“There’s a beauty to wisdom and experience that cannot be faked. It’s impossible to be mature without having lived.”

– Amy Grant

Jobs Update

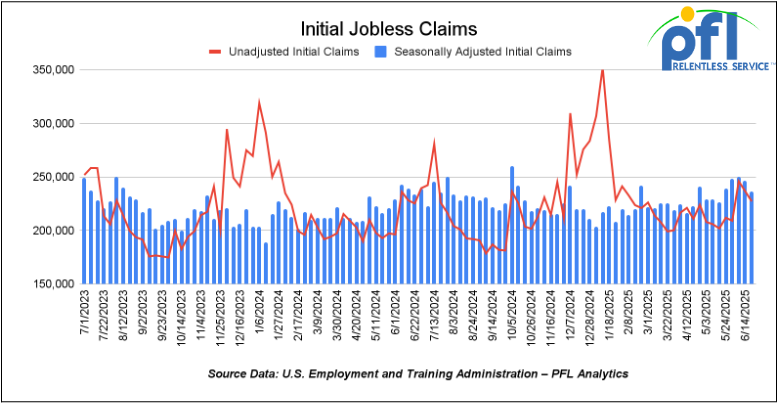

- Initial jobless claims seasonally adjusted for the week ending June 21 came in at 236,000, down 10,000 people week over week week-over-week

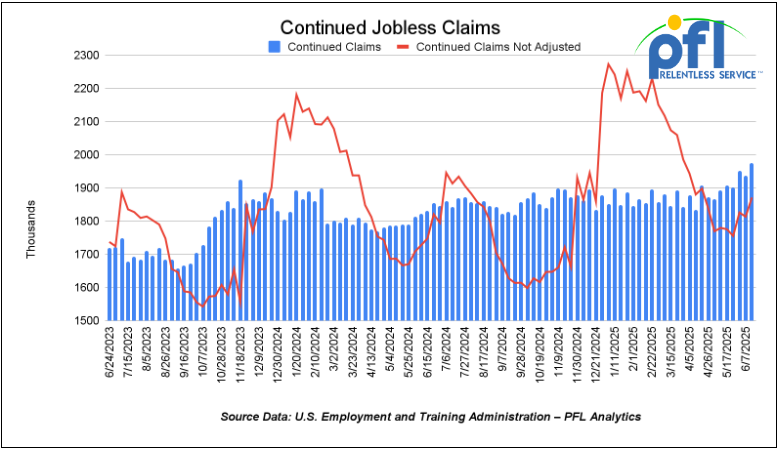

- Continuing jobless claims came in at 1.974 million people, versus the adjusted number of 1.937 million people from the week prior, up 37,000 people week-over-week.

Stocks closed higher on Friday of last week and higher week-over-week

The DOW closed higher on Friday of last week, up 432.43 points (1%), closing out the week at 43,819.27, up 1,612.45 points week-over-week. The S&P 500 closed higher on Friday of last week, up 32.05 points, and closed out the week at 6,173.07 up 205.23 points week-over-week. The NASDAQ closed higher on Friday of last week, up 105.54 points, and closed out the week at 20,273.46, up 826.05 points week-over-week.

In overnight trading, DOW futures traded higher and are expected to open at 44,324 this morning up 199 points from Friday’s close.

Crude oil closed higher on Friday of last week, but lower week-over-week.

West Texas Intermediate (WTI) crude closed up $0.28 per barrel (0.4%), to close at $65.52 per barrel on Friday of last week, but down $9.41 per barrel week-over-week. Brent crude closed up $0.04 USD per barrel (0.1%) on Friday of last week, to close at $67.77 per barrel, down -$9.24 cents per barrel week-over-week.

One Exchange WCS (Western Canadian Select) for August delivery settled on Friday of last week at US$9.95 below the WTI-CMA (West Texas Intermediate – Calendar Month Average). The implied value was US$53.50 per barrel.

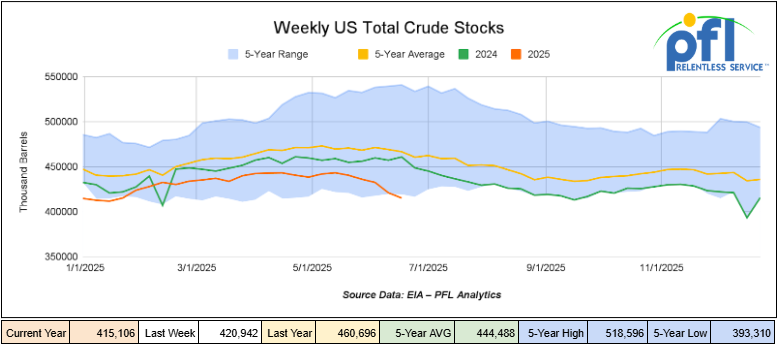

U.S. commercial crude oil inventories (excluding those in the Strategic Petroleum Reserve) decreased by 5.8 million barrels week-over-week. At 415.1 million barrels, U.S. crude oil inventories are 11% below the five-year average for this time of year.

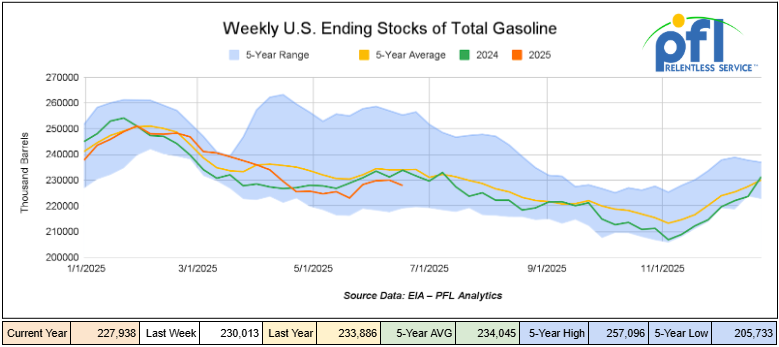

Total motor gasoline inventories decreased by 2.1 million barrels week-over-week and are 3% below the five-year average for this time of year.

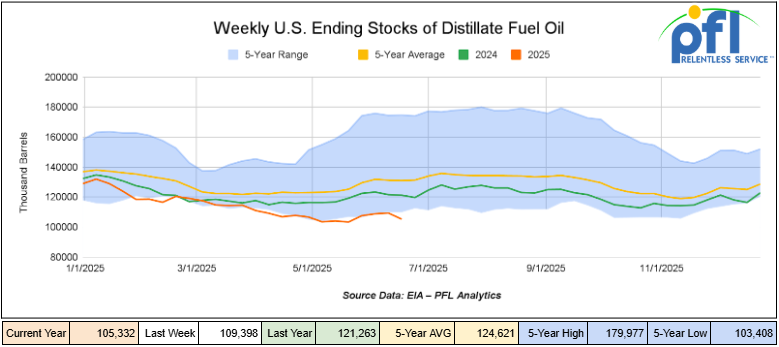

Distillate fuel inventories decreased by 4.1 million barrels week-over-week and are 20% below the five year average for this time of year.

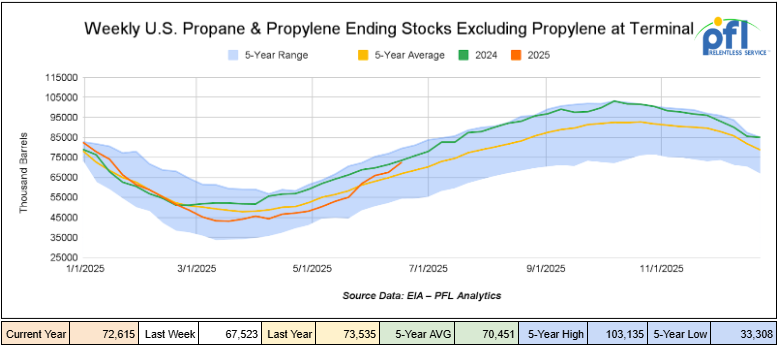

Propane/propylene inventories increased by 5.1 million barrels week-over-week and are 9% above the five-year average for this time of year.

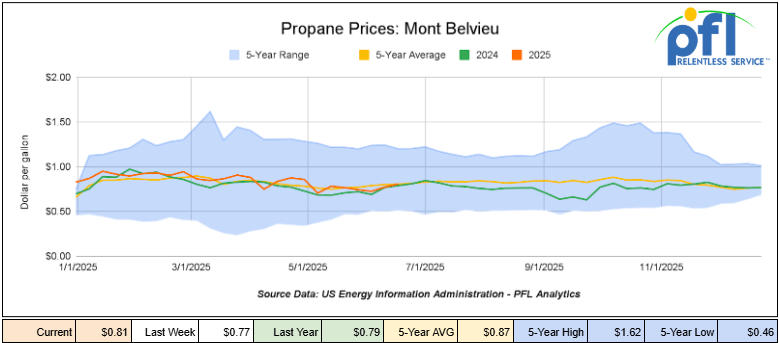

Propane prices closed at 81 cents per gallon on Friday of last week, up 4 cents per gallon week-over-week, and up 2 cents year-over-year.

Overall, total commercial petroleum inventories decreased by 4.2 million barrels last week during the week ending June 20, 2025.

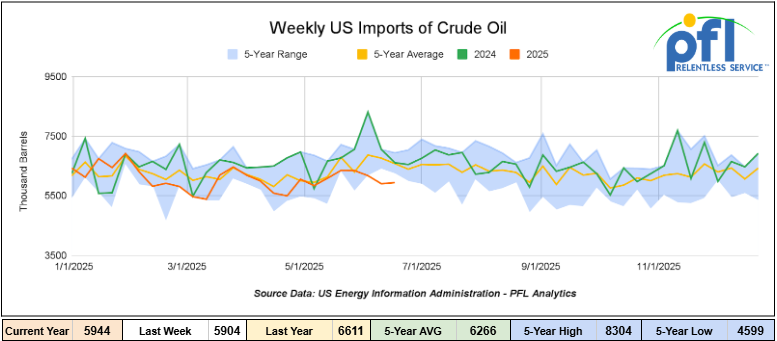

U.S. crude oil imports averaged 5.9 million barrels per day last week, increased by 439,000 barrels per day week-over-week. Over the past four weeks, crude oil imports averaged 6 million barrels per day, 17.4% less than the same four-week period last year. Total motor gasoline imports (including both finished gasoline and gasoline blending components) averaged 1.007 million barrels per day, and distillate fuel imports averaged 73,000 barrels per day during the week ending June 20, 2025.

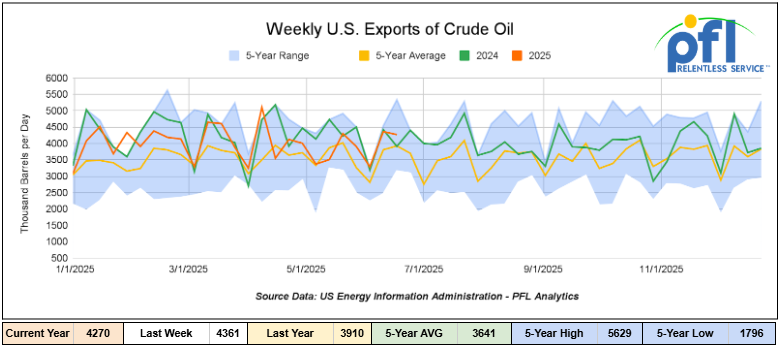

U.S. crude oil exports averaged 4.27 million barrels per day during the week ending June 20, 2025, a decrease of 91,000 barrels per day week-over-week. Over the past four weeks, crude oil exports averaged 3.956 million barrels per day.

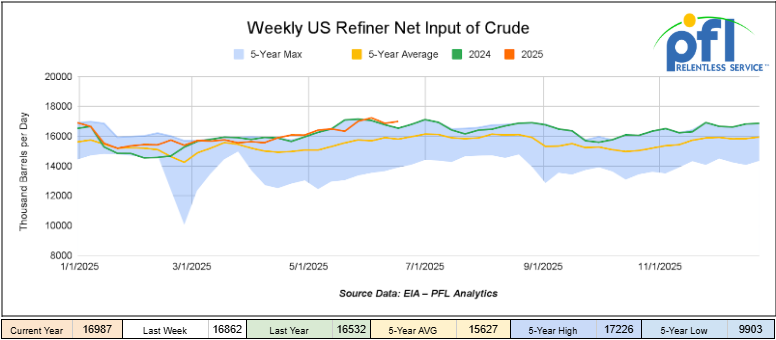

U.S. crude oil refinery inputs averaged 17 million barrels per day during the week ending June 20, 2025, which was 125,000 barrels per day more week-over-week.

WTI is poised to open at $65.31, down 21 cents per barrel from Friday’s close.

North American Rail Traffic

Week Ending June 25, 2025.

Total North American weekly rail volumes were down (-1.05%) in week 26, compared with the same week last year. Total carloads for the week ending on June 25 were 326,998, up (3%) compared with the same week in 2024, while weekly intermodal volume was 312,611, down (-4.95%) compared to the same week in 2024.

6 of the AAR’s 11 major traffic categories posted year-over-year increases. The largest decrease came from Forest Products, which was down (-14.4%), while the largest increase was from Grain, which was up (+18.28%).

In the East, CSX’s total volumes were down (-0.05%), with the largest decrease coming from Coal (-10.01%), while the largest increase came from Grain (+43.53%). NS’s volumes were down (-2.57%), with the largest increase coming from Petroleum and Petroleum Products (+23.68%), while the largest decrease came from Coal (-7.59%).

In the West, BN’s total volumes were down (-2.69%), with the largest increase coming from Petroleum and Petroleum Products (+16.12%), while the largest decrease came from Metallic Ores and Metals (-27.37%). UP’s total rail volumes were up (+11.7%), with the largest increase coming from Grain (+36.02%), while the largest decrease came from Intermodal (-5.63%).

In Canada, CN’s total rail volumes were up (+5.74%) with the largest increase coming from Grain (+126.3%) while the largest decrease came from Other (-13.5%). CPKCS’s rail volumes were down -19.25%, with the largest increase coming from Coal (+33.45%), while the largest decrease came from Forest Products (-68.39%).

Source Data: AAR – PFL Analytics

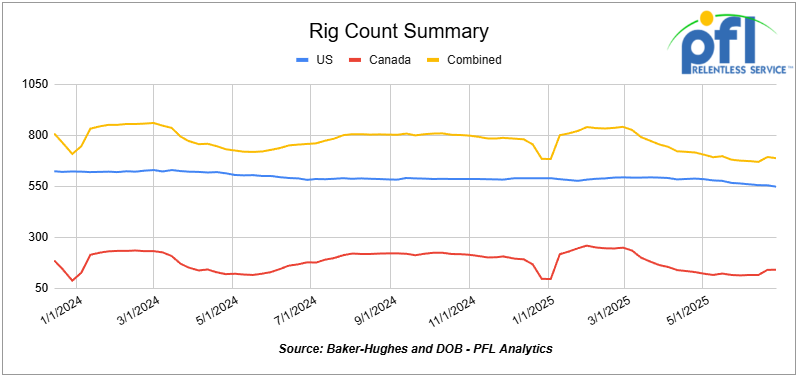

Rig Count

North American rig count was down by -6 rigs week-over-week. U.S. rig count was down -7 rigs week over week and down by -34 rigs year-over-year. The U.S. currently has 547 active rigs. Canada’s rig count was up 1 rigs week-over-week, but down by -36 rigs year-over-year. Canada currently has 140 active rigs. Overall, year-over-year, we are down by -70 rigs collectively.

North American Rig Count Summary

We are watching a few things out there for you:

We are Watching Trump and the U.S. Trade Deals

On Friday of last week, Trump said he was terminating trade talks with Canada, ‘effective immediately’. The reason is Canada is proceeding with a digital services tax that would apply to several major U.S. tech companies. He said: “Based on this egregious Tax, we are hereby terminating ALL discussions on Trade with Canada, effective immediately,” Trump wrote on Truth Social. “We will let Canada know the Tariff that they will be paying to do business with the United States of America within the next seven-day period.”

The President’s Canada post refers to a digital services tax set to go into effect on June 30. That measure would tax multinational tech companies for revenue collected – for example from advertising – from providing services to Canadian users. Several European countries have imposed similar taxes.

Earlier this month, Canada’s Finance Minister François-Philippe Champagne said the country would move forward with the tax, despite U.S. opposition. As of this morning, Canada is rescinding its digital services tax in a bid to save trade talks with the US.

Meanwhile, the United States and China have reached an agreement deescalating trade tensions. But, details are scarce, and the latest pact leaves major issues between the world’s two biggest economies unresolved.

President Trump said late Thursday of last week that a deal with China had been signed “the other day.’’ China’s Commerce Ministry confirmed Friday of last week that some type of arrangement had been reached but offered few details about it.

Lastly, the U.S. and EU are confident they will reach a tariff deal by the July deadline. Stay tuned to PFL for the latest and greatest on trade deals – we are watching this closely – supply chains – logistics and rail are sure to be impacted in a positive or negative way depending on the outcome(s) fingers crossed for good deals!

We attended Caltrax Golf Tournament in Calgary last week

Hats off to the folks at Caltrax! PFL proudly took part in the Iron Rail Invitational Charity Golf Tournament, hosted by Caltrax at Calgary’s Inglewood Golf & Curling Club. The event brought together rail industry colleagues from across Canada and the U.S. for a day of golf, networking, and giving back — all in support of KidSport Calgary & Area, a charity that helps kids access organized sports by removing financial barriers.

PFL was pleased to sponsor a hole at the event, with Cyndi Popov representing the company on the course. Strong turnout (144 golfers), beautiful weather, and great conversation made for a memorable day all in support of a fantastic cause!

Cyndi on Hole #7

Source PFL: PFL Analytics

We look forward to taking part again next year!

We are watching Petroleum Carloads

The four-week rolling average of petroleum carloads carried on the six largest North American railroads rose to 28,195 from 27,847 which was an increase of +348 rail cars week-over-week. Canadian volumes were mixed. CPKC’s shipments were lower by -6.0% week over week, CN’s volumes were higher by +2.0% week-over-week. U.S. shipments were mostly higher. The BN had the largest percentage increase and was up by +24.0%. The NS was the sole decliner and was down by -1.0%

We are watching Canadian Crude by Rail

Crude by rail out of Canada decreased month over month. The Canadian Energy regulator reported late evening on June 18, that 76,866 barrels were exported per day during the month of April 2025, down from 77,520 barrels in March of 2025, a decrease of 654 barrels per day, month over month.

Crude by rail will always be necessary out of Canada for stranded oil not connected by pipelines and raw bitumen shipped as a non-haz product which is not able to flow in pipelines and is competitive with pipeline tolls is a growing market to keep an eye on. Other factors would be existing long term contractual commitments and basis -we really need to see basis the WTI-CMA (West Texas Intermediate – Calendar Month Average) blow out to -17 per barrel for sustained periods of time to make economic sense. That may come sooner than we think as Canadian producers are resilient and we are seeing more production than anticipated and pipelines are getting fuller sooner than expected. In the short term – there has been quite a few turnarounds, wild fires and maintenance that has limited production. Stay tuned to PFL for further details.

We are watching Key Economic Indicators

Consumer Confidence

The Conference Board’s Index of Consumer Confidence decreased to 93 in June 2025, down from 98.5 in May.

The University of Michigan’s Index of Consumer Sentiment increased to 60.5 in June, up from 52.2 in May.

Lease Bids

- 10, 2500CF Open Top Hoppers needed off of UP or BN in Texas for 5 years. Cars are needed for use in aggregate service. Need Rapid Discharge Doors

- 50, 5000CF Covered Hoppers needed off of UP or BN in Houston for 6 Month. Cars are needed for use in Fertilizer service. Needed ASAP

- 30-50, 6000cf Steel Hoppers needed off of CSX or NS in East for 5 Year. Cars are needed for use in petcoke service.

- 50, 23.5-25.5 DOT111 Tanks needed off of Any Class 1 in USA for 5 years. Cars are needed for use in Asphalt service.

- 20, 25.5k CPC 1232 Tanks needed off of UP, BN, CSX, NS in OK, TX, Northeast for 3 Year. Cars are needed for use in Asphalt service.

- 10, 30K 117R or 117J Tanks needed off of Any Class 1 in USA for 1 year. Cars are needed for use in Glycerin service.

- 15-20, 29K 117R Tanks needed off of NS or CSX in Ohio for 6-12 Months. Cars are needed for use in Ply Oil service.

- 20, 30K 117J Tanks needed off of UP or BN in Midwest for 5 Years. Cars are needed for use in Ethanol service.

- 100, 30K 117J Tanks needed off of BN in Montana for 2 years. Cars are needed for use in Crude service.

- 10, 25.5K Any Type Tanks needed off of CSX in Florida for 2 Years. Cars are needed for use in UCO service.

- 10, 25.5K Any Type Tanks needed off of Any Class 1 in Any Location for 3-12 months. Cars are needed for use in Asphalt service.

- 6, 30K 117R or 117J Tanks needed off of Any Class 1 in USA for 1 year. Cars are needed for use in Av Gas service.

- 10, 25.5K-30K 117R or 117J Tanks needed off of UP or BN in Texas for 1 year. Cars are needed for use in Dicyclopentadiene service.

- 70, 30K DOT 117R/ DOT 117J Tanks needed off of UP in Corpus Christi for 5 Year. Cars are needed for use in Gasoline service.

- 20, 28.3K 117J Tanks needed off of BN in Montana for 2 years. Cars are needed for use in Crude service.

Sales Bids

- 28, 3400CF Covered Hoppers needed off of UP BN in Texas. Cars are needed for use in Cement service. Cement Gates needed.

- 20, 17K DOT111 Tanks needed off of various class 1s in various locations. Cars are needed for use in corn syrup service.

Lease Offers

- 60, 4750, Covered Hoppers located off of UP or BN in Eads, CO. Cars are clean UP to 5 Years, 3 Hopper, Gravity Gate, Trough Hatches

- 100, 6250, Covered Hoppers located off of UP in US . Cars were last used in DDG. 1 Year term. Dirty to Dirty. Free move on UP.

- 50, 33K, 400W Pressure Tanks located off of All Class 1s in US and Canada. Cars were last used in Propane. Summer or Longer Lease Available.

- 50, 29K , DOT 111 Tanks located off of CN in Hamilton, ON. Cars were last used in Biodiesel. 1 year +

- 20-25, 30K, 117J Tanks located off of BNSF in West Texas. Cars were last used in Ethanol. 1 year minimum

- 24, 25.5K-30K, DOT 111 Tanks located off of UP or BN in Texas. Cars were last used in Base Oils. 1-2 Year

- 25-50, 19.6K, DOT 111 Tanks located off of UP in US. Cars were last used in Molases .

- 10, 30, 117R Tanks located off of CN in Wisconsin. Cars were last used in Gasoline. Multiyear

- 33, 30, 117R Tanks located off of UP in Gulf. Cars are clean Multiyear

- 50, 30, 117R Tanks located off of UP in Gulf. Cars were last used in Diesel. Multiyear

- 120, 29.8K, 117R/117J Tanks located off of CPKC in MN. Cars were last used in Ethanol.

- 50, 20K, DOT 111 Tanks located off of UP or BN in Wichita Falls, TX. Cars were last used in HCL.

- 50-100, 117R/117J Tanks located off of CN, CP, UP, CSXT in Various. Cars were last used in Biodiesel. Summer – 4 months

- 50-100, 117R/117J Tanks located off of CN, CP, UP, CSXT in Various. Cars were last used in Diesel . Summer – 4 months

Sales Offers

- 21, 50′, Plate C Boxcars located off of various class 1s in NM. End of Life

- 3, 50′, Plate C Boxcars located off of various class 1s in multiple locations. End of Life

- 27, 50′, Plate C Boxcars located off of various class 1s in PQ. End of Life

- 100-300, 3250, Covered Hoppers located off of various class 1s in multiple locations. Sand Cars

- 5, 2740, Mill Gondolas located off of various class 1s in NC. End of Life

- 1, 2260, Mill Gondolas located off of various class 1s in AL. End of Life

- 30, 2740, Mill Gondolas located off of various class 1s in multiple locations. End of Life

- 21, 2740, Mill Gondolas located off of various class 1s in WA. End of Life

- 15, 4750, Covered Hoppers located off of various class 1s in multiple locations. End of Life

- 5, 4750, Covered Hoppers located off of various class 1s in multiple locations. End of Life

- 50-100, 31.8K, CPC 1232 Tanks located off of UP or BN in TX. Requal Due in 2025

Call PFL today to discuss your needs and our availability and market reach. Whether you are looking to lease cars, lease out cars, buy cars, or sell cars call PFL today at 239-390-2885

Live Railcar Markets

| CAT | Type | Capacity | GRL | QTY | LOC | Class | Prev. Use | Offer | Note |

|---|

PFL will be at the Following Conferences

- Where: Calgary

- Attending: David Cohen (954-729-4774), Curtis Chandler(239-405-3365), Cyndi Popov (403-402-5043)

- Where: Grand Geneva Resort

- Attending: Brian Baker (239.297.4519)

- Conference Website

- Where: Loews Arlington Hotel

- Attending: Brian Baker (239.297.4519), David Cohen (954-729-4774), and Curtis Chandler (239-405-3365)

- Conference Website

- Where: The Westin Galleria Dallas

- Attending: David Cohen (954-729-4774), and Curtis Chandler (239-405-3365)

- Conference Website

- Where: The Westin Galleria Dallas

- Attending: Brian Baker (239.297.4519)

- Conference Website