“We aim above the mark to hit the mark.” – Ralph Waldo Emerson

Jobs Update

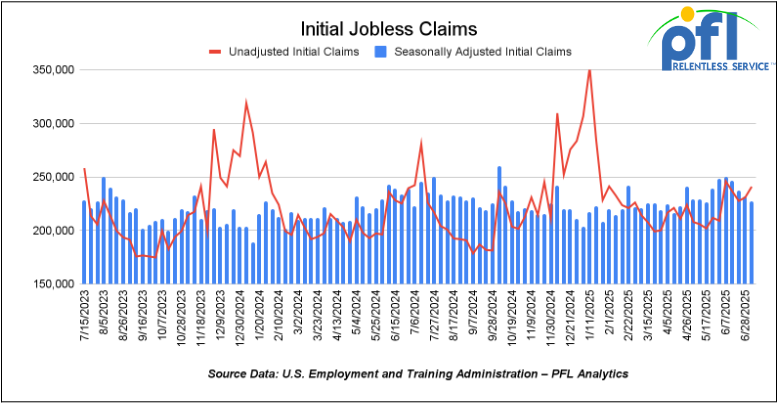

- Initial jobless claims seasonally adjusted for the week ending July 5 came in at 227,000, down 5,000 people week over week week-over-week.

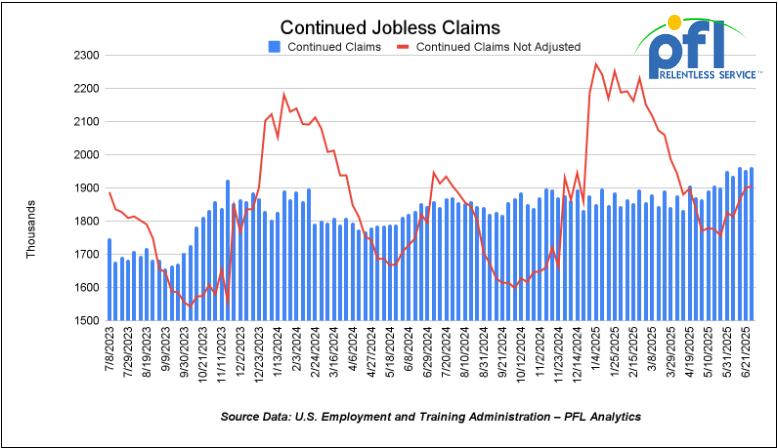

- Continuing jobless claims came in at 1.965 million people, versus the adjusted number of 1.955 million people from the week prior, up 10,000 week-over-week.

Stocks closed lower on Friday of last week and lower week-over-week

The DOW closed lower on Friday of last week, down -279.13 points (0.63%), closing out the week at 44,371.51, down -457.02 points week-over-week. The S&P 500 closed lower on Friday of last week, down 20.71 points, and closed out the week at 6,259.75, down -19.6 points week-over-week. The NASDAQ closed lower on Friday of last week, down -45.14 points, and closed out the week at 20,585.53, down -15.57 points week-over-week.

In overnight trading, DOW futures traded lower and are expected to open at 44,464 this morning down 135 points from Friday’s close.

Crude oil closed higher on Friday of last week and higher week-over-week.

West Texas Intermediate (WTI) crude closed up $1.88 per barrel (2.8%), to close at $68.45 per barrel on Friday of last week, and up $1.45 per barrel week-over-week. Brent crude closed up $1.72 USD per barrel (2.5%) on Friday of last week, to close at $70.36 per barrel, up $1.56 cents per barrel week-over-week.

One Exchange WCS (Western Canadian Select) for August delivery settled on Friday of last week at US$9.95 below the WTI-CMA (West Texas Intermediate – Calendar Month Average). The implied value was US$55.05 per barrel.

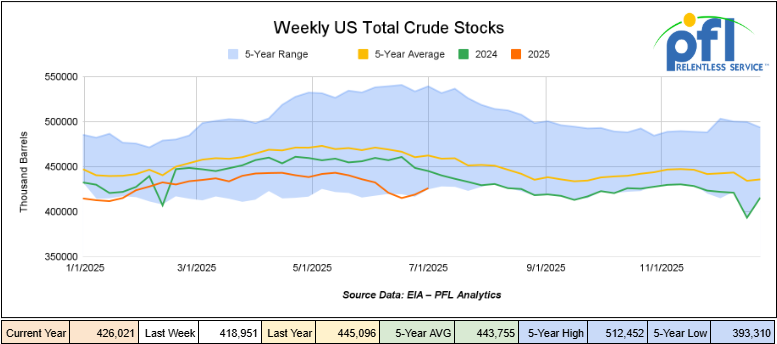

U.S. commercial crude oil inventories (excluding those in the Strategic Petroleum Reserve) increased by 7.1 million barrels week-over-week. At 426 million barrels, U.S. crude oil inventories are 8% below the five-year average for this time of year.

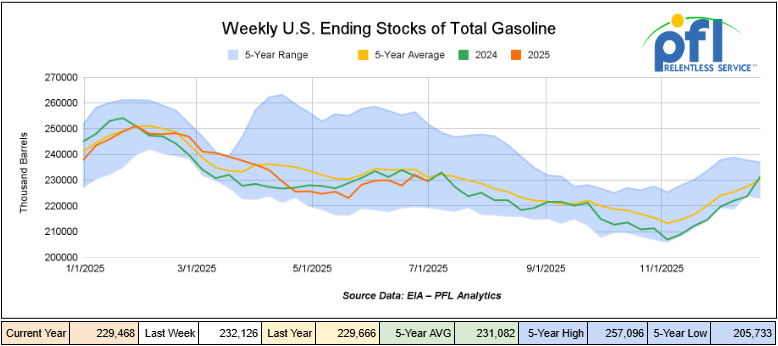

Total motor gasoline inventories decreased by 2.7 million barrels week-over-week and are 1% below the five-year average for this time of year.

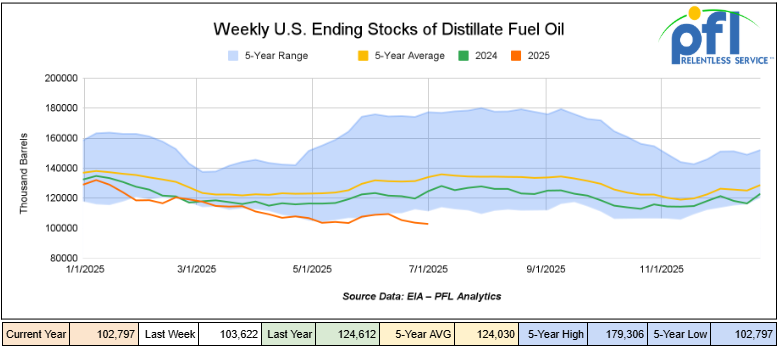

Distillate fuel inventories decreased by 800,000 barrels week-over-week and are 23% below the five-year average for this time of year.

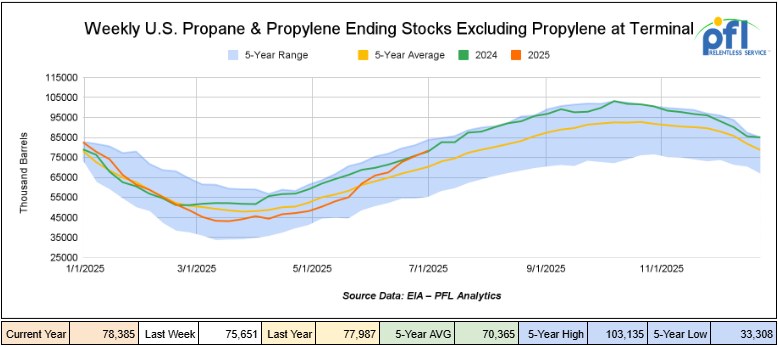

Propane/propylene inventories increased by 2.7 million barrels week-over-week and are 12% above the five-year average for this time of year.

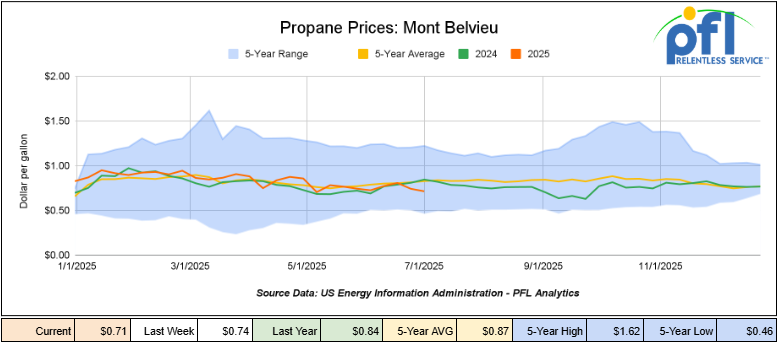

Propane prices closed at 71 cents per gallon on Friday of last week, down 3 cents per gallon week-over-week, and down 13 cents year-over-year.

Overall, total commercial petroleum inventories increased by 6.4 million barrels during the week ending July 4, 2025.

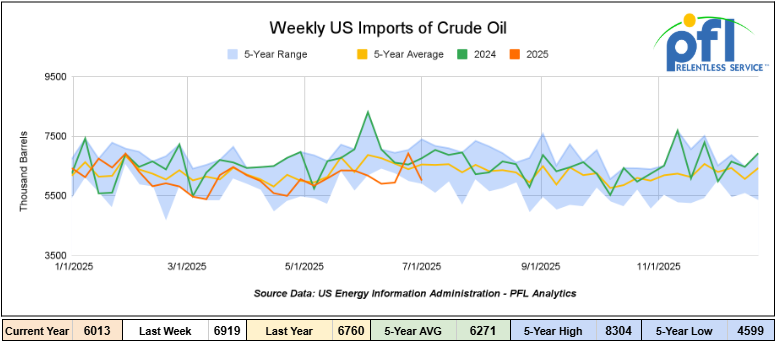

U.S. crude oil imports averaged 6 million barrels per day during the week ending July 4, 2025, a decrease of 906,000 barrels per day week-over-week. Over the past four weeks, crude oil imports averaged 6.1 million barrels per day, 9.6% less than the same four-week period last year. Total motor gasoline imports (including both finished gasoline and gasoline blending components) averaged 832,000 barrels per day, and distillate fuel imports averaged 42,000 barrels per day during the week ending June 27, 2025.

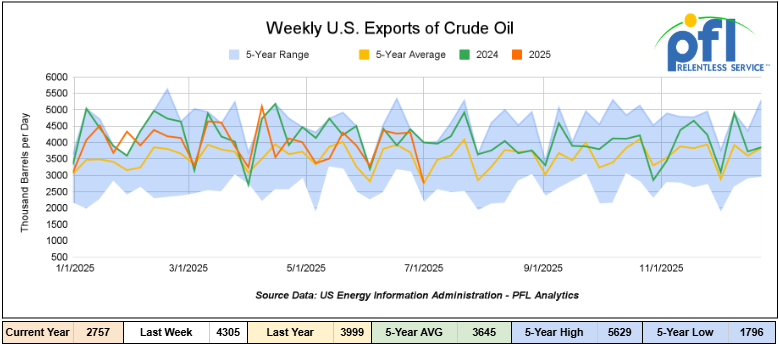

U.S. crude oil exports averaged 2.757 million barrels per day during the week ending July 4, 2025, a decrease of 1.548 million barrels per day week-over-week. Over the past four weeks, crude oil exports averaged 3.923 million barrels per day.

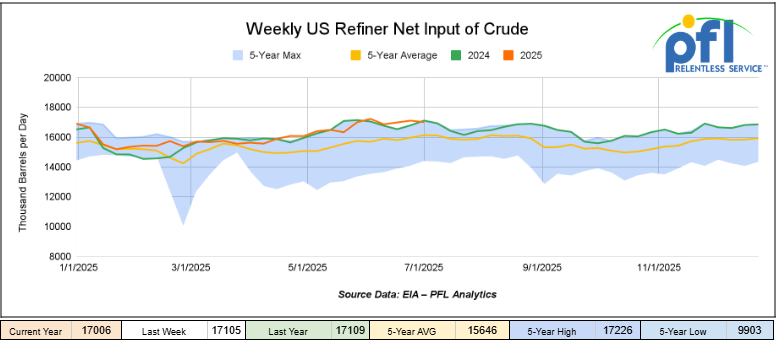

U.S. crude oil refinery inputs averaged 17 million barrels per day during the week ending July 4, 2025, which was 98,000 barrels per day less week-over-week.

WTI is poised to open at $71.40, up $1.04 per barrel from Friday’s close.

North American Rail Traffic

Week Ending July 9, 2025:

Total North American weekly rail volumes were down (-0.05%) in week 28, compared with the same week last year. Total carloads for the week ending on July 9 were 298,370, down (0.99%) compared with the same week in 2024, while weekly intermodal volume was 295,926, up (0.91%) compared to the same week in 2024.

6 of the AAR’s 11 major traffic categories posted year-over-year increases. The largest decrease came from Forest Products, which was down (-16.04%), while the largest increase was from Grain, which was up (+13.68%).

In the East, CSX’s total volumes were down (-1.12%), with the largest decrease coming from Grain (-17.73%), while the largest increase came from Nonmetallic Minerals (+6.34%). NS’s volumes were down (-0.68%), with the largest increase coming from Petroleum and Petroleum Products (+45.05%), while the largest decrease came from Coal (-14.18%).

In the West, BN’s total volumes were up (3.3%), with the largest increase coming from Coal (+16.76%), while the largest decrease came from Chemicals (-8.11%). UP’s total rail volumes were up (+6.54%), with the largest increase coming from Coal (+21.69%), while the largest decrease came from Motor Vehicles and Parts (-7.02%).

In Canada, CN’s total rail volumes were down (-10.58%) with the largest increase coming from Other (+23.58%) while the largest decrease came from Metallic Ores and Metals (-24.36%). CPKCS’s rail volumes were down (-20.76%), with the largest increase coming from Motor Vehicles and Parts (+26.14%), while the largest decrease came from Forest Products (-68.75%).

Source Data: AAR – PFL Analytics

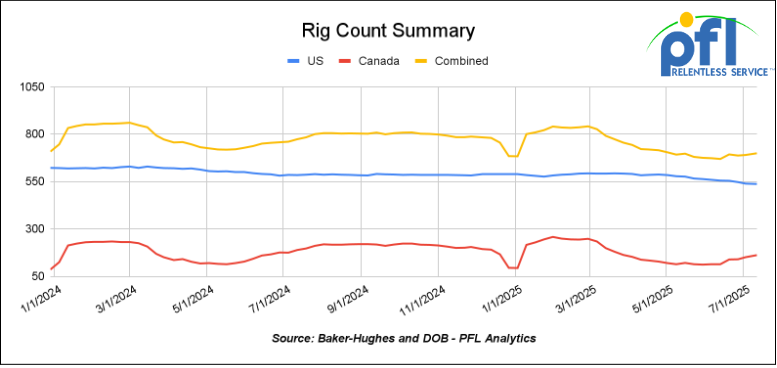

Rig Count

North American rig count was up by 9 rigs week-over-week. U.S. rig count was down -2 rigs week over week and down by -47 rigs year-over-year. The U.S. currently has 537 active rigs. Canada’s rig count was up 11 rigs week-over-week, but down by -27 rigs year-over-year. Canada currently has 162 active rigs. Overall, year-over-year, we are down by -74 rigs collectively.

North American Rig Count Summary

We are watching a few things out there for you:

PFL was at the Calgary Stampede in Canada last week

The Calgary Stampede might be known for rodeos, midway rides, and pancake breakfasts, but if you’ve been there during Stampede week, you know it’s also a serious hotspot for business. In fact, at PFL, we would call it one of the largest rail conferences (if we can call it that) in the industry. All the leasing companies were there, class 1’s, short lines, rail shippers, petrochemical companies, the list goes on. What started back in 1912 as a frontier fair has grown into The Greatest Outdoor Show on Earth — and one of the most high-impact networking weeks in Western Canada.

This year, Curtis Chandler, President of PFL, and David Cohen, VP of Operations of PFL, attended the weeklong event to join the fun and spend time with our Canadian crew in Calgary. PFL made the rounds at receptions, leadership events, and meetups hosted by some of the biggest players in rail, energy, agriculture, and logistics, while sticking in as many one-on-one meetings, breakfasts, and lunches as possible in-between planned events. With so many customers, partners, and decision-makers in one place, it made every hour count.

One Exchange, a company which Curtis Chandler is a founding partner of, hosted an event where PFL customers are always welcome. There was a great turnout this year, with over 500 people attending through the hours of 3:30 PM and 2:00 AM on Monday of last week. Curtis, having deep roots in trading and infrastructure in his former home of Alberta, invited his friend, the Premier of Alberta, who accepted the invitation. See picture below of David, Curtis, and the Alberta Premier, Danielle Smith at the One Exchange Party:

Curtis Chandler, Alberta Premier Danielle Smith, and David Cohen

Source: PFL Analytics

A big thanks to everyone who made time for us in Calgary, traveled to Calgary to meet with us, and attended the OX party. We learned a lot while in Calgary, did some deals and worked on new ones because of the event. For more information on what is going on up in Canada, please call PFL today.

PFL was at the MARS last week

Brian Baker, Vice President of Rail Services, attended this year’s summer MARS conference in Lake Geneva, WI, last week, and it was, as usual, a great event. There were over 650 people in attendance, and it was a great networking opportunity.. There were over 650 people in attendance, and it was a great networking event. With over 650 people in attendance, it was an excellent opportunity to meet with colleagues across the industry. The golf outing was a standout as well — not only a fun way to kick things off, but also a valuable setting to build relationships in a more relaxed environment.

We also appreciated the Economic Update from Dr. Walter Kemmsies, Trade, Logistics & Infrastructure Strategist at The Kemmsies Group, which provided meaningful insights into broader market conditions and global economic factors impacting rail. From the conversations and sessions throughout the event, it’s clear the rail industry remains strong, but there’s also agreement that there’s still plenty of room for improvement across the board to make things more efficient and shipper-friendly. For more information on MARS, give Brian a call at the desk.

We are watching Petroleum Carloads

The four-week rolling average of petroleum carloads carried on the six largest North American railroads fell to 27,840 from 28,326, which was a decrease of -486 rail cars week-over-week. Canadian volumes were mixed. CN’s shipments were higher by +3.0% week over week, CKPC’s volumes were lower by -16.0% week-over-week. U.S. shipments were also mixed. The NS had the largest percentage increase and was up by +5.0%. The CSX had the largest percentage decrease and was down by -13%.

We are watching Trump as Trump Tariffs Target Allies Again

In the latest and greatest, President Trump announced on Thursday of last week, a 35% tariff on most Canadian imports starting August 1. The increase (up from 25%) is aimed at pushing the Canadian government to take stronger action against fentanyl trafficking, which Trump says is entering the U.S. from Canada with little resistance.

Goods covered under the USMCA, along with energy and fertilizer, are exempt. Everything else—from aluminum to consumer goods – will be hit unless Canada steps up enforcement and makes meaningful trade concessions. In a direct letter to Prime Minister Mark Carney, Trump made it clear: talk is cheap. Results matter.

What It Means for Rail:

Canada is the top foreign trading partner by rail. More than $30 billion in freight moves by rail between the U.S. and Canada annually, with key corridors running through Detroit, Chicago, Buffalo, and the Pacific Northwest.

- July Shipping Surge

Importers will likely front-load orders into the U.S. ahead of the August 1 deadline; however, we are already halfway through July as it is. Cross-border rail volumes could spike temporarily – particularly in intermodal, auto parts, and bulk commodities. - Cross-Border Slowdown to Follow

If and when tariffs hit (that is the loaded question in this ever-changing landscape), expect a drop in affected Canadian-origin freight. Unless exemptions expand, these lanes may soften through the fall. - U.S. Manufacturing and Agriculture Benefit

Higher costs on Canadian goods mean more opportunity for domestic suppliers. That spells growth in U.S.-based rail demand, especially from shippers shifting away from imports from Canada. - Railroads Will Adjust

Canadian carriers like CPKC and CN may see short-term declines in U.S.-bound traffic. U.S. railroads could see a boost as domestic and southern lanes pick up.

Most exposed railcar types include intermodal containers, centerbeam flats for lumber (we have already seen a big slowdown in forest products traffic), building materials, and auto racks tied to cross-border vehicle production.

Canada’s Response:

Left-wing Prime Minister Carney has signaled a willingness to negotiate, and in a notable shift, Canada has paused its planned retaliatory tariffs, at least for now. This may be an attempt to keep talks alive, but Trump’s position is firm, and Carney is weak and does not hold very many cards because of his government’s extreme left-wing policies, holding back companies from exploiting Canada’s vast resource base and diversifying its customers base. The latest Trump announcement will hopefully give Canada a jolt in the arm – promote trade within the Canada itself (Canada has trade barriers within their own country among its Provinces that promote north/south trade), diversify its markets, build east – west pipelines, open mining projects, get rid of their version of the green new deal, reduce taxes – the list goes on. Carney has signaled to the Canadian people that he will some of these things such as fast-tracking projects from 4-8 years to 2 years (yet, there are so many projects that have been held up and almost shovel ready – why would these projects take 2 years to review again? what is wrong with 2 months Canada does not have 2 years?). We will wait and see what Carney does, but it seems the investment community in general does not trust him, at least not yet!

Potential Rail Takeaways

- Watch for a volume spike through late July, followed by softening in August on high-tariff lanes.

- U.S. shippers may gain ground as import substitution takes hold.

- Short-term disruption, but long-term realignment could benefit U.S. producers and railroads that are ready to pivot.

With the August 1 tariff deadline approaching, early signs of market repositioning are already visible. Stay tuned to PFL with offices on both sides of the border we are monitoring developments closely.

In other Tariff news, Trump said over the weekend that he will impose a 30% tariff on goods from the European Union and Mexico that will take effect on Aug. 1.

Trump revealed the new rates in letters to European Commission President Ursula von der Leyen and Mexico’s President Claudia Sheinbaum, which he posted on his social media site, Truth Social, this past Saturday

“Mexico has been helping me secure the border, BUT, what Mexico has done, is not enough,” Trump wrote to Sheinbaum.

Trump said that there will not be tariffs on goods from the EU if the 27-member bloc, “or companies within the EU, decide to build or manufacture products within the United States,” he wrote.

He said that if the EU or Mexico retaliates with higher tariffs, “then, whatever the number you choose to raise them by, will be added on to the 30% that we charge.”

In response, EU chief Ursula von der Leyen said the bloc was ready to take all “necessary” steps to safeguard its economic interests, after US President Donald Trump announced that he would impose 30% tariffs on all EU goods. It looks as though the Europeans are preparing to retaliate, but are working toward the August 1, 2025 deadline.

Looks as though it is going to be one heck of a week in the markets with the President promising to make new announcements on Russia, as his patience is wearing thin on the Russian Ukrainian war where Putin is refusing to negotiate a peace deal! Stay tuned to PFL for further developments.

We are Watching the Surface and Transportation Board

Bad news for shippers -a federal court has tossed out the Surface Transportation Board’s (“STB”) 2024 reciprocal switching rule that would have allowed shippers who suffer from inadequate rail service to gain access to a second railroad.

The STB exceeded its authority when it adopted the rule, the U.S. Court of Appeals for the Seventh Circuit said in a decision issued on Wednesday of last week.

The rule arose out of the 2022 service crisis that was related to widespread crew shortages on the big four U.S. railroads. The board said the rule would provide a streamlined path for access to reciprocal switching when service to a terminal-area shipper fails to meet any one of three performance standards.

CSX, CN, and UP brought the lawsuit challenging the rule. The railroads had argued that the rule would have negative consequences for industry and shippers alike. A forced switching order, they said, would require alternative service that is more operationally and economically complex than existing service.

The court agreed that the board’s rule was inconsistent with the Staggers Act of 1980, which largely deregulated the rail industry. “The Board exceeded its statutory authority because the Final Rule, by its terms, deviates from the statutory standards Congress established authorizing reciprocal switching,” the three-judge panel said.

The decision, however, did not overturn the board’s requirement that the Class I railroads provide expanded service performance metric reports every week. “We refrain from deciding today whether the disclosure requirements, as written, exceed the agency’s statutory authority,” the court said.

We are Watching Economic Indicators

Consumer Spending

In May 2025, total consumer spending adjusted for inflation increased by 0.3% over April 2025, slightly improving from the 0.2% gain in April. This modest increase suggests a slight rebound in consumer confidence despite ongoing economic uncertainties. According to the U.S. Bureau of Economic Analysis, the increase in current-dollar personal consumption expenditures (PCE) was $48.5 billion, driven by a $56.2 billion rise in services spending, partially offset by a $7.7 billion decline in goods spending.

The personal saving rate rose to 5.1% in May, up from 4.9% in April, continuing its upward trend and indicating that consumers remain cautious, prioritizing savings amid inflationary pressures and trade-related uncertainties.

Year-over-year, the PCE price index rose by 2.0%, down from 2.1% in April, signaling continued moderation in consumer inflation, but still above the Federal Reserve’s 2% target.

Other reports suggest that we could be in for some headwinds. While consumer spending remains pretty good, consumer borrowing tanked in May, which is potentially bad news for an economy that runs on consumption. After a one-off surge in April, consumer borrowing tanked again in May, a sign that Americans might be close to tapping out as they hit their credit card limits. There was a surge in borrowing in April as consumers tried to get ahead of potential tariff costs, but it appears this was an outlier. Consumer debt grew by just 1.2 percent ($5.1 billion) in May as revolving credit contracted, according to the latest data from the Federal Reserve. This returns to the trend of declining borrowing that began at the beginning of the year. The Federal Reserve consumer debt figures include credit card debt, student loans, and auto loans, but do not factor in mortgage debt. When you include mortgages, U.S. households are buried under a record level of debt. As of the end of Q1 2025, total household debt stood at $18.2 trillion. Americans currently owe $1.3 trillion in revolving credit, which is primarily made up of credit card debt. If spending wanes in the days to come, that will be bad news for everything, including rail. Stay tuned to PFL, we are watching this one closely.

Lease Bids

• 30-50, 6000cf Hopper Steel located off of CSX or NS in East. For use in petcoke service. Period: 5 Years.

• 50, 5000CF Hopper Covered located off of UP or BN in Houston. For use in Fertilizer service. Period: 6 Months. Bid: Negotiable.Needed ASAP.

• 10, 2500CF Hopper Open Top located off of UP or BN in Texas. For use in aggregate service. Period: 5 years. Bid: Negotiable.Need Rapid Discharge Doors.

• 20, 25.5k Tank CPC 1232 located off of UP, BN, CSX, NS in OK, TX, Northeast. For use in Asphalt service. Period: 3 Years. Bid: Negotiable.

• 10, 25.5K Tank Any Type located off of CSX in Florida. For use in UCO service. Period: 2 Years. Bid: Negotiable.

• 100, 30K Tank 117J located off of BN in Montana. For use in Crude service. Period: 2 years. Bid: Negotiable.

• 20, 30K Tank 117J located off of UP or BN in Midwest. For use in Ethanol service. Period: 5 Years. Bid: Negotiable.

• 15, 29K Tank 117R located off of NS or CSX in Ohio. For use in Ply Oil service. Period: 6-12 Months. Bid: Negotiable.

• 10, 30K Tank 117R or 117J located off of Any Class 1 in USA. For use in Glycerin service. Period: 1 year. Bid: Negotiable.

• 50, 23.5-25.5 Tank DOT111 located off of Any Class 1 in USA. For use in Asphalt service. Period: 5 years. Bid: Negotiable.

• 10, 25.5K Any Type Tank located off of Any Class 1 in Any Location. For use in Asphalt service. Period: 3-12 months. Bid: Negotiable.

• 100, 33K Tank 117J located off of BN or UP in Bellview. For use in Butane/ service. Period: Sept-March. Bid: Negotiable.

• 4, 30K Tank 117J located off of in Michigan. For use in Food Grade Ethanol service. Period: Multi year. Bid: Negotiable.

Sales Bids

• 28, 3400CF located off of UP BN in Texas. For use in Cement service. Bid: Negotiable.Cement Gates needed.

• 20, 17K DOT111 located off of various class 1s in various locations. For use in corn syrup service.

Lease Offers

• 60, 4750 Covered Hoppers located off of UP or BN in Eads, CO. Last used in Grain. Offer: Negotiable. UP to 5 Years, 3 Hopper, Gravity Gate, Trough Hatches.

• 100, 6250 Hoppers located off of UP in US. Last used in DDG. Offer: Negotiable. 1 Year term. Dirty to Dirty. Free move on UP..

• 50, 29K Tanks located off of CN in Hamilton, ON. Last used in Biodiesel. Offer: Negotiable. 1 year +.

• 20, 30K Tanks located off of BNSF in West Texas. Last used in Ethanol. Offer: Negotiable. 1 year minimum.

• 24, 25.5K-30K Tanks located off of UP or BN in Texas. Last used in Base Oils. Offer: Negotiable. 1-2 Year.

• 25, 19.6K Tanks located off of UP in US. Last used in Molases. Offer: Negotiable.

• 10, 30K Tanks located off of CN in Wisconsin. Last used in Gasoline. Offer: Negotiable. Multiyear.

• 33, 30K Tanks located off of UP in Gulf. Last used in Clean. Offer: Negotiable. Multiyear.

• 50, 30K Tanks located off of UP in Gulf. Last used in Diesel. Offer: Negotiable. Multiyear.

• 120, 29.8K Tanks located off of CPKC in MN. Last used in Ethanol. Offer: Negotiable.

• 50, 20K Tanks located off of UP or BN in Wichita Falls, TX. Last used in HCL. Offer: Negotiable.

• 50, 30K Tanks located off of CSX, NS, or CN in Detroit. Last used in Diesel. Offer: Negotiable. Multiyear.

Sales Offers

• 21, 50′ Boxcar Plate Cs located off of various class 1s in NM. Offer: Negotiable. End of Life.

• 3, 50′ Boxcar Plate Cs located off of various class 1s in multiple locations. Offer: Negotiable. End of Life.

• 27, 50′ Boxcar Plate Cs located off of various class 1s in PQ. Offer: Negotiable. End of Life.

• 100, 3250 Covered Hopper s located off of various class 1s in multiple locations. Offer: Negotiable. Sand Cars.

• 5, 2740 Gondola Mills located off of various class 1s in NC. Offer: Negotiable. End of Life.

• 1, 2260 Gondola Mills located off of various class 1s in AL. Offer: Negotiable. End of Life.

• 30, 2740 Gondola Mills located off of various class 1s in multiple locations. Offer: Negotiable. End of Life.

• 21, 2740 Gondola Mills located off of various class 1s in WA. Offer: Negotiable. End of Life.

• 9, 4750 Covered Hopper N/As located off of various class 1s in multiple locations. Offer: Negotiable. End of Life.

• 5, 4750 Covered Hopper N/As located off of various class 1s in multiple locations. Offer: Negotiable. End of Life.

• 50, 31.8K Tank CPC 1232s located off of UP or BN in TX. Offer: Negotiable. Requal Due in 2025.

Call PFL today to discuss your needs and our availability and market reach. Whether you are looking to lease cars, lease out cars, buy cars, or sell cars call PFL today at 239-390-2885

Live Railcar Markets

| CAT | Type | Capacity | GRL | QTY | LOC | Class | Prev. Use | Offer | Note |

|---|

PFL will be at the Following Conferences

- Where: Calgary

- Attending: David Cohen (954-729-4774), Curtis Chandler(239-405-3365), Cyndi Popov (403-402-5043)

- Where: Grand Geneva Resort

- Attending: Brian Baker (239.297.4519)

- Conference Website

- Where: Loews Arlington Hotel

- Attending: Brian Baker (239.297.4519), David Cohen (954-729-4774), and Curtis Chandler (239-405-3365)

- Conference Website

- Where: The Westin Galleria Dallas

- Attending: David Cohen (954-729-4774), and Curtis Chandler (239-405-3365)

- Conference Website

- Where: The Westin Galleria Dallas

- Attending: Brian Baker (239.297.4519)

- Conference Website