“The good life is a process, not a state of being. It is a direction not a destination.”

– Carl Rogers

Jobs Update

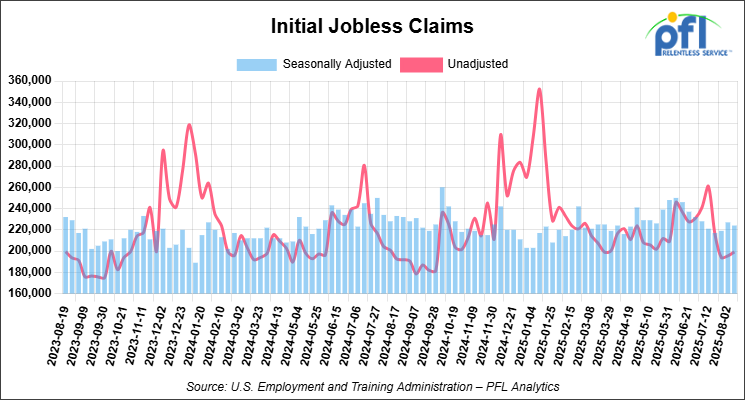

• Initial jobless claims seasonally adjusted for the week ending August 9, 2025, came in at 224,000, down 3,000 people week over week.

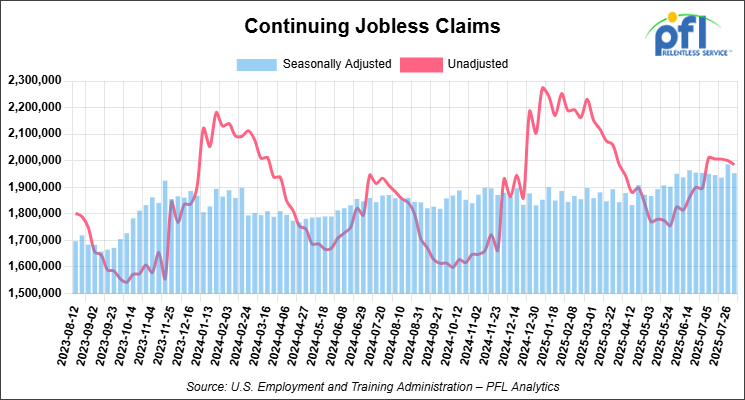

• Continuing jobless claims came in at 1,953,000, versus the adjusted number of 1,986,000 people from the week prior, down 33,000 week-over-week.

Stocks closed mixed on Friday of last week and higher week-over-week

The DOW closed higher on Friday of last week, up 34.86 points (0.08%), closing out the week at 44,946.12, up 770.51 points week-over-week. The S&P 500 closed lower on Friday of last week, down -18.74 points (-0.29%), and closed out the week at 6,449.80, up 60.35 points week-over-week. The NASDAQ closed lower on Friday of last week, down -87.69 points (-0.40%), and closed out the week at 21,622.98, up 172.96 points week-over-week.

In overnight trading, DOW futures traded higher and are expected to open at 44,994 this morning, down -46 points from Friday’s close.

Crude oil closed lower on Friday of last week and lower week-over-week

West Texas Intermediate (WTI) crude closed down -1.16 per barrel (-1.8%), to close at $62.80 on Friday of last week, and down $1.08 week-over-week. Brent crude closed down -0.99 per barrel (-1.5%), to close at $65.85, and down $0.74 week-over-week.

One Exchange WCS (Western Canadian Select) for September delivery settled on Friday of last week at US$11.50 below the WTI-CMA (West Texas Intermediate – Calendar Month Average). The implied value was US$54.35 per barrel.

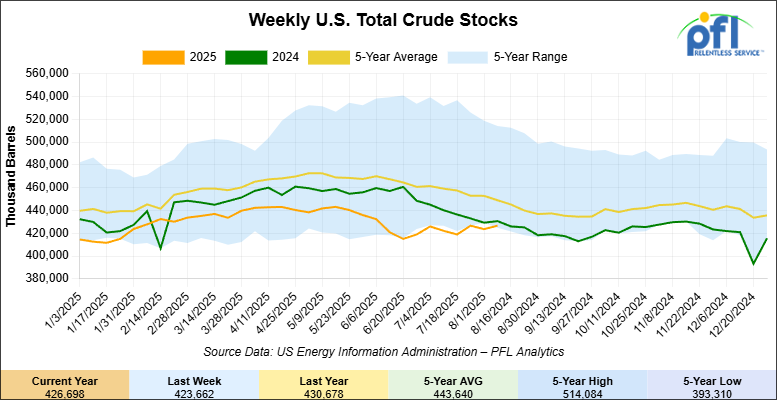

U.S. commercial crude oil inventories (excluding those in the Strategic Petroleum Reserve) increased by 3 million barrels week-over-week. At 426.7 million barrels, U.S. crude oil inventories are about 6% below the five-year average for this time of year.

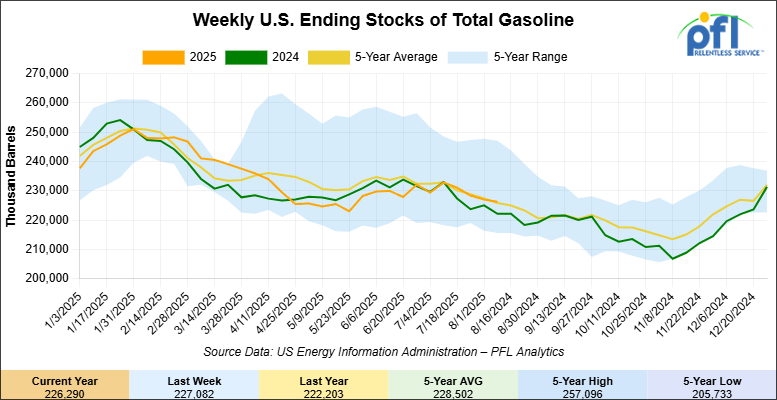

Total motor gasoline inventories decreased by 800,000 barrels week-over-week and are at the five-year average for this time of year

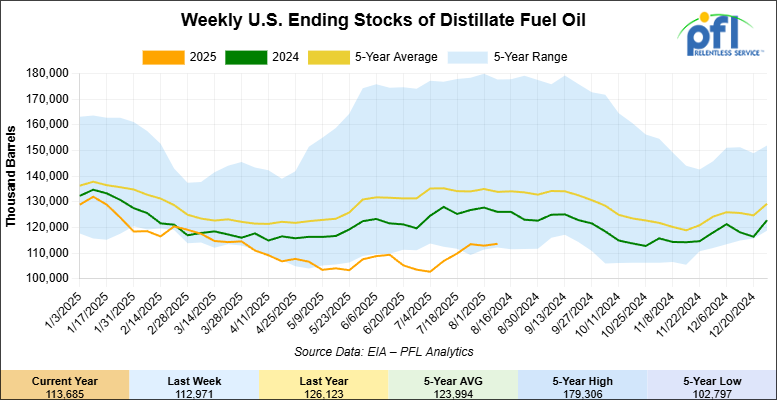

Distillate fuel inventories increased by 700,000 barrels week-over-week and are 15% below the five year average for this time of year.

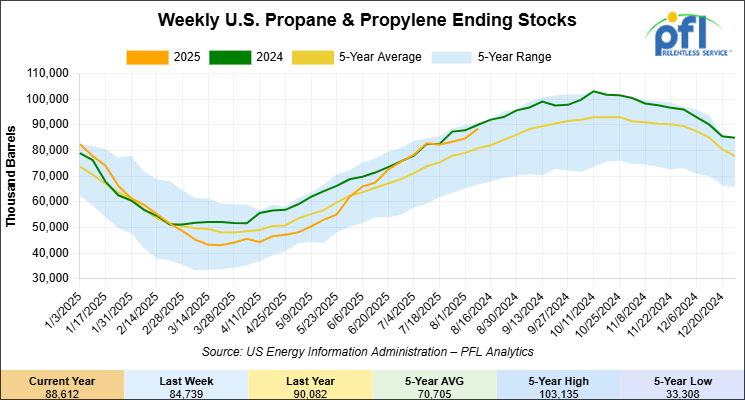

Propane/propylene inventories increased by 3.9 million barrels week-over-week and are 11% above the five-year average for this time of year

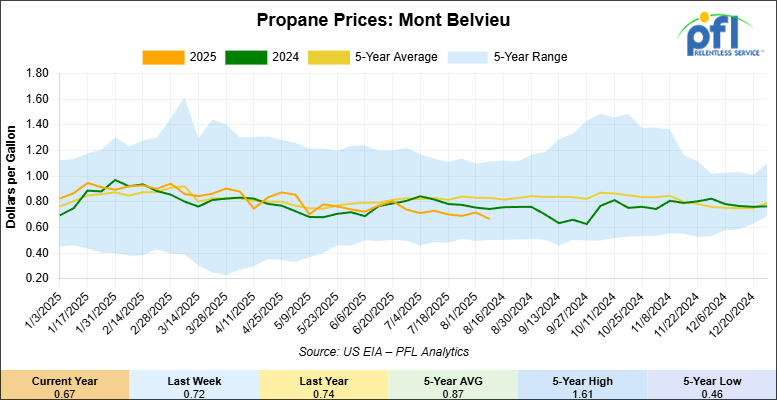

Propane prices closed at 67 cents per gallon on Friday of last week, down 5 cents per gallon week-over-week and down 8 cents year-over-year.

Overall, total commercial petroleum inventories increased by 7.5 million barrels during the week ending August 8, 2025.

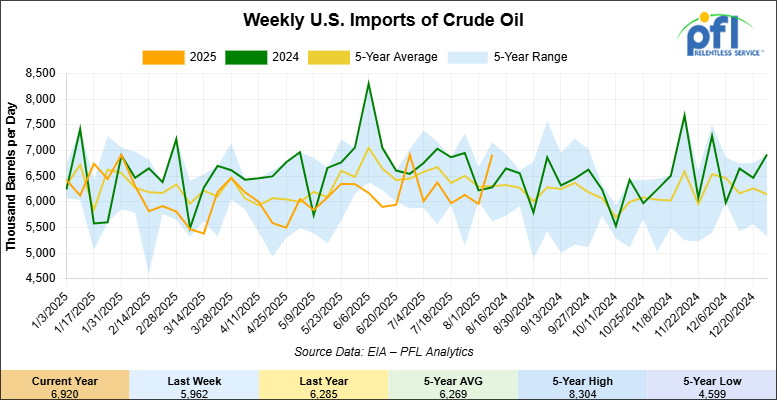

U.S. crude oil imports averaged 6.9 million barrels per day during the week ending August 8, 2025, increased by 958,000 barrels per day week-over-week. Over the past four weeks, crude oil imports averaged 6.2 million barrels per day, 5.1% less than the same four-week period last year. Total motor gasoline imports (including both finished gasoline and gasoline blending components) averaged 632,000 barrels per day, and distillate fuel imports averaged 107,000 barrels per day during the week ending August 8, 2025.

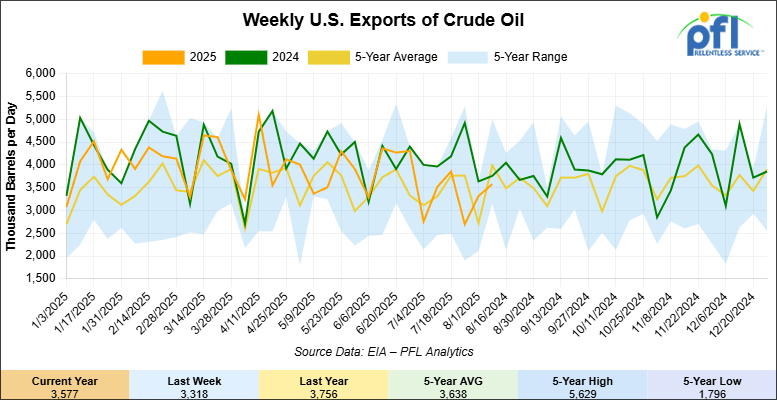

U.S. crude oil exports averaged 3.577 million barrels per day during the week ending August 8, 2025, an increase of 259,000 barrels per day week-over-week. Over the past four weeks, crude oil exports averaged 3.362 million barrels per day.

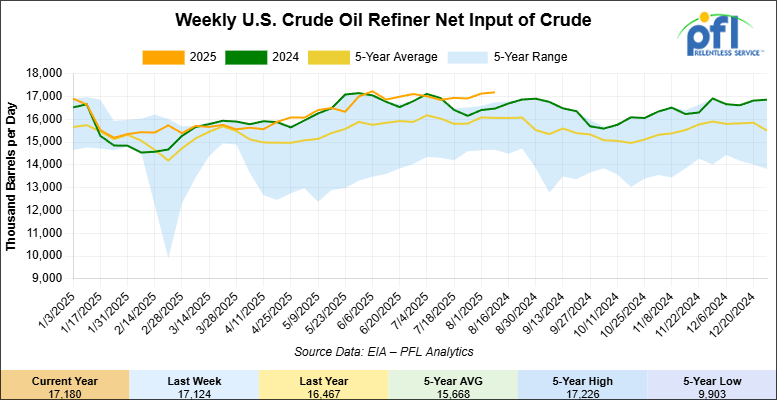

U.S. crude oil refinery inputs averaged 17.2 million barrels per day during the week ending August 8, 2025, which was 56,000 barrels per day more week-over-week.

WTI is poised to open at $63, up 20 cents per barrel from Friday’s close.

North American Rail Traffic

Week Ending August 13, 2025:

Total North American weekly rail volumes were up (+0.35%) in week 33, compared with the same week last year. Total carloads for the week ending August 13 were 321,780, down (-0.81%) compared with the same week in 2024, while weekly intermodal volume was 344,611, up (+1.45%) year over year.

6 of the AAR’s 11 major traffic categories posted year-over-year decreases. The largest decrease came from Forest Products (-13.84%), while the largest increase was Motor Vehicles & Parts (+10.00%).

In the East, CSX’s total volumes were up (+1.02%), with the largest decrease coming from Grain (-24.08%), while the largest increase came from Intermodal Units (+5.79%). NS’s volumes were up (+3.69%), with the largest increase coming from Petroleum & Petroleum Products (+39.69%), while the largest decrease came from Grain (-13.14%).

In the West, BNSF’s total volumes were up (+3.79%), with the largest increase coming from Motor Vehicles & Parts (+23.61%), while the largest decrease came from Chemicals (-16.30%). UP’s total rail volumes were down (-0.58%), with the largest increase coming from Metallic Ores & Metals (+24.20%), while the largest decrease came from Other (-16.85%).

In Canada, CN’s total rail volumes were down (-2.80%), with the largest increase coming from Grain (+37.75%), while the largest decrease came from Other (-11.93%). CPKCS’s rail volumes were down (-21.07%), with the largest increase coming from Coal (+31.41%), while the largest decrease came from Forest Products (-66.42%).

Source Data: AAR – PFL Analytics

Rig Count

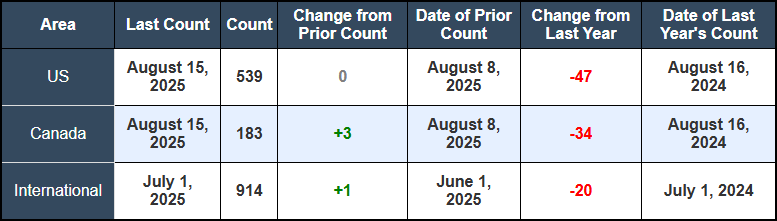

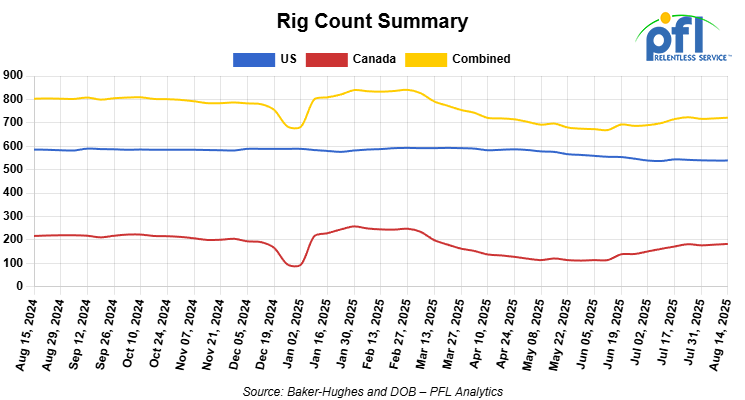

North American rig count was up by 3 rigs week-over-week. The US rig count was flat week-over-week, but down by -47 rigs year-over-year. The US currently has 539 active rigs. Canada’s rig count was up 3 rigs week-over-week, but down by -34 rigs year-over-year. Canada currently has 183 active rigs. Overall, year-over-year we are down by -81 rigs collectively.

North American Rig Count Summary

We are watching a few things out there for you:

We are Watching Petroleum Carloads

The four-week rolling average of petroleum carloads carried on the six largest North American railroads rose to 27,841 from 28,164, which was a decrease of -323 rail cars week-over-week. Canadian volumes were mixed. CPKC’s shipments were higher by +4.0% week over week, CN’s volumes were up down -10.0% week-over-week. U.S. shipments were also mixed. The BN was the sole decliner and was down by -14.0%. The NS had the largest percentage increase and was up by +8.0%.

We are Watching Intermodal Networks

Our ports once predictable have shown extreme divergence. The North American intermodal landscape seems stable. Transatlantic routes are seeing volatility affecting East Coast operations. Meanwhile, the U.S. – Mexico corridor is experiencing a boom in efficiency and new service offerings..

East Coast Headwinds from European Port Congestion

Persistent operational issues at Europe’s primary container gateways at Rotterdam, Hamburg, and Antwerp, are creating a ripple effect that has reached North American shores. Chronic underinvestment, labor disruptions, and inland bottlenecks are causing “vessel bunching,” where ships arrive at U.S. and Canadian East Coast ports in unpredictable, concentrated waves.

- Direct Network Impact: This volatility is creating surges at key ports like NY/NJ and Savannah, stressing major rail corridors to inland hubs like Chicago and Memphis.

- Equipment Dislocation: The most significant consequence for inland rail is the disruption to equipment cycles. Delayed vessels and congested ports slow the return of containers and chassis, creating shortages at critical inland terminals.

- Shipper Reality: The traditional just-in-time model for European-origin cargo is no longer reliable. Shippers are building buffer inventory to account for unpredictable transit times.

New Americold-CPKC Hub Anchors U.S.-Mexico Cold Chain

Americold and Canadian Pacific Kansas City (CPKC) celebrated the grand opening of a new $120+ million temperature-controlled import-export hub in Kansas City on Tuesday of last week. The 335,000-square-foot facility is an anchor for the Mexico Midwest Express (MMX), North America’s only single-line rail service for refrigerated goods between the U.S. and Mexico.

- Strategic Importance: This is Americold’s first facility on the CPKC network and is described by CPKC’s CEO as “the first of many across our unrivaled North American network.” It solidifies Kansas City’s role as a key logistics hub for cross-border food and beverage supply chains.

- Shipper Benefits: The hub is designed to streamline the cold chain by offering on-site USDA inspections to circumvent potential border delays and handling containers exceeding 50,000 pounds, reducing highway congestion.

- Market Impact: Expected to create nearly 190 new jobs, the facility is a tangible result of the increased efficiency and faster transit times being offered on the CPKC network, which has seen some intermodal volumes grow at twice the market rate.

This investment provides a clear signal to shippers of temperature-controlled goods that the U.S.-Mexico rail corridor is a rapidly maturing and viable alternative to long-haul trucking. For railcar owners and lessors, the development of this and future hubs will create sustained demand for refrigerated and other specialized railcars to service the growing, high-value, cross-border food trade.

We are Watching the Booming Carload Sector

The carload segment is poised for a period of sustained growth, anchored by a massive expansion in the Permian Basin. This opportunity, however, is unfolding in a new era of heightened regulatory pressure focused on the very commodities—petrochemicals and hazardous materials—that are central to this growth.

Permian Expansion Signals Long-Term Demand

Billions of dollars in new energy infrastructure are set to create a structural, long-term demand driver for carload rail, particularly for covered hoppers and tank cars.

- Upstream Catalyst: Enterprise Products Partners’ $580 million acquisition from Occidental Petroleum secures the feedstock for a new wave of natural gas processing plants.

- Massive New Capacity: The new Athena plant, slated to come online in late 2026, is part of a larger build-out that will significantly increase the region’s capacity to produce Natural Gas Liquids (NGLs).

- Downstream Rail Demand: While pipelines move raw gas and NGLs to the Gulf Coast, rail is the essential mode for transporting the finished products. Petrochemical plants “crack” gas into high-value plastic pellets (moved in covered hoppers) and liquid chemicals or NGLs (moved in tank cars) for domestic use and export.

The build-out solidifies the Gulf Coast’s role as a global hub, creating opportunities for traders in logistics infrastructure, such as transload and storage facilities, that will be needed to connect the new production to the rail network.

Regulatory Pressure Intensifies After Hazmat Derailment

The growth in petrochemical carloads is happening under an increasingly watchful regulatory eye. A recent derailment in Texas has amplified the pressure on both railroads and shippers to enhance safety protocols.

- New Federal Rules: The U.S. is implementing new mandates, including a PHMSA rule requiring real-time, electronic train consist information for first responders. While the original compliance deadline for Class I railroads was June 24, 2025, federal regulators have granted a one-year period of “enforcement discretion” due to implementation challenges, effectively pushing the compliance deadline to June 24, 2026.

- Sweeping Legislation Proposed: Congress is considering the Railway Safety Act of 2025, which proposes mandates for wayside defect detectors, two-person crews, and stricter inspection protocols.

- Shared Responsibility: The regulatory focus makes it clear that safety is a shared burden. Shippers who own or lease their own fleets are under increasing pressure to ensure their railcars are meticulously maintained and “inspection-ready” at all times.

This new regulatory landscape elevates the importance of fleet quality. Well-maintained, modern railcars that meet the latest safety standards will command a premium, and owners should see this as a moment to audit fleets and invest in upgrades. For hazmat shippers, proactive maintenance is now a critical component of risk management, as a failure to keep a private fleet compliant will result in operational downtime, higher costs, and increased liability. It seems to us that the costs of rail and moving product around is going to get more expensive as time goes on, cutting into shippers’ bottom lines that will have to be passed onto the end user resulting in even more inflation! Stay tuned to PFL, we are watching this one.

We are Watching the Return of Venezuelan Crude and NGL’s

Shifting Spreads and Competing Supply

The market for petroleum-related rail movements is facing a complex set of new variables. The return of Venezuelan crude to the U.S. Gulf Coast is set to reshape heavy crude logistics, while NGL markets are showing a clear divergence between a bearish outlook for propane and firm demand for ethylene.

Venezuelan Crude Returns, Pressuring Rail Economics. The reinstatement of Chevron’s waiver to import Venezuelan crude marks the beginning of the end of a tight spell for heavy sour feedstocks on the Gulf Coast. This offers a direct, waterborne competitor to Canadian heavy crude delivered by rail. During the import hiatus, the discount for Western Canadian Select (WCS) crude narrowed significantly, but this trend could now reverse. The latest data shows mixed petroleum carload volumes from Canada, both CN flows and CPKC are down as pricing spreads make long-haul unviable (aside from undiluted bitumen that cannot move on pipelines.) As it stands now Canadian imports are at multi-year lows.

NGL Export Markets in the short term are impacting pressure car demand – NGL markets are sending mixed signals for tank car demand. Propane prices at Mont Belvieu hit a 10-month low last week, weighed down by a bearish export outlook and a weak arbitrage to Asia. Export volumes saw a significant sequential decline in the week ending August 8, suggesting softer demand for pressurized railcars moving product to coastal terminals. In contrast, ethylene export demand remains firm, driven by strong buying from Europe, which has now displaced Asia as the primary destination for U.S. exports. This should support continued demand for specialized ethylene tank cars.

We are Watching North Americas Labor Outlook:

Stability in the U.S., Uncertainty in Canada

The 2025 collective bargaining round presents a stark contrast between the U.S. and Canada, creating different risk profiles for shippers with cross-border supply chains.

- U.S. Progress: In the U.S., nine of the twelve major rail unions have already ratified national “pattern agreements,” delivering an 18.8% wage increase over five years and enhanced benefits, largely without third-party intervention.

- Canadian Contention: In Canada, negotiations broke down, leading to a lockout and federal intervention. A new contract is now being decided by a third-party arbitrator, a move the union is challenging in court.

The key takeaway for all stakeholders is the divergent risk profile. The low risk of a major U.S. rail strike provides a stable outlook for domestic network planning. In contrast, the Canadian situation, while stable for now due to binding arbitration, remains more volatile. The union’s legal challenge to government intervention signals underlying tensions that could pose a long-term risk for cross-border supply chains.

We are Watching Key Economic Indicators

Producer Price Index

In July, the PPI for final demand rose 0.9% m/m after being flat in June, and increased 3.3% y/y. Core PPI (final demand less foods, energy, and trade services) rose 0.6% m/m and 2.8% y/y. The monthly increase was led by services (+1.1%), including a 2.0% rise in trade margins; transportation and warehousing rose 0.9–1.0%, and services excluding trade, transportation, and warehousing were up 0.7%. Goods prices advanced 0.7%, including +1.4% for foods, +0.9% for energy, and +0.4% for goods excluding food and energy. Gasoline fell 1.8% on the month.

The CPI increased 0.2% m/m in July (seasonally adjusted), after 0.3% in June. Over the past 12 months, the all-items index rose 2.7% y/y (not seasonally adjusted). Core CPI (all items less food and energy) rose 0.3% m/m and 3.1% y/y. Within the month, shelter +0.2% and was the primary driver; food was unchanged (food at home −0.1%, food away from home +0.3%); energy −1.1% with gasoline −2.2%, electricity −0.1%, and natural gas −0.9%.

Lease Bids

- 30-50, 6000cf Steel Hopper located off of CSX or NS in East. For use in petcoke service. Period: 5 Years.

- 50, 5000CF Covered Hopper located off of UP or BN in Houston. For use in Fertilizer service. Period: 6 Months. Bid: Negotiable.Needed ASAP.

- 10, 2500CF Open Top Hopper located off of UP or BN in Texas. For use in aggregate service. Period: 5 years. Bid: Negotiable.Need Rapid Discharge Doors.

- 20, 25.5k CPC 1232 Tank located off of UP, BN, CSX, NS in OK, TX, Northeast. For use in Asphalt service. Period: 3 Years. Bid: Negotiable.

- 10, 25.5K Any Type Tank located off of CSX in Florida. For use in UCO service. Period: 2 Years. Bid: Negotiable.

- 20, 28.3K 117J Tank located off of BN in Montana. For use in Crude service. Period: 2 years. Bid: Negotiable.

- 15-20, 29K 117R Tank located off of NS or CSX in Ohio. For use in Ply Oil service. Period: 6-12 Months. Bid: Negotiable.

- 10, 30K 117R or 117J Tank located off of Any Class 1 in USA. For use in Glycerin service. Period: 1 year. Bid: Negotiable.

- 50, 23.5-25.5 DOT111 Tank located off of Any Class 1 in USA. For use in Asphalt service. Period: 5 years. Bid: Negotiable.

- 50-100, 33K 117J Tank located off of BN or UP in Bellview. For use in Butane/ service. Period: Sept-March. Bid: Negotiable.

- 4, 30K 117J Tank located in Michigan. For use in Food Grade Ethanol service. Period: Multi year. Bid: Negotiable.

- 10-20, 29K CPC 1232 Tank located off of CP in Washington, Iowa. For use in Biodiesel service. Period: 1 Year min. Bid: Negotiable.

- 50, 33K 117J Tank located off of CP or CN in Canada. For use in Propane service. Period: Summer. Bid: Negotiable.

- 6, 4750 Covered Hopper located off of NS in Georgia. For use in Fertilizer service. Period: 3-5 years. Bid: Negotiable.

- 100, 21.9K 117J Tank located off of All Class 1s in Midwest. For use in CO2 service. Period: 6 months. Bid: Negotiable.

Sales Bids

• 28, 3400CF located off of UP BN in Texas. For use in Cement service. Bid: Negotiable. Cement Gates needed.

• 20, 17K DOT111 located off of various class 1s in various locations. For use in corn syrup service.

Lease Offers

- 60, 4750 Covered Hoppers located off of UP or BN in Eads, CO. Last used in Grain. Offer: Negotiable. UP to 5 Years, 3 Hopper, Gravity Gate, Trough Hatches.

- 100, 6250 Covered Hoppers located off of UP. Last used in DDG. Offer: Negotiable. 1 Year term. Dirty to Dirty. Free move on UP..

- 24, 25.5K-30K DOT111 Tanks located off of UP or BN in Texas. Last used in Base Oils. Offer: Negotiable. 1-2 Year.

- 25, 19.6K DOT111 Tanks located off of UP in US. Last used in Molases. Offer: Negotiable.

- 50, 20K DOT111 Tanks located off of UP or BN in Wichita Falls, TX. Last used in HCL. Offer: Negotiable.

- 50, 30K 117R Tanks located off of CSX, NS, or CN in Detroit. Last used in Diesel. Offer: Negotiable. Multiyear.

- 50, 20K 117J Tanks located off of All Class 1s in N/A. Last used in Styrene. Offer: Negotiable. Cars are currently moving.

Sales Offers

- 21, 50′ Boxcar Plate Cs located off of various class 1s in NM. Offer: Negotiable. End of Life.

- 3, 50′ Boxcar Plate Cs located off of various class 1s in multiple locations. Offer: Negotiable. End of Life.

- 27, 50′ Boxcar Plate Cs located off of various class 1s in PQ. Offer: Negotiable. End of Life.

- 100, 3250 Covered Hoppers located off of various class 1s in multiple locations. Offer: Negotiable. Sand Cars.

- 5, 2740 Mill Gondolas located off of various class 1s in NC. Offer: Negotiable. End of Life.

- 1, 2260 Mill Gondolas located off of various class 1s in AL. Offer: Negotiable. End of Life.

- 30, 2740 Mill Gondolas located off of various class 1s in multiple locations. Offer: Negotiable. End of Life.

- 21, 2740 Mill Gondolas located off of various class 1s in WA. Offer: Negotiable. End of Life.

- 9, 4750 Covered Hoppers located off of various class 1s in multiple locations. Offer: Negotiable. End of Life.

- 5, 4750 Covered Hoppers located off of various class 1s in multiple locations. Offer: Negotiable. End of Life.

- 50, 31.8K Tank CPC 1232s located off of UP or BN in TX. Offer: Negotiable. Requal Due in 2025.

Call PFL today to discuss your needs and our availability and market reach. Whether you are looking to lease cars, lease out cars, buy cars, or sell cars call PFL today at 239-390-2885

Live Railcar Markets

| CAT | Type | Capacity | GRL | QTY | LOC | Class | Prev. Use | Offer | Note |

|---|

PFL will be at the Following Conferences

- Where: Calgary

- Attending: David Cohen (954-729-4774), Curtis Chandler(239-405-3365), Cyndi Popov (403-402-5043)

- Where: Grand Geneva Resort

- Attending: Brian Baker (239.297.4519)

- Conference Website

- Where: Loews Arlington Hotel

- Attending: Brian Baker (239.297.4519), David Cohen (954-729-4774), and Curtis Chandler (239-405-3365)

- Conference Website

- Where: The Westin Galleria Dallas

- Attending: David Cohen (954-729-4774), and Curtis Chandler (239-405-3365)

- Conference Website

- Where: The Westin Galleria Dallas

- Attending: Brian Baker (239.297.4519)

- Conference Website