“The hardest arithmetic to master is that which enables us to count our blessings.”

– Eric Hoffer

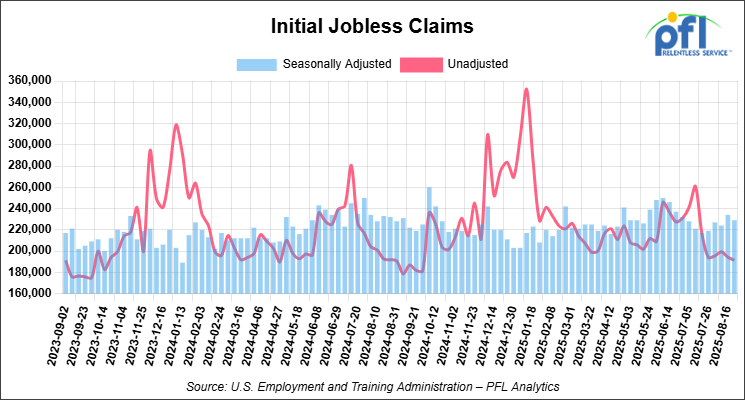

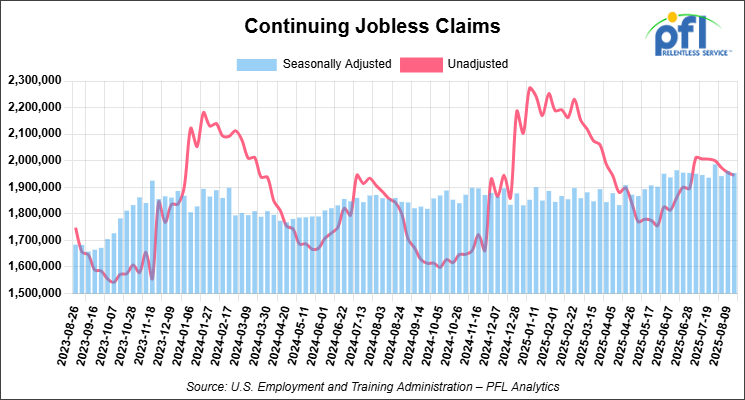

Jobs Update

• Initial jobless claims seasonally adjusted for the week ending August 28, 2025 came in at 229,000, versus the adjusted number of 234,000 people from the week prior, down 5,000 people week over week.

• Continuing jobless claims came in at 1,954,000, versus the adjusted number of 1,961,000 people from the week prior, down 7,000 week-over-week.

Stocks closed higher on Friday of last week and mixed week-over-week

The DOW closed higher on Friday of last week, up 846.24 points (1.89%), closing out the week at 45,631.74, up 685.62 points week-over-week. The S&P 500 closed higher on Friday of last week, up 96.74 points (1.52%), and closed out the week at 6,466.91, up 17.11 points week-over-week. The NASDAQ closed higher on Friday of last week, up 396.22 points (1.88%), and closed out the week at 21,496.53, down -126.45 points week-over-week.

In overnight trading, DOW futures traded lower and are expected to open at 45,429 this morning, down -172 points from Friday’s close.

Crude oil closed higher on Friday of last week and higher week-over-week

West Texas Intermediate (WTI) crude closed up 14 cents per barrel (0.22%), to close at $63.66 on Friday of last week, and up 86 cents week-over-week. Brent crude closed up 6 cents per barrel (0.09%), to close at $67.73, and up $1.88 week-over-week.

One Exchange WCS (Western Canadian Select) for October delivery settled on Friday of last week at US$12.10 below the WTI-CMA (West Texas Intermediate – Calendar Month Average). The implied value was US$51.82 per barrel.

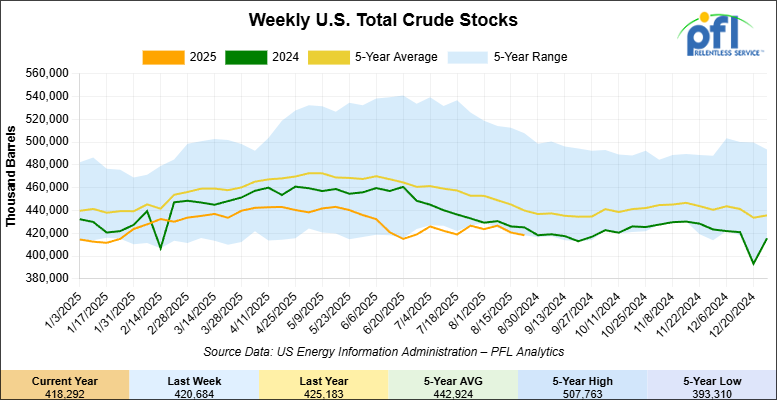

U.S. commercial crude oil inventories (excluding those in the Strategic Petroleum Reserve) decreased by 2.4 million barrels week-over-week. At 418.3 million barrels, U.S. crude oil inventories are 6% below the five-year average for this time of year.

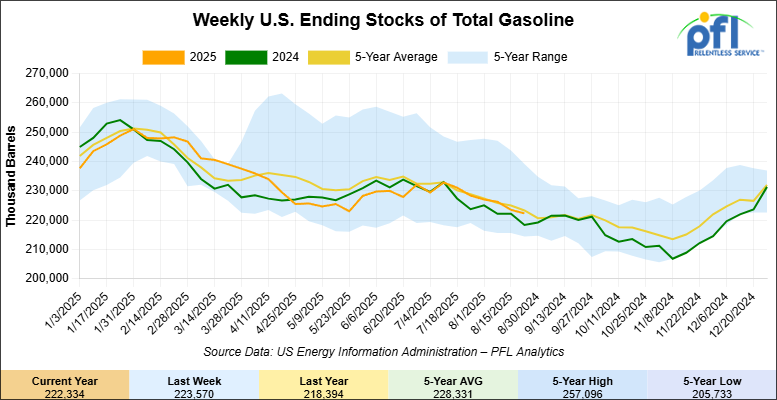

Total motor gasoline inventories decreased by 1.2 million barrels week-over-week and are at the five-year average for this time of year

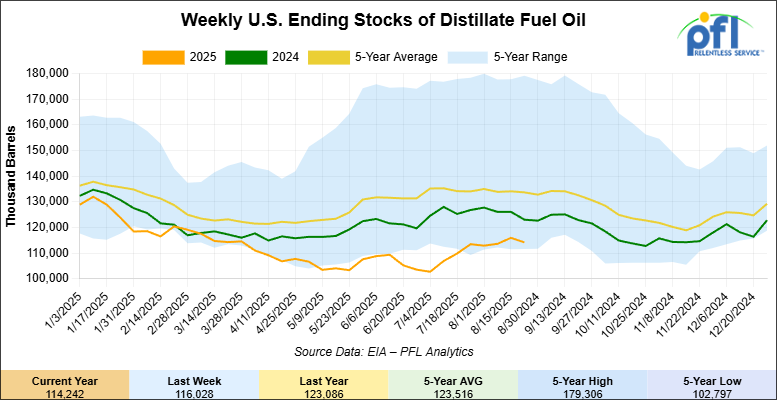

Distillate fuel inventories decreased by 1.8 million barrels week-over-week and are 15% below the five-year average for this time of year.

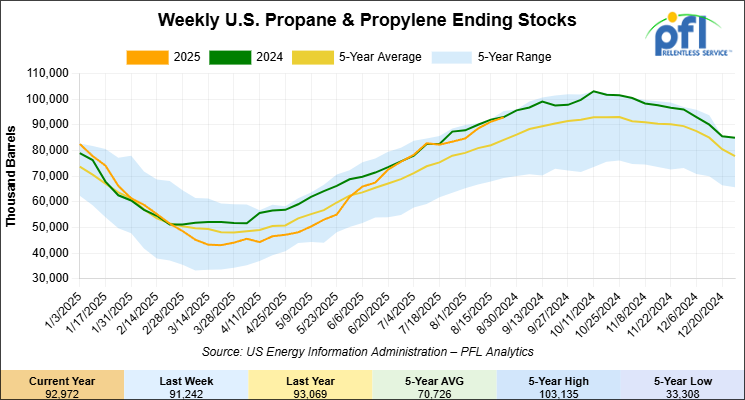

Propane/propylene inventories increased by 1.7 million barrels week-over-week and are 13% above the five-year average for this time of year.

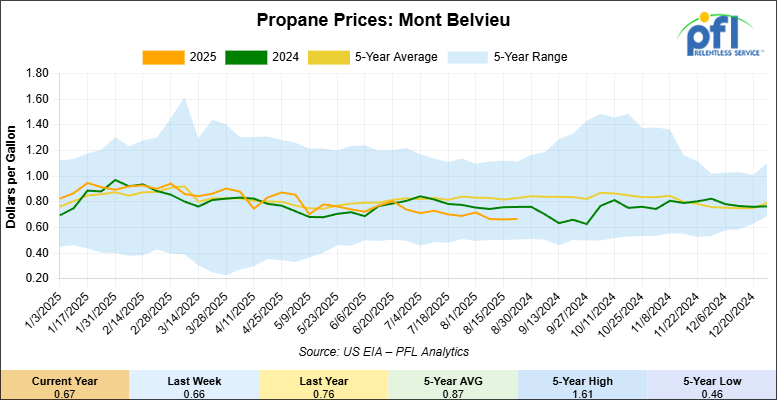

Propane prices closed at 67 cents per gallon on Friday of last week, up 1 cent per gallon week-over-week, but down 9 cents year-over-year.

Overall, total commercial petroleum inventories decreased by 4.4 million barrels during the week ending August 22, 2025.

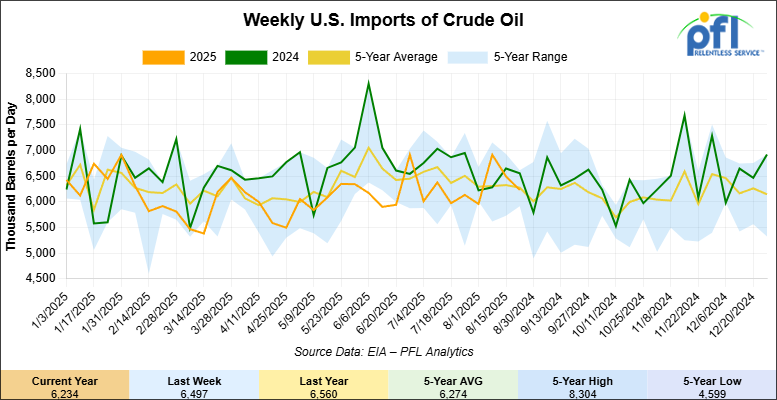

U.S. crude oil imports averaged 6.2 million barrels per day during the week ending August 22, 2025, a decrease of 263,000 barrels per day week-over-week. Over the past four weeks, crude oil imports averaged about 6.4 million barrels per day, 0.4% less than the same four-week period last year. Total motor gasoline imports (including both finished gasoline and gasoline blending components) averaged 767,000 barrels per day, and distillate fuel imports averaged 141,000 barrels per day during the week ending August 27, 2025.

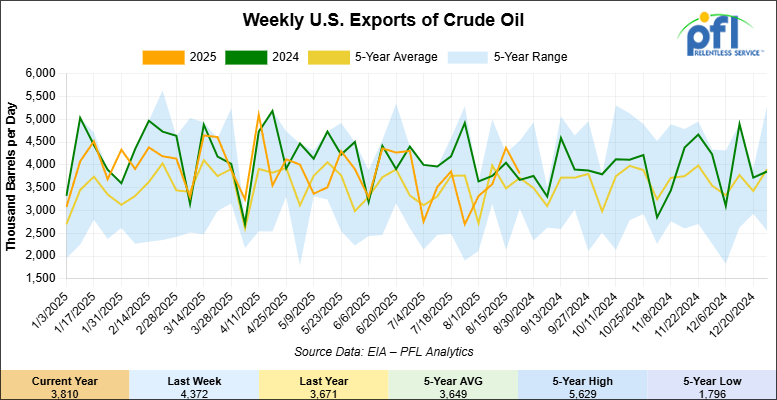

U.S. crude oil exports averaged 3.81 million barrels per day during the week ending August 22, 2025, a decrease of 562,000 barrels per day week-over-week. Over the past four weeks, crude oil exports averaged 3.769 million barrels per day.

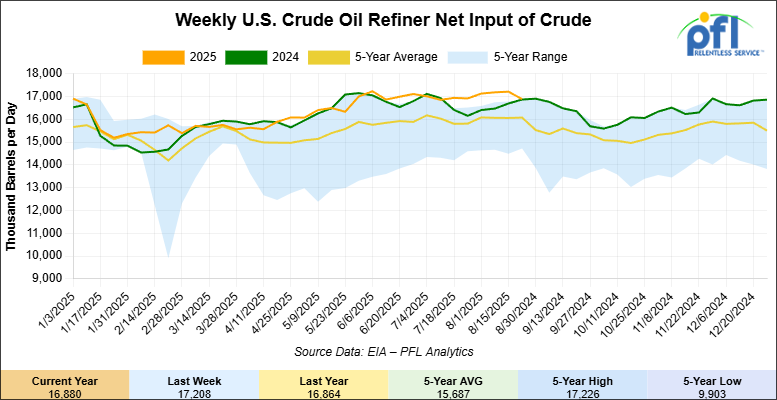

U.S. crude oil refinery inputs averaged 16.9 million barrels per day during the week ending August 22, 2025, which was 328,000 barrels per day less week-over-week.

WTI is poised to open at $65.81, up $1.80 per barrel from Friday’s close.

North American Rail Traffic

Week Ending August 27, 2025:

Total North American weekly rail volumes were down (-1.41%) in week 35, compared with the same week last year. Total Carloads for the week ending August 27th were 324,686, down (-0.57%) compared with the same week in 2024, while weekly Intermodal volume was 343,756, down (-2.19%) year over year. 6 of the AAR’s 11 major traffic categories posted year-over-year decreases. The largest decrease came from Forest Products (-11.51%), while the largest increase was Grain (+5.17%).

In the East, CSX’s total volumes were down (-0.20%), with the largest decrease coming from Metallic Ores and Metals (-20.66%), while the largest increase came from Nonmetallic Minerals (+16.71%). NS’s total volumes were up (+1.23%), with the largest increase coming from Petroleum & Petroleum Products (+31.30%), while the largest decrease came from Grain (-17.59%).

In the West, BNSF’s total volumes were down (-0.89%), with the largest increase coming from Nonmetallic Minerals (+8.13%), while the largest decrease came from Coal (-19.94%). UP’s total volumes were down (-4.39%), with the largest increase coming from Grain (+24.42%), while the largest decrease came from Nonmetallic Minerals (-13.47%).

In Canada, CN’s total volumes were up (+9.90%), with the largest increase coming from Intermodal Units (+57.21%), while the largest decrease came from Coal (-19.94%). CPKCS’s total volumes were down (-17.37%), with the largest increase coming from Grain (+10.43%), while the largest decrease came from Forest Products (-62.47%).

Source Data: AAR – PFL Analytics

Rig Count

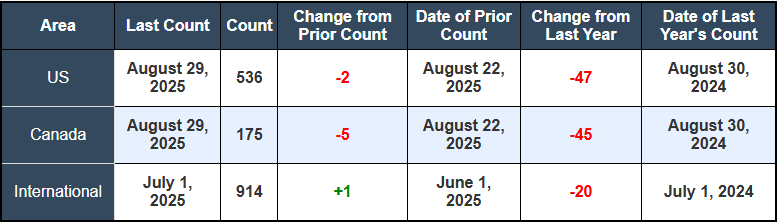

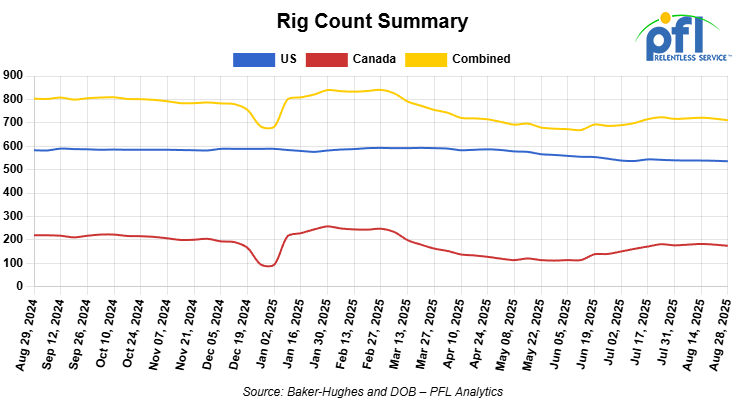

North American rig count was down by -7 rigs week-over-week. The US rig count was down by -2 rigs week-over-week, and down by -47 rigs year-over-year. The US currently has 536 active rigs. Canada’s rig count was down by -5 rigs week-over-week and down by -45 rigs year-over-year. Canada currently has 175 active rigs. Overall, year-over-year we are down by -92 rigs collectively.

North American Rig Count Summary

We are watching a few things out there for you:

We are watching Petroleum Carloads

The four-week rolling average of petroleum carloads carried on the six largest North American railroads rose to 27,950 from 27,787 which was an increase of +163 rail cars week-over-week. Canadian volumes were mixed. CPKC’s shipments were lower by -5.0% week over week, CN’s volumes were higher by +6.0% week-over-week. U.S. shipments were also mixed. CSX had the largest percentage increase and was up by +6.0%. The BNSF had the largest percentage decrease and was down by -15%.

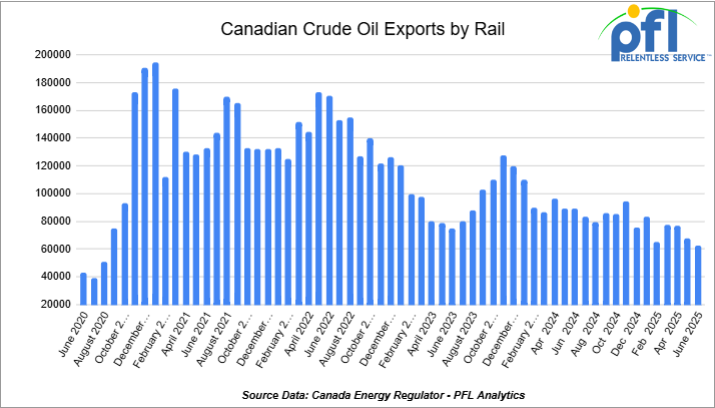

We are watching Canadian Crude by Rail

Crude by rail out of Canada decreased month over month. The Canadian Energy regulator reported late evening on August 25, that 62,847 barrels were exported per day during the month of June 2025, down from 67,686 barrels in May of 2025, a decrease of 4,839 barrels per day, month over month. This is its lowest reading since August of 2020 where Canada only exported 51,052 barrels per day.

Crude by rail will always be necessary out of Canada for stranded oil not connected by pipelines. Raw bitumen, which is shipped as a non-haz product and is not able to flow in pipelines, is competitive with pipeline tolls and is a growing market to keep an eye on.. Other factors would be existing long-term contractual commitments and basis – we really need to see basis WTI-CMA (West Texas Intermediate – Calendar Month Average) blowout to -17 per barrel for sustained periods of time to make economic sense. That may come sooner than we think, Canadian producers are resilient and we are seeing more production than anticipated and less pipelines capacity sooner than expected. There were quite a few turnarounds, including wildfires and maintenance that limited production during the summer, but that production has been coming back online. BP’s flooding at the Whiting refinery did not help matters for the Canadian Producer backing up production into Alberta diverting volumes to storage. Stay tuned to PFL for further details.

We are watching Canadian Crude Production

Canadian oilsands operators are reporting significant production growth, not from new mega-projects, but from a sharp focus on operational efficiency that is creating more demand for takeaway capacity. By shortening the duration of facility turnarounds and extending the time between them, producers have added nearly 500,000 bbls/d of production over the last five years. This increased output is putting a spotlight on export routes, with the recently expanded Trans Mountain pipeline positioning itself as a key outlet.

With Canadian production surging, any constraints on pipeline capacity—whether physical or economic – could create upside for crude-by-rail demand to get the additional barrels to market. We are expecting to see basis widen (WTI-CMA (West Texas Intermediate – Calendar Month Average) in Q4.

We Continue to watch the Canadian Left Wing Prime Minister

Last week, left-wing Prime Minister Mark Carney’s government launched a new Major Projects Office (MPO) in Calgary, (sounds like a good use of Canadian tax dollars – open up yet another government office full of bureaucrats) with a mandate to fast-track infrastructure projects and pivot Canadian trade away from its over-dependence on the U.S.. However, this initiative is being met with skepticism from industry and provincial leaders who point to the fact that contradictory federal left-wing policies remain in place.

Alberta Premier Danielle Smith has been vocal, stating that “uncertainty and added costs from countless federal environmental policies must be addressed” to attract capital. She specifically cited policies still in place by the left-wing government – including an oil tanker ban on the west coast, an emissions cap on oil and gas, and an onerous project approval process – as major impediments to investment. Enbridge CEO Greg Ebel echoed this, noting the tanker ban makes a new west coast pipeline a “pipeline to nowhere.”

Further complicating the picture, Canada’s Energy Minister Tim Hodgson said this week that a further expansion of the Trans Mountain pipeline is not considered a “project of national interest” and is unlikely to be expedited, despite the government’s stated goal of diversifying trade.

The Carney government appears to be trying to play both sides. Opening up the Calgary office is widely viewed as an “olive branch” that lacks substance as long as the administration refuses to scrap the restrictive policies that make new energy export projects practically impossible. The sad thing is, they know this and are playing the people of Alberta and all of Canada for that matter. For shippers, this policy gridlock creates significant uncertainty. The government is talking about building new export capacity while simultaneously undermining the viability of existing and future projects. You can’t make this stuff up, folks!

We are Watching North America Energy Logistics

A few things going on out there that you should be made aware of:

- Logistics Snarls Disrupt Mexico’s Fuel Supply by Rail: Fuel supply disruptions have hit multiple Mexican states this month, driven by a combination of logistical issues with state-owned Pemex’s tank trucks and a significant interruption in fuel imports by rail from the U.S.. Retailers in Chiapas, Nuevo Leon, and the Mexico City area have all experienced shortages, with market sources indicating the rail freight disruptions have particularly affected fuel importers in the Nuevo Leon and Bajio regions. The issues have been linked to stricter border controls faced by CPKC, which along with Ferromex, controls all U.S. border rail crossings.

- Canadian Crude-by-Rail Plummeted Amid Current Pipeline and Competition and tighter basis: Canadian crude-by-rail exports fell to a five-year low in June, down 29.5% year-over-year to just 62,847 barrels per day, as detailed above in our Canadian crude by rail commentary. The sharp decline is a direct result of current ample pipeline space following the expansion of the Trans Mountain pipeline (TMX), which has made costlier rail shipments less attractive. Enbridge is currently pursuing multiple projects to debottleneck and boost capacity from western Canada to the U.S. Gulf Coast, citing strong demand from U.S. refiners, however, these projects take time, and pipelines could get fuller sooner than one may think. Now that Venezuelan crude is online, there is competition for heavy oil and the U.S. is experiencing dwindling refinery capacity amid Phillips and Valero shuttering refineries in California due to the left-wing activists and the state of California itself.

PFL’s Take: The slowdown in cross-border fuel movements is a critical issue for any company shipping refined products into Mexico. With Mexico importing about half of its daily gasoline and diesel demand, rail plays a key role. Shippers should anticipate continued delays. For crude shippers, the data confirms a challenging environment for crude-by-rail.

We are watching Class 1’s Potential Mergers

The fallout from the proposed Union Pacific-Norfolk Southern merger continued to send shockwaves through the industry this week, with major developments that have significantly shifted the deal’s outlook.

- Rivals Push Back – On Tuesday of last week, CPKC officially voiced its opposition, with CEO Keith Creel warning the deal would trigger an “unnecessary wave of railway mergers” and arguing the industry should instead focus on more flexible interline partnerships. This sentiment was echoed by CN, which has also expressed support for partnerships over mergers. Adding another layer to the strategic calculus, Berkshire Hathaway Chairman Warren Buffett stated on Monday that BNSF will not make a bid for CSX or Norfolk Southern in response to the UP-NS deal.

- A Political Game-Changer at the STB -The most significant development came from Washington D.C. On Thursday of last week, President Trump fired Surface Transportation Board (STB) member Robert Primus. Primus was a vocal opponent of further industry consolidation and was the sole dissenting vote in the 2023 approval of the CPKC merger.

The removal of Primus is a political game-changer that fundamentally increases the odds of the UP-NS merger’s approval. For shippers, this elevates the long-term risk of a rail duopoly, as a BNSF-CSX merger would likely follow in an effort to remain competitive. Such a scenario would drastically reduce carrier options and could lead to structurally higher rates and less leverage for shippers in contract negotiations. Statements from CPKC and Warren Buffett suggest that rivals are proceeding with caution, but the pressure to respond to a combined UP-NS will be immense.

In other Class 1 news:

- CSX Named Maersk’s Intermodal Supplier of the Year: On Tuesday of last week, CSX announced it has been recognized by Maersk as its Intermodal Supplier of the Year in North America for 2025. Maersk commended CSX’s dedication to improving on-time performance and delivering industry-leading reliability. For shippers, this award serves as a key performance indicator, signaling that CSX is delivering high-quality service on critical metrics that matter for supply chain efficiency.

- Union Pacific Expands ‘Focus Sites’ Program: On Monday, Union Pacific announced it has added 15 new “Focus Sites” across eight states to its network. Significantly, 12 of the new sites are located on short line railroads, a move designed to expand UP’s network reach and give shippers greater and faster access to domestic and global markets. This expansion provides shippers looking to grow their operations with a clear roadmap of pre-vetted locations that can simplify the process of establishing or expanding rail service.

We are Watching the “Green Old Deal” – Solar Struggles

You know what they say, folks – in with a stroke of a pen and out with a stroke of a pen. Looks as though solar and wind are on the way out. We have always said wind does not make sense for many reasons (including, but not limited to, killing birds, beaching whales, and windmills do not last as long as they think, wind does not blow all the time…)

We on the other hand, have never wrapped our heads around large-scale solar projects that are clearly disruptive to the environment in many ways. Recently, a significant trade probe into solar panel imports advanced last week. On Friday of last week, the U.S. International Trade Commission (ITC) issued an affirmative preliminary injury determination in an anti-dumping investigation targeting solar cells from Laos, Indonesia, and India. The petition, filed by a coalition of U.S. manufacturers including First Solar and Hanwha Qcells, alleges that Chinese firms in those countries are selling products at unfairly low prices. This finding allows the Department of Commerce to proceed with its investigation, with a preliminary decision on potential duties expected by December 15.

Solar companies are struggling out there – installers and manufacturers alike as the shine on solar is dissipating. Mexico announced a 50% tariff on Chinese-made Solar panels last week as trade wars as it relates to solar are taking shape worldwide. In fact, Mexico slapped a range of tariffs on a wide range of goods, including an immediate temporary ban on finished footwear imports from China, and the suspension of small-package shipments to the U.S. via its postal service. This latter move is in direct response to Washington ending the de minimis rule that allowed packages under $800 to enter the U.S. duty-free, a change that took effect Friday of last week.

What does this mean for rail – less solar panels reaching U.S. shores leading to short-term decreases in rail movement to site, fossil fuel shippers (crude, diesel, heating oil and LPG producers on the back of increased natural gas production for power generation) should benefit. Eventually, these changes should lead to more stable or increased volumes for tank car movements. Stay tuned to PFL, we are watching this one closely.

We are Watching Wage Pressures and Funding Pullbacks

- U.S. Labor – Signalmen Reach Tentative Agreement: On Tuesday of last week, the National Carriers Conference Committee (NCCC) and the Brotherhood of Railroad Signalmen (BRS) reached a tentative national agreement. The five-year deal, now subject to ratification, includes an 18.8% wage increase and enhanced health benefits. For shippers, this agreement is a positive development, as it reduces the immediate threat of labor disruptions on the U.S. rail network, promoting greater operational stability.

- U.S. Regulatory – DOT Withdraws California High-Speed Rail Funding: The U.S. Department of Transportation announced on Tuesday of last week that the Federal Railroad Administration has withdrawn over $175 million in federal funding for four projects related to California’s High-Speed Rail system. Transportation Secretary Sean P. Duffy cited the project’s lack of progress as the reason for the move.

This week’s events underscore a period of intense strategic repositioning across the industry. The political shakeup at the STB makes the UP-NS merger appear far more likely, forcing rivals and shippers to accelerate their strategic planning for a fundamentally altered competitive landscape. Simultaneously, new trade actions from Mexico and the U.S. are creating immediate headwinds for cross-border supply chains, particularly in the e-commerce sector.

For energy shippers, the combination of surging Canadian crude production and a U.S. trade probe that could hamper solar development suggests a potentially stronger outlook for crude-by-rail demand. The key takeaway is that while long-term structural changes are in motion, near-term trade and commodity-specific developments are creating immediate risks and opportunities for shippers.

We are watching Key Economic Indicators

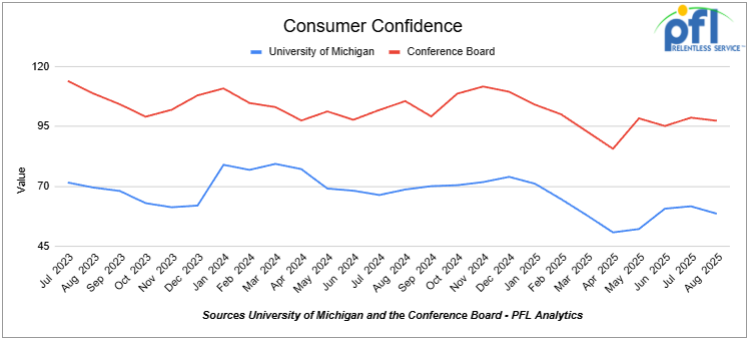

Consumer Confidence

The Conference Board’s Index of Consumer Confidence decreased to 97.4 in August 2025, down from 98.7 in July.

The University of Michigan’s Index of Consumer Sentiment decreased to 58.6 in August, down from 61.7 in July.

Lease Bids

- 30-50, 6000cf Steel Hopper located off of CSX or NS in East. For use in petcoke service. Period: 5 Years.

- 50, 5000CF Covered Hopper located off of UP or BN in Houston. For use in Fertilizer service. Period: 6 Months. Bid: Negotiable.Needed ASAP.

- 10, 2500CF Open Top Hopper located off of UP or BN in Texas. For use in aggregate service. Period: 5 years. Bid: Negotiable.Need Rapid Discharge Doors.

- 20, 25.5k CPC 1232 Tank located off of UP, BN, CSX, NS in OK, TX, Northeast. For use in Asphalt service. Period: 3 Years. Bid: Negotiable.

- 10, 25.5K Any Type Tank located off of CSX in Florida. For use in UCO service. Period: 2 Years. Bid: Negotiable.

- 20, 28.3K 117J Tank located off of BN in Montana. For use in Crude service. Period: 2 years. Bid: Negotiable.

- 15-20, 29K 117R Tank located off of NS or CSX in Ohio. For use in Ply Oil service. Period: 6-12 Months. Bid: Negotiable.

- 10, 30K 117R or 117J Tank located off of Any Class 1 in USA. For use in Glycerin service. Period: 1 year. Bid: Negotiable.

- 50, 23.5-25.5 DOT111 Tank located off of Any Class 1 in USA. For use in Asphalt service. Period: 5 years. Bid: Negotiable.

- 50-100, 33K 117J Tank located off of BN or UP in Bellview. For use in Butane/ service. Period: Sept-March. Bid: Negotiable.

- 4, 30K 117J Tank located off of in Michigan. For use in Food Grade Ethanol service. Period: Multi year. Bid: Negotiable.

- 10-20, 29K CPC 1232 Tank located off of CP in Washington, Iowa. For use in Biodiesel service. Period: 1 Year min. Bid: Negotiable.

- 50, 33K 117J Tank located off of CP or CN in Canada. For use in Propane service. Period: Summer. Bid: Negotiable.

- 6, 4750 Covered Hopper located off of NS in Georgia. For use in Fertilizer service. Period: 3-5 years. Bid: Negotiable.

- 100, 21.9K 117J Tank located off of All Class 1s in Midwest. For use in CO2 service. Period: 6 months. Bid: Negotiable.

Sales Bids

- 28, 3400CF Covered Hopper located off of UP BN in Texas. For use in Cement service. Bid: Negotiable.Cement Gates needed..

- 20, 17K Tank DOT111 located off of various class 1s in various locations. For use in corn syrup service. Bid: Negotiable.

- 120, Various Gondola Open-Top Aluminum Rotary located off of various class 1s in various locations. For use in Sulphur service. Bid: Negotiable.Built 2004 or later.

Lease Offers

- 60, 4750 Covered Hoppers located off of UP or BN in Eads, CO. Last used in Grain. Offer: Negotiable. UP to 5 Years, 3 Hopper, Gravity Gate, Trough Hatches.

- 100, 6250 Covered Hoppers located off of UP in US. Last used in DDG. Offer: Negotiable. 1 Year term. Dirty to Dirty. Free move on UP..

- 24, 25.5K-30K DOT111 Tanks located off of UP or BN in Texas. Last used in Base Oils. Offer: Negotiable. 1-2 Year.

- 25, 19.6K DOT111 Tanks located off of UP in US. Last used in Molases. Offer: Negotiable.

- 50, 20K DOT111 Tanks located off of UP or BN in Wichita Falls, TX. Last used in HCL. Offer: Negotiable.

- 50, 30K 117R Tanks located off of CSX, NS, or CN in Detroit. Last used in Diesel. Offer: Negotiable. Multiyear.

- 50, 20K 117J Tanks located off of All Class 1s in Multiple Locations. Last used in Styrene. Offer: Negotiable. Cars are currently moving.

- 22, 25.5K DOT111 Tanks located off of UP in Texas. Last used in Asphalt. Offer: Negotiable.

- 40, 33K Tanks 340W located off of CPKC or UP in Texas. Last used in Propane or Butane. Offer: Negotiable. Available for winter or 1 year.

Sales Offers

- 21, 50′ Boxcar Plate Cs located off of various class 1s in NM. Offer: Negotiable. End of Life.

- 3, 50′ Boxcar Plate Cs located off of various class 1s in multiple locations. Offer: Negotiable. End of Life.

- 27, 50′ Boxcar Plate Cs located off of various class 1s in PQ. Offer: Negotiable. End of Life.

- 100, 3250 Covered Hoppers located off of various class 1s in multiple locations. Offer: Negotiable. Sand Cars.

- 5, 2740 Mill Gondolas located off of various class 1s in NC. Offer: Negotiable. End of Life.

- 1, 2260 Mill Gondolas located off of various class 1s in AL. Offer: Negotiable. End of Life.

- 30, 2740 Mill Gondolas located off of various class 1s in multiple locations. Offer: Negotiable. End of Life.

- 21, 2740 Mill Gondolas located off of various class 1s in WA. Offer: Negotiable. End of Life.

- 9, 4750 Covered Hoppers located off of various class 1s in multiple locations. Offer: Negotiable. End of Life.

- 5, 4750 Covered Hoppers located off of various class 1s in multiple locations. Offer: Negotiable. End of Life.

- 50, 31.8K Tank CPC 1232s located off of UP or BN in TX. Offer: Negotiable. Requal Due in 2025.

Call PFL today to discuss your needs and our availability and market reach. Whether you are looking to lease cars, lease out cars, buy cars, or sell cars call PFL today at 239-390-2885

Live Railcar Markets

| CAT | Type | Capacity | GRL | QTY | LOC | Class | Prev. Use | Offer | Note |

|---|

PFL will be at the Following Conferences

- Where: Calgary

- Attending: David Cohen (954-729-4774), Curtis Chandler(239-405-3365), Cyndi Popov (403-402-5043)

- Where: Grand Geneva Resort

- Attending: Brian Baker (239.297.4519)

- Conference Website

- Where: Loews Arlington Hotel

- Attending: Brian Baker (239.297.4519), David Cohen (954-729-4774), and Curtis Chandler (239-405-3365)

- Conference Website

- Where: The Westin Galleria Dallas

- Attending: Brian Baker (239.297.4519)

- Conference Website

- Where: The Westin Galleria Dallas

- Attending: David Cohen (954-729-4774), and Curtis Chandler (239-405-3365)

- Conference Website