deals done. Hats off to the people at SWARS organizing the event and PFL was happy to attend. For more information as it relates to the SWARS meeting in Phoenix please contact PFL today. SWARS’ annual meeting is in Houston on March 16-17 at the Marriott Marquis Hotel. We expect attendance of that event to be north of 1,000 participants so book your spot early.

We are watching Petroleum Carloads

The four-week rolling average of petroleum carloads carried on the six largest North American railroads fell to 28,337 from 28,680, which was a decrease of -343 rail cars week-over-week. Canadian volumes were mixed. CPKC’s shipments were lower by -4.0% week over week, CN’s volumes were higher by +4.0% week-over-week. U.S. shipments were also mixed. The NS had the largest percentage increase and was up by +12.0%. The UP had the largest percentage decrease and was down by -3%.

We are watching our Ports

The Port of Los Angeles, the busiest container hub in the country, is taking its first real step in decades toward building a brand-new terminal. The plan, called Pier 500, would add about 200 acres of space and 3,000 feet of wharf along the Pier 400 channel, with two berths designed to handle the next generation of mega-ships.

The Port has put out a call for private partners to handle the early work — studies, permits, and design. Proposals are due January 29, 2026, and leaders estimate the full project could take up to 10 years to complete. The timing lines up with record volumes: in July, Los Angeles moved more than one million TEUs in a single month for the first time ever. Officials also promise Pier 500 will be the “cleanest terminal possible,” using new technology to cut emissions and boost efficiency.

A terminal this size will put even more pressure on on-dock rail and inland intermodal yards. Whether Pier 500 makes things smoother or simply shifts the bottlenecks will come down to how well the rail connections are built in from the start. PFL is watching this one closely.

We are Watching the Surface Transportation Board

On Tuesday of last week, the Surface Transportation Board (STB) proposed a rule to modernize how Class I railroads report performance. The Notice of Proposed Rulemaking would cut back on older requirements, like supplemental Positive Train Control expense reporting, and replace them with metrics tied more directly to service reliability.

For shippers, this matters. Better visibility into dwell, velocity, and on-time performance gives customers a clearer picture of whether railroads are keeping commitments. Stronger service data also gives shippers leverage if performance slips and a case needs to be brought before regulators. In short, the STB is trying to shift the focus from accounting details to the numbers that impact day-to-day freight movement.

Comments on the proposed rule are due by October 30, 2025. If adopted, carriers would face a new standard for transparency, and shippers could have better tools to hold them accountable.

PFL is watching how this rulemaking develops, and whether it leads to more meaningful service data that helps our customers plan and protect their supply chains.

We continue to watch M&A Activity

The North American rail sector was fundamentally reshaped last week by an activist-driven leadership change at CSX Corp., in the most significant consequence yet of the proposed Union Pacific-Norfolk Southern megamerger. The abrupt ouster of President and CEO Joe Hinrichs and the installation of a successor with a strong M&A background signaled that the strategic direction of the continent’s largest railroads was now subject to intense and decisive pressure from Wall Street.

On September 29, CSX announced the immediate departure of Hinrichs. In his place, the board appointed Steve Angel, the former CEO of industrial gas giant Linde plc. The strategic direction implied by Angel’s appointment was made explicit by his compensation agreement, which included a provision that would triple his salary and bonus in the event of a change of control at CSX – strongly suggesting the board was preparing for a merger as a primary strategic option.

This leadership change was the direct result of a sustained public pressure campaign by activist investor Ancora Holdings Group, which had publicly demanded CSX either find a merger partner or terminate Hinrichs, citing deteriorating performance. While investors celebrated, the SMART Transportation Division (SMART-TD), the largest union representing CSX’s workforce, offered a starkly different perspective, issuing a powerful statement that the relationship between management and labor “sank to all-time lows” during Hinrichs’ tenure.

While CSX grappled with internal fallout, the external battle over the proposed Union Pacific-Norfolk Southern merger intensified as key stakeholders began to draw clear battle lines.

The American Chemistry Council (ACC) and the Rail Customer Coalition (RCC) formally voiced deep concerns to the Surface Transportation Board (STB), warning that the merger could erode market competition and drive up costs. In a significant escalation, competitor BNSF Railway took its case to the public, issuing a call for shippers to speak out against the deal and attempting to frame it as a fundamental threat to the U.S. supply chain.

The regulatory environment itself became a flashpoint. On October 1, former STB member Robert Primus filed a federal lawsuit against President Trump over his August dismissal. The lawsuit argued that Trump violated federal statutes requiring STB members to serve fixed terms and only be removed “for cause,” noting no reason was given beyond that Primus “didn’t align with the America First agenda.” As the sole Democratic appointee on the panel that will review the merger, his removal was seen as a move to influence the outcome, introducing genuine uncertainty about the board’s composition.

We are Watching Energy Logistics, Pipeline Politics, and Production Plateaus

Alberta Premier Danielle Smith announced the province would commit $14 million to directly propose a new, one-million-barrel-per-day oil pipeline to the B.C. coast. The move was a response to a looming export bottleneck, as the Trans Mountain pipeline averaged 84% utilization through the first half of 2025 and is projected to be full by 2027-2028. However, the project immediately faced the same political obstacles that killed past proposals, with B.C.’s Premier and First Nations coalitions voicing strong opposition. This political paralysis reinforced rail’s role as the primary outlet for growth in Western Canadian oil production, however, with WCS trading below $50 US per barrel makes it uneconomic.

Diamondback Energy CEO Travis Stice delivered a stark warning that U.S. shale production will stall if crude prices remain near $60 per barrel, as the best drilling locations are depleted. Diamondback cut its 2025 capex by $500 million, Permian rig counts are falling, and the EIA projected that U.S. crude production would decline in 2026.

We continue to watch Canadian Left Wing Prime Minister Carney

While the broad strokes of left-wing Prime Minister Mark Carney’s economic agenda have been known for some time, the business community got a jarring look at the government’s next phase of implementation on Thursday of last Thursday. In a major economic address in Toronto, the left-wing Prime Minister laid out a series of specific directives that moved his long-stated climate finance principles from theory into direct regulatory action.

He announced that his government is now directing the Office of the Superintendent of Financial Institutions (OSFI) to develop and implement mandatory climate-risk capital adequacy requirements for Canadian banks. This effectively forces lenders to hold more capital against loans made to high-carbon sectors, making such financing more expensive and scarce.

Furthermore, he confirmed that TCFD-aligned (Task Force on Climate-related Financial Disclosures) reporting would become mandatory for all federally regulated businesses, including railways, starting in 2026.

For the North American rail industry, the Prime Minister’s speech signaled a significant escalation. The pressure is no longer just the government’s general philosophy; it is now a set of specific, actionable policies. By directing the nation’s financial regulators, the government is taking direct aim at the viability of a core business line for Canadian railroads: the transport of oil and gas.

The move creates profound uncertainty for any long-term capital planning. Railroads and railcar lessors who serve the energy sector must now factor in the risk of a federal government that is actively implementing policies designed to constrain their customers’ access to capital.

We are Watching Innovation in Automation and Propulsion

Away from the high-stakes corporate drama, the industry’s pursuit of technological advancement continued, with a focus on efficiency and automation.

Autonomous Yard Movement: Short line operator Watco announced a commercial agreement to deploy Intramotev’s “TugVolt” autonomous, battery-electric, self-propelled wagons. The technology has the potential to revolutionize “first-mile, last-mile” logistics by automating the complex process of positioning and moving rail cars for loading and unloading.

AI in the Maintenance Shop: Railinc, a subsidiary of the Association of American Railroads, announced a collaboration with Duke University to explore how artificial intelligence can make wagon repair work more efficient. The initiative aims to leverage AI for predictive diagnostics to minimize rolling stock downtime and improve asset utilization.

Propulsion Efficiency: Mitsubishi Electric won a prestigious 2025 R&D 100 Award for its SynTRACS motor system for railcars. The system is notable for not using rare-earth materials and for reducing energy consumption by 18% compared to conventional systems, contributing directly to lower operating costs.

We are Watching Financial Signals from the Railcar Sector

Developments within the railcar leasing and supply sectors as all our readers know provide a valuable barometer of broader economic health and investor sentiment. Rail traffic always gives us insight as to what the economy is actually doing or likely going to do. A couple of interesting moves occurred that we thought may be of interest to our readers

Confidence in Trinity Industries: Despite Trinity Industries posting a recent quarterly loss and a year-over-year revenue decline, there were clear signs of long-term investor confidence. Capital Investment Advisors LLC acquired a new stake in the company, suggesting a belief in the durable fundamentals of the railcar leasing business that looked beyond a single difficult quarter.

Supplier Consolidation Continued: A. Stucki Company, a provider of engineered components, announced its acquisition of Wheelworx, a company specializing in wheel and axle services. The move was indicative of the ongoing strategy among suppliers to broaden their service offerings and achieve greater economies of scale.

We are watching Key Economic Indicators

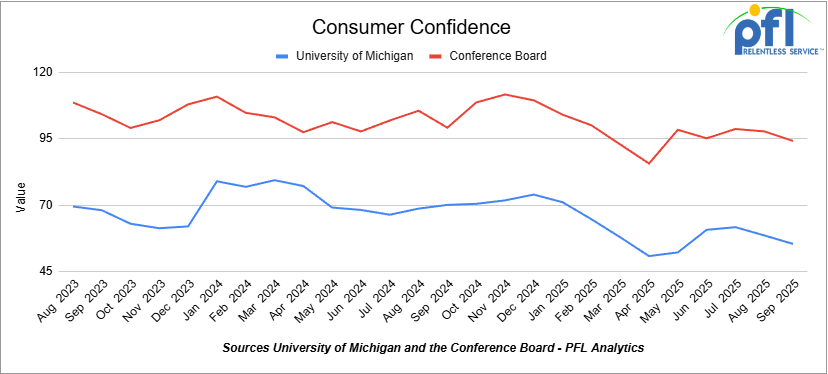

Consumer Confidence

The Conference Board’s Index of Consumer Confidence decreased to 94.2 in September 2025, down from 97.8 in August.

The University of Michigan’s Index of Consumer Sentiment decreased to 55.4 in August, down from 58.6 in July.

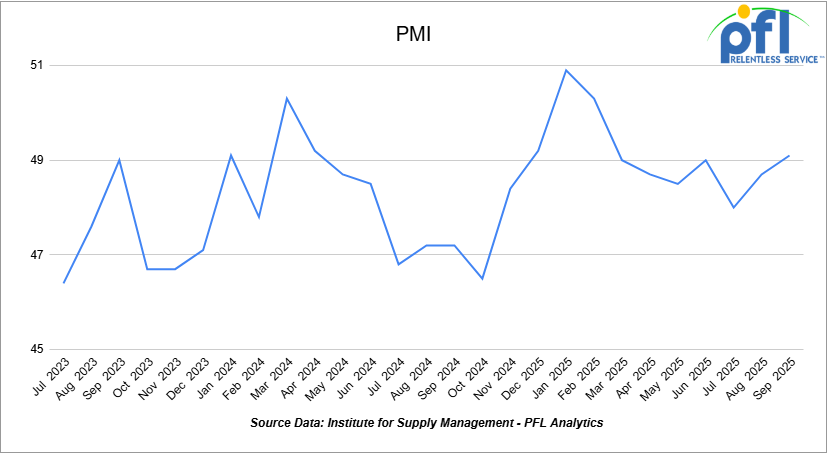

Purchasing Managers Index (PMI)

The Institute for Supply Management releases two PMI reports – one covering manufacturing and the other covering services. These reports are based on surveys of supply managers across the country and track changes in business activity. A reading above 50% on the index indicates expansion, while a reading below 50% signifies contraction, with a faster pace of change, the farther the reading is from 50.

The Manufacturing PMI in September was 49.1%, up from 48.7% in August. This is still in contraction territory, marking the seventh straight month below 50%. In somewhat better news, the New Orders sub-index stood at 48.9%, having fallen from higher levels earlier. On the Services PMI side, the most recent reading is 52.0%, up from 50.1% in August, signaling continued expansion in the services sector.

Lease Bids

- 30-50, 6000cf Steel Hopper located off of CSX or NS in East. For use in petcoke service. Period: 5 Years.

- 50, 5000CF Covered Hopper located off of UP or BN in Houston. For use in Fertilizer service. Period: 6 Months. Bid: Negotiable.Needed ASAP.

- 10, 2500CF Open Top Hopper located off of UP or BN in Texas. For use in aggregate service. Period: 5 years. Bid: Negotiable.Need Rapid Discharge Doors.

- 10, 25.5K Any Type Tank located off of CSX in Florida. For use in UCO service. Period: 2 Years. Bid: Negotiable.

- 15-20, 29K 117R Tank located off of NS or CSX in Ohio. For use in Ply Oil service. Period: 6-12 Months. Bid: Negotiable.

- 10, 30K 117R or 117J Tank located off of Any Class 1 in USA. For use in Glycerin service. Period: 1 year. Bid: Negotiable.

- 50, 23.5-25.5 DOT111 Tank located off of Any Class 1 in USA. For use in Asphalt service. Period: 5 years. Bid: Negotiable.

- 50-100, 33K 117J Tank located off of BN or UP in Bellview. For use in Butane/ service. Period: Sept-March. Bid: Negotiable.

- 4, 30K 117J Tank located off of Any Class 1 in Michigan. For use in Food Grade Ethanol service. Period: Multi year. Bid: Negotiable.

- 100, 21.9K 117J Tank located off of All Class 1s in Midwest. For use in CO2 service. Period: 6 months. Bid: Negotiable.

- 20, 25.5K Any Type Tank located off of UP in Point Comfort, TX. For use in Diethylene Glycol service. Period: 3-5 Years. Bid: Negotiable.No Lining Required.

- 100, 33K Tank Pressure located off of CN or CP in Canada. For use in Propane service. Period: Winter. Bid: Negotiable.

Sales Bids

- 28, 3400CF Covered Hopper located off of UP BN in Texas. For use in Cement service. Bid: Negotiable.Cement Gates needed..

- 20, 17K Tank DOT111 located off of various class 1s in various locations. For use in corn syrup service. Bid: Negotiable.

- 120, Various Gondola Open-Top Aluminum Rotary located off of various class 1s in various locations. For use in Sulphur service. Bid: Negotiable.Built 2004 or later.

Lease Offers

- 60, 4750 Covered Hoppers located off of UP or BN in Eads, CO. Last used in Grain. Offer: Negotiable. UP to 5 Years, 3 Hopper, Gravity Gate, Trough Hatches.

- 100, 6250 Covered Hoppers located off of UP in US. Last used in DDG. Offer: Negotiable. 1 Year term. Dirty to Dirty. Free move on UP..

- 25, 19.6K DOT111 Tanks located off of UP in US. Last used in Molases. Offer: Negotiable.

- 50, 20K DOT111 Tanks located off of UP or BN in Wichita Falls, TX. Last used in HCL. Offer: Negotiable.

- 50, 30K 117R Tanks located off of CSX, NS, or CN in Detroit. Last used in Diesel. Offer: Negotiable. Multiyear.

- 50, 20K 117J Tanks located off of All Class 1s in Multiple Locations. Last used in Styrene. Offer: Negotiable. Cars are currently moving.

- 22, 25.5K DOT111 Tanks located off of UP in Texas. Last used in Asphalt. Offer: Negotiable.

- 29, 25.5K 117J Tanks located off of BN or UP in Texas. Cars are Clean. Offer: Negotiable.

- 40, 30K Tanks 117J located off of BNSF or UP in Houston. Cars are Clean. Offer: Negotiable.

Sales Offers

- 21, 50′ Boxcar Plate Cs located off of various class 1s in NM. Offer: Negotiable. End of Life.

- 3, 50′ Boxcar Plate Cs located off of various class 1s in multiple locations. Offer: Negotiable. End of Life.

- 27, 50′ Boxcar Plate Cs located off of various class 1s in PQ. Offer: Negotiable. End of Life.

- 100, 3250 Covered Hoppers located off of various class 1s in multiple locations. Offer: Negotiable. Sand Cars.

- 5, 2740 Mill Gondolas located off of various class 1s in NC. Offer: Negotiable. End of Life.

- 1, 2260 Mill Gondolas located off of various class 1s in AL. Offer: Negotiable. End of Life.

- 30, 2740 Mill Gondolas located off of various class 1s in multiple locations. Offer: Negotiable. End of Life.

- 21, 2740 Mill Gondolas located off of various class 1s in WA. Offer: Negotiable. End of Life.

- 9, 4750 Covered Hoppers located off of various class 1s in multiple locations. Offer: Negotiable. End of Life.

- 5, 4750 Covered Hoppers located off of various class 1s in multiple locations. Offer: Negotiable. End of Life.

- 50, 31.8K Tank CPC 1232s located off of UP or BN in TX. Offer: Negotiable. Requal Due in 2025.

- 100, 4600CF Open Top Hoppers located off of BN or CSX in Southeast. Offer: Negotiable. N/A.

Call PFL today to discuss your needs and our availability and market reach. Whether you are looking to lease cars, lease out cars, buy cars, or sell cars call PFL today at 239-390-2885

Live Railcar Markets

| CAT | Type | Capacity | GRL | QTY | LOC | Class | Prev. Use | Offer | Note |

|---|

PFL will be at the Following Conferences

- Where: Loews Arlington Hotel

- Attending: Brian Baker (239.297.4519), David Cohen (954-729-4774), and Curtis Chandler (239-405-3365)

- Conference Website

- Where: The Westin Galleria Dallas

- Attending: David Cohen (954-729-4774), and Curtis Chandler (239-405-3365)

- Conference Website

- Where: The Westin Galleria Dallas

- Attending: Brian Baker (239.297.4519)

- Conference Website