“The hardest arithmetic to master is that which enables us to count our blessings.”

– Eric Hoffer

Jobs Update

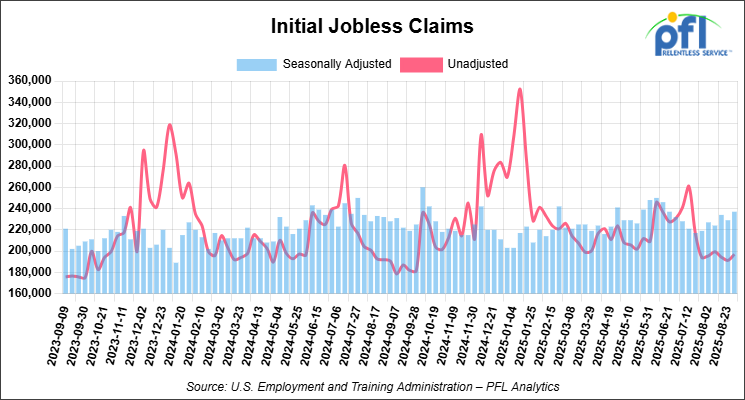

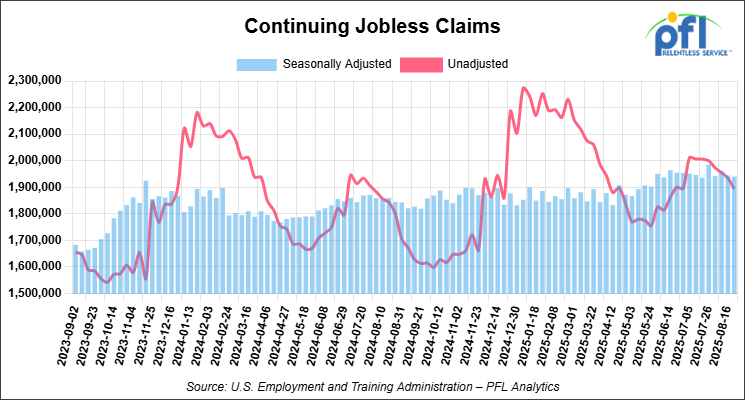

• Initial jobless claims seasonally adjusted for the week ending August 30, 2025 came in at 237,000, versus the adjusted number of 229,000 people from the week prior, up 8,000 people week over week.

• Continuing jobless claims came in at 1,940,000, versus the adjusted number of 1,944,000 people from the week prior, down 4,000 week-over-week.

Stocks closed lower on Friday of last week and mixed week-over-week

The DOW closed lower on Friday of last week, down -220.43 points (-0.48%), closing out the week at 45,400.86, down -144.02 points week-over-week. The S&P 500 closed lower on Friday of last week, down -20.58 points (-0.32%), and closed out the week at 6,481.50, up 21.21 points week-over-week. The NASDAQ closed lower on Friday of last week, down -7.31 points (-0.03%), and closed out the week at 21,700.39, up 244.84 points week-over-week.

In overnight trading, DOW futures traded higher and are expected to open at 45,534 this morning, up 75 points from Friday’s close.

Crude oil closed lower on Friday of last week and lower week-over-week

West Texas Intermediate (WTI) crude closed down -1.61 per barrel (-2.54%), to close at $61.87 on Friday of last week, down $2.14 week-over-week. Brent crude closed down -1.49 per barrel (-2.22%), to close at $65.50, and down $2.62 week-over-week.

One Exchange WCS (Western Canadian Select) for October delivery settled on Friday of last week at US$11.55 below the WTI-CMA (West Texas Intermediate – Calendar Month Average). The implied value was US$51.37 per barrel.

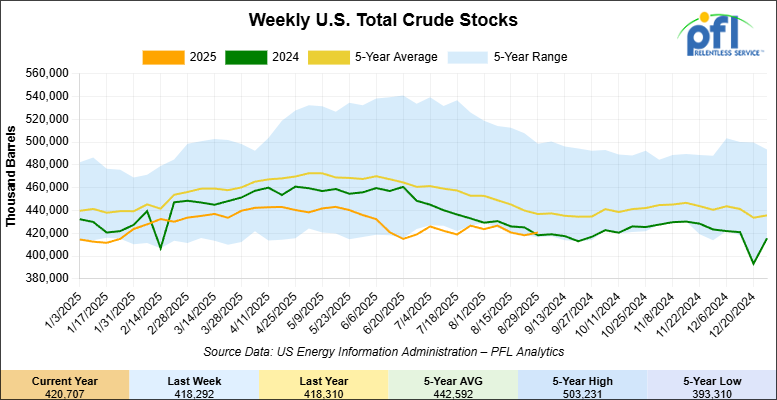

U.S. commercial crude oil inventories (excluding those in the Strategic Petroleum Reserve) increased by 2.4 million barrels week-over-week. At 420.7 million barrels, U.S. crude oil inventories are 4% below the five-year average for this time of year.

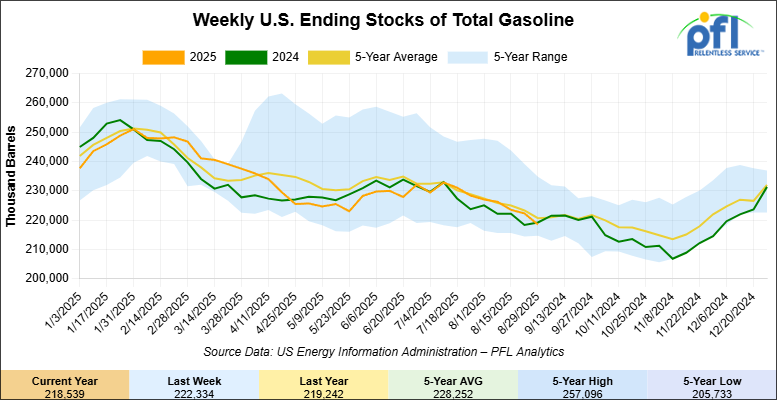

Total motor gasoline inventories decreased by 3.8 million barrels week-over-week and are 2% below the five-year average for this time of year.

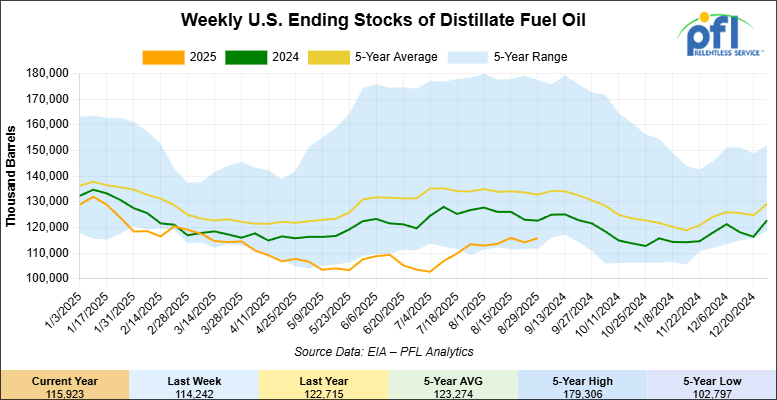

Distillate fuel inventories increased by 1.7 million barrels week-over-week and are 13% below the five-year average for this time of year.

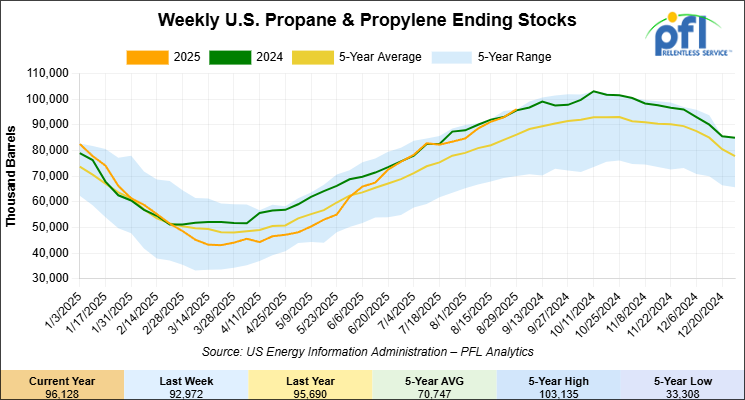

Propane/propylene inventories increased by 3.2 million barrels week-over-week and are 12% above the five-year average for this time of year.

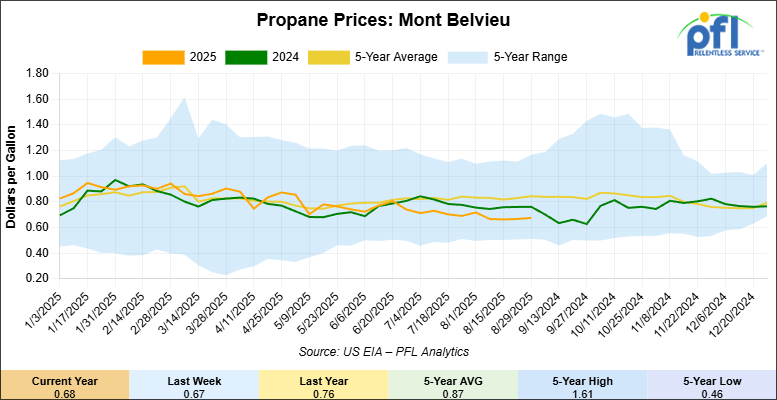

Propane prices closed at 68 cents per gallon on Friday of last week, up 1 cent per gallon week-over-week, and down 8 cents per gallon year-over-year.

Overall, total commercial petroleum inventories increased by 7.1 million barrels last week during the week ending August 29, 2025.

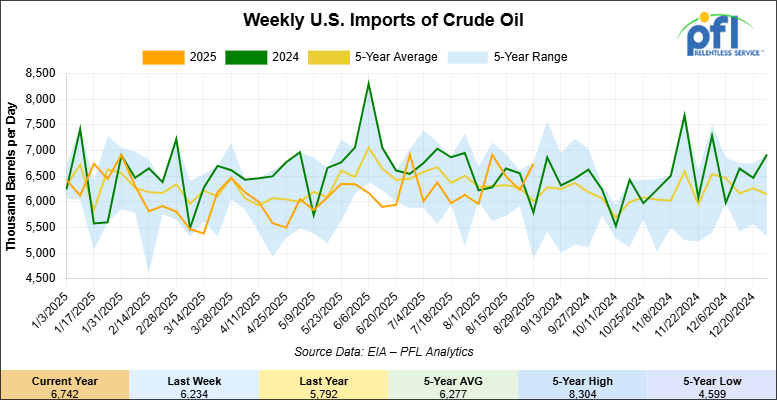

U.S. crude oil imports averaged 6.7 million barrels per day during the week ending August 29, 2025, an increase of 508,000 barrels per day week-over-week. Over the past four weeks, crude oil imports averaged 6.6 million barrels per day, 4.4% more than the same four-week period last year. Total motor gasoline imports (including both finished gasoline and gasoline blending components) averaged 582,000 barrels per day, and distillate fuel imports averaged 96,000 barrels per day. during the week ending August 29, 2025.

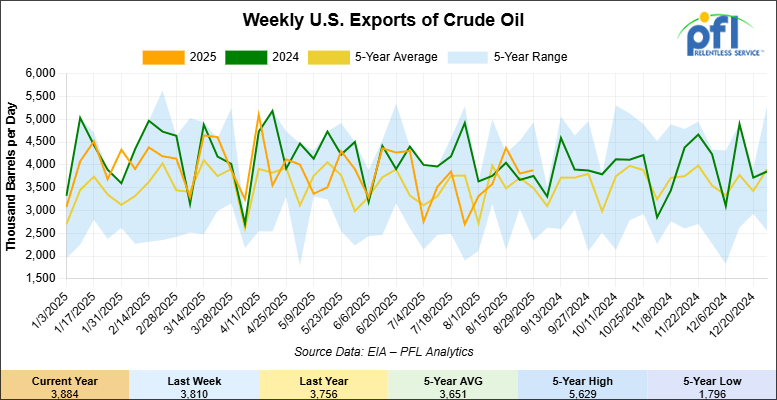

U.S. crude oil exports averaged 3.884 million barrels per day during the week ending August 29, 2025, an increase of 74,000 barrels per day week-over-week. Over the past four weeks, crude oil exports averaged 3.911 million barrels per day.

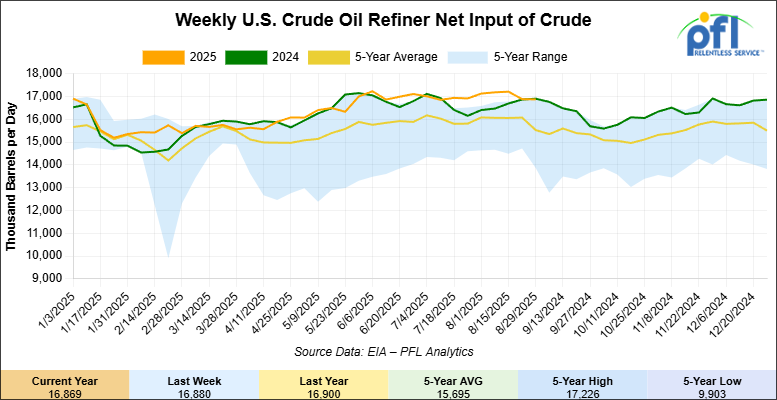

U.S. crude oil refinery inputs averaged 16.9 million barrels per day during the week ending August 29, 2025, which was 11,000 barrels per day less week-over-week.

WTI is poised to open at $63.17, up $1.30 per barrel from Friday’s close.

North American Rail Traffic

Week Ending September 3, 2025:

Total North American weekly rail volumes were down (-0.34%) in week 36, compared with the same week last year. Total Carloads for the week ending September 3, 2025 were 330,410, down (-0.86%) compared with the same week in 2024, while weekly Intermodal volume was 349,474, up (+0.16%) year over year. 7 of the AAR’s 11 major traffic categories posted year-over-year increases. The largest decrease came from Forest Products (-15.44%), while the largest increase was Chemicals (+5.24%).

In the East, CSX’s total volumes were down (-0.38%), with the largest decrease coming from Petroleum & Petroleum Products (-24.44%), while the largest increase came from Intermodal Units (+5.56%). NS’s total volumes were down (-0.45%), with the largest increase coming from Petroleum & Petroleum Products (+36.31%), while the largest decrease came from Grain (-24.01%).

In the West, BNSF’s total volumes were up (+0.22%), with the largest increase coming from Chemicals (+10.25%), while the largest decrease came from Metallic Ores and Metals (-11.16%). UP’s total volumes were up (+3.35%), with the largest increase coming from Other (+20.63%), while the largest decrease came from Intermodal Units (-2.08%).

In Canada, CN’s total volumes were down (-1.04%), with the largest increase coming from Grain (+31.50%), while the largest decrease came from Metallic Ores and Metals (-22.67%). CPKCS’s total volumes were down (-18.39%), with the largest increase coming from Nonmetallic Minerals (+8.06%), while the largest decrease came from Forest Products (-68.19%).

Source Data: AAR – PFL Analytics

Rig Count

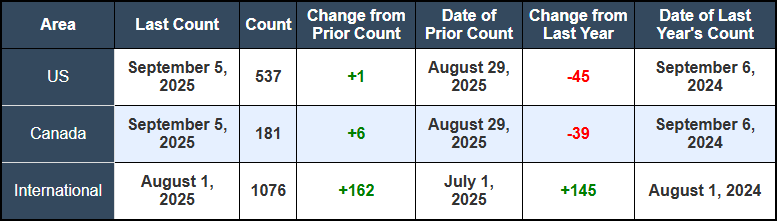

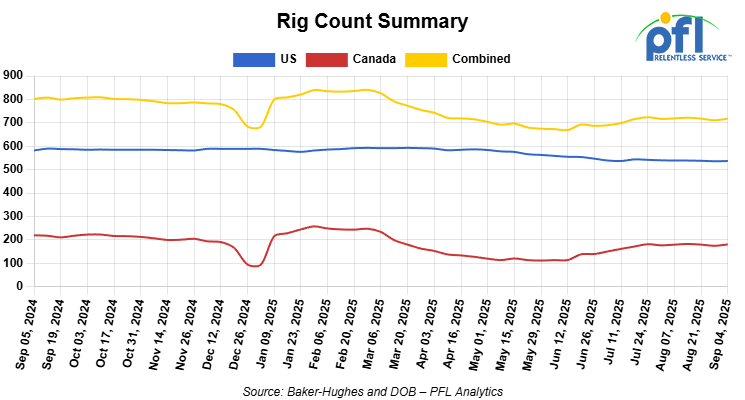

North American rig count was up by +7 rigs week-over-week. The US rig count was up by +1 rig week-over-week, but down by -45 rigs year-over-year. The US currently has 537 active rigs. Canada’s rig count was up by +6 rigs week-over-week and down by -39 rigs year-over-year. Canada currently has 181 active rigs. Overall, year-over-year we are down by -84 rigs collectively.

International rig count which is reported monthly was up by +162 rigs month-over-month and up by +145 rigs year-over-year. Internationally, there are 1076 active rigs

North American Rig Count Summary

We are watching a few things out there for you:

PFL is Watching OPEC

OPEC+ agreed to further raise oil production yesterday, as its leader Saudi Arabia pushes to regain market share, while slowing the pace of increases compared with previous months due to an anticipated weakening of global demand.

OPEC+ has been increasing production since April after years of cuts to support the oil market, but the Sunday decision to further boost output came as a surprise amid a likely looming oil glut in the northern hemisphere winter months.

PFL is Watching Axis in the East – Chaos in the West

Last week was an eye opener in energy markets, folks. In the East, a wartime axis between Russia and North Korea, blessed by Beijing, is solidifying with alarming speed and clarity. In North America, the picture is one of policy chaos, market friction, and a massive new source of demand (AI) that is adding a new layer of uncertainty.

In the East, what does the Putin-Kim Summit in Beijing mean for the Market?

The high-profile meeting between Russia’s Vladimir Putin and North Korea’s Kim Jong Un that took place in Beijing on September 3rd was a public confirmation of a functional wartime pact. The leaders signaled a new era of coordinated opposition to the West.

Kim pledged “full support” for Russia, calling it a “fraternal duty.” South Korean intelligence estimates that North Korea has already sent 15,000 troops to Russia, along with vast quantities of artillery and ballistic missiles. Putin publicly praised the “bravery and heroism” of North Korean soldiers, confirming their direct role in the conflict. This alliance creates a closed-loop economy that is highly resistant to Western sanctions. North Korea provides Russia with the munitions and manpower needed to sustain its war effort, putting pressure on Europe and its energy security. In return, Russia provides Pyongyang with a vital lifeline of food, fuel, and, most critically, advanced military and aerospace technology that can accelerate its nuclear and satellite programs.

The formalization of this axis is a major geopolitical event. It demonstrates how sanctioned states can band together to create parallel systems that undermine the effectiveness of Western economic pressure. For Asia, it raises the regional threat level, forcing South Korea and Japan to deepen their military alliances with the United States. We should continue to see volatile energy markets in the days to come as long-term trade seems to be unraveling yet repositioning itself all at the same time.

We are watching Petroleum Carloads

The four-week rolling average of petroleum carloads carried on the six largest North American railroads rose to 28,262 from 27,950 which was an increase of +312 rail cars week-over-week. Canadian volumes were higher. CPKC’s shipments were higher by 12.0% week over week, CN’s volumes were higher by +7.0% week-over-week. U.S. shipments were mixed. The BN had the largest percentage increase and was up by +8.0%. The CSX had the largest percentage decrease and was down by -10%.

We are Watching Ohio

The Ohio Rail Development Commission (ORDC) has released its updated State Rail Plan, underscoring the state’s commitment to keeping freight rail at the forefront of its transportation strategy. With more than 5,000 miles of track in operation, Ohio’s rail system already serves as a backbone for the region’s industrial supply chains—supporting over 600,000 jobs and generating $164 billion in annual business output. The state is doubling down on freight as the priority, the state and is signaling a clear path forward for industries that depend on reliable, high-volume rail service. For more information on the states rail plan please click here. Bottom line, it’s great for rail – stay tuned to PFL, we are watching this on.

We are Watching the CPKC

Canadian Pacific Kansas City (CPKC) is making strides in its hydrogen-powered locomotive pilot it says. The company currently operates three hydrogen locomotives, including one actively pulling coal trains under commercial service conditions – making it one of the first hydrogen units in the world to prove itself outside of test tracks.

In May 2025, CPKC placed orders for four additional CP 1200 hydrogen locomotives, expanding the pilot fleet to seven units. The railway is also collaborating with CSX on developing hydrogen retrofit kits, which would allow existing diesel-electric locomotives to be converted rather than replaced outright—a potentially game-changing step in cost and scalability. Hydrogen remains in the early stages of rail deployment, but CPKC’s program is drawing industry-wide attention as policymakers and shippers press for lower-emission transport.

We Continue to watch the Canadian Left Wing Prime Minister

On Friday of last week at a press conference in Mississauga, Ontario, Canada Left Wing Carney announced that he is delaying electric vehicle sales mandate by one year and using taxpayer dollars to launch a 60-day review of the program to help find “future flexibilities and ways to reduce costs.”

Bottom line the federal electric vehicle sales mandate will not be implemented in 2026 as planned. The mandate was introduced by the Liberals under former prime minister Justin Trudeau, the mandate would have required 20% of all new vehicles sold in Canada next year to be electric. Carney said, Canada’s domestic automakers need more liquidity in the face of pressures from the ongoing trade war with the United States.

The standard as written is to rise steadily each year until 2035, by which point all new light-duty vehicles sold in Canada were to be fully electric or plug-in hybrids.

Carney was also pressed by reporters on his overall commitment to climate change, given recent policy changes which moved away from aggressive climate action from the Trudeau government. Left wing Carney said the fight against climate change is a “moral obligation” and he committed to reducing emissions, though he signaled it must be one in the context of trade and competitiveness too.

“We will keep the industrial carbon pricing. We must improve its function. And there will be a political strategy for climate competitiveness, and a strategy for nature,” Carney said.

This statement by Liberal Carney is a huge problem for Canada. The Carbon tax in Canada is a big deal and these radical hard left policies are punishing not only producers of energy, but western Canadian governments and the Canadian consumer who is already struggling. On another note, If you’re waiting on a brand-new oil pipeline to Canada’s West Coast, don’t hold your breath. Speaking in Banff last week, Trans Mountain (Government Owned) President Michael Davies said that even a best-case project would take a minimum of five years from concept to barrels flowing—and that’s if everything goes right. That puts any realistic in-service date well past 2030. Right now, optimization of current infrastructure is underway with Enbridge – Trans Mountain could increase flows by 300,000 – 400,000 barrels per day by adding additional pumping stations. A new pipeline still needs to get built – instead of talking about how long it will take you might as well start the process! If there is any good news – as more production comes online in western Canada, rail is the only way out.

The head of the Canadian Vehicle Manufacturers’ Association, said the pause on the EV mandate is “an important first step,” but still called for its repeal.

“The EV mandate imposes unsustainable costs on auto manufacturers, putting at risk Canadian jobs and investment in this critical sector of the economy,” Brian Kingston said in a media statement.

In July, Carney met with the heads of Ford Canada, Stellantis Canada and GM Canada, who told the prime minister there was no way for the industry to meet the targets set out in the EV mandate.

Bottom line, the Green Deal is still alive and well in Canada, just a little delayed – seems to us they want to go ahead and get everyone over to driving electric cars, despite the environmental aspects of doing so and the public not wanting to buy electric cars to the extent that they thought they would.

PFL is Watching Alberta’s Potential Data Centre Boom

Alberta is vying to become the next North American hub for hyperscale data centres. TransAlta’s chair confirmed last week that the utility is in active talks with developers, with agreements expected before the end of 2025. The pitch – abundant land, competitive power pricing, and proximity to energy infrastructure.

If these deals land, Alberta could see billions in investment and as much as 2 GW of new electricity demand. That’s on top of the province’s existing growth in petrochemicals and manufacturing — setting the stage for a construction surge rolling into 2026–2027. While most headlines focus on the power story, the logistics ripple effects are just as important.

Rail Impact

- Big, Heavy, Oversized Freight – Transformers, back-up generators, switchgear, and cooling systems don’t fit nicely on a flatbed. Rail is the obvious choice to move these mega-loads.

- Concrete, Steel, and Rock – Building hyperscale takes a mountain of bulk inputs. Expect rail to play a role in hauling in the raw stuff.

- Not Just Pipelines – Natural gas may power the plants, but diesel, chemicals, and specialty fuels for backup and cooling systems will still move by rail.

- Keep the Lights On – Once running, these centers need 24/7 supply chains for parts and equipment. Rail keeps that reliability in check.

- Watch the Calendar – With builds starting in 2026, expect rail demand to spike right when ag and energy flows are already stretching capacity.

At a Glance

| What’s Happening | Why It Matters for Rail | When |

|---|---|---|

| Project Freight | Transformers, HVAC, cooling gear, backup systems | 2026–2027 |

| Construction Inputs | Steel, cement, aggregates in bulk | 2026–2027 |

| Fuel & Energy Supply | Diesel, chemicals, specialty backup fuels | Post-2027 |

| Spare Parts & Operations | Constant inbound flows to keep centres reliable | Post-2027 |

| Capacity Crunch | Overlaps with ag/energy peak volumes in the West | 2026–2027 |

We are Watching Economic Indicators

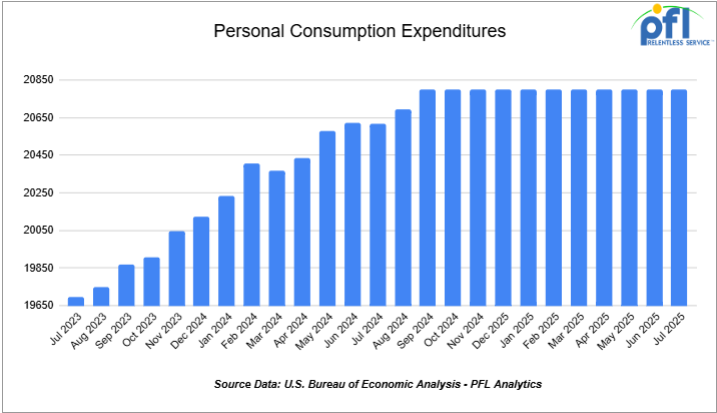

Consumer Spending

In July 2025, total consumer spending adjusted for inflation increased by 0.3% over June 2025, improving from the 0.1% gain in June. This stronger pace highlights a rebound in household demand, particularly for durable goods, and suggests consumers remain willing to spend despite economic uncertainties. According to the U.S. Bureau of Economic Analysis, the increase in current-dollar personal consumption expenditures (PCE) was $108.9 billion, driven by a $60.2 billion rise in services spending and a $48.7 billion increase in goods spending.

The personal saving rate slipped to 4.4% in July, down from 4.5% in June, indicating that consumers are drawing more on savings to support spending amid higher costs.

Year-over-year, the PCE price index rose by 2.6%, up from 2.5% in June, while core PCE inflation reached 2.9%, reflecting persistent underlying price pressures above the Federal Reserve’s 2% target.

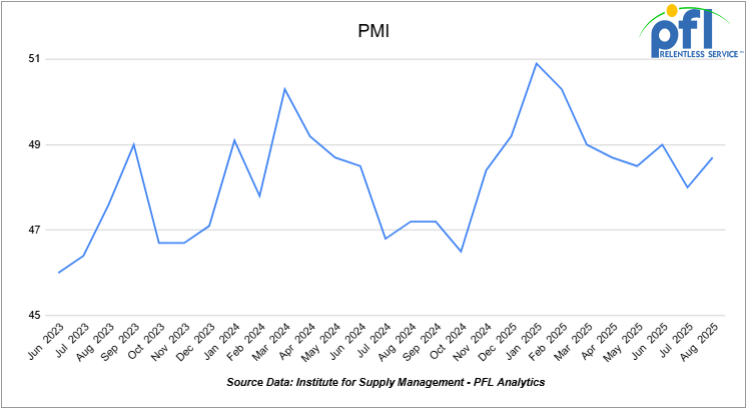

U.S. Manufacturing

The ISM Manufacturing PMI edged up to 48.7 in August, from 48 in July, but remained in contraction territory and marked the sixth consecutive month of decline in the sector. While still below the 50 threshold that signals growth, the latest reading shows contraction continuing at a slightly slower pace.

Weakness was most pronounced in production (47.8 vs. 51.4) and order backlogs (44.7 vs. 46.8), reflecting renewed softness in output and lingering challenges in sustaining demand momentum. Employment also remained weak, ticking up only modestly (43.8 vs. 43.4), as firms continued to manage headcount cautiously rather than expand hiring.

Despite the overall contraction, there were signs of stabilization. New orders returned to expansion (51.4 vs. 47.1) for the first time in six months, offering a hopeful signal of demand recovery. Supplier deliveries also lengthened (51.3 vs. 49.3), suggesting supply chain pressures accompanying stronger orders. Meanwhile, price pressures eased slightly, with the Prices Index falling to 63.7 from 64.8, continuing the recent moderation in input costs.

Overall, the data paints a picture of a manufacturing sector still under pressure, but with tentative signs of demand resilience emerging in August.

Lease Bids

- 30-50, 6000cf Steel Hopper located off of CSX or NS in East. For use in petcoke service. Period: 5 Years.

- 50, 5000CF Covered Hopper located off of UP or BN in Houston. For use in Fertilizer service. Period: 6 Months. Bid: Negotiable.Needed ASAP.

- 10, 2500CF Open Top Hopper located off of UP or BN in Texas. For use in aggregate service. Period: 5 years. Bid: Negotiable.Need Rapid Discharge Doors.

- 20, 25.5k CPC 1232 Tank located off of UP, BN, CSX, NS in OK, TX, Northeast. For use in Asphalt service. Period: 3 Years. Bid: Negotiable.

- 10, 25.5K Any Type Tank located off of CSX in Florida. For use in UCO service. Period: 2 Years. Bid: Negotiable.

- 20, 28.3K 117J Tank located off of BN in Montana. For use in Crude service. Period: 2 years. Bid: Negotiable.

- 15-20, 29K 117R Tank located off of NS or CSX in Ohio. For use in Ply Oil service. Period: 6-12 Months. Bid: Negotiable.

- 10, 30K 117R or 117J Tank located off of Any Class 1 in USA. For use in Glycerin service. Period: 1 year. Bid: Negotiable.

- 50, 23.5-25.5 DOT111 Tank located off of Any Class 1 in USA. For use in Asphalt service. Period: 5 years. Bid: Negotiable.

- 50-100, 33K 117J Tank located off of BN or UP in Bellview. For use in Butane/ service. Period: Sept-March. Bid: Negotiable.

- 4, 30K 117J Tank located off of in Michigan. For use in Food Grade Ethanol service. Period: Multi year. Bid: Negotiable.

- 10-20, 29K CPC 1232 Tank located off of CP in Washington, Iowa. For use in Biodiesel service. Period: 1 Year min. Bid: Negotiable.

- 50, 33K 117J Tank located off of CP or CN in Canada. For use in Propane service. Period: Summer. Bid: Negotiable.

- 6, 4750 Covered Hopper located off of NS in Georgia. For use in Fertilizer service. Period: 3-5 years. Bid: Negotiable.

- 100, 21.9K 117J Tank located off of All Class 1s in Midwest. For use in CO2 service. Period: 6 months. Bid: Negotiable.

Sales Bids

- 28, 3400CF Covered Hopper located off of UP BN in Texas. For use in Cement service. Bid: Negotiable.Cement Gates needed..

- 20, 17K Tank DOT111 located off of various class 1s in various locations. For use in corn syrup service. Bid: Negotiable.

- 120, Various Gondola Open-Top Aluminum Rotary located off of various class 1s in various locations. For use in Sulphur service. Bid: Negotiable.Built 2004 or later.

Lease Offers

- 60, 4750 Covered Hoppers located off of UP or BN in Eads, CO. Last used in Grain. Offer: Negotiable. UP to 5 Years, 3 Hopper, Gravity Gate, Trough Hatches.

- 100, 6250 Covered Hoppers located off of UP in US. Last used in DDG. Offer: Negotiable. 1 Year term. Dirty to Dirty. Free move on UP..

- 24, 25.5K-30K DOT111 Tanks located off of UP or BN in Texas. Last used in Base Oils. Offer: Negotiable. 1-2 Year.

- 25, 19.6K DOT111 Tanks located off of UP in US. Last used in Molases. Offer: Negotiable.

- 50, 20K DOT111 Tanks located off of UP or BN in Wichita Falls, TX. Last used in HCL. Offer: Negotiable.

- 50, 30K 117R Tanks located off of CSX, NS, or CN in Detroit. Last used in Diesel. Offer: Negotiable. Multiyear.

- 50, 20K 117J Tanks located off of All Class 1s in Multiple Locations. Last used in Styrene. Offer: Negotiable. Cars are currently moving.

- 22, 25.5K DOT111 Tanks located off of UP in Texas. Last used in Asphalt. Offer: Negotiable.

- 40, 33K Tanks 340W located off of CPKC or UP in Texas. Last used in Propane or Butane. Offer: Negotiable. Available for winter or 1 year.

Sales Offers

- 21, 50′ Boxcar Plate Cs located off of various class 1s in NM. Offer: Negotiable. End of Life.

- 3, 50′ Boxcar Plate Cs located off of various class 1s in multiple locations. Offer: Negotiable. End of Life.

- 27, 50′ Boxcar Plate Cs located off of various class 1s in PQ. Offer: Negotiable. End of Life.

- 100, 3250 Covered Hoppers located off of various class 1s in multiple locations. Offer: Negotiable. Sand Cars.

- 5, 2740 Mill Gondolas located off of various class 1s in NC. Offer: Negotiable. End of Life.

- 1, 2260 Mill Gondolas located off of various class 1s in AL. Offer: Negotiable. End of Life.

- 30, 2740 Mill Gondolas located off of various class 1s in multiple locations. Offer: Negotiable. End of Life.

- 21, 2740 Mill Gondolas located off of various class 1s in WA. Offer: Negotiable. End of Life.

- 9, 4750 Covered Hoppers located off of various class 1s in multiple locations. Offer: Negotiable. End of Life.

- 5, 4750 Covered Hoppers located off of various class 1s in multiple locations. Offer: Negotiable. End of Life.

- 50, 31.8K Tank CPC 1232s located off of UP or BN in TX. Offer: Negotiable. Requal Due in 2025.

Call PFL today to discuss your needs and our availability and market reach. Whether you are looking to lease cars, lease out cars, buy cars, or sell cars call PFL today at 239-390-2885

Live Railcar Markets

| CAT | Type | Capacity | GRL | QTY | LOC | Class | Prev. Use | Offer | Note |

|---|

PFL will be at the Following Conferences

- Where: Calgary

- Attending: David Cohen (954-729-4774), Curtis Chandler(239-405-3365), Cyndi Popov (403-402-5043)

- Where: Grand Geneva Resort

- Attending: Brian Baker (239.297.4519)

- Conference Website